Chapter 17 – Investment Companies 6th Edition

1. Mutual Fund Balance Sheets and Recent Trends

a. Long-Term Funds

In 2013 equity investments were 55.5% of total funds invested in long term funds (Table

17-7). This percent has yet to recover to precrisis levels. Investments in corporate and

foreign bonds comprised 18.4%, and U.S. government and agency securities made up

14.7%., while municipal investments were 6.3%. The percentages of debt and equity

however can vary widely over different market conditions. Market timing funds (also

called asset allocation funds) are designed to vary the amount of money in the different

asset classes according to forecasts of performance. During the financial crisis assets fell

from $7,829 billion in 2007 to $5,435.3 billion in 2008, a drop of almost 31%. By 2010

assets recovered to $6,783.1 billion and in 2013 rose to $10,221.8 billion.

The SEC does not limit 12b-1 fees but FINRA does. The annual management fee, which

may be termed ‘ongoing sales fees,’ is capped at 0.75%. The SEC has proposed that the

fee be terminated once an investor had paid the equivalent to the load charged on classes

of mutual fund shares that pay a front end load. If for example the shares with a front end

load paid a5% load charge, the management fee portion of the 12b-1 assessed on other

fund classes must be terminated when the investor’s total payment is equivalent to a 5%

front end load.

b. Money Market Funds

In 2013 MMMFs held 14.0% in open market paper, 31.3% in Treasuries and agencies,

12.2% in municipals and 17.7% in repos. Money market funds currently maintain a

constant NAV of $1.00, although the FSOC has proposed mandating that MMMF shares

fluctuate similar to long term mutual funds. Currently though, as interest is earned an

investor is credited with more shares. Money funds increased safety of their investments

during the financial crisis, increasing holdings of U.S. government securities from 13.6%

in 2007 to 35.5% in 2008. Investments in both remain high.

2. Mutual Fund Regulation

The SEC is the primary regulator of mutual funds. The major acts regulating mutual

funds include the banking and securities acts of 1933 and 1934 and the Investment

Company Act of 1940. These laws require mutual funds to meet disclosure requirements

similar to public issues of debt and equity, and introduced many anti-fraud procedures

and limits on fees. Newer laws such as the Insider Trading and Securities Fraud

Enforcement Act of 1988 required funds to develop mechanisms to avoid insider trading

abuses and the Market Reform Act of 1990 allowed the SEC to introduce circuit

breakers. More recently, the National Securities Markets Improvements Act (NSMIA)

of 1996 exempts mutual fund sellers from most state oversight.

Ethical problems in the mutual fund industry

Four main categories of trading abuses have been identified:

1. Market timing: Allowing selected traders, typically fund managers, to buy mutual

fund shares and then sell them in a short time period, usually the next day to

exploit prices changes in holdings in overseas markets.

2. Late trading: This consists of allowing certain investors to be able to buy or sell

17-1

Chapter 17 – Investment Companies 6th Edition

mutual fund shares after close of trading at 4:00 PM EST. Recall the NAV is set

for the day at that time. As new information comes out, investors can profitably

set up trades based on the new info that is not yet incorporated into the fund NAV.

Late trading and market timing allow certain classes of investor to unfairly profit

at the expense of longer term investors.

3. Diluted brokerage arrangements: A form of ‘directed order flow.’ In this practice

mutual fund managers used certain brokers when they decide to buy and sell

shares held in the mutual fund. In exchange for this, the brokers agree to advise

their own clients to purchase that mutual fund, regardless of whether that was the

best fund for that particular client. This is a form of soft dollar kickback.

4. Some brokers allegedly duped investors into purchasing shares with 12b-1 plans,

a form of load charge, by telling the investors the fund had no load. Some funds

and fund families also provided discounts to qualified customers. In some cases,

the brokers did not realize (or just did not tell) the customers they qualified for a

discount and overcharged the customers.

New rules that resulted from the abuses:

In general the new rules are designed to increase disclosure about potential conflicts of

interest, close legal loopholes abused by managers and increase oversight and

independence of fund boards. The minimum percentage of independent board members

was increased from 50% to 75%. Recall that under Sarbanes-Oxley at least one board

member must have accounting expertise and knowledge of GAAP. The SEC also now

requires senior executives of funds to report all trading in funds, not just trading in

individual stocks. Client trades and holdings must also be held confidential (they had

been revealed to other fund managers).

