1. Regulation of Product and Geographic Expansion

The focus of the banking laws from 1933 to 1980 was to limit the number of failures by limiting

How banks could compete

Where banks could compete

What lines of business banks could engage in.

The laws were also designed to protect small banks from being outcompeted and driven out of

business by large banks. The laws worked; about 43% of the existing number of banks failed in

the 1923 to 1933 time period (almost 14,000 banks). From 1941 to 1977 with the tougher

regulations fewer than 200 banks failed.

Teaching Tip: The environment began to change rapidly in the mid to latter 1970s. The U.S.

experienced inflation and interest rates began rising. In 1979 the Fed stopped targeting interest

rates and allowed rates to rise further. Rates were very high by historical standards and projected

to keep rising due to inflation/energy prices. All DIs faced disintermediation under Regulation

Q (Reg Q limited the ability of banks and thrifts to offer competitive interest rates on deposits) as

money market mutual funds grew rapidly. There were increasing levels of competition within

the banking industry and from non-bank financial institutions brought about by scale and scope

economies generated from rapid improvements in computer technology. Regulations severely

limited growth opportunities for banks and thrifts. Thus, there were profit opportunities that the

banks could not exploit. Since regulations limited banks from expanding into many related

financial services, banks did what they could and other non-banks attempted to enter new lines of

banking related businesses. For instance, Merrill Lynch created cash management accounts,

insurers granted loans against life insurance policies, money market mutual funds offered

checking features, even Sears, a large retailer, began offering credit cards. Banks began offering

discount brokerage services, and offering insurance in conjunction with loans. Slow erosion of

regulatory firewalls continued, but history shows that Congress never acts until there is a crisis.1

The crisis was provided by the drop in profitability and the consequent run down in equity values

at savings and loan institutions. Ronald Reagan, a great believer in deregulation, was also

elected President in 1980, the year the first major piece of legislation deregulating financial

services, the DIDMCA, was passed. At this point the setting was ripe for change and the 1980s

became a decade of deregulation of financial services.

a. Product Segmentation in the U.S. Commercial Banking Industry

Germany, Switzerland and the United Kingdom have universal FIs that provide a broader range

of financial services than U.S. banks. The Japanese system is more closely akin to the U.S.

because it was modeled after ours. Nevertheless, overall most foreign banks have long been able

to engage in a broader range of services such as commercial and investment banking, insurance,

and other financial activities than U.S. banks. For regulatory purposes commercial banking is

defined as making commercial loans and taking deposits. Investment banking is underwriting

1The Civil War brought about the National Banking Acts of 1863 and 1864 in order to provide

desperately needed financing for the Federal Government. The severe financial panic of 1907

led to the creation of the Federal Reserve in 1913. The Crash of 1929 and the ensuing

Depression led to the Glass-Steagall Act and the creation of the FDIC. The failure of the FSLIC

brought about the FIRRE Act and the FDICIA. The merger of Traveler’s and Citicorp forced the

FSMA in 1999. You would think that after 150 years Congress would learn to be a little more

proactive.

and distributing securities and otherwise engaging in market making activities.

Separation of financial services was enshrined by regulation during the Depression. The

Glass-Steagall Act came about as a result of the large number of bank failures after the stock

market crash of 1929. Prior to this time banks had been allowed to engage in investment

banking activities. Allowing joint investment banking and commercial banking can create many

conflicts of interest (see below). Glass-Steagall prohibited banks from underwriting most

securities (except GOs, Treasuries, private placements and real estate loans).

Ethics Teaching Tip: Example of the conflicts of interest include implicit or explicit ‘tie in’

arrangements. For example a lender might pressure a loan customer to purchase a new issue the

bank is underwriting as a condition for a favorable review of a loan application. A lender may

also disclose unfavorable information uncovered in the loan application to the bank’s securities

division so that the firm’s stock can be sold before losses occur.

In 1987 the Fed began allowing certain commercial banks to create Section 20 affiliates which

could underwrite corporate debt and equity securities. Since 1997 banks have been allowed to

acquire existing investment banks. This change set off a spate of mergers such as Deutsche

Bank’s acquisition of Bankers Trust. Finally in 1999 the FSMA allowed the creation of full

service FIs. In 2005 there were 640 financial service firms in the U.S. with over $7 trillion in

assets.

