Chapter 15 – Insurance Companies 6th edition

1. Property-Casualty Insurance Companies

a. Size, Structure and Composition of the Industry

There are about 2,700 P&C insurers. The top10 firms write about 53% of the premiums,

and the top 200 firms write 94% of all premiums. State Farm is the largest, followed by

Berkshire Hathaway. Total assets in 2013 were about $1.7 trillion, roughly one-third of

the total assets of the life insurance industry.

Types of products:

Property & casualty. Property insurance covers the loss of real and personal property,

whereas casualty insurance provides protection from legal liability exposures.

Major P&C Lines % of premiums

Loss to

Premiu

m ratio

Homeowners multiple peril 15.0% 59.0%

Private passenger auto liability 20.5% 67.7%

Private passenger auto physical

damage 12.9% 64.8%

Other liability insurance 9.60% 51.4%

Worker’s compensation 9.30% 70.0%

2012 data on major lines. Major lines are those lines that generate approximately 8%

or more of total premiums.

Homeowners multiple peril (personal property and liability coverage) (15.0% of

all premiums); the loss to premiums ratio was 59.0%.

Private passenger auto liability (20.5% of all premiums); the loss to premiums

ratio was 67.7%.

Private passenger auto physical damage (12.9% of all premiums); the loss to

premiums ratio was 64.8%.

Other liability insurance (non-automobile) (9.6% of all premiums); the loss to

premiums ratio was 51.4%.

15–1

Chapter 15 – Insurance Companies 6th edition

Worker’s compensation (9.3% of all premiums) the loss to premiums ratio was

70.0%.

With the 2012 data, the losses to premium ratios were highest for ‘federal flood’ at

196.2%, ‘multiple peril crop’ at 138.3% and ‘mortgage guarantee’ at 151.8%. Of the

major lines offered the ratio was highest for the ‘private passenger auto liability’ and

‘Worker’s compensation’ lines. The smallest loss ratio overall occurred on ‘earthquake

(all lines) and on the major lines the smallest loss ratio occurred for ‘other liability.’.

b. Balance Sheets and Recent Trends

Major assets include (beginning of 2013): Change from 2010

Bonds 55.6% Down

Preferred stocks 0.7% Down

Corporate equities 15.2% Up

Mortgages and real estate 0.9% Down

Cash and short-term investments 5.1% Down

Net deferred taxes 1.8% Down

Reinsurance 2.7% Up

Premium balance 8.1% Up

Accrued Interest 0.6% Down

All Other 2.4% Same

P&C insurers typically place the majority of their investments in long term assets, but

they have more liquid asset holdings (%) than life insurers. This is because P&Cs have

much less predictable claims than life insurers; thus, the P&C’s investment portfolio

reflects their greater need for liquidity.

Major liabilities and equity include (beginning of 2013) Change from 2010

Loss reserves and loss adjustment expenses (LAE) 37.7% Down

Unearned premiums 12.7% Down

Other liabilities 13.4% Up

Policyholders’ surplus 36.2% Up

Loss reserves are funds held to offset expected payouts on insurance policies. Loss

adjustment expenses are expenses related to administering and settling (adjusting)

claims. Unearned premiums are premiums received before the coverage period so that

they have not yet been earned. Net premiums written are the total amount of premiums

received on all lines.

Teaching Tip: Ask students why the surplus account is so large for P&C insurers. The

answer is that P&C insurance itself has been unprofitable in most recent years and P&C

insurers must rely on investment returns to generate profitability. With uncertain

investment returns a large surplus is needed to offset unexpected high losses, expenses

and poor market conditions. See the numerical example below.

15–2

Chapter 15 – Insurance Companies 6th edition

The profitability of an insurance line can be calculated as follows:

Premiums received + income earned on premiums invested – cost of claims incurred –

loss adjustment expenses – other expenses such as brokerage commissions.

If this amount is negative the line is generating losses. This usually happens if

unexpectedly high or costly claims occur, or if adjustment expenses are higher than

anticipated (perhaps due to additional lawsuits than anticipated) or if the rates of return

on investments are lower than anticipated.

The expected loss rate on an insurance line is the expected frequency of loss times the

severity (cost) of the loss. In general, property losses are more predictable than liability

losses. Loss rates for high frequency, low severity events such as a fender bender are

also more predictable than losses on low frequency, high severity events such as a

flood, an earthquake or a terrorist attack.

