Chapter 16 – Securities Firms and Investment Banks

6th Edition

1. Recent Trends and Balance Sheets

a. Recent Trends

As goes the stock market, so goes securities firms’ profitability. Industry profits are

strongly cyclical. Extended bull markets are good for profits, employment and growth;

crashes and downturns hurt trading volume and hence commission income (a mainstay of

revenue at most firms). Fewer firms seek to issue new equity during a bear market, and

debt issuance drops off as coverage ratios decline so underwriting income is also cyclical.

Both underwriting and brokerage income recovered dramatically in the 1990s after

dropping off precipitously subsequent to the 1987 crash. Profitability remained strong

with the bull market of the 1990s. Industry profits were at a record high $21 billion in

2000, but fell 50% in 2001. Reasons for the profit problems included the weak stock

market, the September 11, 2001 attacks, the drop in M&A activity, and the loss of

confidence by investors due to the many ethical violations by some corporations, bankers

and auditors. Profitability remained poor in 2002 at $6.9 billion, but increased in 2003,

hitting a record $22.5 billion and remained high at $19.5 billion in 2004 on large

increases in underwriting activity and hefty cuts in interest and operating expenses. ROE

for 2004 was 13.04%. Domestic underwriting activity was $3,358.3 billion in 2006.

Profits would have been up in 2005 but interest expense on financing securities

inventories increased as interest rates rose. Interest expense rose from $43 billion in

2003 to $136 billion in 2005 to almost $216 billion in 2006. Pre-tax profits fell to $17.6

billion in 2005 but recovered to $33.1 billion in 2006 due to additional revenue growth.

The year 2007 was as bad a year for these firms as it was for most of the financial

services industry due to the subprime crisis. UBS wrote down $10 billion of subprime

related assets in 2007. Likewise, Morgan Stanley wrote down $9.4 billion, Merrill Lynch

wrote down $5 billion. Two hedge funds of Bear Stearns collapsed and went bankrupt

due to their subprime holdings as well. This was the setup to the Federal Reserve assisted

bailout of Bear in March 2008 where J.P. Morgan Chase agreed to purchase Bear for $2 a

share or $236 million.1 J.P. Morgan Chase also received guarantees on parts of Bear’s

mortgage portfolio.

In 2008 the industry reported net losses of $34.1 billion as revenues fell 38.7%.

Expenses fell as well particularly because with the lower interest rates, interest expense

declined. Trading and investment account losses for the industry were $65 billion. As a

result employment in the industry fell from 869,000 to 840,800. Employment kept

falling to 779,800 in September 2009. Profits rebounded sharply in 2009 reaching a

record $61.4 billion. Commissions, fee income and trading profits all rebounded and

interest expense remained very low as the Fed kept interest rates down. High profits

helped in rebuilding capital and efforts to raise external equity.

The years 2010 through 2012 brought many new challenges. The threat of a ‘fiscal cliff’

as U.S. government debt levels grew rapidly while Congress could not decide whether to

increase the debt ceilings, the problems in the Euro area, increasing regulations and

generally weak U.S. economic growth limited profitability for many firms. In May

2010 the ‘flash crash’ brought more scrutiny to trading activities as did the collapse in

1 The sale price was subsequently raised when shareholders complained.

16–1

Chapter 16 – Securities Firms and Investment Banks

6th Edition

October 2011 of MF Global along with the trading glitch at Knight Capital in August

2012. Pretax profits fell from 2010 levels of $34.8 billion to $10.6 billion in 2011 and

$12.4 billion in 2012. The fiscal cliff problem was resolved in January 2013 and after the

European Central Bank pumped about $1 trillion into euro area banks the euro crisis

subsided. In 2013, trading activity, and municipal bond and equity underwriting began to

grow once more and profitability improved.

b. The Balance Sheets

Selected major assets include: (2012)

Receivables from other broker-dealers 26.19%

Long positions in securities and commodities 24.38%

Reverse repurchase agreements 34.21%

Selected major liabilities and equity include: (2012)

Payables to other broker-dealers 14.23%

Payables to customers 15.35%

Short positions in securities and commodities 7.74%

Repurchase agreements 45.83%

Other nonsubordinated liabilities 7.56%

Equity 4.68%

Securities firms finance much of their securities inventory used in market making with

repos. Notice the high levels of repurchase agreement liabilities. This is one reason why

the Fed reacted quickly to ensure liquidity to securities firms when the repo market

briefly ceased functioning on collateral worries during the subprime crisis. These firms

can hold lower capital than banks because they are subject to lower capital requirements

and because their assets are more liquid than banks. Nevertheless, securities firms’

balance sheets are subject to high levels of both market and interest rate risk.

