1.1.1.1.1Part III

1.1.1.1.2Commercial Banks

1.1.1.1.3

1.1.1.1.4Chapter Eleven

Commercial Banks: Industry Overview

1.1.1.2 I. Chapter Outline

1. Commercial Banks as a Sector of the Financial Institutions Industry: Chapter Overview

2. Definition of a Commercial Bank

3. Balance Sheets and Recent Trends

a. Assets

b. Liabilities

c. Equity

d. Off-Balance-Sheet Activities

e. Other Fee-Generating Activities

4. Size, Structure, and Composition of the Industry

a. Bank Size and Concentration

b. Bank Size and Activities

5. Industry Performance

6. Regulators

a. Federal Deposit Insurance Corporation

b. Office of the Comptroller of the Currency

c. Federal Reserve System

d. State Authorities

7. Global Issues

a. Advantages and Disadvantages of International Expansions

b. Global Banking Performance

1.1.1.3 II. Learning Goals

1. Define what a commercial bank is.

2. Identify the main assets held by commercial banks.

3. Identify the main liabilities held by commercial banks.

4. Understand the types of off-balance-sheet activities that commercial banks

undertake.

5. Discuss which factors have motivated the significant decrease in the number of

commercial banks.

6. Evaluate the performance of the commercial banking industry in recent years.

7. Know the main regulators of commercial banks.

8. List the world’s biggest banks.

1.1.1.4 III. Chapter in Perspective

This is the first of three chapters that cover commercial banks. Banks are the largest type of

depository institution (DI). Traditionally, commercial banks made working capital loans to

businesses and accepted commercial and individual checking and savings deposits. Today banks

and other DIs are much more diversified and offer many types of services. For example, large

banks engage in a variety of non-traditional banking activities ranging from underwriting

securities to selling insurance and offering complex derivative products to customers. The

chapter presents a common size bank balance sheet and a discussion of off-balance-sheet

activities and current performance measures. Current profit trends in banking are discussed and

the chapter concludes with coverage of the primary regulators of the banking industry and a good

discussion of global events in banking. Details of types of bank accounts, profit analysis and

capital and risk management are relegated to later chapters.

1.1.1.5 IV. Key Concepts and Definitions to Communicate to Students

Transaction accounts Regional or superregional bank

NOW account Federal funds market

Negotiable CDs Money center bank

Off-balance-sheet (OBS) asset Interest rate spread

Off-balance-sheet liability Provision for loan losses

Megamerger Net charge offs

Economies of scale Net operating income

Economies of scope Dual banking system

X efficiencies Holding company

Community bank Foreign banking systems

1.1.1.6 V. Teaching Notes

1. Commercial Banks as a Sector of the Financial Institutions Industry: Chapter

Overview

Banks are the country’s largest financial intermediary. In March 2014 there were 5,809

domestically chartered FDIC insured commercial banks with total assets of $13,855 billion

(FDIC Statistics at a Glance). During the financial crisis, Goldman-Sachs, Morgan-Stanley and

GMAC were allowed to switch their charters and become banks holding companies. This

allowed them access to deposit funding and made it easier to receive government assistance.

Investment banks funded themselves through short term money market borrowings, but these

markets become too expensive or not available during the crisis. The tradeoff was these

institutions had to accept tighter regulations that reduce their risk and meet higher capital

requirements. With this move and the merger or bankruptcy of Merrill-Lynch, Lehman Brothers

and Bear Stearns the major Wall Street firms ceased to exist as stand-alone entities.

Loans are the major asset of all banks and deposits are the primary funds source. The

composition of the loan portfolio has changed over time and deposits are not as great a

percentage of financing as in the past.

Teaching Tip: The primary assets and liabilities are pieces of paper. This means that banks and

other FIs will typically have a difficult time differentiating their product from one another, and

intense competition and low margins can be expected, particularly as previous significant

competitive barriers such as regulations, time and distance between banks, etc. have been eroded

by periods of deregulation and technological growth in information services. This means ROA is

traditionally low (1-3% range) and the temptation is to have too low capital in an attempt to lever

up ROE to acceptable levels. This problem is exacerbated by executive bonuses based on short

term bank performance measures such as ROE.

2. Definition of a Commercial Bank

Banks are a subset of the three main types of DIs: banks, savings institutions, and credit unions.

