1. Balance Sheet Regulations

a. Regulations on Commercial Bank Liquidity

Under Federal Reserve Regulation D banks are currently required to meet minimum liquid asset

requirements to back transactions deposits. Since 1980 all DIs must back their net transactions

deposits with reserves held at the Federal Reserve.1

Appendix 13D: Deposit Insurance Coverage for Commercial Banks in Various Countries

(available on Connect or from your McGraw-Hill representative)

Text Appendix 13D contains a detailed example of calculating reserve requirements.

Transaction accounts are demand deposits, NOW accounts and share drafts (offered by

credit unions).

The computation period is the length of time over which the level of required reserves is

calculated. In the U.S. the reserve computation period begins on a Tuesday and ends on a

Monday 14 days later. Thus the U.S. uses a two week computation period. The minimum

daily average reserve level that a bank must maintain is computed as a percentage of the

daily average net transaction accounts held by the bank over the two week computation

period. Friday’s balances are carried over for Saturday and Sunday so Friday’s balance

counts for three days. Smart bankers can attempt to lower deposits on Friday by say, sending

them to overseas affiliates, and reversing them on Monday. This reduces the average daily

balance by the amount sent times 2/14 and is called the ‘weekend game.’

The first $12.4 million of net transaction accounts carry a 0% reserve requirement, amounts

from $12.4 million to $79.5 million carry a 3% reserve requirement and all amounts over

$79.5 million require a 10% reserve requirement. Suppose that a bank has average daily

gross transaction deposits of $1,650 million, including $150 million in its own deposits

elsewhere and in currency in the process of collection (CIPC) so that net transaction accounts

are $1,500 million. The minimum average reserves the bank must hold is:

Net Transaction Accounts % Reserve Req. Daily Avg. Required

The first $12.4 million @ 0% $ 0.00

$79.5 – $12.4 = $67.1 million @ 3% $ 2.01

Amount > $79.5 million = $1420.5 million @ 10% $142.05

Minimum required daily average balance $144.06 mill.

The reserve maintenance period is the 14 day period over which the bank must maintain a

daily average balance of reserves (reserves at the Fed and cash) equal to the calculated

amount or more. The reserve maintenance period begins 30 days after the beginning of the

reserve computation period. For this reason this system is called a lagged reserve

accounting system. The U.S. switched from a contemporaneous reserve accounting

system in 1998. Thus the bank manager knows exactly the value of the minimum reserve

target throughout the entire maintenance period. This allows managers to allow the reserves

held to fall below the required minimum on any given day. They can easily calculate the

required levels on the days remaining so that the average daily balance will still meet the

1 Very small institutions are exempt.

required daily average balance.

b. Regulations on Capital Adequacy (Leverage)

