Chapter 12 – Commercial Banks’ Financial Statements and Analysis 6th Edition

1. Financial Statement Analysis Using A Return on Equity Framework

Time series and cross sectional ratio analysis can be useful to identify strengths and

weaknesses of banks. The FFIEC or the FDIC websites can be used to generate average

data for comparison.

Ratio analysis is very useful for identifying trends over time and for highlighting

differences from peer group competitors. Identifying the proper peer group may be

challenging.

a. Return on Equity and Its Components

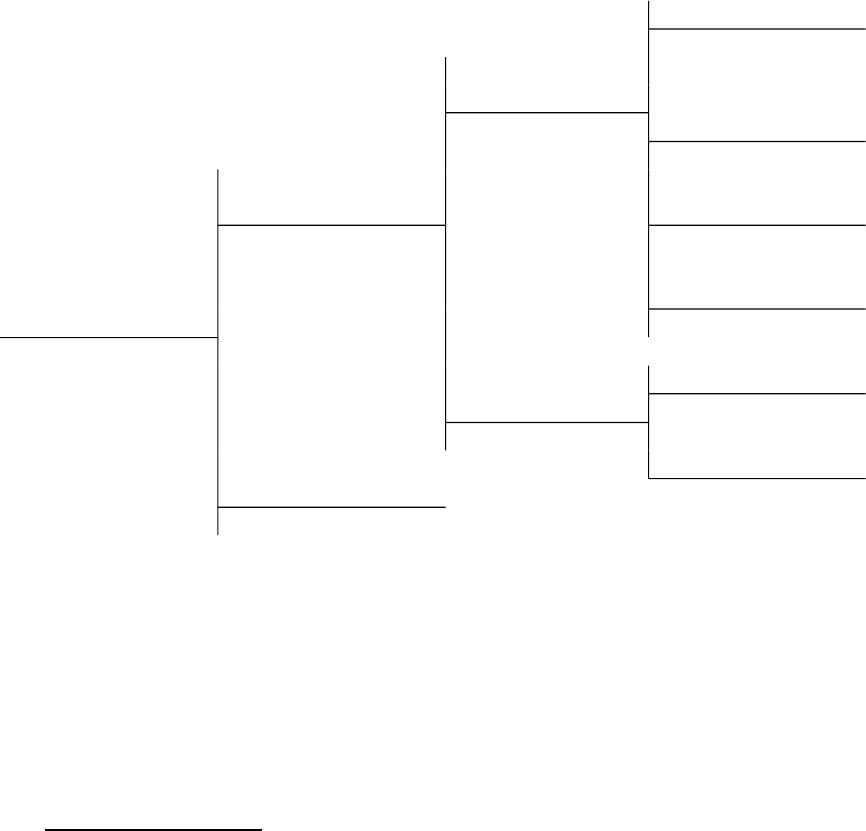

Chart of ratios illustrating the sources of a bank’s ROE, all insured banks, FDIC Banking

Statistics

2013 Full Year Interest Expense 7.04%

Data Operating Income

Profit Margin

Net Income

Operating Income PLL 4.28%

21.60% Operating Income

ROA

Net Income Noninterest expense 57.89%

Total Assets Operating Income

1.06%

ROE Income Taxes 9.72%

Net Income Operating Income

Total Equity Capital

9.57% Asset Utilization Interest Income 3.21%

Operating Income Total Assets

Total Assets

Equity Multiplier 4.93% Noninterest income 1.72%

Total Assets Total Assets

Total Equity Capital

8.99x

Numbers are calculated from the FDIC webpage using yearend 2013 data for all federally

insured commercial banks. Operating income is interest income plus noninterest income,

i.e. this is gross, not net operating income.1 All profit measures have been dramatically

reduced due to the crisis and higher loan losses.

ROE measures the profits per dollar of investor’s equity. Generally, higher numbers

are better.

ROA measures the profits per dollar invested in assets. Note the low ROA of banks.

Higher numbers typically indicate better performance.

