4. a. Reserve requirements = (0 x $12.4m) + ($79.5m – $12.4m)(0.03) + ($325m – $79.5m) (0.10) = 0 + $2.013m +

$24.550m = $26.563 million

5. a. Average daily net transaction accounts = (300m + 250m + 280m + 260m + 260m + 260m + 280m + 300m +

270m + 260m + 250m + 250m + 250m + 240m)/14 = 3,710m/14 = 265m

b. Average vault cash and reserves maintained = $22.7m + $2m = $24.7m

6. a. The CET1 risk-based ratio is ($45 + $40)/$1,090 = 0.07798 or 7.798 percent.

c. The total risk-based capital ratio = ($45 + $40 + $25)/$730 = 0.15068 or 15.068 percent.

7. Basel III introduced a capital conservation buffer designed to ensure that DIs build up a capital surplus, or buffer,

outside periods of financial stress which can be drawn down as losses are incurred during periods of financial stress.

The buffer requirements provide incentives for DIs to build up a capital surplus (e.g., by reducing discretionary

To have no limitations on the bank’s payout ratio, the CET1 ratio must be > 7%, the Tier I ratio must be > 8.5%, and

8. a. CET1 capital decreases to $400,000, Tier I capital decreases to $450,000 and total capital decreases to

b. The risk weight for category 1 mortgages with a loan-to-value ratio of 80 percent is 50 percent. Thus,

d. CET1 equity increases to $1.3 million, Tier I equity increases to $1.35 million, and total capital increases to

e. CET1 and Tier I capital are unchanged. Total capital increases to $1.95 million. General obligation municipal

bonds fall into the 20 percent risk category. So, risk-weighted assets increase to $10 million + $1 million (0.2) =

f. The category 1 mortgage loans with loan-to-value ratios of 40 percent have a risk weight of 35 percent. The

ATMs are 100 percent risk weighted. Thus, risk-weighted assets increase to $10 million – $4 million (0.35) + $2

9. a. Risk-adjusted assets:

Cash 0 x 21 = $0

b. Standby LCs: $30 x 0.50 x 1.0 = $15 = $15

Foreign exchange contracts:

Potential exposure $40 x 0.05 = $2

Total risk-adjusted on- and off-balance-sheet assets = $133.50

x 0.045

c. No, the bank does not have sufficient total capital to meet the Basel requirements. It needs CET1 capital of

$6.0075 million, Tier I capital of $8.01 million, and total capital of $10.68 million. The bank has $5 million of CET1

If the bank issues $1.0075 million in CET1 capital, it will need $0.0025 million in additional Tier I capital, and no

A new balance sheet after the issuance of the new required equity is shown below. You will note that the total capital

exceeds the minimum of $10.68 million.

New balance sheet:

Cash $22.01 Deposits $176

d. Total risk-adjusted on- and off-balance-sheet assets = $133.50

x 0.070

No, the bank does not have sufficient total capital to meet the Basel requirements. It needs CET1 capital of $9.345

If the bank issues $4.345 million in CET1 capital, it will need $0.0025 million in additional Tier I capital, and no

New balance sheet:

Cash $25.3475 Deposits $176

10. a. Risk-adjusted on-balance-sheet assets: $21 x 0 = $0

b. Standby LCs: $20 x 1.0 = $20 x 1.0 = $20

Foreign exchange contracts:

x 0.045

CET1 capital required $5.31

x 0.06

c. No, the bank does not have sufficient total capital to meet the Basel requirements. It needs CET1 capital of $5.31

million, Tier I capital of $7.08 million, and total capital of $9.44 million. The bank has $6 million of CET1 capital

A new balance sheet after the issuance of the new required equity is shown below.

Assets Liabilities and Equity

Cash (0%) $22.44 Deposits $133

d. Total risk-adjusted on- and off-balance-sheet assets = $118

x 0.070

No, the bank does not have sufficient total capital to meet the Basel requirements. It needs CET1 capital of $8.26

Capital conservation buffer must be met with CET1 capital. Thus, if the bank issues $4.03 million in CET1 capital,

A new balance sheet after the issuance of the new required equity is shown below.

Assets Liabilities and Equity

Cash (0%) $25.39 Deposits $133

11. Risk weight

a. $10 million cash reserves. 0% $0

d. $5 million U.K. government bonds,

OECD CRD rated 1 0 $0

h. $2 million loan to foreign bank, OECD rated 3 50 $1 million

j. $10 million 1-4 family home mortgages, 200 $20 million

category 2, loan-to-value ratio 95%

m. $500 million commercial and industrial

loans, B- rated 100 $500 million

credit equivalent amount

o. $100,000 performance-related standby

letters of credit to a municipality issuing

general obligation bonds 50 20 $10,000

s. $17 million three-year loan commitment

to a private agent 50 100 $8.5 million

potential current

exposure exposure

v. $4 million five-year interest rate swap

with no current exposure 5% $0 100 $20,000

12.