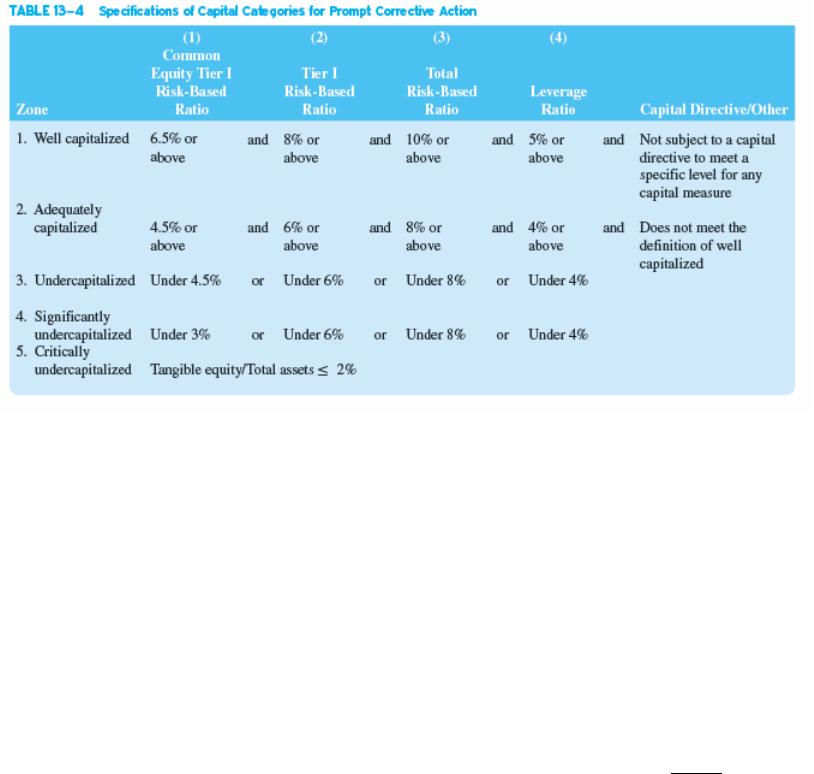

The FDICIA requires banks and thrifts to meet identical risk based capital requirements. FDICIA

requires regulators to mandate prompt corrective actions (PCA) if a bank falls below the well

capitalized criteria. The list of categories is provided in Text Table 13-4 and the recommended

actions are provided in Text Table 13-5. Primary or ‘core’ capital consists of common equity,

called Common Equity Tier 1, or CET1, additional Tier 1 capital and Tier II capital. Detailed

definitions are provided in text Table 13-16. CET1 is basically common stock and retained

earnings less goodwill. Additional Tier I capital consists primarily of perpetual items although

they may be callable after 5 years if replaced with “better” capital and noncumulative perpetual

preferred stock. Tier II capital includes subordinated debt and other general bank creditors,

preferred stock, allowance for loan and lease losses (max 1.25% of risk weighted assets) and

some other exceptions that may be allowed by the regulators.

In February 2009 the Obama administration announced stress tests of the 19 largest U.S. banks

to see if bank capital was sufficient to handle a ‘worst case’ economic scenario of unemployment

remaining over 10% and home prices falling another 25%. The tests revealed that 10 of the 19

institutions needed to raise capital worth a total of $74.6 billion, which they promptly did. The

stress test results are presented in text Table 13-6.

Teaching Tip: The 1989 Basle Accord did three things:

1. Defined what banks could count as capital.

2. Increased the amount of capital a bank is required to hold by requiring stricter

minimum capital/asset ratios.

3. Made the required capital levels reflect the risk of the institution.

Many banks had to raise more equity capital. How could they do this?

Sell new shares

Reduce dividends

Reduce amount of risky assets

Increase profit margin on loans – e.g. credit cards and check fees. This is one reason why

credit card loan rates were so slow to fall in the 1990s as interest rates declined.

An interesting question to pose is to ask how much the Basle Accord affected the U.S. and global

economy in the 1990s. U.S. banks, under pressure to improve capital and under fire for loan

quality, were perhaps less likely to lend. This may have worsened the recession of 1990. Japan’s

banking woes were brought to light by the stricter capital standards required under the Basle

agreement. It is at least worth mentioning that care must be taken when changing regulations for

a country’s largest intermediary in order to prevent unintended consequences.

Teaching Tip:

With no risk adjustment, all banks had the same capital requirement, but not all

banks had the same risk. Because higher risk banks did not have to hold more capital, there was

no penalty for additional risk. Normally, capital markets would discipline banks to limit the

amount of financial leverage used by requiring higher borrowing rates. Two different conditions

in the banking industry created a market failure however: deposit insurance and the ‘Too Big

To Fail’ practices of the regulators.

Teaching Tip: There is a conflict between regulators and managers over capital levels.

