Answers to Chapter 13

Questions:

1. Regulators have issued several guidelines to insure the safety and soundness of CBs:

ii. CBs are required to maintain minimum amounts of capital to cushion any unexpected losses. In the case of

banks, the Basle standards require a minimum core and supplementary capital of 8% of their risk-adjusted assets.

2. The United States has experienced several phases of regulating the links between the commercial and investment

banking industries. After the 1929 stock market crash, the United States entered a major recession and

approximately 10,000 banks failed between 1930 and 1933. A commission of inquiry (the Pecora Commission)

For most of the 1933-1963 period, commercial banks and investment banks generally appeared to be

willing to abide by the letter and spirit of the Glass-Steagall Act. Between 1963 and 1987, however, banks

With this onslaught and the de facto erosion of the Glass-Steagall Act by legal interpretation, the Federal

Reserve Board in April 1987 allowed commercial bank holding companies to establish separate Section 20 securities

Significant changes occurred in 1997 as the Federal Reserve and the Office of the Comptroller of the Currency

(OCC) took action to expand bank holding companies= permitted activities. In particular, the Federal Reserve

In 1999, after years of “homemade” deregulation by banks and securities firms, regulators passed the Financial

Services Modernization Act which eliminated the Glass-Steagall barriers between commercial banks and investment

banks (as well as insurance companies). The bill allowed national banks to place certain activities, including

After the passage of FSMA, the two industries came together to a degree. Commercial banks like Bank of

America and Wachovia tried to build up their own investment-banking operations, but they did not have much

success in eating into the core franchises of the five big independent investment banks: Merrill Lynch, Goldman

Sachs, Morgan Stanley, Lehman Brothers, and Bear Stearns. Generally, the investment banks, which were not

Of the five major independent investment banks that existed a year earlier, only two─Goldman Sachs and Morgan

Stanley─remained. Even Goldman Sachs and Morgan Stanley were facing a severe liquidity crisis during the

weekend of September 20-21, 2008. To address the crisis, one week after the closure of Lehman Brothers and the

subjecting themselves to more regulation, the companies would have access to the full array of the Federal Reserve’s

lending facilities. For example, as bank holding companies, Morgan and Goldman will have greater access to the

As part of the increased authority given to the Federal Reserve in the 2010 Wall Street Reform and

Consumer Protection Act, the Fed proposed in late 2011 that net credit exposures between any two of the nation’s six

largest financial firms would be limited to 10 percent of the company’s regulatory capital. Other financial firms

3. a. Yes, the bank is in compliance with the laws. The Financial Services Modernization Bill of 1999 allows

commercial banks and investment banks to own each other with no limits on income.

4. The Financial Services Modernization Act of 1999 completely changed the landscape for insurance activities as it

allowed bank holding companies to open insurance underwriting affiliates and insurance companies to open

commercial bank as well as securities firm affiliates through the creation of a financial service holding company.

With the passage of this Act banks no longer have to fight legal battles to overcome restrictions on their ability to

sell insurance in these states. The insurance industry also applauded the Act as it forced banks that underwrite and

5. The likely effect of this situation is to strengthen the banks’ case for deregulation and increased ability of

commercial banks to offer more financial services such as investment banking, brokerage, and insurance.

6. The main feature of the Riegle-Neal Act of 1994 is the removal of barriers to interstate banking. As of September

7. Under the Federal Deposit Insurance Reform Act of 2005, beginning in January 2007, the FDIC began

calculating deposit insurance premiums based on a more aggressively risk-based system. Further, under the act, if

the reserve ratio drops below 1.15 percent—or the FDIC expects it to do so within six months—the FDIC must,

percent.