The equity multiplier is equal to 1 + Debt/Equity ratio. This implies that the average

1 This is potentially confusing as most bank income statements have a line titled

operating income or net operating income, but the text definition is not the same as in that

line.

12–1

Chapter 12 – Commercial Banks’ Financial Statements and Analysis 6th Edition

debt to asset ratio of banks is 89%. The high percentage of debt is required to offset

the low ROA in order to offer a respectable ROE. Debt magnifies changes in ROE as

conditions change and increases insolvency risk.

b. Return on Assets and Its Components

ROA is the product of the profit margin and asset utilization ratios.

The profit margin measures how effectively the bank turns a dollar of revenue into a

dollar of bottom line profits. Generally, the higher this ratio the better. If this ratio

appears to be too low look for problems in the following ratios in the chart. The

analyst should ascertain whether the PLL is too high. The PLL to Operating Income

ratio fell for banks in 2003 and 2004, improving profitability, but the ratio increased

in 2006 and 2007 due to the mortgage market problems and remained high in 2008

and 2009 before beginning to fall in 2010 and continuing to improve since. Salaries

are a major component of noninterest expense and may be the problem if noninterest

expense to operating income is too high. Additional breakdowns for each component

of these categories may be desirable.

The asset utilization ratio measures how effectively the bank converts its assets into

gross operating revenues. Generally, the higher the better. Excessively high ratios

may indicate that the bank is investing in highly risky loans and/or investments. If

this ratio appears to be too low look for problems in the following two ratios in the

chart. The bank may also have too many nonearning assets.

Problems here may be

indicative of too few loans/excess liquidity, low interest income or a lower amount of

fee based services than peer groups.

c. Other Ratios

Net interest margin (NIM)

LeasesandLoansNetSecuritiesInvestment

ExpenseInterestIncomeInterest

AssetsEarning

IncomeInterestNet

NIM

For 2013 the average NIM = 3.25%. Higher NIM ratios generate a higher bank rate

of return on investments, ceteris paribus. As always, higher returns may come at the

expense of higher risk.

The Spread

The estimated spread was 3.14% for 2013. The spread measures the average yield on

earning assets less the average interest cost of interest bearing liabilities.

Overhead Efficiency

This ratio is seldom greater than 1; the average for 2013 was 60.51%.

12–2

sLiabilitieBearingInterest

ExpenseInterest

AssetsEarning

IncomeInterest

Spread

ExpenseerestintNon

IncomeerestintNon

EfficiencyOverhead

Chapter 12 – Commercial Banks’ Financial Statements and Analysis 6th Edition

Teaching Tip: You may be more familiar with a similar measure, the net noninterest

margin (Noninterest income – noninterest expense) / earning assets. The net

noninterest margin is sometimes called the noninterest burden because it is usually

negative. This ratio was -1.29% in 2013 for the industry.