Bank managers prefer low levels of capital to increase ROE, and bank regulators prefer higher

levels of capital to reduce insolvency risk. Historically, bank capital/asset ratios had been in the

5-8% range, at times dropping below 5%. In the early 1980s capital requirements were actually

reduced from 4% to 3% at thrifts! These high debt levels leave little room for error. The

regulators knew that the U.S. needed higher capital requirements and needed capital requirement

which accounted for different risk of banks. Nevertheless, the U.S. was reluctant to require them

unless other countries imposed similar requirements, otherwise U.S. banks would have faced a

higher cost of funds than foreign banks. Hence, the international capital agreement, the Basle

Accord was created. Signers include the U.S., Canada, France, Germany, Italy, Belgium, Japan,

Luxembourg, Netherlands, Sweden, Switzerland, and the United Kingdom.

Simply examining a capital to asset ratio is an insufficient measure of the adequacy of capital to

protect against losses for three reasons:

1. The capital to asset ratio (leverage ratio) is based on book values and the market value of

equity may be substantially negative,2 even though the institution has a positive leverage ratio.

This in fact happened at many S&Ls in the 1980s.

2. A simple leverage ratio fails to consider the different risk levels of different assets.

3. The leverage ratio fails to capture the risk of off-balance-sheet activities.

As a result of these failings, the Basel Accord developed risk based capital requirements.

Basel II updated the credit risk assessments and formally instituted three ‘pillars’ of capital

regulation. The crisis revealed problems with Basel II and Basel 2.5 was passed in 2009

(effective as of 2013). The purpose of 2.5 was to update capital required to back trading

operations. In September 2010, the Bank of International Settlements (BIS), an international

agency that promotes standard global banking rules, revised the capital requirements, resulting in

Basel III. The minimum leverage ratio was increased from 2% to 4.5% and a capital

conservation buffer of 2.5% which has to be met with common equity was introduced. This

buffer may be drawn down during tough economic times. This requirement is to be phased in

between 2016 and 2019. Thus the total common equity requirement will eventually be 7%. Tier

1 capital requirements were also increased from 4% to 6%. These requirements are phased in by

January 2015. Finally a countercyclical buffer requirement of 0 to 2.5% may be instituted on a

country by country basis as needed. See the table below. The more detailed phase in schedule is

provided in Text Table 13-3.

Text Table 13-4 Calibration of the Capital Framework (all numbers in percent)

Common Equity

(after deductions) Tier I Capital Total Capital

Minimum 4.5 6.0 8.0

Capital

Conservation buffer

2.5

Minimum plus

conservation buffer

7.0 8.5 10.5

2This implies that upon liquidation the deposit insurance agency will be unable to fully recover

payouts to depositors from sale of the assets.

Countercyclical

capital buffer

0.0-2.5

Basel III also requires a Common Equity Tier I surcharge on certain banks determined to be

globally systemically important banks (G-SIBs). A bank is labeled a G-SIB if its failure or

distress has the potential to disrupt the global financial system or economic activity. These banks

are considered too big to fail and would have to be bailed out if necessary. This surcharge is

between 1 and 3.5% over the 7.0% minimum CET1 ratio. There are 29 designated G-SIBs as of

this writing (27 were designated by the BIS and 2 by the bank’s local regulators). The list is in

text Table 13-7. The list is updated every three years and it is anticipated that eventually the list

will include non-banks.

Appendix 13E: Calculating Risk-Based Capital Ratios

Text Appendix 13E contains the details of calculating risk based capital ratios. We are now up to

Basel III, the third version of the international capital accord promulgated by the BIS.

Basle Accord I defined two types of capital: Tier 1 or ‘core’ capital and Tier 2 or ‘supplemental

capital.’

Tier 1 (Core) capital:”No Contractual Obligated Payments”

» Common Equity, including Retained Earnings (Must be 4% of Risk Weighted

Assets (RWA) (RWA is defined below)

Subject to regulatory approval:

» Qualifying cumulative and noncumulative perpetual preferred stock (and surplus)

{No more than 25% of the sum of the other Tier 1 elements}

The defining characteristic of Tier 1 capital is that the bank cannot be sued for nonpayment on

any of these accounts, and no principle payments are due on them.