The FSMA also allows bank holding companies to establish insurance underwriting affiliates and

allows insurance companies to operate banks and securities firms. The FSMA is indeed the

biggest law change since the Glass-Steagall Act it repeals.

Prior to the FSMA, banks and bank holding companies (and insurers) were prohibited from

owning nonfinancial entities. The 1956 Bank Holding Company Act required bank holding

companies to divest any amount beyond a 4.9% stake in nonfinancial entities. Until recently, the

only way a commercial firm could enter banking had been to operate a nonbank bank. Nonbank

banks either make commercial loans or take (uninsured) demand deposits but not both.

The FSMA defines a financial services holding company as one which holds at least 85% of its

assets in financial assets. The intent of the law was to ensure that financial services holding

companies hold financial assets, and divestment of commercial enterprises may be required.

Commercial banks belonging to a financial services holding company could also have a

controlling interest in a nonfinancial enterprise as long as the investment is for a limited time

period (the time period is unspecified in the Act) and as long as the bank does not actively

manage the nonfinancial enterprise.

Although the FSMA allowed the creation of financial conglomerates that operate in many

diverse financial lines, the act continued functional regulations. For instance, a financial

service holding company with a bank, an insurer and a securities firm continues to have each

activity regulated by the appropriate agency.

After the FSMA some commercial banks had only limited success in entering investment

banking underwriting. Wachovia and Bank of America for example had only limited success

before the crisis, but J.P. Morgan did make inroads. The financial crisis ended the separation of

the two. In March 2008 the Fed helped J.P. Morgan acquire Bear Stearns and in September

Lehman Brothers was allowed to fail and Bank of America acquired Merrill Lynch to prevent its

failure. Goldman Sachs and Morgan Stanley were allowed to change their charters to

commercial banks to acquire deposit funding and to make it easier to borrow from the Federal

Reserve.

b. Geographic Expansion in the U.S. Commercial Banking Industry

Throughout the early and mid 1900s many states required banks to be unit banks (banks with no

branches) and the ability to branch has predominantly been regulated at the state level. Most

states prohibited or limited branching because they feared that allowing branch banking would

eliminate the small local independent banks. The McFadden Act of 1927 required nationally

chartered banks to adhere to state branching restrictions. It was actually intended to allow

national banks greater freedom to branch, but the Act contained a provision that left branching

restrictions up to the state, and most states quickly prohibited branch banking and interstate

banking. As of 1997 only six states still limited intrastate branch banking.

Banks always sought ways around the geographic restrictions imposed upon them by regulations.

When they could not acquire or create de novo (build new ones) branches, they created

multibank holding companies that led to defacto intrastate and interstate banking. This led to

the 1956 Bank Holding Company Act which limited the ability of multibank holding

companies to operate out of state subsidiaries. Existing multi-state structures were

grandfathered and allowed to continue. After this, one bank holding companies were formed

that had nonbank subsidiaries operating across state lines. Congress closed this loophole in the

1970 Amendments to the Bank Holding Company Act.

Teaching Tip: Several events led to the eventual demise of many of the restrictions on branching

and interstate banking. First, the regulators allowed DIs from other states to acquire failing

institutions during the 1980s, so defacto interstate banking was occurring. Second, more states

began allowing intrastate branching and interstate banking via reciprocal agreements with

neighboring states. Maine even allowed non-reciprocal interstate banking to encourage

competition.

In 1994 Congress passed the Riegle-Neal Act that allowed interstate banking by allowing banks

to consolidate out of state bank subsidiaries into a branch network or by acquiring existing banks

across state lines. The ability to establish de novo branches across state lines is up to the

individual states. Some states prohibit de novo branching to protect the value of small local

institutions because in these cases the only way to gain market access is to buy a local institution.

The Riegle-Neal Act has also been a major impetus for many mergers.

Teaching Tip: What does this indicate about the lobbying power of smaller banks?

Savings institutions have been allowed to operate across state lines since the 1980s.

2. Bank and Savings Institution Guarantee Funds

a. FDIC

The FDIC was created during the Depression to restore public confidence in the banking system.