1.1.1.1

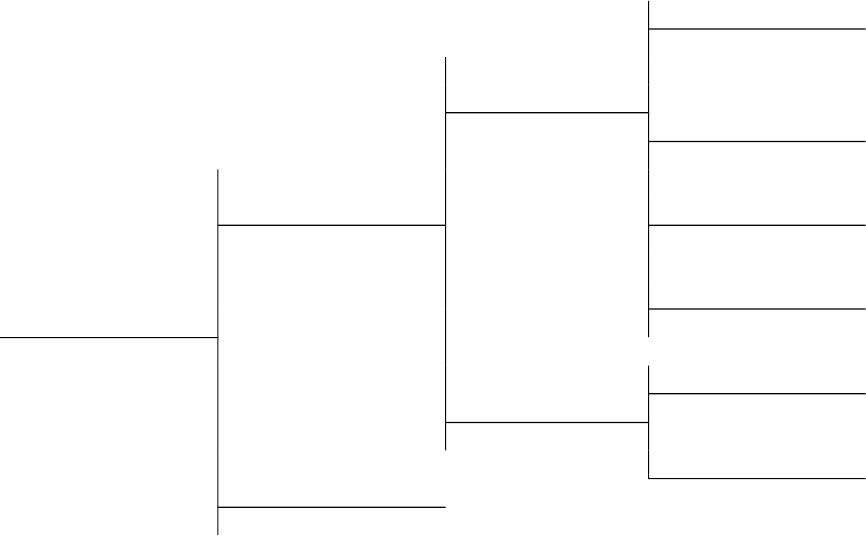

1.1.1.2 Comparison of HBT and BOA

HBT = Heartland Bank and Trust

BOA = Bank of America

Interest Expense HBT = 4.62%

BOA = 3.74%

Operating Income

Profit Margin

Net Income

Operating Income PLL HBT = -1.82%

HBT = 44.51% Operating Income BOA = 7.22%

ROA BOA = 26.41%

Net Income Noninterest expense HBT = 52.01%

Total Assets Operating Income BOA = 49.24%

HBT = 2.31%

ROE BOA = 1.51% Income Taxes HBT = 0.68%

Net Income Operating Income BOA = 13.39%

Total Equity Capital

HBT = 22.86% Asset Utilization Interest Income HBT = 3.99%

BOA = 12.21% Operating Income Total Assets BOA = 3.01%

Total Assets

Equity Multiplier HBT = 5.18% Noninterest income HBT = 1.19%

Total Assets BOA = 5.71% Total Assets BOA = 2.69%

Total Equity Capital

HBT = 9.92

BOA = 8.10

More detailed comparisons are available in the text.

Analysis:

HBT has a substantially higher ROE.

HBT has a higher ROA and is more highly leveraged (larger equity multiplier)

HBT has a higher ROA.

oHBT’s higher ROA is driven by its substantially higher profit margin (PM)

ratios.

oEven though the interest income to assets ratio is higher at HBT, the AU

ratio is lower at HBT because of the substantially lower level of

noninterest income to total assets ratio as compared to BOA.

Operating Income – (Interest expense + PLL + Noninterest expense + Income Taxes) =

Net Income. Hence, the top four ratios in the fourth column comprise the cost

components of the profit margin. The substantially lower values for tax and loan loss

ratios indicate that on net HBT translated more dollars of operating income into net

12–3

Chapter 12 – Commercial Banks’ Financial Statements and Analysis 6th Edition

income.

As a percent of income, BOA incurs far less interest expense than HBT. A further

breakdown of this component reveals that HBT pays a substantially higher percent of

operating income than BOA on MMDAs and wholesale CDs and has higher salary

expenditures as a percent. HBT also uses more wholesale and retail CD funding at higher

rates than BOA.

HBT’s higher profit margin is driven by a very low (even negative) PLL to OI ratio and

much lower tax to OI ratio. A low PLL indicates high loan quality (or unrealistic

management) and fits with the concentration in real estate loans.

Salaries and spending on fixed assets are much lower percentages of operating income at

BOA.

Asset Utilization

BOA generates more operating income per dollar invested in assets. This is in spite of

HBT’s greater percentage investment in loans than BOA.2 BOA has 53.4% of assets in

net loans and leases and HBT has 56.6%. HBT also has a lower percent of nonearning

assets than BOA which should lead to an improved AU.

BOA generates lower interest income per dollar of assets; HBT has substantially higher

asset yields on C&I and real estate loans and on municipals. BOA has higher yields on

the other loans category on leases and on some of their investments.

BOA’s advantage in asset utilization stems in part from the much higher amount of

noninterest income generated per dollar invested in assets. This is because BOA offers

many more off-balance-sheet and fee related services than HBT.

Other ratios:

The NIM for BOA is 4.46%, substantially higher than HBT’s 3.49%. BOA’s advantage

occurs because they have higher earning consumer loans, lower interest costs on deposits

and other funds sources.

HBT has a spread of 4.44%, compared to BOA’s spread of 3.48% indicating that HBT

has a substantial advantage in net interest yields.

The overhead efficiency ratio is substantially higher for BOA. BOA has an overhead

efficiency ratio of 95.88% while HBT’s ratio is only 44.19%. BOA has lower noninterest

expense ratios for salaries and premises, and BOA generates much more noninterest

income than HBT’s, making the efficiency ratio significantly higher for BOA.