Tier 2 or Supplemental Capital (major components)

Allowance for loan and lease losses Up to 1.25% of RWA

Perpetual preferred stock not counted in Tier 1.

Subordinated debt and finite lived preferred stock maturing no sooner than 5 years.

{Maximum amount that can be counted is 50% of Tier 1}

Limits: The amount of Tier 2 capital in excess of Tier 1 capital does not count as allowable

capital.

Total Capital (TC) or Allowable Capital = Tier 1 + Tier 2 (See the limit above)

RWA = Risk Weighted Assets or Risk Adjusted Assets

The recent minimum capital requirements per category are as follows in text Table 13-4:

Risk weighted assets under Basel III

The risk weighting scheme works as follows:

Assets are classified into risk categories and assigned a regulatory determined “weight.”

Low risk items receive a low weight.

The total amount of Risk Weighted Assets (RWA) is then the sum of (Amount Weight) for

each asset category.

Special conversion factors are applied to off-balance-sheet items such as letters of credit and

swaps.

Summary of the Risk Weights for On Balance Sheet Items (See also Text Table 13-17)

On balance sheet items:

Risk Weight Asset

Category 1

0% Cash

Securities backed by U.S. and OECD govt.and some U.S. govt. agencies

Reserves at Fed (central banks)

GNMA mortgage backed securities

Loans to sovereigns with an S&P rating of AA- or better

Category 2

20% CIPC

Mortgage backed non-govt. agency sponsored securities such as FNMA

and FHLMC backed securities

Most securities issued by govt. agencies

GO municipals

U.S. and OECD interbank deposits and guaranteed claims

Repos collateralized by U.S.G.S.

Loans to sovereigns with an S&P rating of A+ to A-

Loans to banks and corporates with an S&P rating of AA- or better

Category 3

35% Single or multi-family mortgages (fully secured, first liens)

Category 4 Revenue bonds, multifamily mortgages

50% Certain loans to sovereigns+

Certain loans to foreign banks+

Certain singly family mortgages*

Category 5

75% Certain single family mortgages

Category 6

100% Commercial and consumer loans

Certain loans to sovereigns, banks and securities firms

All other assets, including intangibles

Category 7

150% Loans and other exposures 90 days or more past due

Volatile commercial real estate loans

Certain single family mortgages

Category 8

200% Certain single family mortgages

Category 9

1250% Securitization exposures

+ The appendix contains the details on the ratings categories for these items.

* The different weights for single family mortgages vary with the loan to value ratio and whether

the mortgage represents a first lien. Details are available in the appendix.

Conversion factors for off-balance-sheet contingent or guaranty contracts (Text Table 13-19)

Sale and repurchase agreements and assets sold with recourse (& not on the balance sheet)

(100%)

Direct credit substitute (financial) standby letters of credit (100%)

Performance related standby letters of credit (50%)

Unused portion of loan commitments with original maturity of ≤ 1 year (20%)

Unused portion of loan commitments with original maturity of > 1 year (50%)

Commercial letters of credit (20%)

Bankers acceptances conveyed (20%)

Other loan commitments (10%)

The risk weights for these categories depend on the riskiness of the creditor under Basel III.

Teaching Tip: Each country can set different risk weights and different account types may be

classified differently within and between countries. For example, although long term Treasury

Bonds carry no default risk and are classified in the 0% risk weight category, regulators may

assign them a 20% risk weight because of their price volatility.

Finding the risk adjusted value of off-balance-sheet contingent guaranty contracts is a two step

process:

1. Multiply the amount outstanding times the appropriate conversion factor listed above. This

gives the credit equivalent amount as if the commitment were on the balance sheet.

2. Multiply the result in step 1 by the appropriate risk weight found in the on balance sheet risk

weight table. For instance, if a bank issues a standby letter of credit guarantee on a commercial

paper issue, the letter of credit commitment is first multiplied by 100% and then multiplied by

100% again. So that the risk weighted asset amount is equal to the original amount of the credit.

