1. Options

Unlike futures and forwards, options give the holder the right, but not the obligation, to either

buy or sell the underlying commodity at a fixed price called the exercise or strike price.

American style options may be exercised at any time up to contract expiration. European

options can only be exercised at maturity. Some options on the S&P500 and some currency

options are European style. Note that the style has nothing to do with trading location. A buyer

may prefer European style options because they are typically cheaper than American options.

a. Call options

A call option provides the right to buy the underlying commodity. The call buyer must pay the

option premium (C) to the call writer. The option buyer may exercise the option and purchase

the underlying spot commodity by paying the exercise or strike price (X). The option has

intrinsic value if the underlying spot price (S) is greater than X. In this case the option is said to

be ‘in the money.’ If at expiration S > X, the option will be exercised, if not the option expires

worthless. In either case, the initial call price C is a sunk cost.

Call options will not normally be exercised prior to maturity unless the underlying commodity

pays a large enough cash flow prior to maturity, even if they are in the money. This is so because

the option is worth more “alive” (unexercised) than “dead” (exercised); the option has both time

value and intrinsic value. The time value is forfeited if the option is exercised. An option holder

wishing to terminate their option position could simply sell the option instead of exercising it.

Mathematically, this is equivalent to stating that C > Max (0, S-X) for a call prior to maturity.

Purchasing a call option is a bullish strategy that makes money if the underlying commodity

price rises. Writing a call is a neutral or bearish strategy. Buying a call is a limited loss strategy

with a potentially unlimited gain, writing a call is the opposite.

Teaching Tip: Options are wasting assets, their time value erodes as expiration approaches.

Option prices are also directly related to the level of underlying spot price volatility. Thus,

buying an option is a bet that either a) the spot price will increase enough to offset the loss in

time value and/or b) the spot price volatility will increase enough to offset the loss in time value.

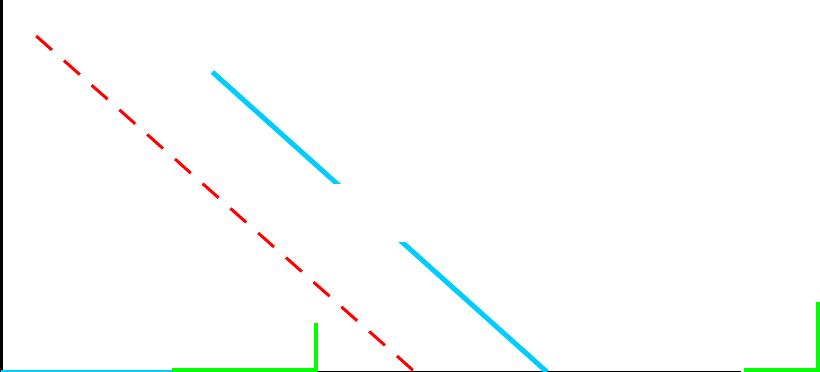

Teaching Tip: Comparing a call option with a spot position.

Suppose an at the money American style Swiss franc (Sfr or CHX on quote sheets) call option

has the following terms:

Exercise price 1Sfr = $0.655 Option Premium = 2¢/Sfr

Contract size = 62,500 Sfr Expiration = 90 days

This option gives the buyer the right to purchase 62,500 Sfr at any time within the next 90

days at an exercise (or strike) price of 62,500 Sfr $0.655/Sfr = $40,937.50.

The price the option buyer must pay to obtain this right (the premium) is 62,500 Sfr

$.02/Sfr = $1,250. Assuming the buyer holds the option to just before expiration for

simplicity, the investor’s profit diagram is:

Profit

Spot

ST

$0.655

This option position does not appear very risky due to the limited loss feature of the option, but it

is actually riskier than a spot position. Why?

• To compare to the option to a spot position you would have to consider an equivalent dollar

amount invested ($40,937.50) or buying 32.75 option contracts ($40,937.50/$1,250). In the

option position, you have only a few months for the currency to move or you stand to lose

100% of $40,937.50.

Teaching Tip: An investor can purchase at the money, in the money, or out of the money calls.

In the money calls will have a larger potential dollar loss but a lower breakeven than out of the

money calls. Out of the money calls are more likely to result in a loss, but may yield high

percentage rates of return if the commodity price increases significantly.

Teaching Tip: To go from a long call to a written call position simply flip the call graph vertically

upside down. The maximum loss will become the maximum gain and the positive slope line will

have a negative slope. To go from a call position to a put position with equivalent terms, flip the

graph horizontally.

