Chapter 11 – Commercial Banks: Industry Overview 6th Edition

1. Size, Structure, and Composition of the Industry

As of March 2014 there were 5,809 insured commercial banks. This number continues to

decline.

Teaching Tip: The decline is somewhat misleading because the number of bank offices

including branches grew from 60,000 in 1984 to 83,593 in 2012. Industry consolidation

has been occurring rapidly, largely via unassisted mergers, but total bank assets and the

total number of banking facilities have grown at significant rates. Banking remains a

growth industry but it is likely that technology will reduce the need for a physical bank

presence over time and we may have seen a peak in the number of offices and branches.

The number of both declined slightly in 2013 (Source, FDIC).

In 2006 Wal-Mart and Target applied for Industrial Loan Corporation (ILC) charters to

provide certain banking services. ILCs are chartered in Utah and are not directly

regulated by any banking regulator. ILCs may make commercial loans, and typically

lend to higher risk corporate borrowers. Wal-Mart’s stated rationale was to lower the cost

of processing electronic payments and Target hoped to issue business credit cards. There

were many vocal opponents of these applications and the FDIC established a moratorium

on all ILC applications while Congress considers banning them. Allowing ILCs of this

type further blurs the separation between commercial enterprises and banking and could

potentially increase the risk of the banking system significantly. Wal-Mart withdrew its

application in 2007.

a. Bank Size and Concentration

The largest banks increasingly dominate the industry (see text or below) and the largest

banks control the vast majority of industry assets. This is now true in all aspects of the

financial services industries. Banks are often classified as:

Money center banks which include the largest banks, typically located in New York

city. Size alone however does not make a money center bank. These banks generally

rely on nondeposit sources of funds and are heavily engaged in wholesale banking

(with or without a retail banking presence) and involved in international markets.

Wholesale banking refers to providing loans services to corporations and other

institutions as well as acquiring nondeposit sources of funds. Retail banking is

providing consumer oriented banking services such as loans and deposits. U.S. based

money center banks include Bank of New York Mellon, Citigroup, J.P. Morgan

Chase, HSBC Bank North America and Deutsche Bank (via acquisition of Banker’s

Trust).