8. Holding relatively small amounts of liquid assets exposes a CB to increased illiquidity and insolvency risk.

Excessive illiquidity can result in a CB’s inability to meet required payments on liability claims (such as deposit

withdrawals) and, at the extreme, its insolvency. Moreover, it can even lead to contagious effects that negatively

impact other CBs. Consequently, regulators impose minimum liquid asset reserve requirements on CBs. In general,

9. The Basle Agreement identifies the risk-based capital ratios agreed upon by the member countries of the Bank for

10. The major feature of the Basle Agreement is that the capital of banks must be measured as an average of

credit-risk-adjusted total assets both on and off the balance sheet.

11. The FDIC Improvement Act (FDICIA) of 1991 required that banks and thrifts adopt risk-based capital

requirements. Consistent with this act, U.S. DI regulators formally agreed with other member countries of the Bank

In 2001, the BIS issued a Consultative Document, “The New Basel Capital Accord,” that proposed the

incorporation of operational risk into capital requirements and updated the credit risk assessments in the 1993

agreement. The new Basel Accord or Agreement (called Basel II) allowed for a range of options for addressing both

Basel III was passed in 2010 (fully effective in 2019). The goal of Basel III is to raise the quality, consistency,

and transparency of the capital base of banks to withstand credit risk and to strengthen the risk coverage of the

12. Since December 18, 1992, under the FDICIA legislation, regulators must take specific actions−prompt corrective

action (PCA)−when a DI falls outside the zone 1, or well capitalized, category. Table 13-5 summarizes these

regulatory actions. Importantly, the prompt corrective action provision requires regulators to appoint a receiver for

13. Under Basel III, depository institutions must calculate and monitor four capital ratios: common equity Tier I

(CET1) risk-based capital ratio, Tier I risk-based capital ratio, total risk-based capital ratio, and Tier I leverage ratio.

i) Common equity Tier I risk-based capital ratio = Common equity Tier I capital/credit risk-adjusted assets

14. Under the Standardized Approach, the Basel III leverage ratio is defined as the ratio of Tier 1 capital to

on-balance-sheet assets. Under the Advanced Approach, Basel III leverage ratio is defined as the ratio of Tier I core

capital divided by the book value of total exposure. Total exposure is equal to the DI’s total assets plus

15.

Zone 1: Well capitalized. The total risk-based capital ratio (RBC) ratio exceeds 10 percent. No regulatory action

is required.

Zone 3: Undercapitalized. The RBC ratio exceeds 6 percent, but is less than 8 percent. Requires a capital

Zone 4: Significantly undercapitalized. The RBC ratio exceeds 2 percent, but is less than 6 percent. Same as

16. CET1 is primary or core capital of the DI. CET1capital is closely linked to a DI’s book value of equity,

reflecting the concept of the core capital contribution of a DI’s owners. CET1 capital consists of the equity funds

Tier I capital is the primary capital of the DI plus additional capital elements. Tier I capital is the sum of CET1

capital and additional Tier I capital. Included in additional Tier I capital are other options available to absorb losses

Tier II capital is supplementary capital. Tier II capital is a broad array of secondary “equity like” capital resources. It

17. The two components are credit risk-adjusted on-balance-sheet assets and credit risk-adjusted off-balance-sheet

assets.

in many instances, stricter than regulations abroad, this reduces the attractiveness of opening full scale branches of

foreign banks in the U.S. Foreign banks will have to justify continued activity in the U.S. market on the grounds of

19. The main features of the Foreign Bank Supervision Enhancement Act of 1991 are:

i. All foreign banks need the approval of the Fed to open new branches or subsidiaries. At the minimum, they need

to satisfy two criteria: first, the regulator of the home country must supervise its activities on a consolidated basis,

20. The Federal Deposit Insurance Reform Act of 2005 instituted a deposit insurance premium scheme, effective

January 1, 2007 that combined examination ratings, financial ratios, and for large banks (with total assets greater

than $10 billion) long term debt issuer ratings. The new rules consolidate the existing nine risk categories into four,

named Risk Categories I through IV. Risk Category I contains all well-capitalized institutions in Supervisory Group

21. Within Risk Category I, the final rule combines CAMELS component ratings with financial ratios to determine

an institution’s assessment rate. For large institutions that have long term debt issuer ratings, the final rule

differentiates risk by combining CAMELS component ratings with these debt ratings. For Risk Category I

institutions, each of five financial ratios component ratings will be multiplied by a corresponding pricing multiplier,

22. With these CAMELS rating and capital ratios, Webb Bank falls into the Category II risk category and has a

deposit insurance assessment rate of 14 basis points per $1 of assessment base (total assets minus tangible equity).

