1.1.1.1.1Part IV: Other Financial Institutions

1.1.1.1.2Chapter Fourteen

Other Lending Institutions: Savings Institutions,

Credit Unions, and Finance Companies

1.1.1.2 I. Chapter Outline

1. Other Lending Institutions: Chapter Overview

2. Savings Institutions

a. Size, Structure, and Composition of the Industry

b. Balance Sheet and Recent Trends

c. Regulators

d. Savings Institutions Recent Performance

3. Credit Unions

a. Size, Structure, and Composition of the Industry

b. Balance Sheets and Recent Trends

c. Regulators

d. Industry Performance

4. Finance Companies

a. Size, Structure, and Composition of the Industry

b. Balance Sheets and Recent Trends

c. Industry Performance

d. Regulation

5. Global Issues

1.1.1.3 II. Learning Goals

1. Recognize the differences between a savings institution, a credit union, and a

finance company.

2. Identify the main assets and liabilities held by savings institutions.

3. Know who regulates savings institutions.

4. Describe how savings institutions performed in the 2000s.

5. Discuss how credit unions are different from other depository institutions.

6. Identify the main assets and liabilities held by credit unions.

7. Define the major types of finance companies.

8. Identify the major assets and liabilities held by finance companies.

9. Examine the extent to which finance companies are regulated.

1.1.1.4 III. Chapter in Perspective

This chapter covers savings associations, credit unions and finance companies. Savings

associations (traditionally called ‘savings & loans’ or S&Ls) and credit unions have historically

been small institutions serving specialized needs of local groups. Savings banks are a hybrid

between savings associations and banks, larger and better diversified than savings associations,

smaller and less diversified than banks. Today of course the functions of all financial

intermediaries (FIs) increasingly overlap. The term savings institution is used to refer to

savings associations and savings banks. The credit union industry has grown to the point that

some credit unions are considered a threat to local banking institutions. Banks have attempted to

persuade Congress to remove credit unions’ nonprofit status. Credit unions are typically small

institutions that do not have the management expertise of other FIs. By themselves, they would

be underdiversified and at risk from failure, so a large cooperative network has been created to

assist credit unions. Finance companies fulfill specific intermediary niches. Some specialize in

subprime lending, some finance working capital needs of companies and some are captive

lenders created to channel funds to a specific company or to finance consumer purchases of the

company’s products. They are distinguishable from banks and thrifts in that they are not funded

by deposits and do not offer retail accounts. As a result this industry is much less regulated than

DIs or insurers. This chapter covers the major assets and liabilities of each of these industries

and identifies the key risks and trends each face. The different regulators for each industry are

discussed along with recent performance. The Instructor’s Manual also includes a brief

summary of The Bankruptcy Abuse Prevention and Consumer Protection Act of 2005.

1.1.1.5 IV. Key Concepts and Definitions to Communicate to Students

Net interest margin QTL test

Disintermediation Mutual organizations

Regulation Q ceiling U.S. Central Credit Union

Regulatory forbearance Corporate central credit unions

Savings institutions Sales finance institutions

Personal credit institutions Subprime lender

Business credit institutions Loan sharks

Factoring Securitized mortgage assets

Captive finance company Payday lenders

Nonrecourse debt

1.1.1.6 V. Teaching Notes

1. Other Lending Institutions: Chapter Overview

Savings associations and savings banks have traditionally specialized in providing mortgage

credit to individuals. Savings banks have always been better diversified than the more

specialized savings associations. Historically, many banks did not make loans to most

individuals, particularly uncollateralized loans. This lack left a niche for credit unions. Credit

unions evolved to meet consumer credit needs; traditionally these were institutions created by

employers to meet banking needs of their employees on site. This had the dual benefit of

reducing employee requests for salary advances and other loans from the company while also

reducing employee absenteeism since most banks were only open during normal working hours.

Together, savings associations, savings banks and credit unions are often called thrifts. The term

originates from their traditional primary source of funds, the savings of ‘thrifty’ individuals.

Finance companies are another form of specialized lender. Some specialize in lending to

consumers, some are primarily business lenders, and some have been created to assist financing

for specific items their parent manufacturer supplies. The major differences between finance

companies and thrifts are that finance companies do not accept deposits and finance companies

are much less regulated.

2. Savings Institutions

a. Size, Structure, and Composition of the Industry

There were 960 savings institutions (SIs) with $1.059 trillion in assets in 2013. In 1989 there

were 3,677 savings institutions. Thus, by 2013 there were almost 74% fewer SIs, but in terms of

total assets the industry is growing as there were only $905 billion in industry assets in 2001.