The initial insurance limit was $2,500; this amount was periodically increased to $100,000 where

it remained until the financial crisis when it was increased to $250,000.23 The FDIC had little

trouble until the 1980s because there were very few failures from the 1930s to the 1980s. There

were more bank failures in the 1980s than during the entire previous existence of the FDIC. Past

failures and new potential failures of large banks revealed that the FDIC was undercapitalized

and that additional regulations were needed to improve the safety and stability of the banking

industry. The result was the FDIC Improvement Act (FDICIA) of 1991. The major provisions

of FDICIA included

Regulators must take prompt corrective action (PCA) and intervene in cases where bank

capital falls below prescribed minimums. See Text Table 13-5 for details.

The pricing of deposit insurance premiums would be risk based.

Regulators were very limited in their ability to use government funds to bailout institutions

deemed ‘too big to fail.’

Federal regulations were extended to foreign bank branches and agencies (Foreign Bank

Supervision and Enhancement Act)

The decade of the 1990s saw strong profit growth at banks and very few failures (only three in

2004 with assets of $151 million total). As of the third quarter of 2004 the FDIC had reserves of

$34.5 billion. The bank fund (or BAIF, see below) reserve ratio was 1.32%, the saving fund (or

SAIF) reserve ratio was essentially the same at 1.33%. The BAIF reserve ratio was higher in

2004 than in 2001-2003. In 2007 the merged DIF fund equaled $52 billion and represented

1.22% of insured deposits. As of the end of 2007 there were 76 problem institutions with $22

billion in assets. Three institutions failed in 2007 with total assets of $2.3 billion. These were

the first bank failures since 2004 when four banks failed. Of course the crisis made the fund’s

position far worse. The FDIC’s DIF reserves were -$7.2 in December 2010 with a reserve ratio

of -0.12%.4 The banks have been required to pay higher insurance fees and even to prepay fees.

The FDIC has also been approved to borrow up to $500 billion from the Treasury, so no talk of

failure emerged. From 2007 through 2010, 325 institutions failed (with assets of $636.3 billion).

In December 2010 there were 884 institutions on the Problem Bank List with assets of $390

billion so the fund was still stressed at that time. Losses to the fund from 2008 through 2011were

$81.7 billion as 414 total institutions failed over the period.

(Source: FDIC Quarterly Banking Profile and FDIC Historical Statistics and the text).

2Unlimited insurance of accounts was temporarily provided during the financial crisis to prevent

any runs.

3 There are various ways individuals can increase their insurance coverage beyond $250,000.

You may have an account, your spouse may have a separate account and then you may have a

joint account to get your insurance coverage up to $750,000; however, most of us don’t have this

problem anyway.

4 This is an improvement from over -$17 billion in 2009.

b. The Demise of the Federal Savings and Loan Insurance Corporation (FSLIC)

The FSLIC was the FDIC counterpart to the savings and loan industry. The FSLIC was overseen

by the Federal Home Loan Bank Board (FHLBB). The FHLBB acted as both a regulator and

promoter of the industry. The FSLIC had few problems during the regulated years. The S&L

industry was allowed to pay higher rates on deposits than banks under Regulation Q, creating an

advantage for S&Ls. As interest rates rose in the 1970s and Regulation Q ceilings prevented

thrifts from raising rates, disintermediation occurred and S&L profits plummeted due to their

large negative rate sensitivity gap. The Depository Institutions Deregulation and Monetary

Control Act (DIDMCA) of 1980 gave S&Ls greater abilities to diversify their investment and

loan portfolios and offer NOW accounts so that they could be more like banks and began to

phase out Regulation Q. Unfortunately, many S&Ls did not have the expertise to compete in

established banking markets. Moreover regulations did not provide incentives for S&L

managers to limit risk on their own and many, fearing that insolvency was inevitable anyway,

undertook greater risks in unfamiliar areas such as junk bonds and commercial real estate.5 The

DIDMCA (and later the followup Garn-St. Germain Act of 1982 which further broadened S&L

powers) did little to stop the profit problems at S&Ls as short term interest rates soared and the

yield curve turned downward sloping. The inverted yield curve hurt S&Ls because they made

long term fixed rate mortgages funded by short term deposits. Many S&Ls already low capital

levels were quickly eroded and record numbers of institutions became insolvent. At one point

the market value of equity for the industry as a whole was negative.