23. Residential 1-4 family mortgages would be separated into two risk categories (“category 1 residential mortgage

exposures” and “category 2 residential mortgage exposures”). Category 1 residential mortgages include traditional,

first-lien, prudently underwritten mortgage loans. Category 2 residential mortgages include junior liens and

24. Risk weights for sovereign exposures are determined using OECD Country Risk Classifications (CRCs). A

sovereign is a central government (including the U.S. government) or an agency, department, ministry, or central

bank of a central government. The OECD’s CRCs assess a country’s credit risk using two basic components: the

0 percent, while countries assigned to category 7 having the highest possible risk assessment and are assigned a risk

weight of 150 percent. The OECD provides CRCs for more than 150 countries. Assessments are publicly available

25. Basel III introduced a capital conservation buffer designed to ensure that DIs build up a capital surplus, or

buffer, outside periods of financial stress which can be drawn down as losses are incurred during periods of financial

stress. The buffer requirements provide incentives for DIs to build up a capital surplus (e.g., by reducing

discretionary distributions of earnings (reduced dividends, share buy-backs and staff bonuses)) to reduce the risk

Basel III also introduced a countercyclical capital buffer which may be declared by any country which is

experiencing excess aggregate credit growth. The countercyclical buffer can vary between 0 percent and 2.5 percent

of risk-weighted assets. This buffer must be met with CET1 capital and DIs are given 12 months to adjust to the

buffer level. Like the capital conservation buffer, if a DI’s capital levels fall below the set countercyclical capital

26. The reserve maintenance period would extend from June 17 through June 30. It starts 30 days later than the start

Problems:

1. To determine the deposit insurance assessment for each institution, we set up the following tables:

CAMELS Components:

Weighted Average CAMELS

Component 1.40 1.65

Base Assessment Rates for Two Institutions

Contribution Contribution

Risk to Risk to

Pricing Measure Assessment Measure Assessment

Multiplier Value Rate Value Rate

Uniform Amount 4.861 4.861 4.861

Tier I leverage ratio (%) (0.056) 8.62 (0.483) 7.75 (0.434)

Net income before

taxes/risk-weighted

assets (%) (0.764) 2.15 (1.643) 1.86 (1.421)