SIs traditionally made long term fixed rate mortgages to individuals funded by short term

deposits. This strategy worked reasonably well until the late 1970s. Until then the Federal

Reserve closely targeted interest rates and the yield curve was generally upward sloping.

Beginning in 1979 however, the Fed allowed interest rates to rise to end the inflationary spiral of

the 1970s and SI net interest margins (interest revenue less interest expense divided by earning

assets) became sharply negative as short term rates hit highs of 15% and 16%, while long term

mortgage rates remained much lower. The Federal Reserve’s Regulation Q limited the rates all

DIs could pay on deposits, so SIs were unable to offer attractive interest rates. Money market

mutual fund growth accelerated rapidly as savers withdrew their funds from SIs. This

withdrawal of funds from DIs came to be known as disintermediation. SIs were hurt worse by

disintermediation than banks because SIs did not offer checking accounts at that time, only

savings and CDs. Checking accounts are held for liquidity purposes, savings and CDs are held

for emergency liquidity purposes and to earn a rate of interest. Because of problems in the DI

industry, particularly thrifts, Congress passed the Depository Institutions Deregulation and

Monetary Control Act of 1980 and the Garn-St. Germain Act of 1982. The latter act was

euphemistically known as the ‘S&L savior act.’ Neither act was particularly successful at

stemming the problems at SIs. The acts authorized NOW accounts and MMDA accounts

respectively and broadened the investment and lending powers of SIs.1 Under the increased

1NOW (negotiable order of withdrawal) accounts are interest bearing checking accounts. NOW

accounts were already in use in some states prior to 1980, particularly in the New England area.

Money market deposit accounts (MMDAs) are interest bearing accounts with limited checking

features.

powers industry assets grew rapidly, in part because of excessive risk taking. SIs were largely

locally or regionally based institutions, and when oil prices collapsed, taking many western state

economies with them, many western S&Ls became insolvent and should have been closed.2

Teaching Tip: Political interference (recall the Keating Five3) and a lack of resources encouraged

regulators to not close insolvent institutions in the hope they would be able to turn around their

losses and return to solvency. This was termed regulatory forbearance.

The number of failures continued to grow and eventually the FSLIC (the agency that insured

SIs) went bankrupt. Congress passed the Financial Institutions Reform, Recovery and

Enforcement Act (the aptly named FIRRE Act) in 1989 that abolished the Federal Home Loan

Bank Board (FHLBB) and the FSLIC. The twelve Federal Home Loan Banks remain. The act

created a new supervisory agency, the Office of Thrift Supervision (OTS) that was placed

under the Treasury. A new insurance fund, the Savings Association Insurance Fund (SAIF),

was created and its management given to the FDIC. The Act mandated closure of weak

institutions, recapitalized the insurance funds, constrained thrift investment and lending policies

to hold more mortgage related loans and investments and stiffened penalties for fraudulent

management actions. Thrifts are granted a tax advantage and the ability to obtain funds from

FHLBs if they maintain 65% or more of their loans and investments in mortgage related

activities (called the qualified thrift lender or QTL test). FIRREA increased the minimum

percentage required to pass the QTL test to discourage SIs from engaging in high risk

non-traditional activities such as junk bond investments. At one time SIs held 20% of

outstanding junk bonds.

Teaching Tip: The FHLBB was the main regulatory authority of SIs and the overseer of the

FSLIC. However, the FHLBB had a dual role of regulating and promoting the industry and

preserving its competitiveness relative to the much larger and more powerful banking industry.

Simultaneously promoting and regulating an industry is a difficult mandate, one that proved to

be impossible for the FHLBB. An additional problem was the so-called ‘revolving door’

between regulators and practitioners where practitioners served on the FHLBB for several years

and then went back into industry positions.