Teaching Tip: The S&L debacle

During this period regulators followed a policy of regulatory forbearance, meaning they did

not close insolvent S&Ls, or in many cases even replace management at technically insolvent

institutions. Regulators allowed and even encouraged ‘creative accounting methods’ to hide

problems in the thrift industry. There existed a revolving door in upper levels of the FHLBB and

the industry, and there was a critical lack of funding for the FSLIC. The typical S&L examiner

made little money (about $14,000 a year) and had very little business experience. Indeed, staff

cuts were common throughout the early 1980s. Congressional/Presidential indifference and even

Congressional interference (cf, the Keating Five) also exacerbated the problem. Some of the

nonstandard accounting procedures used included:

Book value accounting for loans: e.g. a 6% mortgage could be carried at book when interest

rates were 12%. This hid the inadequacy of that loan’s income. At the same time market

value accounting was allowed for physical assets (one time revaluations).

Net Worth Certificates were given to institutions issued by the regulators which contained

promises to pay, but involved no cash. Thrifts were allowed to count the certificates as capital

in order to continue operating.

Loan losses were allowed to be deferred over the original life of the loan, but origination fees

could be immediately and fully recognized as income.

(Material for this section is drawn from White, L., The S&L Debacle, Oxford University Press,

5This was a rational response from S&L managers who feared failure would occur anyway.

Recall from Chapter 10 that equity can be viewed as a call option on firm value. The value of

this call option increases with increased firm risk. Without incentives to limit risk, the results of

deregulating a troubled industry should have been predictable.

1991.)

When the FSLIC was declared insolvent in 1987 Congress was finally forced to act. The result

was the Financial Institutions Reform, Recovery and Enforcement Act (FIRREA). Major

provisions of the FIRE Act as it is sometimes called include: (more detail is provided here than

in the text)

The chartering and supervision of thrifts was taken away from the FHLBB and given to the

new Office of Thrift Supervision (OTS) under the Treasury. The FHLBB was stripped of

its powers and disbanded. The Federal Home Financing Board (FHFB) was created to

oversee the 12 Federal Home Loan Banks. They still exist.

The Savings Association Insurance Fund (SAIF) was created to replace the bankrupt

FSLIC. The SAIF was administered by the FDIC, although at first the Banking Insurance

Fund (BIF), which is also administered by the FDIC, was kept separate. The two funds have

now been merged into the Deposit Insurance Fund (DIF).

The Resolution Trust Corporation (RTC) was created to resolve failed thrifts and dispose of

their assets. The RTC has now fulfilled its commission and been dissolved.

Limits on savings bank’s investments in nonresidential real estate, required divestiture of

junk bond holdings by 1994 and strengthened the QTL Test which required a minimum

percentage of a thrift’s assets be in mortgage related assets in order to receive certain tax and

funding benefits.

Equalized the capital requirements of thrifts and banks.

Required that accounting procedures could be no less conservative than generally accepted

accounting procedures.

Teaching Tip: Ask your students why the SAIF was not placed under the OTS.

c. Reform of Deposit Insurance

Also see the above discussion. It is likely that a combination of poor (unlucky?) environmental

factors combined with management that was inexperienced at competing and inexperienced at

interest rate and credit risk management resulted in the large number of S&L and bank failures in

the 1980s. There were unprecedented swings in interest rates and severe regional recessions,

particularly in Texas and the Southwest in the early to mid 1980s, and later on in the Northeast.

As for commercial banks, in 1987 many large banks had to write off huge amounts of loans to

LDCs.6 Throughout much of the 1980s regulators granted increasing powers to institutions

without providing incentives to limit risk. The ensuing moral hazard problems should have

been predictable. Regulators should have either explicitly or implicitly penalized risk taking.

Thrift regulators failed in their duty to preserve the safety and soundness of the industry, but

bank regulators had more success. Congress and the presidential administrations did not

adequately fund the regulatory agencies so that the problem could have been dealt with

decisively before the losses became so large. Outright fraud, some of it outrageous, did occur

(for instance, see the student exercises at the end). Members of Congress did intervene in

regulatory matters inappropriately. Still, hindsight is always a harsh critic. At the time, most

people did the best they could with the resources they had.

6Citicorp wrote down over $3 billion in LDC loans in one quarter. Many other large banks also

had large write downs of bad loans.

Teaching Tip: An illuminating conversation: At one point in the 1980s I had the privilege of

talking to a CEO of a western thrift. I asked him what they were going to do differently in view

of the recent profit problems at his and many other institutions. This very bright, very well

informed individual replied that they were not going to change anything; they were going to

continue to do things the way they always had. Such was the mindset of the times for too many.