1. Rules on market timing: Firms must promulgate and disclose methods to limit

frequent trading. Firms must disclose whether they are using ‘fair value pricing’

(FVP). FVP is a method to update securities prices where the last price quote is

‘stale’ or out of date by several hours or more. This is important for funds holding

stocks that trade in overseas markets.

2. To limit improper directed order flow, brokers are required to disclose to

customers any tie in arrangements with specific funds. These are defacto conflicts

of interest and should be disclosed.

3. As of October 2004 all funds must have a chief compliance officer (CCO) that

answers to the board. The CCO’s duties include policing personal trading by fund

managers, monitoring allocations of trades and commission, ensuring accurate

information disclosure and reporting wrongdoing to the board.

4. Shareholder reports must discloser all fees shareholders paid as well as

management’s discussion of fund performance over the period. Investors now get

a report showing how much they paid, how much the broker (if any) was paid,

and how the fund compares with industry averages for fees, loads and brokerage

commissions.

5. PROPOSED by SEC, but not approved: “Hard closing” on buy/sell order

processing as of 4:00 PM EST daily. The industry is fighting this one because

they claim brokers would have to have the orders by as early as 10:00 am in the

day. (This is a problem that could easily be solved by technology however.)

17-2

Chapter 17 – Investment Companies 6th Edition

In March 2009 the SEC increased disclosure requirements for mutual funds. The funds

must now offer a straightforward explanation of key fund information at the beginning of

a prospectus provided to investors as a result of a potential investment order. The full

prospectus will still be available on the web.

Teaching Tip: Morningstar is maintaining a fund watch list for funds under investigation

with prescriptions for investors, such as “Proceed with caution,” “Don’t send new

money,” and “Consider selling.” This information is available at www.morningstar.com.

The scandals don’t seem to have had a lasting deleterious effect on the industry. Surveys

by the Investment Company Institute (ICI) indicate that 75% of people have a favorable

perception of the industry, although this perception is driven heavily by current mutual

fund performance.

3. Mutual Fund Global Issues

During the 1990s mutual funds were the fasting growing financial institution in the

United States. Growth slowed or declined in most major countries of the world in 2001,

reversing a decade long trend, but picked up again as the economic growth improved in

the mid-2000s only to decline again during the crisis. However, in the late 2000s growth

in non-U.S. investments outpaced growth in U.S. funds. Total assets of non-U.S. mutual

funds were $162.6 billion in 1992. As of 2013 there were $14.18 trillion invested in

mutual funds outside the U.S. Overall growth in non U.S. mutual funds holding has been

almost 53% since 2008. The U.S. is up 42% over the same period. The number of funds

is declining slightly in the U.S. but growing elsewhere. Mutual funds growth overseas is

concentrated in Japan, France, Australia and Great Britain as these countries have well

developed securities markets.

4. Hedge Funds

Introduction

Hedge funds are investment pools that solicit money from wealthy individuals and

institutions. In 2013, total investment in hedge funds was $2.25 trillion. The more than

8,000 hedge funds are much less regulated than typical mutual funds because they are not

open to the general public. Not all hedge funds are required to register with the SEC,

although stricter requirements are forcing more hedge funds to register; hence, hedge

funds self-report data. Unlike mutual funds, hedge funds are exempt from public

liquidity, disclosure, leverage and distribution requirements. To qualify for these

exemptions hedge funds are not open to the general public. They may only be issued via

a private placement and an individual hedge fund may have no more than 100 owners

that are deemed ‘accredited investors.’ To be accredited the investors must have a net

worth of over $1 million or have annual income of at least $200,000 ($300,000 if

married). Many hedge funds require a minimum investment of between $100,000 and

$20 million. Hedge funds need not report holdings to the SEC, they are allowed to

participate in illiquid markets and they are not required to adhere to a particular

investment style. In 2003 the SEC recommended that large hedge funds (over $25

million) register as investment advisers. This would subject them to audits and increase

17-3

Chapter 17 – Investment Companies 6th Edition

SEC oversight. In 2003 only about 25% of hedge funds were registered. The failures of

the Bear Stearns High Grade Structured Credit Strategies fund, the Bear Stearns

High-Grade Structured Credit Enhanced Leverage Fund and the Bernard Madoff

Investment Securities led to increased scrutiny of hedge funds. The Dodd Frank bill

requires that hedge funds with more than $100 million register with the SEC under the

Investment Advisors Act. Fund advisors must now report financial information on the

funds they manage to the FSOC to help limit systemic risk in the economy. The Federal

Reserve can also exercise oversight of funds deemed large enough or interconnected

enough to present a systemic risk.1

Banks and other firms like to be the ‘Prime Broker’ for hedge funds because hedge

funds are high dollar volume active traders. Attempting to get and keep this business can

lead to conflicts of interest.