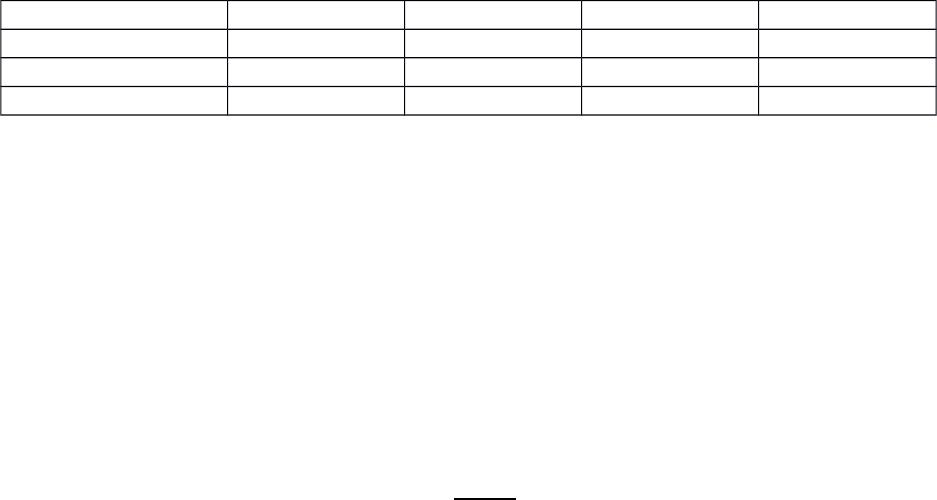

The largest SIs are much smaller than the largest banks and these remain niche institutions.

Industry comparisons

2013, except as

noted Banks* SIs Credit Unions

Finance

Companies

2Texas, Louisiana, and Wyoming were three particularly hard hit states.

3Charles Keating ran Lincoln Savings and Loan in Irvine California. FHLBB auditors

uncovered irregularities in Lincoln’s accounts and evidence of fraud. Five senators, including

John Glenn and John McCain, intervened with the FHLBB on Keating’s behalf to ask that

Lincoln not be closed and that Keating be allowed to continue running the S&L. Lincoln failed

eventually. Keating was convicted and served jail time, and the senators were censured for

improper interference with the regulatory process

Number 5,809 ↓ 960↓ 6,906↓

Total Assets (Bill $) $13,855↑ $1,059.0 ↓ $1,056.0↑ $1,759.4 ↓

ROA 1.00% 1.15 % .88%

Equity% of Assets 11.19% 11.95% 10.20% 13.3%

* First quarter of 2014

The up and down arrows indicate the most recent identifiable trend, if any. Typically the credit

union ROA is lower on average than the ROA for banks and savings institutions, but the average

ROA for large credit unions is often actually greater than the other DIs. Poor profitability at

small credit unions lowers the overall average substantially.

b. Balance Sheets and Recent Trends

Major assets include: (2013)

Cash and securities 12.98%

Mortgages and mortgage backed securities 65.01%

Commercial loans 5.52%

Consumer loans 8.78%

Allowance for loan losses (0.95%)

All Other 8.66%

100.00%

SIs remain nondiversified institutions with a large concentration of assets in mortgages and

mortgage related areas. Indeed the QTL test mandates a lack of diversification. SIs are

consequently likely to experience profit problems when mortgage markets suffer downturns.

The commercial and consumer loan amounts are far under the amounts allowed for SIs under

existing regulations and are less than for banks. SIs have either not been willing or able to

compete with banks for the provision of these services.

Teaching Tip: SI management teams may lack skills necessary to compete with banks,

particularly in commercial lending. They lack business loan analysis and financial statement

analysis expertise. Many SIs lack other aspects of the relationship with corporations, such as a

history of trustworthiness and the ability to provide multiple banking services. Consumer credit

analysis is very important when there is no house for collateral. Consumer loans will also have a

smaller average size than mortgages. This implies that a higher loan volume is required to

generate the same profitability as a mortgage loan. More credit checks, more loans to service and

generally higher collections costs can make consumer loans less appealing to many small SIs.

Major liabilities include (2013)

Total deposits are 76.17% of funds sources. Deposits primarily consist of small time and

savings deposits.

Federal Home Loan Bank and other borrowings comprise about 11.88% of funds sources.

Equity capital is 11.95%, slightly up from 2010 levels.

Most SIs were traditionally mutual associations owned by the depositors as are credit unions.

Today however, the majority have converted to stock ownership in order to raise more capital.

About 55% are stock chartered and these institutions have about 87% of industry assets. The

largest SI used to be Washington Mutual (WaMu) with total assets of $350 billion in 2007

although WaMu was bought out during the financial crisis. The largest remaining SI is USAA

FSB with total assets of $62 billion in 2013. Recall that the four largest banks each have more

than $1 trillion in assets.

Teaching Tip: It is not clear to me that these specialized, underdiversified institutions can or

should continue. Mortgage concentration at banks (and to a lesser extent credit unions) has

increased due to the shrinking thrift industry and strong mortgage markets. SIs that are good at

managing interest rate risk may survive as niche institutions that finance mortgages, probably as

subsidiaries of larger banking entities. I expect that if interest rates continue to rise and the home

buyer’s market continues to struggle for a long period these institutions will face significant

profit pressures.

c. Regulators

The aforementioned Office of Thrift Supervision (a bureau of the U.S. Treasury) examined

and regulated all federal savings institutions until July 21, 2011. The Dodd-Frank bill

consolidated the OTS with the Comptroller of the Currency and then the OTS was eliminated

in October 2011. The thrift charter was not eliminated. The Fed is also now charged with

regulations SI holding companies. Until recently The FDIC managed the Savings Association

Insurance Fund. The SAIF has now been merged with the Bank Insurance Fund to form the

Deposit Insurance Fund (DIF). The FDIC administers the DIF which backs bank and SI

deposits.