If the bank however issued a standby letter of credit to a municipal borrower to back G.O. bonds

the amount would be multiplied by 100% and then by 20% since G.O. bonds appear in the 20%

risk weight (on balance sheet) category.

Finding the risk adjusted asset value of off-balance-sheet OTC derivative instruments or market

contracts is more complex. The risk weighting for these contracts is due to counterparty credit

risk. Therefore exchange traded contracts, which do not bear counterparty risk are not included.

The notional value of all nonexchange traded swaps, forwards, OTC options and other such

exposures are first converted into on balance sheet credit equivalents as before, but this

conversion is a two step process that requires estimating the contract’s current and potential

exposure.

The credit equivalent amount is then separated into two components: current exposure and

potential exposure.

Current exposure is the cost to replace the contract today if the counterparty defaults

immediately.

Current exposure on a forward contract may be calculated by assuming that the

counterparty defaults today and the forward contract has to be replaced using the new

forward rate for the time remaining on the contract. If the bank had bought pounds

forward at $1.50 per pound, but now the forward rate is $1.60 per pound the replacement

cost is the discounted value of $0.10 per pound bought forward. Replacement cost can be

positive or negative, but if it is negative the bank must count it as zero under existing

regulations.

Current exposure on a swap can be calculated as the net present value of the existing

swap less the net present value of a replacement swap.

Potential exposure measures the expected cost to replace the contract in the future if the

counterparty defaults later on. Exchange rate contracts are more volatile than interest rate

contracts so their values can change more, and regulators require higher conversion factors

for them than for interest rate exposures. The value of longer term contracts is also more

volatile than short term contracts, and long term derivatives also carry higher conversion

factors.

Credit conversion factors for interest rate and foreign exchange contracts used in calculating

potential exposure (text Table 13-20)

Remaining Maturity Interest rate contracts Exchange rate contracts

Less than 1 year 0.0% 1.0%

1-5 years 0.5% 5.0%

> 5 years 1.5% 7.5%

The notional value times the appropriate factor from the above table yields the potential

exposure.

The sum of the potential exposure and the current exposure gives the total on balance sheet

equivalent credit amount. This sum is then multiplied by the appropriate risk weight which was

generally 50% under Basel I, but is 100% under Basel II and III. (See the following example,

its really not that difficult if you do not have to calculate the current exposure.)

Example calculation:

XYZ Bank (Millions)

Cash & Reserves $ 5 Deposits $113

Investments in Treasuries $ 10 10 year Sub. Debt $ 16

Commercial loans BB+ $ 12 Perpetual Noncum. PS $ 1

Single family mortgages $ 45 Common stock $ 2

Consumer loans $ 35 Retained Earnings $ 5

Commercial loans CCC+ $ 25 Total $137

Allowance for loan losses ($ 10 )

Physical assets $ 15

Total Assets $137

Note:

Off-Balance-Sheet: Banker’s Acceptances $20 million to entities with an A+ rating.

Three year fixed for floating interest rate swap with notional value of $75 million and a

replacement cost of $3 million.

Three year forward contract to sell euros for $10 million. The contract has a replacement

cost of $1 million.

XYZ Bank (Millions $)

Risk

Weight Capital

Cash & Reserves $ 5 0% Deposits $113 –

Investments in Treasuries $ 10 0% 10 year Sub. Debt $ 16 Tier 2

Commercial Loans $ 12 100% Perpetual Noncum. PS $ 1 Add. Tier 1

Single family mortgages* $ 45 50% Common stock $ 2 Tier 1

Consumer loans $ 35 100% Retained Earnings $ 5 Tier 1

Commercial RE (volatile) $ 25 150% Total $137

Allowance for loan losses ( $ 10) N/A

Physical assets $ 15 100%

Total Assets $137

* assumed 50% weight

The on balance sheet risk weighted asset total is calculated as the sum of the amount of each

asset times the risk weight. Total on balance sheet risk weighted assets are thus $122 million.