Liability lines may suffer what are termed long tail losses, meaning that a claim is filed

long after the occurrence of the insured event. Examples include asbestos claims, claims

for toxic shock syndrome, tobacco use, breast implants, etc. These losses can be

particularly hard to forecast, and these possibilities make it difficult to properly price the

product line exante.

Price inflation is the major factor that increases costs on property lines and it is fairly

predictable. Social inflation (increases in required insurance payouts associated with

societal attitudes) may result in large cost changes on liability lines however if judges and

juries award larger penalties for medical malpractice or other product liability cases. The

tobacco lawsuits provide a recent example. As the text indicates the number of claims

and jury awards for medical malpractice suits have increased dramatically in recent

years. To offset this trend, a growing number of states are placing caps on malpractice

awards beyond actual damages (the so called ‘pain and suffering’ awards). Certain areas

such as Wyoming have had difficulty attracting sufficient numbers of medical personnel

because of the high costs of malpractice insurance.

The loss ratio measures the actual losses on a specific policy (this ratio may include

actual claim payouts and loss adjustment expenses) relative to earned premiums. A loss

ratio over 100% implies the line is unprofitable on its own. Loss ratios have risen from

the 60% range in the 1960s to over 70% or even 80% today. Expense ratios include

items such as general expenses and broker commissions measured relative to premiums

earned. Expense ratios are quite high. In 2012 expense ratios averaged about 28.2% of

premiums written. The gross premium charged on a line is the sum of the ‘pure

premium’ (found as frequency of loss times average loss) plus a load fee that represents

the firm’s profit margin.

15–3

Chapter 15 – Insurance Companies 6th edition

The advent of the Internet and computer technology should reduce expenses

considerably. At first, many industry observers believed that the Internet would make

insurance agents and brick and mortar offices obsolete. This is unlikely in the near

future. Technology should allow insurers to offer better service to their customers in

managing their accounts and reduce back office processing costs, which in turn may

allow the customer to receive better deals. The insurance industry has never been known

for its innovation and it is likely that technology will help insurance firms cut costs to a

greater degree than we have seen in the past. Indeed, this will likely have to happen

given the poor profit record of many insurers in recent years.

The combined ratio is the sum of the loss and expense ratios. The combined ratio also

may include dividends paid out to policyholders. If the combined ratio after dividends

is less than 100%, insurance underwriting was profitable that year. Underwriting

insurance was unprofitable every year during the 1990s and the early 2000s. For

instance, the combined ratio after dividends was 105.6% in 1998, 115.7 in 2001 (the

worst ever), 107.2% in 2002, and 100.1% in 2003 and the lines finally became profitable

in 2004 with a combined ratio of 98.7. If the combined ratio is greater than 100%, the

insurer can maintain profitability only by generating a high enough rate of return on

invested premiums (see the example below).

Hurricanes Charley, Frances, Ivan and Jeanne all occurred in 2004 generating estimated

losses of over $25 billion. In 2005 Hurricanes Katrina, Wilma and Rita added to the

industry’s losses with estimated costs of $57.7 billion. The 2005 P&C industry combined

ratio was 100.9. Without these catastrophic losses the 2004 and 2005 combined ratios

would have been 94.5 and 92.9 respectively. 2006 and 2007 had much smaller

catastrophic losses and most lines did very well yielding combined ratios of 92.4 and 93.5

respectively. The industry is again profitable overall, but it has become dependent on

sufficiently high rates of return on invested premiums to maintain profitability in the face

of very volatile loss experiences. Underwriting profits appear to cycle through time as

high loss experiences occur periodically and reduce profits. These events eventually get

priced into insurance contracts and then they stop occurring for a while and industry

profits are quite good for a time.