Teaching Tip: A majority of options expire worthless and many institutions write calls to

generate additional income to improve their current period rate of return.

b. Put options

A put option provides the right to sell the underlying commodity. The put buyer must pay the

option premium (P) to the put writer. The option buyer may exercise the option and sell the

underlying spot commodity by delivering the commodity in exchange for the exercise or strike

price (X). The option has intrinsic value if the underlying spot price (S) is less than X. If at

expiration S < X the option will be exercised, if not the option expires worthless. In either case

the initial put price P is a sunk cost.

Similar to calls, put options will not normally be exercised prior to maturity unless the option is

deep in the money.

-$1,250 $0.675

Purchasing a put option is a bearish strategy that makes money if the underlying commodity

price falls. Writing a put is a neutral or bullish strategy. Buying a put is a limited loss strategy

with a potentially large gain, writing a put is the opposite.

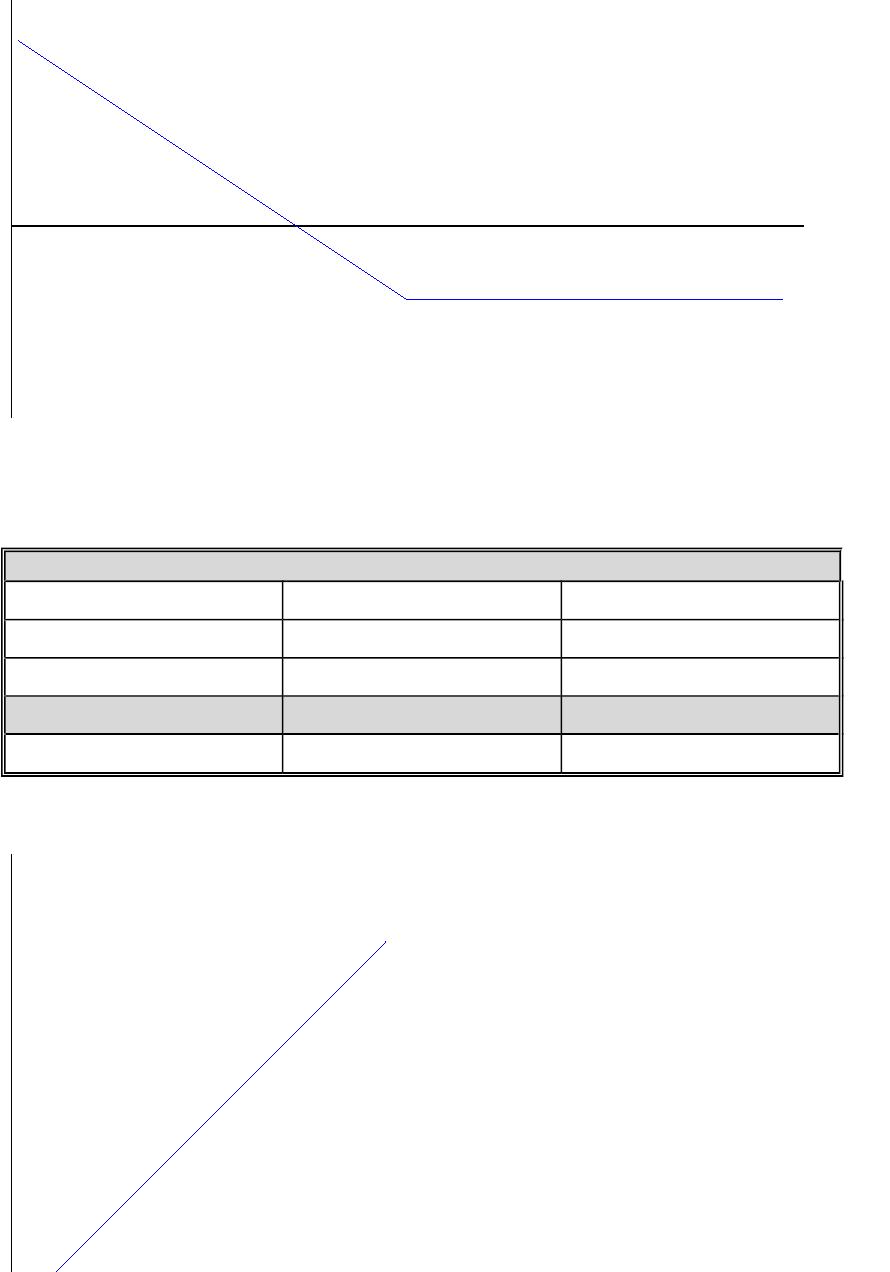

Long Put

Profit

Teaching Tip: The profit diagram of any option position (or any option hedge) can be found from

a profit table as below, where 0 = time of put purchase, T = contract expiration. The breakeven is

found by setting the profit to zero and solving for ST. These tables and the associated graphs are

excellent teaching tools.