Non-commercial bank firms in this industry must maintain a minimum 2% capital ratio.

This level is probably too low for the risks they take. Indeed Bear-Stearns probably

failed because of its excessive leverage. During the crisis, these firms employed leverage

ratios greater than 30 to 1. This means if the firm loses 3% of the value of their assets,

they are bankrupt. Rumors of large losses at Bear in relation to their capital base led

investors to stop lending and forced a liquidity crisis and a lack of confidence that led to

the firm’s demise. J.P. Morgan Chase purchased the firm for $236 million even though

Bear’s offices in New York were valued at over $2 billion.

2. Regulation

The Securities Investor Protection Corporation (SIPC) insures losses of funds

deposited with securities firms up to $500,000 per investor in the event of the failure of a

securities firm. Losses to security values due to adverse market moves are not insured.

The daily activities of the securities industry are primarily regulated via the New York

Stock Exchange and the Financial Industry Regulatory Authority (FINRA). Thus, to a

large extent these firms are self-regulated according to rules promulgated by the SEC.

16–2

Chapter 16 – Securities Firms and Investment Banks

6th Edition

The Federal Reserve regulates margin requirements on stocks and occasionally suggests

rules changes involving securities trading and underwriting. Recently the Fed suggested

shortening securities settlement from the current three days to one day because securities

are often used as collateral for bank loans.

Since the passage of the National Securities Markets Improvement Act of 1996 removed

state oversight of securities firms, the SEC has the primary jurisdiction over securities

firms and sets standards for their activities. The SEC regulates underwriting and trading

activities and promulgates a series of rules such as Rule 144A regulating private

placements, Rule 415 allowing shelf registrations,2 etc. Under Rule 144A security

issuers may avoid the registration process (and the considerable expense) if they are sold

to a few qualified buyers. The buyers are typically institutional investors but certain high

net worth individuals can qualify. These securities may now be re-traded among the

qualified investors but may not be sold to the public.

Teaching Tip: Very few equities are privately issued; the private market is mostly for

debt. Privately placed debt issues will have lower flotation costs but often carry higher

interest rates.

In the early 2000s certain states began to take a much more active role in regulations of

the markets. Former New York State General Attorney Spitzer led in this process. These

prosecutions led to SEC rules changes to help ensure fewer conflicts of interests between

analysts and investment bankers and better methods of allocating IPO shares.

Investment bankers paid large fines as a result (fines totaled $1.4 billion, see Chapter 8).

In particular, analysts have been barred from attending/participating in the ‘road shows’

and may not receive compensation based on the amount of underwriting business the firm

generates. Within days of the settlement however, Bear Stearns allegedly violated the

new rules. Morgan Stanley allegedly withheld emails pertinent to hundreds of arbitration

cases, falsely claiming the email were lost in the September 11, 2001 terrorist attacks

when they were not.

Teaching Tip:

Interestingly, Bear Stearns (and I am sure the rest) had a very explicit code of ethics

requiring employees to treat customers fairly and to report all ethical violations. The

corporate culture on Wall Street, including compensation schemes, needs an overhaul.

Moreover, these violations matter. They impede growth by raising the cost of funds to

everyone. How much value was destroyed by unethical behavior of managers at Enron,

WorldCom, HealthSouth, Tyco, Parmalat, etc.? How much spillover to other firms’ stock

prices occurred as a result of the loss of confidence in management? What did this do to

our cost of funds, or reliance on foreign funds if you prefer. What has/will this cost us in

the future in terms of costly contracting? Already a class action lawsuit against bankers

2To help speed up the process issuers sometimes pre-register securities using a procedure

termed a shelf registration. After the registration is approved the issuer may then market

the issue at any time within the subsequent two years after filing a short form with the

SEC that is normally approved within a day or two.