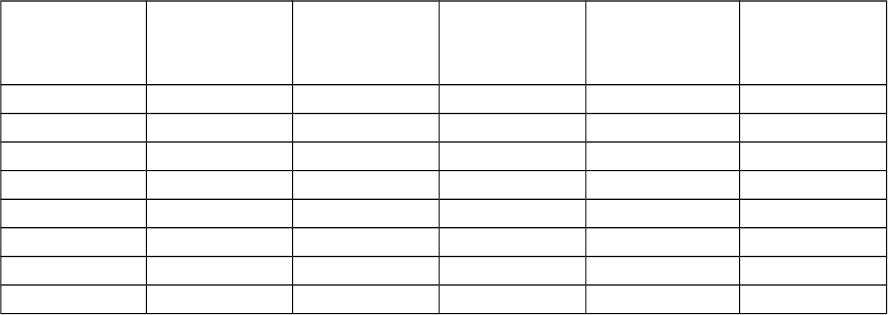

Partial Text Table 15-6 Property-Casualty Industry Underwriting Ratios

Year Loss Ratio

Expense

Ratio

Combined

Ratio

Dividends to

Policyholder

s

Combined

Ratio after

Dividends

2006 66.2 25.4 91.6 0.8 92.4

2007 68.0 27.1 95.1 0.5 95.6

2008 77.4 27.2 104.6 0.5 105.1

2009 73.2 27.3 100.5 0.5 101.0

2010 73.5 28.4 101.9 0.5 102.4

2011 79.4 29.8 107.8 0.4 108.2

2012 74.5 28.2 102.7 0.5 103.2

2013 65.7 28.6 94.3 0.5 94.8

Source Text, from AM Best, www.ambest.com

15–4

Chapter 15 – Insurance Companies 6th edition

Notice the increases in loss and expense ratios beginning in 2007 and rising until 2011.

The dividend ratio fell as profitability decreased. The industry lines as a whole were

unprofitable from 2008 through 2012 (before net interest income on investments).

Standard and Poor’s (S&P) issued a statement in June 2011 indicating concern about

profitability of commercial lines due to price declines and competition coupled with poor

investment income. Premiums written increased in 2010 after a 3 year drop and have

continued to improve. Nevertheless 2011 was a bad year with large catastrophe losses

($33.6 billion, the fifth worst year ever). Net income fell from $35.2 billion in 2010 to

$19.2 billion, a 46% drop. Even with Hurricane Sandy, profits improved in 2012 as the

combined ratio fell from 108.2 in 2011 to 103.2 in 2012. Net income surged to $33.5

billion for the year. The year 2013 was better still with a much lower combined ratio,

even though the investment yield also fell.

Example 1: Calculating ratios for a hypothetical individual line

Premiums

$9,455,12

2

Losses

$7,456,78

9

Expenses

$2,578,10

0

Dividends 4.00% of premiums

Loss ratio 78.87% losses to premiums

Expense ratio 27.27% expenses & commissions to premiums

Combined ratio 110.13% (sum of loss, expense and dividend ra#os)

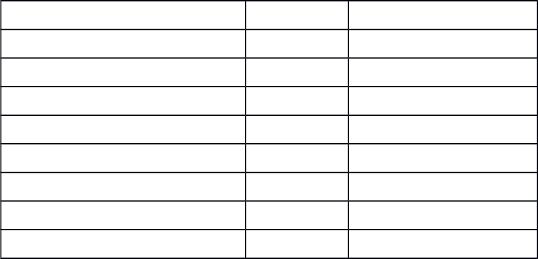

Example 2: Calculating ratios with aggregate data.

This example uses 2013 industry average data from Text Table 15-6, except for

Investment Yield which is found in the text discussion. The text data is derived from

A.M. Best; all numbers are a percent of premiums. The Loss Ratio includes Loss

Adjustment Expenses (LAE); the expense ratio is brokerage commissions and other

operating expenses expressed as a percent of premiums.

Loss Ratio

Expense

Ratio

Combined

Ratio

Dividends to

Policyholders

Combined

Ratio after

Dividends

Investment

Yield

65.7 28.6 94.3 0.5 94.8 10.6

The Combined Ratio = Loss Ratio + Expense Ratio = 65.7 + 28.6 = 94.3

With the Combined Ratio < 100, profitability from writing insurance was

positive; premium income was more than losses and dividend payments by 5.7%.

The Combined Ratio after Dividends = Combined Ratio + Dividends to Policyholders

Combined Ratio after Dividends = 94.3 + 0.5 = 94.8

Dividends to policyholders are a part of the marketing effort on sales of policies, as

such they are usually considered too important to be eliminated, although they do

vary with profitability. After considering dividend payments to policyholders,

15–5

Chapter 15 – Insurance Companies 6th edition

premiums were more than outlays by 5.2%.

The Operating Ratio = Combined Ratio after Dividends – Investment Yield

Operating Ratio = 94.8 – 10.6 = 84.2

With the operating ratio < 100, the numbers indicate that the loss ratios coupled with

relatively strong investment yields generated profitability for the P&C industry as a

whole for the year.

Uncertain loss ratios, high expense ratios, the need to pay dividends, a lack of flexibility

to adjust premiums and uncertain investment yields all indicate the need for large policy

surpluses, which the industry currently has (equal to about 36.2% of assets).