All three offer similar services. Banks will normally be larger, have a more diversified loan

portfolio that includes more business lending and will have more sources of funds beyond

deposits. Banks also play a unique role in our economy. The banking system is the conduit for

monetary policy and banks are involved in much of the payments system and in credit allocation.

Banks provide risk, maturity, denomination, and liquidity intermediation services to savers;

helping to maximize the amount of funds available to potential borrowers.

3. Balance Sheet and Recent Trends

a. Assets

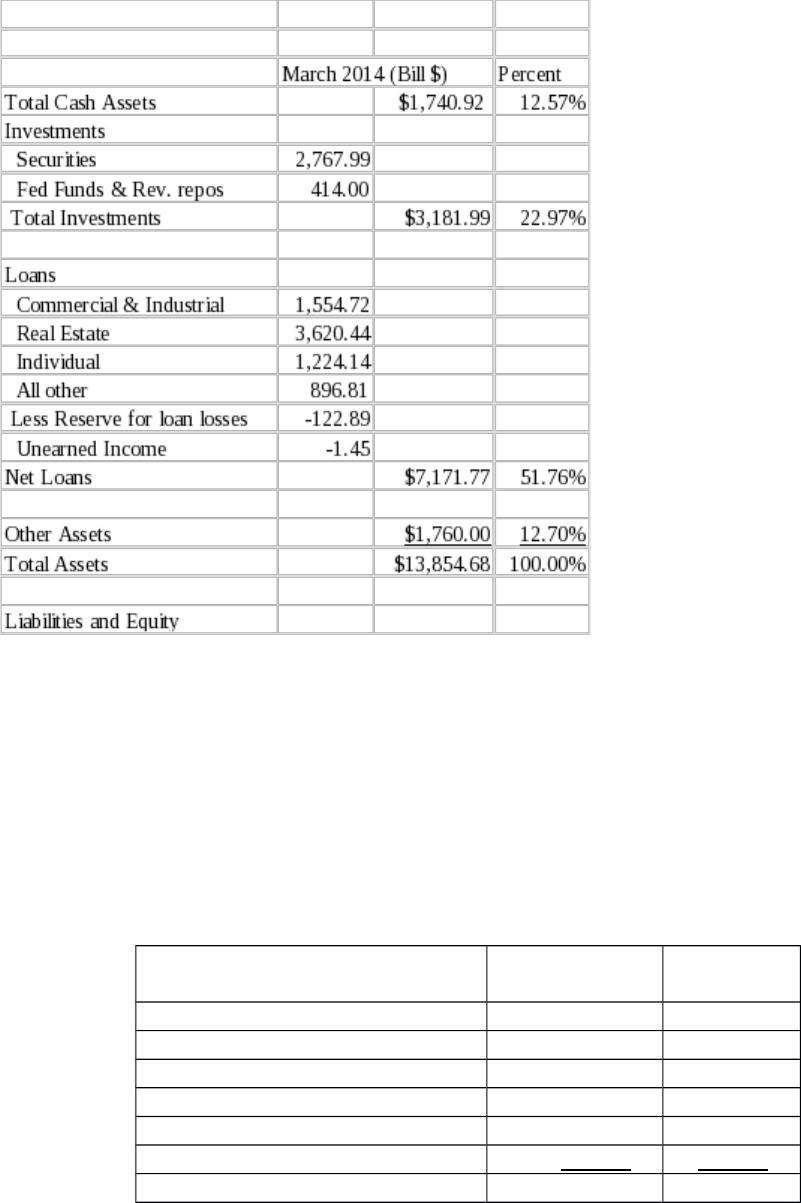

Major categories (as of 3/31/14) (Total Assets = $13,854.68 billion)

Liquid assets – Total cash assets (primarily vault cash, currency in the process of collection,

correspondent balances and reserves at the Fed) comprised 12.57% of assets. This is much

higher than in 2007.

Investment securities comprised about 23% of assets. U.S. government securities which

include Treasuries and other U.S. government obligations such as agency & GSE securities,

government backed pass-throughs and CMOS made up about 63% of the investment

portfolio.

Loans – Loans are the highest earning asset on the bank balance sheet. They are also the

largest category. As of 2013 loans comprised about 52% of total assets. The major loan

types include:

Bank loans by type % of Net

Loans

% of Assets

Commercial and industrial loans 21.68% 11.22%

Real estate loans 50.48% 26.13%

Consumer loans 17.07% 8.84%

Other loans 12.50% 6.47%

Reserve for loan losses -1.71% -0.89%

Reserves for unearned income -0.02% -0.01%

Totals 100.00% 53.33%

The reserve for loan losses has fallen since 2010. This is good since the primary risk a bank

faces is credit risk, and a bank is unlikely to be able to remain profitable if there are

significant problems in the loan portfolio.