The reserve for loan losses is ignored in this calculation.

The risk weighted equivalent asset amounts for the off-balance-sheet items are calculated as

follows:

Off-Balance-Sheet: Banker’s Acceptance $20 million to entities with an A+ rating.

Banker’s acceptances carry a 20% conversion factor so the credit equivalent amount is

$20 million 0.20 = $4 million. The counterparty is rated A+ so the risk weight is 50% and the

risk weighted equivalent asset amount is $2 million.

Three year fixed for floating interest rate swap with notional value of $75 million and a

replacement cost of $3 million.

Potential exposure:

The potential exposure is calculated as $75 million times the conversion factor of 0.5% that

applies to interest rate contracts with a maturity of 1 to 5 years:

$75 million 0.005 = $375,000

Current exposure:

The current exposure is the replacement cost of $3 million.

The total credit equivalent amount = current exposure + potential exposure = $3,375,000

Under Basel III, the risk weight is 100% so the equivalent on balance sheet risk weighted amount

is equal to $3,375,000 1.00 = $3,375,000.

Three year forward contract to sell euros for $10 million. The contract has a replacement

cost of $1 million.

Potential exposure:

The potential exposure is calculated as $10 million times the conversion factor of 5% which

applies to exchange rate contracts with a maturity of 1 to 5 years:

$10 million 0.05 = $500,000

Current exposure:

The current exposure is the replacement cost of $1 million.

The total credit equivalent amount = current exposure + potential exposure = $1,500,000

Under Basel II, the risk weight is 100% so the equivalent on balance sheet risk weighted amount

is equal to $1,500,000 1.00 = $1,500,000.

Total Risk Weighted Assets (RWA)

On Balance Sheet RWA $122,000,000

Banker’s Acceptances $ 2,000,000

Swap $ 3,375,000

Forward $ 1,500,000

Total RWA $128,875,000

CET1 Capital = $7,000,000

Additional Tier I = $1,000,000

Total Tier I = $8,000,000

Tier 2 Capital = $5,610,937 million = $4 million + $1,610,937

Tier 2 Capital is calculated as follows: Only $4 million in 10 year subordinated debt can

be counted as Tier 2 capital because this category is limited to no more than 50% of Tier

1 Capital. Only part of the $10 million loan loss reserve can be counted; recall that a

maximum amount of loan loss reserves that can be counted as capital is 1.25% of risk

weighted assets, or $1,610,937 = $128,875,000 * 0.0125 in this case.

Total Capital or Allowable capital = Tier 1 + Tier 2 = $13,610,937

Common equity Tier I risk-based capital ratio = CET1/RWA = $7,000,000/$128,875,000 =

5.43%

Total Capital/ RWA $13,610,937 / $128,875,000 = 10.56%

Tier 1 Capital / RWA $8,000,000 / $128,875,000 = 6.21%

Leverage ratio = Total Capital / (Total Assets + Off Balance Sheet Exposure) = $13,610,937 /

$137,000,000 +$3,375,000+$1,500,000) = 9.59%

This bank is adequately capitalized rather than well capitalized because the CET1 risk based

ratio is less than 6.5%. See text Table 13-4.

End of Appendix 13E

In 2014 the leverage ratio for all FDIC insured institutions was 9.54% and continued to

trend upward. The Tier I risk based capital ratio was 13.34%, the total risk-based capital ratio

was 15.07%. In the first quarter of 2014 total current exposure to Tier I capital from derivatives

was 23.5%, potential exposure to Tier I capital was 56.7% for a total exposure ratio of 80.3%.

These exposures have been declining over time.

(Source FDIC Quarterly Banking Profile 1st Qtr, 2014)

c. Off-Balance-Sheet Regulations

In the 1980s banks began increasing off-balance-sheet (OBS) activity to offset declining profit

margins on traditional bank operations and to escape scrutiny, capital and other requirements

imposed on balance sheet activities. Since 1983 banks have had to report OBS activity on

Schedule L of their call reports.