State authorities regulate and supervise state chartered thrifts.

d. Savings Institution Recent Performance

Net interest margins, ROA and ROE reached historical highs in the late 1990s, with thrifts

enjoying high ROAs over 1% and ROEs approaching 15%. Profitability fell in 2002, but rose

through 2003. ROE fell somewhat in 2004, but remained high with low interest rates and a

strong housing market. In 2004 average ROA was 1.19% and average ROE was 11.22%. The

flattening and at times inverted yield curve of the mid 2000s reduced thrift profitability. The

subprime mortgage crisis also led to substantial profit problems at many SIs. Loan loss

provisions grew in 2006 and doubled in 2007 dropping ROA from 1.15% to 2005 to 0.77% in

2007. About half of all SIs had a decline in profits between 2006 and 2007. However, capital

ratios remained healthy and only one SI failed in 2007. Performance in the late 2000s dropped

due to the recession. In 2008 net income was -$8.6 billion, the first negative annual earnings

since 1991. ROA was -0.72%. SI performance improved in 2009 along with the economy, by

the first quarter of 2010 ROA was back to 0.65% and ROE was 5.85%. In 2013 ROA improved

to 1.15% and ROE to 9.66% as the economy and housing improved. Nevertheless, asset growth

rates have been negative from 2008 through 2013.

Like banking, industry consolidation is occurring in the thrift industry. Larger institutions have

been more profitable and are increasingly dominating the industry in terms of asset size. As of

2013, the largest 2.0% of SIs control about 53% of industry assets. Finally, most SIs have little

or no foreign exposure and they have not suffered from international crises.

3. Credit Unions

Credit unions are nonprofits mutually owned by their depositors. Credit unions cannot serve the

general public as members must have a common bond in order to join. Traditionally most credit

unions were employer based. Even today many credit unions are sponsored by a corporation or

government employer. The sponsor often donates land, money and/or expertise to assist in the

formation of the credit union. Credit unions are not taxed and as they do not compete with one

another due to the common bond requirement, they are exempt from anti-trust prohibitions.

Credit unions can and do act cooperatively and pool funds for their mutual benefit.

a. Size, Structure, and Composition of the Industry

In 2010 there were 7,598 credit unions (CUs) with assets of $916.1 billion. In 2013 there were

6,906 CUs with total assets of $1,056.0 billion.4 In 2013 there were more than 95.2 million

members of credit unions. The industry has a strong trade association and lobby group. With

growing bank fees, CU membership growth rates increased dramatically in 2012. Even though

the industry is growing in asset size, and they have a large membership, credit unions are very

small compared to banks and other thrifts. The average size credit union is $152.9 million as

compared to $2,209.4 million for banks. The largest credit union is the Navy Credit Union at

$54.3 billion in assets.

Credit unions were not badly affected by the interest rate volatility of the 1980s because they did

not have a large maturity imbalance, at that time they did not hold many mortgage loans.

Structure of the Industry:

Credit Union National Association (CUNA) – CUNA is a lobby group and trade

association that provides advice and has helped organize some other groups designed to

benefit credit unions. For example, CUNA helps CUs sell mortgages they have originated,

provides mutual fund investments, provides data processing services and marketing

expertise.

Corporate Central Credit Unions (CCCU) – There are 16 CCCUs organized on a regional

basis cooperatively owned by their member credit unions. CCCUs pool individual credit

union’s funds and invest them in securities markets. This allows small member CUs to enjoy

economies of scale in investing and reduces the level of expertise required at individual CUs.

CCCUs also make seasonal and other short term loans to individual credit unions that may

need cash due to layoffs, strikes, Christmas, etc. The CCCUs provide check clearing

services, data processing, accounting and payment services and informational seminars to aid

CU managers.

The U.S. Central Credit Union: This is a bank in Kansas. It acts as a bank to the corporate

central credit unions. It coordinates credit card services, provides international and large

scale investments and taps international sources of funds which are funneled to the CCCUs

and eventually to local credit unions.