16–3

Chapter 16 – Securities Firms and Investment Banks

6th Edition

that underwrote WorldCom debt has resulted in payments of $6 billion by bankers (with

the largest payment of $2.85 billion by Citigroup). Citigroup also paid $2 billion to settle

a class action suit over Enron and $75 million to settle a similar suit over its involvement

with Global Crossing. Citi has now instituted mandatory ethics training for all

employees.3 The long jail sentences that Ebbers (WorldCom CEO), Rigas (Adelphia

CEO), Dennis Kozlowski and others received should also help deter some of the more

egregious fraud schemes. I believe that at some point increased sentences may be needed

to rein in unethical investment banking practices as well.

The markets themselves have not been immune to scandal. In 1996 the SEC charged the

NASD (the regulatory body of the NASDAQ stock market) with ignoring evidence of

price fixing by NASDAQ market makers or dealers. The dealers were allegedly

colluding to keep bid-ask spreads artificially high by refusing to quote odd eighths and

blackballing dealers who did not comply (at that time many stock prices traded in

minimum increments of one eighth). The NASD agreed to spend $100 million to

improve rules enforcement. Subsequently, 30 brokerage firms agreed to pay $900 million

to settle a civil suit alleging they engaged in price fixing of NASDAQ securities.

In 2003 the NYSE fined a trader of Fleet Specialist Inc $25,000 for front running. Front

running occurs when a specialist executes orders for their own account ahead of public

orders. The trader sold GM stock from the specialist’s own account on rumors of

accounting problems at GM ahead of a public sell order.

In July 2002, Congress passed the Sarbanes-Oxley Act seeking to improve corporate

governance and accounting oversight. This bill created an independent auditing oversight

board run by the SEC, increased penalties for corporate malfeasance, and gave

disgruntled shareholders more options to pursue lawsuits. The law restricts accounting

firms’ ability to provide non-audit services to audit clients and no longer allow the AICPA

to set accounting and auditing standards. These will be set by the Public Company

Accounting Oversight Board. The act requires that the CEO and CFO prepare and sign a

statement certifying the reasonableness of the firm’s financial statements. The NYSE and

the NASD have also changed their listing requirements with respect to corporate

governance. Details may be obtained from their websites (see the list of websites at the

end and in Chapter 8).

Anti-money laundering activities:

The USA Patriot Act added three new requirements to securities firms as of October

2003. The new rules included:

1. Firms must verify the identity of any person seeking to open an account.

2. Firms must keep records of the information used to verify the client’s identity.

3. Firm must determine whether the client appears on any lists of known or

suspected terrorists or terrorist organizations.

The industry is subject to Congressional oversight, but this usually takes the form of

3 Citgroup data from “Evening Wrap Up, Citi Settles,” Mark Congoloff, The Wall Street

Journal Online, June 10, 2005.

16–4

Chapter 16 – Securities Firms and Investment Banks

6th Edition

ex-post investigations after problems have emerged. For instance, Goldman Sachs (GS)

was investigated by a congressional panel in 2010 concerning GS’ creation of mortgage

backed CDOs which they had shorted to limit their risk. GS was accused of knowingly

creating and selling risky mortgage investments after they knew they were likely to be

riskier than the rating indicated and put themselves in a position to profit from a decline

in the securities’ values. This is an obvious conflict of interest. Under the Dodd Frank

Act, the Financial Services Oversight Council (FSOC) has oversight of systemic risk of

the industry. More investment advisors will have to be registered with either the SEC or

state advisors. Securitization markets should now have more oversight and originators

will have to retain a greater interest in loans that will be resold. More derivatives

regulation over time can be expected as well. FINRA is increasing oversight and

reporting requirements for dark pools and for flash trading. As of this writing no formal

limits have been proposed on these activities but they are suspected to increase volatility

and of being used in market manipulation strategies.

The government can also mandate higher capital requirements for larger and for

interconnected firms. Government oversight of industry practices has increased as a

result of the bill. Executive compensation restrictions were also promulgated by the

Obama administration which tried to strengthen the independence of the compensation

committee from senior management. Shareholders now also have a non-binding vote on

executive compensation packages and Obama’s pay czar, Kenneth Feinberg, has a say on

executive pay for firms that accepted bailout money.