Many low frequency, high severity losses occurred in the 1990s and 2000s including

many natural disasters such as the strong El Nino, the many severe hurricanes, including

Katrina, earthquakes, tsunamis, cyclones, tornadoes and flooding, and some manmade

disasters such as asbestos and tobacco liability claims and the attack on the World Trade

Center. These have generated abnormally large losses. Some have estimated that the

dollar cost of the terrorist attacks was as high as $40 billion. The federal government

now has a terrorism insurance program. The government is responsible for 90% of

insurance industry losses that arise from a terrorist incident if the losses exceed a certain

amount. Each insurer would have to pay 15% of its commercial P&C premiums.

Nevertheless the cost to insure high probability targets remains expensive.

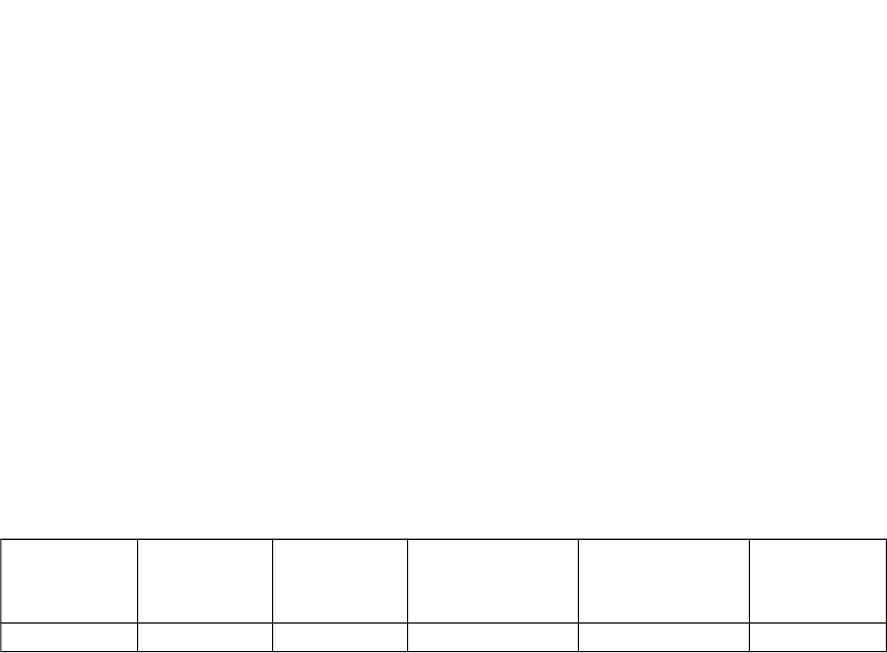

Partial version of Text Figure 15-3: Top Recent U.S. Catastrophes By Year

Catastrophe Year Amount ($ mill.)

Hurricane Sandy 2012 $25,000

Midwest Drought 2012 $16,000

Midwest tornadoes 2011 $14,200

Hurricane Ike 2008 $12,500

Hurricane Katrina 2005 $66,000

Florida Hurricanes 2004 $25,000

9/11 Terrorist Attacks 2001 $40,000

Hurricane Andrew 1992 $19,900

The text mentions the court decision that allowed Halliburton to resolve its asbestos

liability (asbestos causes lung cancer and workers and community members in production

sites such as Libby, Montana have suffered decades of higher cancer rates) by

bankrupting one of its subsidiaries. This could help keep liability insurance down but it

may set a disturbing precedent and may encourage other firms to engage in unethical

behavior because the potential penalties may now be perceived as lower.

Insurance companies can attempt to share risks by buying insurance from other insurance

companies. This growing practice is called reinsurance. About 10% of all insurance

contracts world wide are ‘reinsured.’ P&C insurers engage in reinsurance to a greater

extent than life insurers due to the greater unpredictability of P&C claims. Foreign

insurance firms write about 75% of the reinsurance contracts used by U.S. insurers.

Catastrophe bonds are a unique form of reinsurance. Different bonds may have different

structures but the basic idea is that the bond’s principal and interest are reduced if a given

catastrophe occurs. The reduction in the bond issuer’s payments then can offset the

15–6

Chapter 15 – Insurance Companies 6th edition

additional losses on the insurance line. As the text mentions, Munich Re issued a $250

million deep discount catastrophe bond in 2010 that would pay principle of 100(1-) at

maturity. The equals the losses incurred on all reinsurer policies over a 24 hour period

should an event such as a flood or hurricane occur if losses are above a minimum

threshold. As of 2013 there was about $18.6 billion of catastrophe bonds outstanding and

new issuance reached a record $7.1 billion.1

c. Regulation

P&C insurers are chartered and regulated at the state level. Some states regulate the

premiums insurers may charge; this has also contributed to the high loss ratios of the

1990s. The NAIC assists state regulators in providing examination forms and data on

ratios at insurers.