Superregional or regional banks that operate primarily in one or more regions of

the country

Vommunity banks that operate in local markets

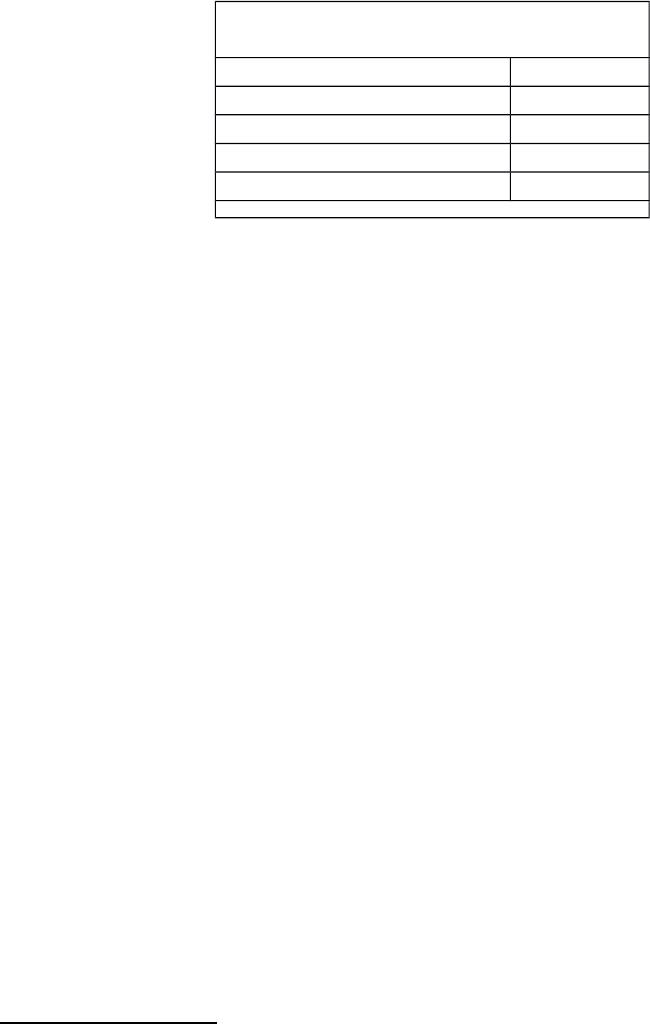

Summary of Text Figure 11-6

Size & Type

2013

% of total #

banks

% of total

banks assets

Community banks 91.1% 8.8%

$1-10 billion 7.4% 8.6%

≥ $10 billion 1.5% 82.6%

11-1

Chapter 11 – Commercial Banks: Industry Overview 6th Edition

100.0% 100.0%

Notice the heavy concentration of assets among the largest banks. Nevertheless,

thousands of small banks remain throughout the country, although more and more of

these small institutions are being absorbed by mergers. Absorptions are running higher

than new charters so the trend toward increasing concentration will continue.

b. Bank Size and Activities

Large banks generally are less liquid, are more heavily concentrated in loans and use

more purchased sources of funds. They have greater access to brokered deposits and

non-deposit liabilities and they tend to hold less equity.

Large banks lend to more sophisticated corporate customers which means that their profit

margins are often lower than for smaller banks that operate in more isolated, less

competitive circumstances. A key ratio for bank management includes the net interest

margin which is equal to the interest rate spread divided by earning assets. The interest

rate spread is the interest earned on assets minus the interest paid on liabilities.

Large banks typically pay higher salaries than smaller banks and have greater

investments in facilities and in the provision of services. On the other hand large banks

generate substantially more fee income than small banks.

Teaching Tip: At times small banks have been more profitable than large banks, but this

has not always been the case. The higher profitability at smaller banks is often due to a

lack of local competition. As large banks gain the ability to enter local markets it is

questionable whether the smaller banks’ profitability can be maintained.

2. Industry Performance

Banks enjoyed excellent profitability during most of the 1990s, weaker performance in

the early 2000s, but record high performance in 2003 and on into 2004.1 In 2004 banks

had an average ROA of 1.31% and a ROE of 14.01%, both figures were good. Bank

ROA’s vary from 0.5% to 2% typically. Bank profitability had been high because of

higher noninterest income and lower loan loss provisions. Consumer loan demand and

demand for mortgage credit remained high in this time period as well. Banks also

benefited from a long period of low interest rates and good economic growth with low

inflation which encouraged borrowing. Credit card rates in particular did not fall as

quickly as bank costs, improving bank margins. Better information technology helped

reduce costs and the growth of credit derivatives and mortgage securitization helped

banks to continue high lending volume while shifting risks to other entities. The yield on

earning assets in 2004 was 5.18% and the cost of funding earning assets was 1.56%,

giving a net interest margin of 3.62%which is quite good.2

1U.S. banks had less exposure to the late 1990s Russian and Asian crises than banks of

other countries, presumably having learned their lesson from the LDC debt fiascoes of

the 1970s and 1980s, or more likely because of aggressive lending by Japanese banks.

2 Source FDIC Quarterly Banking Profile, Third Quarter 2004.

11-2

Chapter 11 – Commercial Banks: Industry Overview 6th Edition

As interest rates rose in 2005 and 2006 bank profitability remained strong although

increasing loan loss provisions and weaker trading revenue and servicing income kept

2006 profitability from reaching record highs. However the flattening yield curve,

competitive pricing and increases in fund costs contributed to falling profit rates at banks.