Theoretically, hedge funds are designed to engage in risk arbitrage strategies, often

involving spreads in multiple markets. In practice, these funds often bet that prices will

return to historical patterns, and they may use mathematical models to identify alleged

mispricings that can be profitably exploited at low risk. If prices do not conform to the

expected patterns however, a hedge fund can find losses mounting rapidly. In order to

make enough return on mispricings, many of these funds are highly leveraged, so small

losses can quickly endanger a fund. The most well known fund, Long Term Capital

Management (LTCM), is a classic example of hubris and over-reliance on mathematical

models to measure and control risk. An excellent video on hedge funds and the

Black-Scholes model titled, “Trillion Dollar Bet,” is available from PBS Television.

No one hedge fund could generate the systemic risk caused by LTCM because of

increased monitoring by fund creditors, but hedge funds use similar models and invest in

similar situations. In thin markets such as emerging country debt or equities,

simultaneous transactions by multiple hedge funds (“herd” effects) could create or

exacerbate crises.

a. Types of Hedge Funds

Hedge funds are not all the same and may be classified into three broad types although

overlapping strategies are certainly possible, particularly across different market

conditions.

Market directional funds take positions in securities or markets ahead of

informational announcements or expected market moves. Thus they engage in risky

arbitrage strategies. Market timers would fit into this category. These often use

leverage and are exposed to significant levels of market risk. Some may use a

contrarian strategy and unlike mutual funds, may engage in extensive short selling.

Market neutral or value oriented funds may try to fund securities that are

temporarily mispriced such as a stock or bond of a firm in an out of favor industry or

1 Much tougher regulations of the hedge fund industry were proposed but failed to pass

Congress. Details are in the text. Note that if the hedge fund is not required to register

with the SEC it may still be regulated by the appropriate state agency.

17-4

Chapter 17 – Investment Companies 6th Edition

in financial distress. Funds of funds, multi-strategy funds and specialty funds looking

for hostile takeovers, LBOs etc, may fit into this category and they usually have less

risk exposure than directional funds.

Risk avoidance funds fit the traditional interpretation of the term ‘hedge fund.’

These funds take levered bets on lower risk or even pure arbitrage situations rather

than engaging in risky arbitrage. They may buy stock and offset the risk by shorting a

convertible bond on the same firm.

b. Hedge Fund Fees

Hedge funds charge management fees that are similar to standard annual mutual fund

expenses. These fees typically run between 1.5% and 2.0%. However, hedge funds

charge a performance fee as well if certain conditions are met. Performance fees average

20% of the gain in the fund assets. In order to assess the performance fee the fund will

have to meet a hurdle rate (minimum rate of return) and often must pass a ‘high-water

mark’ test. The high-water mark means the performance fee cannot be assessed unless

the fund’s NAV is at an all time high at the time of assessment.

c. Offshore Hedge Funds

The Cayman Islands are the location of about 75% of hedge funds. This is because

offshore funds are not taxed on distributions of profits and are not subject to U.S. estate

taxes on fund shares. Offshore funds trade more perhaps because they don’t face capital

gains taxes, they engage in less window dressing and don’t engage in as much ‘herd

behavior’ as onshore funds.

Hedge Fund Performance

Hedge funds did very well in the 1990s and did well throughout much of the 2000s until

the subprime crisis hit in 2007 when two Bear Stearns hedge funds involved in mortgage

backed securities quickly failed. UBS/Dillon Read Capital closed hedge funds in 2007,

and in early 2008 Citigroup barred investor withdrawals from one of its hedge funds.

The financial crisis reduced the amount of assets in hedge funds, although a few funds

did well during the crisis. The typical hedge fund had negative returns of 15.7% in 2008,

with about 75% of funds losing money that year. Even so, many funds outperformed the

indexes in the same time period. More recently hedge funds on average have not

outperformed the S&P 500 on a non-risk adjusted basis (see below):

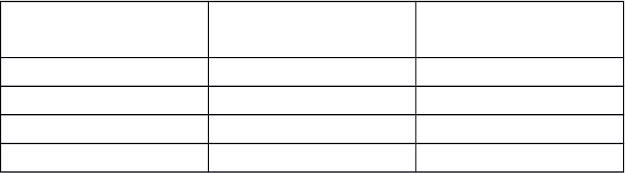

Year

Average Hedge

Fund Return S&P500 Return

2010 10.3% 15.1%

2011 5.0% 2.0%

2012 6.2% 14.5%

YTD Aug 2013 4.0% 20.0%

Fund redemptions followed a similar pattern as for mutual funds.