The institution did not long survive after our conversation.

In April 2001 the FDIC proposed four major changes to the deposit insurance system resulting in

the following changes:

1. The BIF and SAIF funds were merged in order to achieve cost economies for both DIs and the

FDIC. Both funds offer identical coverage and due to mergers many institutions already have

different deposits insured by both funds. For example, 40% of SAIF insured deposits were at

the time held by commercial banks. As of March 2005 the two funds were merged.

2. Until 2007 the FDIC did not charge deposit insurance premiums to well-capitalized highly

rated DIs as long as fund reserves were at least 1.15% of insured deposits. As a result,

because over 90% of all insured DIs were typically in this top category, the vast majority of

depository institutions avoided paying deposit insurance premiums. As of January 2007 (after

the passage of the FDIC Reform Act of 2005) the FDIC began more aggressive pricing for

risk regardless of the reserve level of the fund, and planned to disaggregate banks in the top

rated category and charge appropriate risk premiums. The scoring model is presented in

Appendix A. The fund also must now implement a recapitalization plan if the reserve ratio

falls below 1.15% (or they believe it will in the subsequent quarter) as happened in 2008.

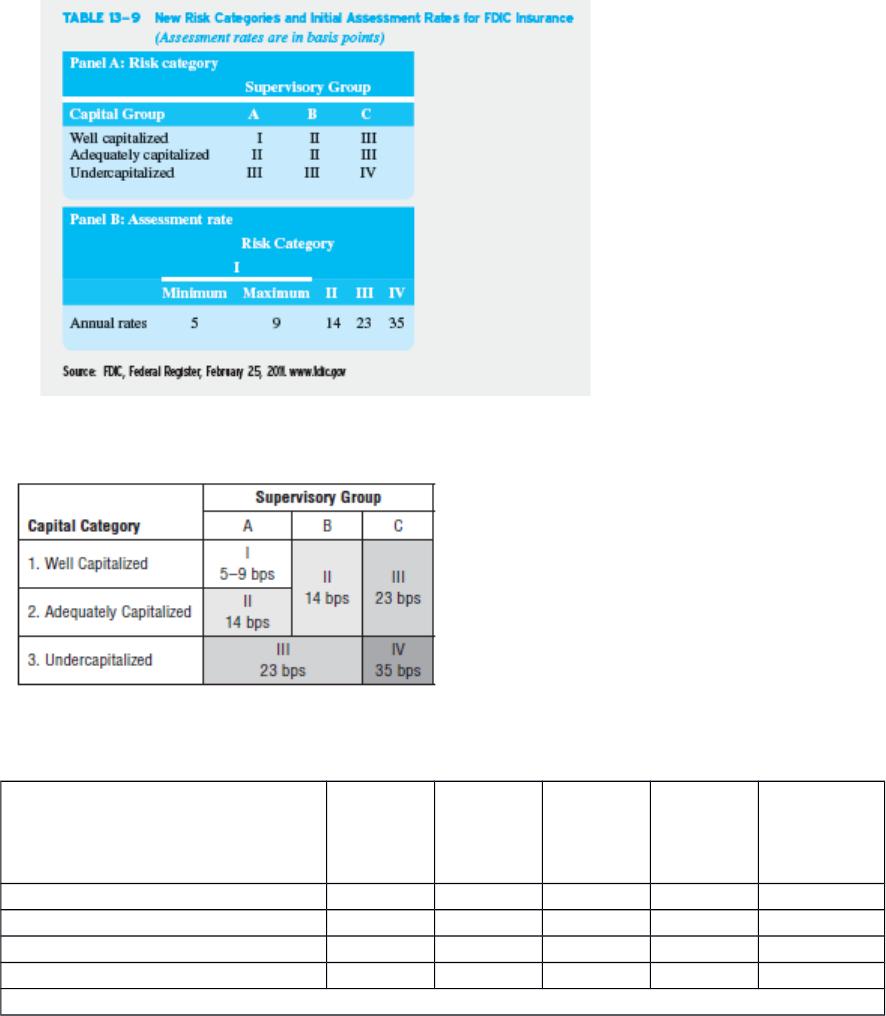

Appendix 13A: Calculation of Deposit Insurance Premium Assessments

Appendix 13A contains a summary of the risk adjusted credit score model proposed by the FDIC

to price deposit insurance. Among other things, the model utilizes CAMELS ratings and various