In late 2006 and in 2007 problems in mortgages also began to hurt banks. Foreclosure

filings jumped 93% in July 2007 from July 2006. In the fourth quarter of 2007 loan loss

provisions reached $31.3 billion, their highest level at the time since 1991. This was a

300% increase from the fourth quarter in the prior year although seven large institutions

accounted for over half the increase in loss provisions. Trading losses were $10.6 billion;

the first ever quarterly net trading loss. Ten large institutions accounted for the entire

decline in trading earnings. Net interest income rose 11.8% from the prior year’s same

quarter. In all, net income for the fourth quarter of 2007 was the lowest reported since

the same quarter in 1991. Earnings problems were widespread with 51% of all

institutions reporting lower net income, but the depth of the decline was driven by a few

large institutions. ROA for the quarter was only 0.18%, down from 1.20% in the 4th

quarter of the prior year. This was the lowest ROA since 1990 and ROE was only a

dismal 1.74%.3

In 2008 ROA was a dismal 0.13%, it fell again in 2009 to 0.09% before rising to 0.60%

in 2010. Similarly ROE was 1.33% in 2008, 0.85% in 2009 and 5.44% in 2010. The

problem was not in interest spreads as the net interest margin remained high throughout

the period (3.87% in 2010). Problems remained in credit losses. Less than half reporting

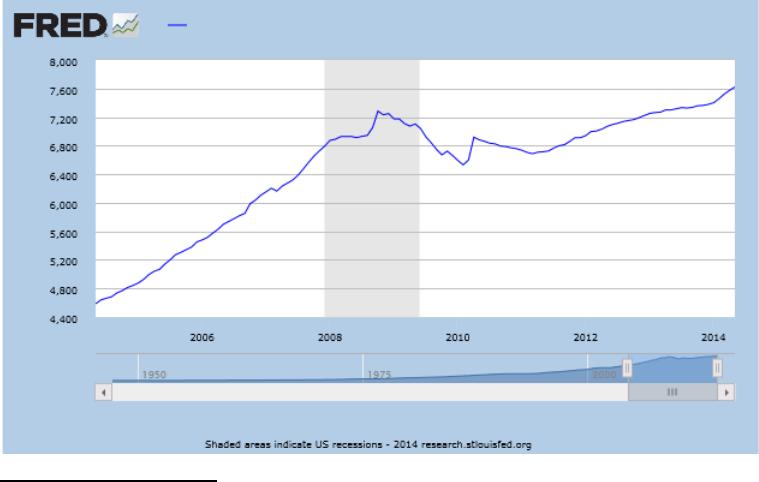

institutions saw earnings increases in 2007. Banks began reducing lending in late 2008

(see graph below). This has hurt the ability of small firms to grow and generate jobs.

Larger firms have been able to access bond financing and have not had the same funding

problems as smaller firms.

3 Data and analysis not in the text are from the FDIC Quarterly Banking Profile, Fourth

Quarter 2007.

11-3

Chapter 11 – Commercial Banks: Industry Overview 6th Edition

(Source: Federal Reserve Bank of St. Louis FRED data)

The provision for loan losses is a charge to earnings based on management’s expectation

of how many loans will go bad in the current quarter. Net charge offs (NCOs) are actual

write offs. Net charges offs reached five year highs in 2007, at $16.2 2 billion as

compared to $8.5 billion in the fourth quarter of 2006. This yielded an annualized net

charge off rate of 0.83%.4 NCOs continued to climb in 2008 and 2009 before beginning

to drop in 2010.

NCO rates Year 2013 all FDIC insured

commercial banks (% of loans)

Overall 0.70%

Real Estate 0.50%

C&I 0.30%

Consumer 2.16%

Credit Card 3.43%

Source FDIC Net Charge-Offs to Loans Statistics on DIs Report

NCO rates are all improving. The overall state of the banking industry is also improving.