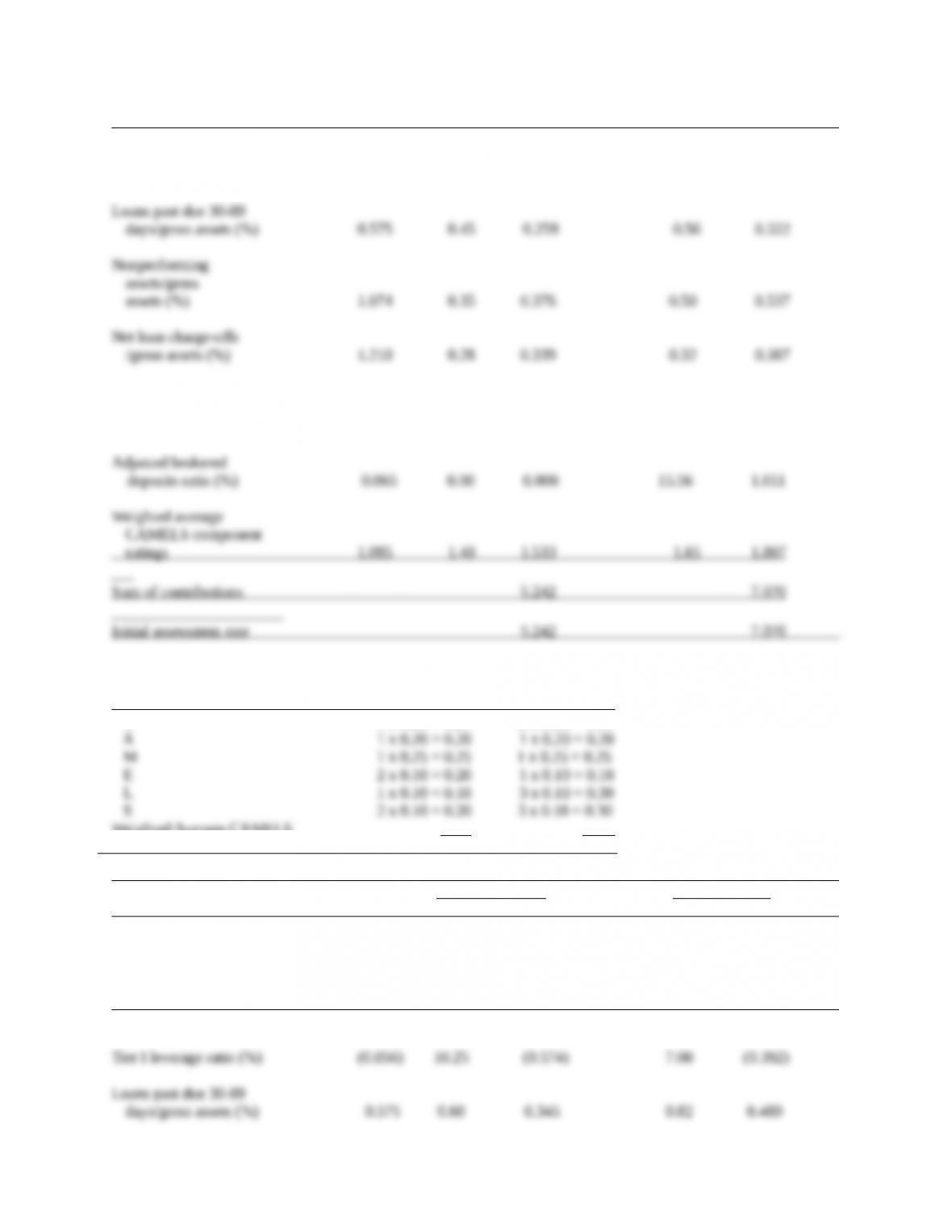

2. To determine the deposit insurance assessment for each institution, we set up the following tables:

CAMELS Components:

C 1 x 0.25 = 0.25 2 x 0.25 = 0.50

Weighted Average CAMELS

Component 1.20 1.65

Base Assessment Rates for Two Institutions

A B C D E F

Institution 1 Institution 2

Contribution Contribution

Risk to Risk to

Pricing Measure Assessment Measure Assessment

Multiplier Value Rate Value Rate

Uniform Amount 4.861 4.861 4.861

Nonperforming

assets/gross

assets (%) 1.074 0.45 0.483 0.90 0.967

Adjusted brokered

deposits ratio (%) 0.065 0.00 0.000 25.89 1.683

For Institution A, the sum is 4.692. However, the minimum assessment rate for Category I banks is 5 basis points.

3. a. Reserve requirements = (0 x $12.4m) + ($79.5m – $12.4m)(0.03) + ($225m – $79.5m) (0.10)

b. The average daily balance over the maintenance period was $10 million. Therefore, average reserves held were

short $1.563million.

c. For the 14-day period, the cumulative sum of its daily average net transaction accounts is = $225m x 14 =

Reserve requirements = (0 x $12.4m) + ($79.5m – $12.4m)(0.03) + ($210m – $79.5m) (0.10) = 0 + $2.013m +