Teaching Tip:

Ask students whether limits on executive pay are appropriate or not. What would be the

pros and cons? The industry argues that they will be unable to attract top talent without

large performance type bonuses. Executive pay would seem to be very high however and

it is higher than is typical in much of the rest of the world. Many in the public would

argue that executives in firms that took taxpayer dollars have no business receiving any

performance bonuses. AIG executives received bonuses even as the firm was on the

verge of bankruptcy.

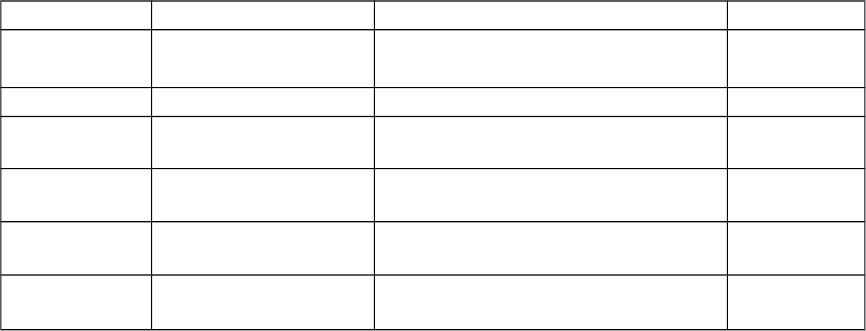

The Scandals Continue

Date Firm/Principal Acvity

Selement

Payment

January 2011 Primary Global

Research LLC, Bob

Nguyen

Solicing informaon for inside

trading

June 2012 Barclays Bank LIBOR manipulaon $450 million

July 2012 Peregrine Financial,

Russell Wassendorf ,

Misallocang and misreporng

usage of $215 million in client funds

December

2012

Goldman Sachs trader

Mahew Taylor

Concealed $8.3 billion futures

posion

$1.5 million

December

2012

Morgan Stanley

Senior banker in6uenced analyst and

share allocaon of Facebook IPO

December

2012 UBS LIBOR manipulaon $1.5 billion

16–5

Chapter 16 – Securities Firms and Investment Banks

6th Edition

December

2012 HSBC Money laundering $1.9 billion

February

2013

Royal Bank of

Scotland LIBOR manipulaon $610 million

October 2013 J. P. Morgan Bad mortgage pracces originaon

and sale $13 billion

October 2013 J. P. Morgan Trade error in London cost ;rm $6

billion $920 million

October 2013 J. P. Morgan Excessive credit card charges $ 80 million

October 2013 J. P. Morgan Manipulang energy markets $410 million

December

2013 Deutsche Bank Euribor manipulaon $981 million

February

2014 Morgan Stanley Bad mortgage pracces originaon

and sale $1.25 billion

July 2014 Cigroup Bad mortgage pracces originaon

and sale $7.00 billion

July 2014 Lloyds Banking Group LIBOR manipulaon $370 million

Sources: Text, Wall Street Journal and Bloomberg, various dates

This list is not complete. Charges of the same banks as involved in LIBOR fixing of

manipulating ISDAfix, a rate used for swaps, are also emerging as of July 2014. Also as

of this writing, evidence is emerging of allegations that the Bank of England, the British

central bank, knew of manipulations of currency rate quotes for as long as eight years

without taking action. The currency markets involve over $5.3 trillion in daily trading

volume.4 The SEC is investigating whether traders distorted prices for currency options

and exchange traded funds. Reports are emerging that traders shared information about

client orders in order to manipulate prices. As of June 2014 about 20 traders at the top

three banks (Deutsche, Citi and Barclays) involved in currency trading had been fired.

Teaching Tip:

These firms are regulated but we continue to have ethical problems. Ask students

whether regulations are sufficient to prevent these problems. If not, then what else

should be done? As of January 1, 2013 Dutch bankers are required by law to swear an

oath to act ethically, details can be found at:

http://www.nibc.com/investor-relations/dutch-banking-code.html. Should the U.S. do

something similar?