On Balance Sheet Items Face Value Weight Value

Cash $121,600 0% $0

Short-term government securities (<92 days.) 5,400 0% $0

Long-term government securities (>92 days) 414,400 0% $0

Conversion Face Credit-Equivalent Risk-Adjusted

Off Balance Sheet Items: Factor Value Amount Asset Value

U.S. Government Counterparty

Loan commitments:

< 1 year 20% $300 $60 $0

1-5 year 50% 1,140 570 0

U.S. Depository Institutions Counterparty

Loan commitments:

< 1 year. 20% 100 20 4

> 1 year 50% 3,000 1,500 1300

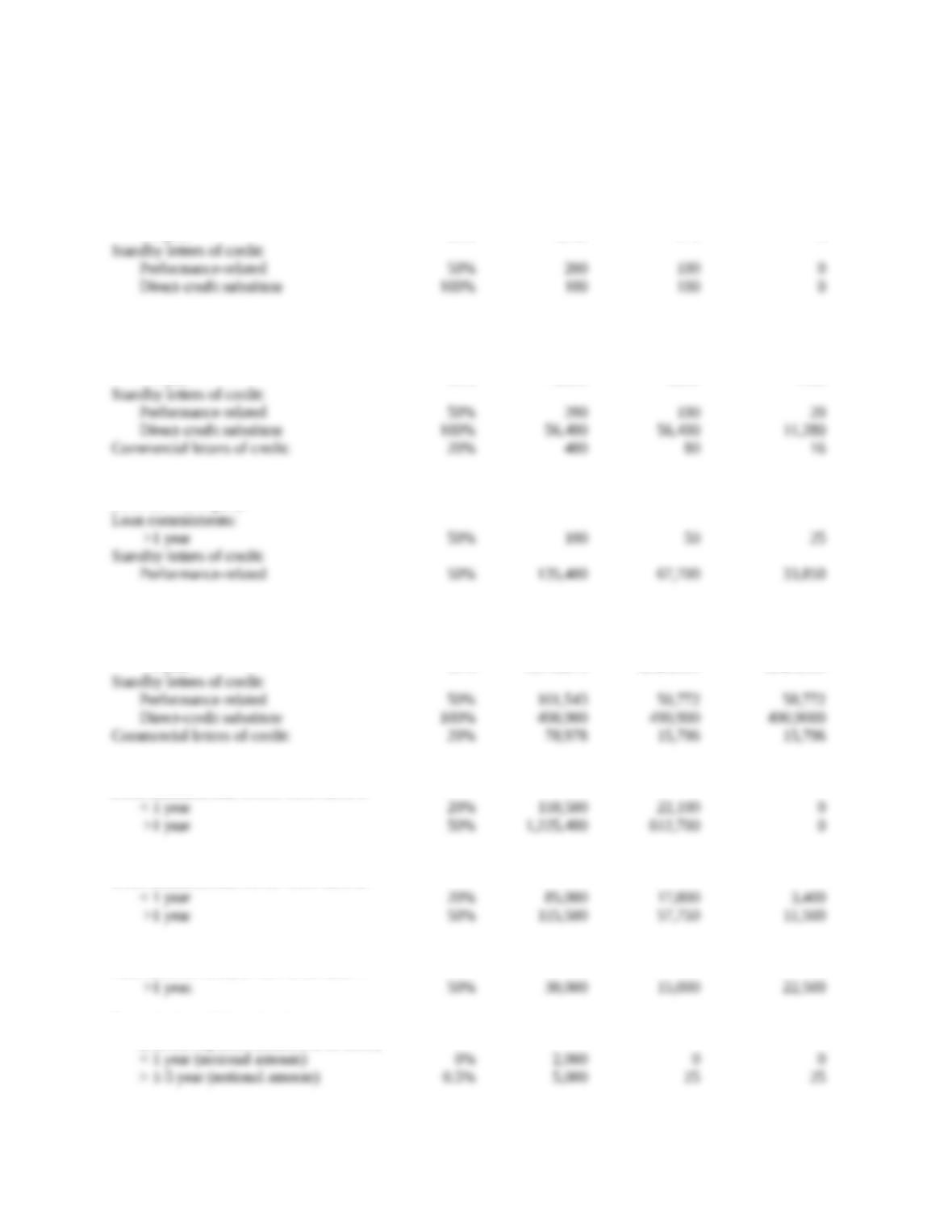

State and Local Government Counterparty

(revenue municipals)

Corporate Customer Counterparty

Loan commitments:

< 1 year 20% 3,212,400 642,480 642,480

>1 year 50% 3,046,278 1,523,139 1,523,139

Sovereign Counterparty

Loan commitments, OECD CRC rated 1:

Sovereign Counterparty

Loan commitments, OECD CRC rated 2:

Sovereign Counterparty

Loan commitments, OECD CRC rated 7:

Interest rate market contracts:

(current exposure assumed to be zero.)

The risk-adjusted asset base under Basel III is:

13. Under Basel III: CET1 = 4.5% capital requirement x $11,077,606 = 498,492

14. The bank has $13,731,769 in total on-balance-sheet assets, $8,693,839 in off-balance sheet lending

15. CET1 capital = $225,000 + $200,000 + $565,545 = $990,545; Tier I capital = $990,545 + $50,000 = 1,040,545;