In recent years the most rapidly growing form of credit union has been community based credit

unions. The common bond usually must be a common employer, common association or

common locality. Prior to the 1980s the common bond was interpreted narrowly and location

based credit unions were the least common. Now credit unions can have multiple common

bonds, once one is a member of a credit union they can be a member for life, and some location

4 It is interesting to note that the credit union industry’s total assets are less than the total assets

of even one of the largest banks.

based credit unions have become large enough to compete with banks. Because credit unions are

not taxed and don’t have a profit goal, they can offer better loan and/or deposit rates to members

than banks can offer. The banking industry has recently filed lawsuits claiming that credit unions

were unfairly competing with banks. The banks argue that the credit unions’ tax exemption is

equivalent to a $1 billion subsidy per year. CUNA claims that even if that is so, the value to each

credit union member is between $200 and $500 per year. With 90+ million members, this

amounts to $18 billion to $46 billion per year, a good return for the subsidy. The courts sided

with the banks in several lawsuits and attempted to limit access to credit unions, but Congress

effectively removed the restriction imposed by the courts. This issue will probably be revisited in

the future as the credit union industry continues to grow and credit unions expand their product

offerings. Certain employer based credit unions now offer business loans to employer groups,

adding another product line traditionally held by the banks. The growing level of competition

aside however, credit unions remain a cottage industry compared to banks.

b. Balance Sheets and Recent Trends

Credit union’s major assets include (2013):

Cash & govt. investments 29.5%

Other investment securities 3.4%

Consumer loans 24.3%

Home mortgages & MBS 32.5%

Teaching Tip: The investment portfolio is generally of lower default risk and much more liquid

than the investment portfolio of a bank or SI. The loan portfolio is predominantly short term,

although credit unions now hold substantial mortgage loans that could hurt profitability if

interest rates rise precipitously. Note that the bulk of the loans are to members. If an employer

or a region has protracted difficulties, the solvency of the credit union could be imperiled. One

of the functions of the cooperative structure is to assist troubled credit unions in such situations.

Major credit union liabilities include:

Member deposits 86.2%

NOW accounts 11.3%

Small Time & Savings 67.9%

Large Time 7.0%

Other liabilities 3.6%

Reserves and Undivided Earnings 10.2%

Credit unions rely on member deposits for 86% of funds, a higher percent than either banks or

SIs. Reserves and undivided earnings are equity. Credit unions have a slightly lower amount of

equity than banks and other thrifts.

Teaching Tip: Deposits at a credit union are called shares since depositors are the shareholders

(owners). Regular shares are passbook savings, share drafts are NOW accounts and share

certificates are CDs. The majority of small credit unions do not offer share drafts.

c. Regulators

National Credit Union Administration (NCUA) Board – This is the primary regulatory

body of national credit unions. The NCUA charters, insures, regulates and examines

federally chartered and/or federally insured credit unions. The NCUA is also charged with

promoting the growth and welfare of the industry. The NCUA sets maximum loan rates for

CUs and in 1982, the NCUA eliminated all deposit rate ceilings and weakened the common

bond requirement. The NCUA instituted more formal risk assessment ratings for CUs in

1987.

National Credit Union Share Insurance Fund (NCUSIF) – Created in 1970, the NCUSIF

insures member credit union deposits up to $250,000 per account.

Teaching Tip: Although this is no longer likely to be a problem since 98% of credit union

deposits have NCUSIF insurance, you may wish to warn students never to put their money in an

institution that does not have federal insurance. Since depositors are shareholders they could

lose their deposits in the event of failure of an uninsured institution.

d. Industry Performance

ROA at credit unions can (theoretically) be higher than at banks or other thrifts due to the tax

advantage credit unions enjoy. Smaller credit unions have disadvantages due to lack of

economies of scale, less highly trained management, non-business professionals on the board of

directors and a lack of loan demand and thus their profitability (2013 ROA of 0.11%) can be

correspondingly low. Larger credit unions tend to have higher profit ratios. Assets of the largest

credit unions have been growing at about 20% per year.

Corporate central credit unions, CCCUs, were badly hurt during the financial crisis due to their

holding of MBS. The NCUA was forced to bailout two CCCUs and to purchase the bulk of

overall CCCU holdings of MBS, about $50 billion worth. As a result of the crisis, five of the

largest corporate credit unions were declared insolvent.

Teaching Tip: Although efficient utilization of assets is important, profitability should not be the

primary goal of a credit union. When a credit union allows this to become the primary goal, they

are abusing their special tax status. As credit unions seek to grow, a profit goal can defacto

emerge as the top priority. In the author’s experience, some credit unions are banks hiding under

a different name. Not all credit unions treat customers any better than banks (which can be quite

bad), and not all offer better loan or deposit rates.