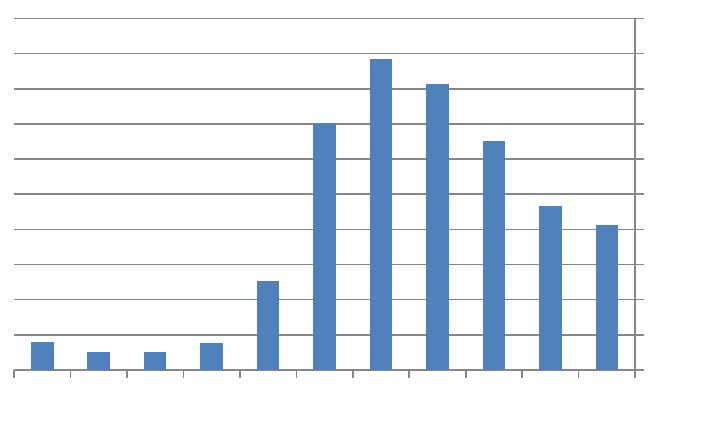

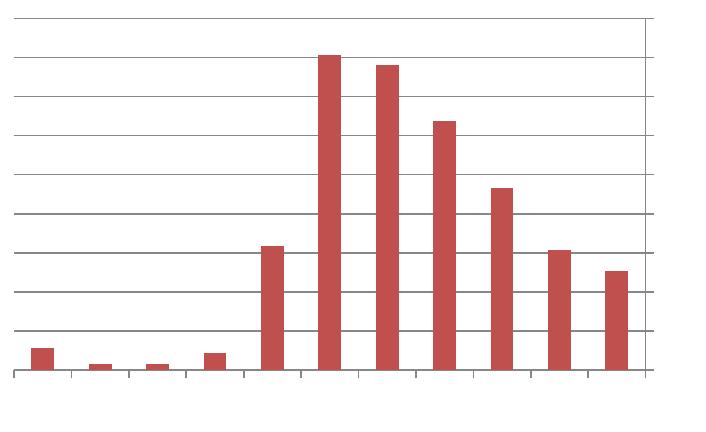

The number and assets of problem institutions are falling as indicated in the graphs below

after peaking in the 2009-2010 period:

4 Ibid

11-4

Chapter 11 – Commercial Banks: Industry Overview 6th Edition

2014 YTD

2013

2012

2011

2010

2009

2008

2007

2006

2005

2004

0

100

200

300

400

500

600

700

800

900

1000

Data Source: FDIC, Historical Statistics, Statistics at a Glance

11-5

Chapter 11 – Commercial Banks: Industry Overview 6th Edition

2014 YTD

2013

2012

2011

2010

2009

2008

2007

2006

2005

2004

0

50

100

150

200

250

300

350

400

450

Data Source: FDIC, Historical Statistics, Statistics at a Glance

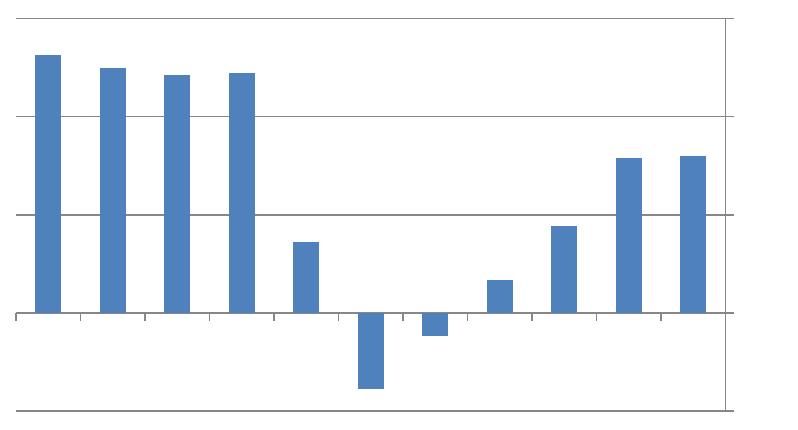

As a result of the reduced amount of failures the FDIC’s deposit insurance fund coverage

ratio has improved since its nadir in 2010 as depicted below:

11-6

Chapter 11 – Commercial Banks: Industry Overview 6th Edition

2014 YTD2013201220112010200920082007200620052004

-0.50

0.00

0.50

1.00

1.50

Data Source: FDIC, Historical Statistics, Statistics at a Glance

The long run of low interest rates has allowed banks to book good profits unrelated to

credit losses. For the year 2013 interest income fell by 3.10% but interest expense fell by

18.49% so that net interest income fell only slightly over the year by 0.83%. The

provision for loan loss fell by a large margin from $52.34 billion to $28.33 billion or

about a 46% drop. Trading account gains and fees rose by 24.6% over the year although

securities gains fell by 54%. Overall net income attributable to the bank rose by about

10% from $130.1 billion to $143.1 billion. Fifty-five percent of institutions had earnings

increases, and only about 7% were unprofitable for the year versus over 10% in 2012.

The yield on earning assets was 3.65% and the net interest margin was 3.25%. Return on

assets was 1.06% for the year and return on equity was 9.57%, both were improvements

from 2012 figures of 1.00% and 8.91% respectively. Net loans and leases to deposits

11-7

Chapter 11 – Commercial Banks: Industry Overview 6th Edition

remained steady in 2013 at 68.5% of deposits and the equity to asset ratio was largely

unchanged in 2013 at 11.11% from its value in 2012 at 11.10%.

3. Regulators

a. Federal Deposit Insurance Corporation

The FDIC, created in 1933, manages the deposit insurance funds for the thrift and

banking industries. The FDIC examines banks and disposes of failed bank and savings

association assets.

b. Office of the Comptroller of the Currency

The OCC has been around since the Civil War. The OCC grants national charters,

although banks may be state chartered instead. The OCC examines national banks and

approves or disapproves their merger applications.

Teaching Tip: Prior to 1863 the U.S. had only state chartered banks. In an attempt to help

finance the Civil War, the National Banking Acts of 1863 and 1864 created nationally

chartered banks that the federal government could more tightly regulate. The laws

required nationally chartered banks to hold U.S. government bonds to collateralize their

bank notes. This allowed the government to finance the rest of the war. The acts did not

outlaw state banking and as a result we have a dual banking system today.

About twenty-three percent of federally insured banks are nationally chartered banks; the

remainder is state chartered. Nationally chartered banks must be members of the Fed and

must be FDIC insured. State chartered banks have a choice on both. State chartered

banks may have fewer regulations imposed upon them and state chartered banks cannot

use the word ‘national’ in their name.

c. Federal Reserve System

About 31% of federally insured banks are members of the Federal Reserve and 69% are

not (Text Figure 11-8). Fed membership allows banks direct access to the FedWire

system. The Fed regulates bank holding company activities.

d. State Authorities

State chartered banks are regulated by state banking authorities. Federally insured state

chartered banks pass into receivership of the FDIC if they fail.

4. Global Issues

Total international asset positions of banks that report data to the Bank of International

Settlements (BIS) were $32.9 trillion at year end 2013. Of the top 20 global banks in the

world ranked by asset size, only 2 are U.S. banks (Citigroup and Bank of America).

Teaching Tip: This result is an artifact of U.S. bank regulations that have promoted small

community banks. If one looked at lists of the most profitable and sophisticated banks,

one would find more U.S. banks on that list.

The advantages of globalizing operations include:

11-8

Chapter 11 – Commercial Banks: Industry Overview 6th Edition

Additional risk diversification by including operations in other economies

Economies of scale and scope

U.S. banks have been global industry leaders in generating innovative new

products such as OTC derivatives not developed by overseas banks

Expanded funds sources

Maintenance of customer relationships as many corporate customers have gone

global and have needed banking services for their overseas operations

Avoidance of domestic regulations – The U.S. tends to be the most tightly

regulated market and engaging in overseas operations allows U.S. banks to

operate with less scrutiny

Disadvantages of globalization of banking services include:

Greater information production and monitoring costs involved in evaluating overseas

loans and investments. The U.S. generally has higher disclosure requirements than

most other countries.

Overseas operations may face expropriation or repatriation problems.