Mortgage lending was increasing until very recently at most banks and C&I loans have been

declining. The former has occurred because of the demise of S&Ls and growth in the

mortgage markets. Longer term the latter is occurring because businesses have been able to

procure alternative financing through the commercial paper market at rates below bank loans

and because the public debt markets have grown rapidly. The financial crisis resulted in

reduced lending overall as the focus was on safety and less lending to risky commercial

entities. Percent of commercial loans is now beginning to increase again. It was about

17.4% of loans in 2010 and is almost 22% in 2014. The increase is most likely due to the

improving economy. The percentage of real estate loans on the balance sheet has fallen

slightly since 2010 when this category comprised 58% of loans.

Other assets, primarily non-earning assets accounted for about 12.70% of total assets.

Teaching Tip: In the 1950s cash and securities comprised some 70% of total assets and loans

were about 26%. What does this imply about how the industry has changed? Obviously,

liquidity risk and credit risk are much higher than in the past. However, banks now have more

funds sources and the loan portfolio is better analyzed and better diversified than in the past.

b. Liabilities

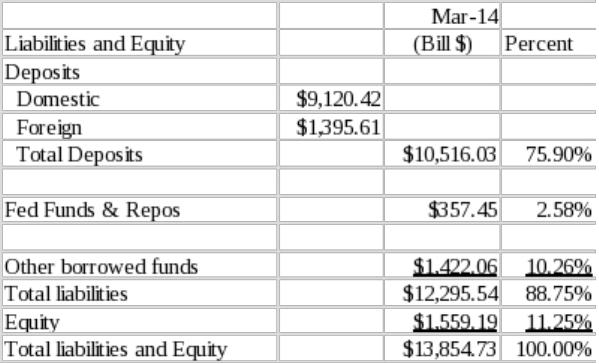

Major categories (March 2014 data)

Deposits: Deposits are the largest source of funds. As of 2013 deposits comprised almost

76% of total funding. About 49% of deposits were insured. Transaction accounts are

checking accounts (such as NOWs that pay interest or demand deposits that do not pay

interest).

Transaction deposits comprised 17.58% of total domestic deposits. Transactions deposits

are declining as a source of funding at banks.

Nontransaction deposits include savings account, MMDAs and CDs. In 2013

nontransaction accounts made up 82.42% of total deposits.

About 72% of domestic deposits are interest bearing and about 90% are retail, sometimes

called ‘core’ deposits.

Teaching Tip: In the 1950s interest bearing sources of funds were under 25% of total funding;

today most funds sources are interest bearing. What does this imply about the sensitivity of

bank profits to interest rates today as compared to the past? This also illustrates why banks

have sought to increase fee based sources of income in order to reduce the interest sensitivity

of their profits.

Borrowings and Other Liabilities include notes and bonds outstanding, fed funds

borrowed, and repurchase liabilities and were 17% of total funding.

The liabilities of banks tend to have less default risk than the assets and typically have a

shorter maturity than the assets. That is, banks normally provide maturity and credit risk

intermediation services to savers by providing savers with safer, shorter maturity accounts

while purchasing or creating longer term riskier claims. The banks in turn earn the interest

rate spread between the rates charged on the assets and the rates paid on the liabilities.

c. Equity

Capital requirements specify the minimum amount of capital a bank must maintain (see Chapter

13 for specific requirements) under the Basle Accord. Information on the Basle Accord and

recent changes can be found at the website of the Bank of International Settlements (BIS). In

March 2014 equity comprised 11.25% of total funding. Equity consists of common stock (par

and surplus), preferred stock and retained earnings. Regulators define other accounts that may

serve as equity for the purposes of calculating minimum capital requirements.