The collapse of the two Bear Stearns hedge funds led to investor losses of $1.6 billion

and led to the bankruptcy of the company. The funds bought CDOs with borrowed funds

and initially enjoyed a positive spread. The fund managers insured some, but not all, of

17-5

Chapter 17 – Investment Companies 6th Edition

the risks by purchasing credit default swaps. As the subprime crisis unfolded and the

value of the CDO holdings dropped far more than anticipated, Bear’s creditors asked for

additional collateral on loans and the funds did not have the cash needed. This led to fire

sales of assets and word quickly got out that Bear was in trouble. This in turn led to

additional sales of subprime securities which exacerbated the problems at Bear eventually

leading to the assisted buyout as Bear quickly ran out of capital.

Bernard Madoff Investment Securities was the fund run by former NASDAQ chairman

Bernie Madoff.2 Madoff ran an old fashioned Ponzi scheme, claiming to have $65 billion

in stock holdings that were fictitious.3 He apparently had not purchased stocks since the

mid-1990s. Madoff was arrested in late 2008 and the firm was liquidated after his sons

turned him in to authorities. Madoff pled guilty to 11 felonies and was sentenced to 150

years in jail with restitution charges of $170 billion.

More recently a large hedge fund, Galleon Group LLC, was closed in October 2009 due

to an insider trading scandal. The founder, Raj Rajaratnam, and 20 others were charged

with criminal violations of insider trading laws. The firm had allegedly used inside

information from consulting groups to invest. In July of 2013 SAC Capital was charged

with pervasive large scale inside trading where apparently the firm’s main competitive

strategy was to obtain and trade on nonpublic information. The government is seeking a

$2 billion settlement.

1.1.1.1 VI. Web Links

http://www.federalreserve.gov/ Website of the Board of Governors of the Federal

Reserve

http://www.wsj.com/ Website of the Wall Street Journal Interactive

edition. The web version of the well known

financial newspaper can be personalized to meet

your own needs. Instructors can also receive via

e-mail current events cases keyed to financial

market news complete with discussion questions.

http://www.ici.org Investment Company Institute website. See the

Mutual Fund Factbook for industry statistics.

http://www.lipperweb.com/ Lipper Analytical Services is an excellent site for

mutual fund information.

2 The Madoff fund was not a hedge fund, but acted as a fund of hedge funds.

3 A Ponzi scheme is a con where high returns are paid to fund investors with money paid

in by new investors. The scheme can grow as long as sufficient new funds are paid into

the fund. Word of mouth of the high returns offered by the Madoff fund led to large fund

inflows for a time. Investors must be skeptical whenever a fund offers higher than

normal returns.

17-6

Chapter 17 – Investment Companies 6th Edition

https://personal.vanguard.com/us/home?fromPage=portal

Vanguard Group’s website.

http://www.sec.gov/ The SEC’s website.

http://www.nasdaq.com/ The NASD’s website.

http://www.morningstar.com Rated by Barron’s as the number one website for

information about the mutual fund industry.

1.1.1.1.1.1 VII. Student Learning Activities

1. Go to http://www.morningstar.com and obtain the report on a large fund of

your choice. What is the fund’s strategy and how has it performed over the last 3 and

5 years? What is the fund’s star rating? What are the top five holdings of the fund?

2. Obtain the “Mutual Funds for Dummies” book by Eric Tyson. What are the

major reasons for investing in mutual funds? What is changing in the mutual fund

business?

3. For any specific mutual fund, where can you find its lowest quarterly return

(its worst three-month period) during the past 10 years? What are the tax consequences

of exchanging shares from one fund to another within the same fund family? Mutual

funds can be purchased directly from the fund company or indirectly through another

party (for example, through a broker, financial planner, or retirement plan). What

portion of sales of stock and bond funds is made directly to the investor? Please cite

your sources.

4. At the Investment Company Institute website obtain the report titled

“Frequently Asked Questions About Taxation for Mutual Funds.” How are mutual

fund holdings taxed? Does the investor’s holding period matter? How does fund

turnover affect an investor’s liability?

5. Using the latest Factbook found at the Investment Company Institute website,

rank the following types of fund by total assets in the most recent time period:

Aggressive Growth, Growth, Growth and Income, Balanced, Asset Allocation, Bond

funds and Money Market Mutual Funds. Explain the major differences between each

type of fund.

17-7