American International Group (AIG) Inc., formerly the second largest P&C insurer in the

world by revenues, became embroiled in several scandals in the mid 2000s. AIG

allegedly assisted one or more firms in implementing fraudulent accounting to smooth the

client’s earnings by engaging in payments that looked like insurance transactions but

were not. AIG paid $126 million in penalties and costs, but admitted no wrongdoing.

The scandals cost the CEO his job however. Marsh and McLennan (M&M) (an

insurance broker) received $845 million in kickbacks associated with bid rigging. M&M

allegedly directed clients to higher cost insurance packages in order to earn the high fees.

Not all insurers acted honorably during some of the recent crises. For instance, State

Farm and others tried to classify the Katrina storm surge as flood damage which was not

covered under many homeowners’ policies. The courts disagreed and ruled that State

Farm was liable for actual and punitive damages.

2. Global Issues

The insurance industry is becoming more global and there have been several large cross

border mergers recently although insurers have probably not participated in globalization

to the same extent as banks and other financial service providers. About 59% of total

global life insurance premiums written are generated by five countries: the U.S., Japan

the United Kingdom, France and Germany. The world’s largest life insurer by revenue in

2012 was Japan Post Holdings with revenue of $211.0 billion. The largest P&C insurer

was Berkshire Hathaway with $143.7 billion in revenue.

The years 2011 and 2012 were poor years for insurers worldwide. Although there were

fewer catastrophe related deaths than in prior years there were still over $111 billion

insured losses in 2011 and $65 billion in 2012. In 2012 the bulk of the losses were in the

U.S. In earlier years the catastrophes were more global and included greater loss of lives.

In 2008 over 240,000 people died in over 130 natural disasters and 174 man-made

disasters with the largest losses in Asia. About half the global losses were associated with

the massive earthquake in China. The financial crisis reduced sales of equity linked

products and the general malaise also saw reductions in revenue from other lines,

particularly in P&C lines at that time.

1 Data source: http://www.iii.org/fact-statistic/catastrophe-bonds

15–7

Chapter 15 – Insurance Companies 6th edition

1.1.1.1

1.1.1.2

1.1.1.3 VI. Web Links

http://www.federalreserve.gov/ Website of the Board of Governors of the Federal

Reserve

http://www.wsj.com/ Website of the Wall Street Journal Interactive

edition. The web version of the well known

financial newspaper can be personalized to meet

your own needs. Instructors can also receive via

e-mail current events cases keyed to financial

market news complete with discussion questions.

http://www.ambest.com A.M. Best is a leading source of information on the

insurance industry. Industry and firm specific data

are provided.

http://www.nuco.com/ The National Underwriter Company publishes a

“broad array of print, e-media and software

products for the insurance and financial services

industries.”

http://www.naic.org/ The National Association of Insurance

Commissioners

http://www.dfs.ny.gov/insurance/dfs_insurance.htm The New York State Insurance

Department

http://www.iii.org Insurance Information Institute website

1.1.1.3.1.1

1.1.1.3.1.2 VII. Student Learning Activities

1. Go to www.actuary.com and learn what an actuary is and what an actuary does. What

different types of actuaries are there? What is required to become an actuary?

2. Locate the Berkeley mortality tables on the web and use them to ascertain how many

fewer (%) males and females age 80-84, 85-89 and 90-94 are projected to die in

2071- 80 rather than now. How is this type of data useful in setting life insurance

costs? Explain.

3. Locate a property and casualty firm’s most recent annual report (many are on line).

15–8

Chapter 15 – Insurance Companies 6th edition

What is the firm’s loss ratio? The combined ratio? What do these ratios imply about

the firm’s profitability?

4. Go to A.M. Best’s website and report on the major determinants of an insurance

company’s ratings.

5. Research and formulate answers to the following questions:

U.K. insurance regulators recently ruled that U.K. insurers can no longer charge

higher auto insurance rates to men than to women. Do you agree or disagree with

this ruling? Isn’t charging different rates gender discrimination? What are the

pros and cons of each side of the argument?

Should insurers be required to offer medical coverage to anyone who applies?

One of the arguments for the new health care plan passed by Congress was that

many people with health risks could not obtain medical coverage (or sufficient

supplemental medical coverage) of any kind. Present both sides of the argument.

Should government pay for medical costs or insurance? What would be the pros

and cons?

15–9