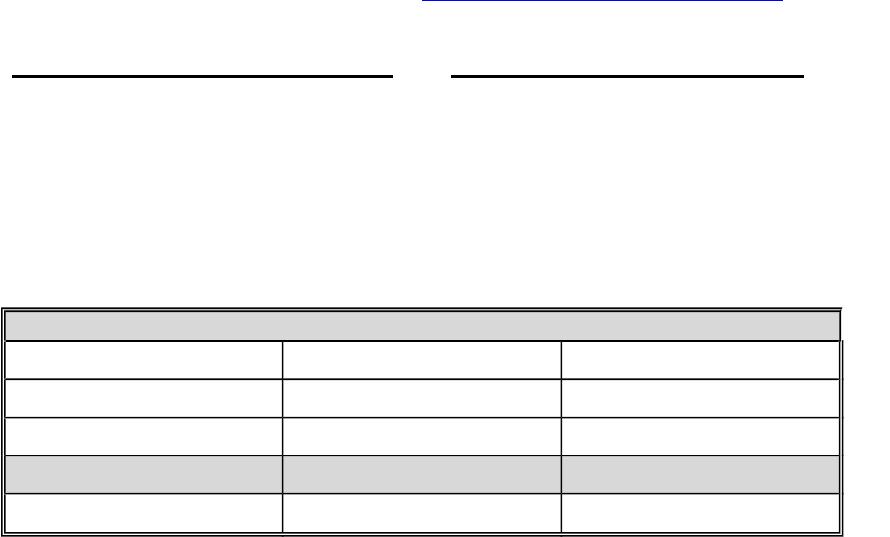

1.1 BUYING A PUT

1.1.1 Profit Table ST < E ST > E

-P0-P0-P0

+PTE- ST0

= Profit E – ST – P0-P0

Breakeven ST = E – P0

If ST does not appear in the profit equation, the profit graph is a straight line, whereas if ST is

present the sign on ST indicates the slope (positive or negative) of the line.

Writing a put

Profit

St

X

1.2 WRITING A PUT

1.2.1 Profit Table ST < E ST > E

+P0+P0+P0

-PT-(E- ST) 0

= Profit ST – E + P0+P0

Breakeven ST = E – P0

c. Option Values

The intrinsic value of a call option is the maximum of zero or S-X.

The intrinsic value of a put option is the maximum of zero or X-S.

An option also has time value because the option’s returns are asymmetric. An out of the money

option that has not yet expired may yet wind up in the money, an in the money option may wind

up further in the money. If not, the option is simply not used. As a result, normally an option is

worth more than its intrinsic value. The option’s time value is calculated as the option premium

minus the intrinsic value.

Teaching Tip: The time value is representative of the right to purchase the security or not,

depending upon whether it is profitable to do so. It literally represents the probability that the

commodity price will increase and move the option further in the money. Time value is greatest

for an at the money option. For deep out of the money options, the time to expiration provides

little likelihood that an option will be exercised; for deep in the money options, the ability to not

exercise the option has little value.

Other variables include:

: The greater the standard deviation of the value of the underlying security the greater

the option’s value. This is because the option is a right that can be used if profitable and

not used if it is not desirable.

St

X

Risk free rate (Rf): The greater the risk free rate the higher (lower) the value of a call

(put) option, ceteris paribus. This is because buying a call is an alternative to buying

stock on margin. The cost of buying stock on margin is increased by higher interest rates,

making the call alternative more valuable. Buying a put is an alternative to shorting the

underlying stock and investing the proceeds at Rf. With a higher Rf the put alternative is

relatively less valuable.

Time to expiration: Generally, the longer the time period until expiration the greater the

option’s value.

d. Option Markets

The average number of exchange trade option contracts outstanding was about $32 trillion in

2010. The value of options contracts traded worldwide in 2013 was over $9.4 trillion according

to the FIA Annual Volume Survey. From modest beginnings in 1973 with the Chicago Board

Options Exchange (CBOE), the world’s first market dedicated to options, option trading has

grown worldwide. In the U.S. options are traded similarly to futures in trading pits at open

outcry auctions. In 2000, the CBOE introduced hand held computers that greatly accelerated

order execution.