ratios such as the percentage o loans past due at least 30 days, investment ratings and percentage

of nonperforming assets. The model now also includes a factor for the amount of brokered

deposits as a percent of total deposits. Greater usage of brokered deposits increases a bank’s

insurance assessment. Text Table 13-19 has the assessment rates for different risk categories. The

assessment base and assessment rates were changed effective April 1, 2011. New rules apply for

large and complex institutions. Large institutions are those with at least $10 billion in assets are

treated differently in a separate category. Complex institutions are those with more than $500

billion in assets and controlled by an entity with more than $500 billion in assets. Risk

categories are eliminated for large and complex institutions and a separate assessment category

was created as per the Dodd-Frank bill requirements. Rates for large and complex institutions

are set based on CAMELS ratings and other financial ratios that estimate likely future losses.

The categories in Text Table 13-9 below establish the Supervisory group and present the base

assessment rates:

For smaller institutions the assessment rate is based on capital ratios and supervisory group as

delineated below (with lots of exceptions):

Source: FDIC Quarterly Banking Profile September, 2013.

Adjustments to the base assessment rate are made as follows::

Initial and Total Base Assessment

Rates( basis points)

Risk

Category

I

Risk

Category

II

Risk

Category

III

Risk

Category

IV

Large and

Highly

Complex

Institutions

Initial base assessment rate 5-9 14 23 35 5-35

Unsecured debt adjustment -4.5-0 -5-0 -5-0 -5-0 -5-0

Brokered deposit adjustment … 0-10 0-10 0-10 0-10

Total Base Assessment Rate 2.5-9 9-24 18-33 30-45 2.5-45

Source: Quarterly Banking Profile September 2013

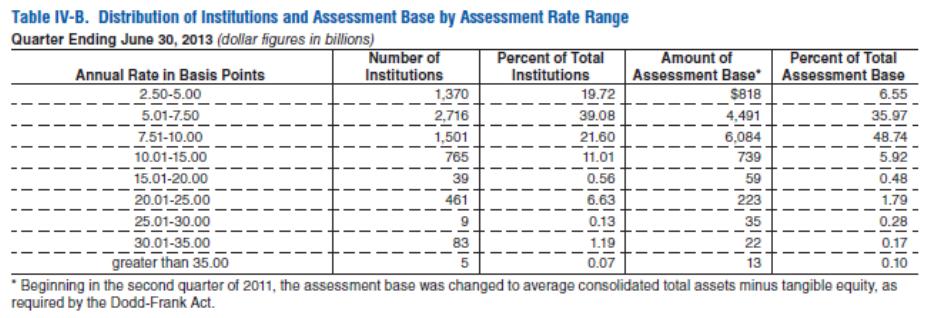

The FDIC Assessment Rate Distribution for the quarter ending June 30, 2013 was as follows:

Source FDIC Quarterly Banking Profile, 4th Qtr, 2010 Institutions are categorized by supervisory

ratings, debt ratings and financial data as of the report date.

Notice that now even low risk, well capitalized banks (the majority) must pay for deposit

insurance, this is a change from prior years.

Source: Table IV-B, FDIC Quarterly Banking Profile, September 2013

d. Non-U.S. Deposit Insurance Systems

European banking systems are largely composed of fewer, larger banks. Traditionally they have

not had explicit deposit insurance, and they have not had bank runs akin to the U.S. experience.

This is probably because depositors believed that their respective governments would either not

allow the banks to fail, or they believed that the government would repay the depositors. Deposit

insurance was implicitly provided and the government probably extracted implicit insurance

premiums. In any case, as global competition provides impetus to standardize regulations we

can expect more governments to explicitly offer deposit insurance and charge fees for the

service. The financial crisis also led to increases in explicit deposit insurance in a number of

countries. Appendix D lists deposit insurance schemes before and after the financial crisis.

Teaching Tip: Deposit insurance isn’t really necessary to prevent bank runs if the lender of last

resort (central bank nationally or perhaps someday the IMF internationally) can be counted upon

to fund failing banks. Also why is deposit insurance granted to corporate accounts? Wouldn’t it

be better to force corporations to evaluate the riskiness of their banks and price their required

returns on deposits accordingly? Their account sizes are typically well over the insurance limit

in any case and this would seem to help limit the moral hazard problem induced by deposit

insurance. A similar system is used in European banks.