Teaching Tip:

Using the average data from the FDIC, HBT is above the norm in leverage (EM) and

2 Loans are typically the highest earning asset category.

12–4

Chapter 12 – Commercial Banks’ Financial Statements and Analysis 6th Edition

beneath the norm in AU measures.3 HBT’s PM is well above the norm. Their PLL / OI

measure is very low, reflecting the low risk nature of their lending. Noininterest expense

to OI is about the same as the industry norm but their average tax rate is lower. HBT

earns lower amounts of noninterest income in relation to total assets than the typical

bank. BOA is well above the average for ROE, ROA and PM. BOA is under the norm in

terms of use of leverage (EM) and is slightly beneath the norm for AU. BOA’s PLL/OI

ratio is much lower than the norm, indicating better credit quality, and their tax rate is

above average. Their interest income to total asset ratio is below the norm.

2. Impact of Market Niche and Bank Size on Financial Statement Analysis

a. Impact of a Bank’s Market Niche

If a bank can find a profitable niche in which to specialize, they can potentially generate

higher rates of return than more diversified institutions at times. Specialization in credit

analysis for one loan type for example builds expertise in credit evaluation and generates

time and cost economies. If the specialty chosen falls on hard times however, a

diversified institution may fare better. Heartland generated higher profit rates than BOA

by specializing in real estate lending funded with core deposits. BOA had a more

diversified portfolio and used more purchased funds and fewer core deposits. This may

make them more sensitive to interest rate changes unless they are well hedged.

b. Impact of Size on Financial Statement Analysis

Some major comparisons

Large banks have greater access to purchased funds and usually maintain more liquid

assets.

Large banks also typically carry lower amounts of equity. At times the ROA of large

banks has been less than for small banks because the large banks operate in more

competitive markets.

Large banks have higher salary expense (%) and typically have higher % costs for

premises.

Large banks certainly have more noninterest income than smaller banks, but they may

also have higher noninterest expense as indicated above. BOA had much more

noninterest income per dollar of assets than HBT due to BOA’s much higher

involvement in off-balance-sheet activities.

1.1.1.3

1.1.1.4 VI. Web Links

http://www.federalreserve.gov/ Website of the Board of Governors of the Federal

Reserve

www.chicagofed.org Website of the Chicago Federal Reserve Bank, call

reports for banks are available from this site.

3 Some of these differences are due to using numbers from different time periods so be

careful using these comparisons.

12–5

Chapter 12 – Commercial Banks’ Financial Statements and Analysis 6th Edition

http://www.americanbanker.com The publication of the banker’s trade association.

http://www.wsj.com/ Website of the Wall Street Journal Interactive edition. The

web version of the well known financial newspaper can be

personalized to meet your own needs. Instructors can also

receive via e-mail current events cases keyed to financial

market news complete with discussion questions.

http://www.fdic.gov/ The Federal Deposit Insurance Corporation’s website. New

regulations and current and historical banking statistics are

available on this site.

http://www.ffiec.gov/ Federal Financial Institutions Examination Council will

shortly provide peer group average data for banks. The

website also includes forms needed to fill out call reports

and contains the Uniform Bank Performance Report.

http://www.bankofamerica.com/ Bank of America Corp.’s website

http://www.hbtbank.com/ Heartland Bank and Trust Company website

http://www.ginniemae.gov/ The Government National Mortgage Association

http://www.fanniemae.com/ The Federal National Mortgage Association

http://www.freddiemac.com/ The Federal Home Loan Mortgage Corporation

1.1.1.4.1.1

1.1.1.4.1.2

1.1.1.4.1.3 VII. Student Learning Activities

1. Go to http://www.bankofamerica.com/ and learn about current career opportunities

with the corporation. Make an oral report to the class about different job openings

and requirements.

2. Go to http://www.ffiec.gov/ and obtain summary ratios for Bank of America. Using

the most recent quarterly data available compare Bank of America with its peer group

averages for the following ratios:

ROE

ROA

PLL/Average Assets

Explain why these ratios vary from the peer average.

12–6