The TARP program resulted in capital injections into banks. The Treasury purchased over $200

billion of preferred stock and provided emergency funding of $25 billion to Citigroup and $20

billion to Bank of America. In total TARP funding was $386 billion although about $200 billion

had been paid back by the summer of 2010 (not including dividends earned of $25 billion) and as

of 2013 TARP funds were fully paid back and a surplus of $27 billion was remitted to the

Treasury. The nineteen largest U.S. banks were subjected to ‘stress tests’ to ensure they had

sufficient capital to survive a poor economic scenario (10% unemployment and another 25%

drop in home prices). The tests revealed that 10 of the 19 banks needed to increase their capital

by a total amount of almost $75 billion. This proved to be no problem and the institutions

quickly raised more than double the amount of capital needed.

According to the Board of Governors Press Release, March 26, 201, after the latest stress tests

the Fed approved the capital plans of 25 bank holding companies and objected to five other

plans. Four of the rejected plans failed on qualitative assessment grounds and the fifth had a

stressed scenario Tier 1 capital ratio less than 5%. The five rejected banks were Citigroup Inc.,

HSBC North America, RBS Citizens Financial, Santander Holdings USA and Zions

Bancorporation. Overall, the high quality capital to risk weighted assets ratio has increased from

5.5% in 2009 to 11.6% in the fourth quarter of 2013. The top 30 bank holding companies have

about 80% of all U.S. bank holding company assets. They are projected to continue increasing

capital through the first quarter of 2015 (Board of Governors Press Release).

Teaching Tip: Government involvement in executive pay for banks that took TARP funds

provided an incentive for banks to quickly repay TARP loans.

Teaching Tip: Students should be surprised to learn that banks typically employ about 90% debt

in their capital structure. Few nonfinancial firms allow their debt ratios to get over 50% (other

than in Highly Levered Transactions). Nonfinancial firms in volatile industries often use little or

no long term debt. DIs must employ a high amount of leverage to offer stockholders a

satisfactory rate of return since their ROA is generally very low (in the 0.5%-2% range). Their

ROA is low because they primarily have paper assets and liabilities. Recall from

microeconomics that in industries with non-differentiable products, competition will force

economic rents (NPVs) to zero. The ability of banks to use such high debt ratios arises from a)

banks’ ability to closely manage and hedge risk and b) deposit insurance. Banks that do not learn

to manage risk appropriately quickly fail when environmental factors change. Moreover, most

bank creditors do not demand a risk premium in the form of higher deposit rates at risky banks

because the government guarantees their deposits. This is an example of a market failure and

the problem of moral hazard engendered by deposit insurance.

d. Off-Balance-Sheet Activities

Off-balance-sheet (OBS) assets and liabilities are activities that may lead to changes in

on-balance-sheet assets and liabilities respectively, contingent upon some event occurring. The

notional value of derivatives at commercial banks was 1684.60% of assets in March 2014.

Example of OBS activities include (ranked by size in 2014):1

Interest rate contracts (including swaps, futures and forwards) 79.60%

Foreign exchange contracts (including swaps, spot and forwards) 14.14%

Credit derivatives 4.81%

Other commodities and equities 1.46%

Problems in OBS activity led to the TARP program, the Term Asset Backed Securities Loan

Facility (TALF) and the Public-Private Investment Fund (PPIF). The PPIF was designed to

purchase up to $1.25 trillion of real estate related OBS. This facility was jointly funded with

private money and matching government funds. They had completed their budgeted purchases

in March 2010. Because of problems with OBS securities the Dodd-Frank bill requires

regulation of OTC derivatives. Even in 2014 it is still unclear how detailed the regulations (and

how strict the enforcement) will eventually be.

e. Other Fee-Generating Activities

Much of this material is not in the text.

Correspondent banking – larger banks serve as agents for smaller banks, assisting in

check clearing

purchasing securities

foreign exchange

1 It is questionable whether the size of these commitments can be compared in this way since the

risks and likelihood of becoming an on balance sheet commitment varies dramatically for the

different activities.

loan participations (both ways)

obtaining and placing fed funds

trust services

obtaining brokered deposits (Jumbo C.D.s, Euro$)

Leasing – Banks may be able to use tax breaks from purchasing equipment that

small/medium size businesses cannot.

Trust operations – Trust functions are offered only by larger banks, but trust services are

made available at most banks through correspondent relationships. Trust operations are

providing fiduciary services for a third party.

Swap brokers – Many larger banks act as swap brokers/swap partners helping financial

institutions better match the interest sensitivity of their assets and liabilities. They take a fee

for this service.

Brokerage services

Underwriting- Underwriting income via bank subsidiaries.

Banks can advise and manage mutual funds but cannot sponsor the fund.