The fixed costs to enter foreign markets may be quite high and may not be easily

recovered once an investment is made.

Global Banking Performance

Overall European bank performance remained strong throughout the mid 2000s; however

the same structural forces affecting U.S. banks such as the flattening yield curve and

competitive pressures on NIMs eventually slowed profit growth. Mortgage demand

remained high through much of the period and boosted growth in Spain and France and

generally good growth in the euro area helped.

However foreign banks were not immune to the financial crisis of 2007 and 2008. In

Europe bank net income declined precipitously in 2008. Large banks in the UK, Ireland,

the Netherlands, Switzerland, Iceland and Spain recorded annual losses during the crisis.

In October 2008 the German government guaranteed all consumer bank deposits and

arranged a bailout of Hypo Real Estate, the country’s second largest commercial property

lender. The Netherlands, Belgium and Luxembourg put together a $16.37 billion bailout

of Fortis NV. Many European and Asian countries quickly passes stimulus packages to

offset the problems in the U.S. and their own economies.

The Greek economic crisis severely impacted many European banks and illustrates how

interconnected economies are today and demonstrates the risk of contagion. Problems in

Greece eventually led to banking crises in Spain, Portugal and Italy. Even the French

bank Credit Agricole announced record losses of over $4 billion (equivalent) on write

downs of Greek loans. Globally, the total banking exposure to the four imperiled

countries was over $2.5 trillion. At one point many questioned whether the common

currency could be maintained in light of the region’s problems. After meeting and

stalling for a long period Europe’s finance ministers and the IMF came up with a bailout

of $147 billion and a promise of funding up to $1 trillion to ensure stability. The price

tag was fiscal ‘austerity’ in Greece which as very unpopular and led to strikes and

protests and a change in government. Eventually however the reforms did bring about

11-9

Chapter 11 – Commercial Banks: Industry Overview 6th Edition

improvements in Greek credit and S&P raised the debt rating from ‘selective default’ to

B-.

Aggregate problems in banking are related to macroeconomic problems. As bank credit

growth fell or actually declined firms had to curtail spending plans which then led to

slower economic growth. Bank balance sheets fell throughout the latter part of the crisis

and have yet to fully recover. Growth in Europe remains anemic, and the threat of

deflation has encouraged more aggressive actions by the European Central Bank. The

ECB has reduced its target interest rate and now charges a negative deposit rate on

reserves to encourage bank lending.

Teaching Tip:

Europe is trying to defy economic laws, which is difficult to do in the long run. The euro

is not an ‘optimal currency area’ because of the lack of fiscal and bank integration.

Unless Europe can more fully integrate, expect a continuing need for fiscal transfers to

weaker economies and/or continued crises.

1.1.1.1

1.1.1.2 VI. Web Links

http://www.federalreserve.gov/ Website of the Board of Governors of the Federal

Reserve

http://www.mybank.com/ This comprehensive listing will help you locate

banks on the World Wide Web.

http://www.occ.treas.gov/ Office of the Comptroller of the Currency

http://www.americanbanker.com The publication of the banker’s trade association

http://www.wsj.com/ Website of the Wall Street Journal Interactive

edition. The web version of the well known

financial newspaper can be personalized to meet

your own needs. Instructors can also receive via

e-mail current events cases keyed to financial

market news complete with discussion questions.

http://www.fdic.gov/ The Federal Deposit Insurance Corporation’s

website: new regulations and current and historical

banking statistics are available on this site.

1.1.1.2.1.1 VII. Student Learning Activities

1. Go to Value Line Investment Surveys, Standard and Poors or some other investment

service and obtain a current industry analysis for the bank industry. Is performance

projected to improve over the data given in the text or is performance slipping?

11-10

Chapter 11 – Commercial Banks: Industry Overview 6th Edition

Identify the major causes of any differences.

2. How has the Dodd-Frank bill impacted profitability at U.S. banks? Are the impacts

the same for different size banks? Explain. Both the Wall Street Journal and the

Economist are good starting points for your research.

11-11