3. Global Issues

Investment banking activities are highly globalized. For instance, in 2012 Deutsche Bank

was the number one underwriter of convertible debt and mortgage debt. Foreign

transactions in U.S. stocks increased from $211.2 billion in 1991 to $12,037.9 billion in

4 Carney Faces Grilling as Currency Scandal Snares BOE. Bloomberg, By Scott

Hamilton and Suzi Ring Mar 10, 2014 8:37 AM MT,

http://www.bloomberg.com/news/2014-03-10/carney-faces-leadership-test-as-currency-sc

andal-snares-boe.html.

16–6

Chapter 16 – Securities Firms and Investment Banks

6th Edition

2008. This represents a compound average annual growth rate of 26.85%. U.S.

transactions in foreign stocks increased from $152.6 billion in 1991 to $5,410.9; an

annual compound growth rate of over 23%. The financial crisis deterred the rate of

growth. In 2013 foreign transactions in U.S. stocks were $7,571.68 billion and U.S.

trading in foreign stocks was $3,969.5 billion. International offerings have also grown

rapidly, but recent scandals, the U.S. stock market weakness, disclosure requirements and

the decline in the value of the dollar has probably deterred foreign investors and foreign

issuers from participating in the U.S. markets. U.S. firms are seeking a greater presence

in fast growing markets such as China and India.

The financial crisis has increased the need for capital at banks. Many firms are now

engaging in strategic alliances with foreign partners. For instance, Morgan Stanley sold a

21% stake of its firm to Mitsubishi UFJ in 2008. Citigroup took a different tact and sold

some of its foreign businesses such as Nikko Asset Management and Nikko Citi Trust to

increase capital. The industry continues to restructure as a result of the crisis.

Teaching Tip: Investment bankers can help U.S. institutions gain exposure to

international markets. Banks have created structured derivative debt products that allow

an institution to earn higher overseas interest rates while limiting exchange rate risk.

Bankers can also sometime help improve the marketability of foreign bonds that are

difficult to sell because they are denominated in a foreign currency. Many U.S. financial

institutions are limited as to how much currency risk they can incur. Bankers have at

times securitized these foreign currency denominated bonds by placing them in a trust

and issuing dollar denominated claims to U.S. buyers.5 Hedge funds engage in risk

arbitrage strategies on a global basis. The most famous of these (or infamous), Long

Term Capital Management, engaged in risk arbitrage on an unprecedented global scale.

1.1.1.1

1.1.1.2 VI. Web Links

http://www.federalreserve.gov/ Website of the Board of Governors of the Federal

Reserve

http://www.wsj.com/ Website of the Wall Street Journal Interactive

edition. The web version of the well known

financial newspaper can be personalized to meet

your own needs. The Wall Street Journal Online

‘Scandal Scorecard’ provides readers with a fast

way to keep track of the large number of scandals

and what has happened to the players.

http://www.sifma.com/ The Securities Industry Association website.

Industry information, the SIA Factbook (other than

the current annual version) and discussions on key

industry issues may be found here.

5 These claims are usually overcollateralized to help limit exchange rate risk.

16–7

Chapter 16 – Securities Firms and Investment Banks

6th Edition

http://www.sec.gov/ The Securities Exchange Commission

http://www.nyt.com/ The New York Times, from time to times the NYT

has excellent articles on financial topics.

http://www.tfibcm.com/ Thompson Reuters website. This site has the latest

updates on U.S. and global underwriting volume

and M&A activity.

http://www.nyse.com/ The website of the NYSE, exchange rules are

online.

http://www.nasdaq.com/ The National Association of Securities Dealers

website.

http://www.sipc.org/ The Securities Investor Protection Corporation

website.

1.1.1.2.1.1

1.1.1.2.1.2 VII. Student Learning Activities

1. Go to the website of the SIPC and summarize the answers to the ‘7 most

asked questions about the SIPC.’

2. At the NASD’s website, read the study outline for the Series 7 exam. What is

the purpose of the Series 7 exam? What are the seven critical functions of a registered

representative?

3. Go to the SIFMA website and read about the complexity of the new Dodd

Frank law. How many new regulations are proposed? Will this law help or hurt the

industry? Defend your answer.

16–8