Options on individual common stocks and stock indexes are popular today for both hedgers

and speculators. Hedgers may use long put options or written call options on individual

stocks or indexes to hedge a long stock position. Stock index options are cash settled and the

major S&P500 contract is a European option. Index options allow the investor to hedge

systematic risk and partial hedges can be used to adjust a portfolio’s beta up or down.

Listed stock option contracts are for 100 shares. An AMR options quotes can be used to

illustrate:

Example January AMR options quote:

AMR Underlying stock price $8.79

Expiratio

n

Call Put

STRIK

E

LAS

T

VOLUM

E

OPEN

INTERES

T

LAS

T

VOLUM

E

OPEN

INTERES

T

May 6.00 3.30 12 578 0.45 20 4175

Jan 7.50 1.30 60 17062 0.15 138 58909

The May call is in the money and the call premium is $3.30 * 100 = $330. The intrinsic value of

the call (S-X) is ($8.79 – $6.00) * 100 = $279. The time value of the call is $330 – $279 = $51.

An investor would not exercise this call because that would be throwing away the $51 time

value. The May put is out of the money and the put’s intrinsic value (X-S) is 0. Note that the put

still has time value however equal to $0.45 * 100 = $45. Notice that the closer to the money

option has much higher open interest.

Options exist on futures contracts as well. The buyer of a call (put) option on a futures

contract has the right, but not the obligation, to purchase (sell) a futures contract at the

exercise price. Options on futures are popular because it is often cheaper to deliver the

futures contract rather than the underlying commodity. The futures contract is typically more

liquid than the underlying spot and more information about supply and demand for futures

may be available than can be easily found for the underlying commodity or security.

The Philadelphia Options Exchange offers several popular currency options contracts.

Options are available for the euro, British pound, Japanese yen, Australian dollar, Canadian

dollar and the Swiss franc.

Options may be used to limit default risk as well. Credit spread options and digital default

options are two examples:

Credit spread call options may be used to provide a payoff in the event of a loan default.

A credit spread call option pays the holder if the default risk premium or yield spread on

a specified benchmark bond of the borrower increases above some exercise spread.

A digital default option pays a stated amount, usually the par on the loan or bond in the event of

a default on the underlying credit.

2. Regulation of Futures and Options Markets

The Commodity Futures Trade Commission (CFTC) is the main regulator of futures

contracts and options on futures contracts. The CFTC seeks to eliminate trading abuses and

prevent market manipulation.

The Securities Exchange Commission (SEC) regulates options on stocks and stock indexes.

The bank regulators have guidelines for institutions to follow. A bank must have internal

hedging guidelines and policies. The bank must have derivatives trading limits and must

disclose large positions that could materially affect the bank. Regulators can mandate a bank

hold more capital to offset risk from derivatives positions. The financial crisis revealed that

regulators had not required sufficient capital to back banks’ off balance sheet derivative

activities.

Until the Dodd-Frank Act neither the SEC nor the CFTC directly regulated OTC derivatives.

Under the new law OTC derivatives may be required to be traded on an exchange and as

such would come under the purview of the SEC and CFTC. Moreover bank regulators will

presumably more tightly regulate bank usage of derivatives.

3. Swaps

A swap is an agreement whereby two parties agree to pay each other specified cash flows for a

set period of time. They are custom designed contracts primarily used to hedge currency and/or

interest rate risk. Interest rate swaps, currency swaps, credit risk swaps, commodity swaps and

equity swaps comprise the major types.

a. Interest Rate Swaps

According to the Bank of International Settlements, as of June 2013 the notional principal of

interest rate swap contracts outstanding was $425.6 trillion. Interest rate swaps are by far the

largest single component of the OTC derivatives market. The euro is the largest component of

single currency interest rate swaps at $168.7 trillion followed by the U.S. dollar at $120.3

trillion. Note that the notional principal amounts overstate the significance of the interest rate

swap market since these amounts are NOT swapped. The market value of the interest rate swap

market is a better measure of the true size and the market value was $13.7 trillion.

In a plain vanilla interest rate swap one party agrees to pay a fixed interest rate on a given

notional principal to the counterparty, and the counterparty agrees to pay a variable rate of

interest on the same notional principal. Swap maturities range from a few months to many years.

The party making a fixed interest payment may be called the swap buyer, whereas the party

making a variable payment may be called the swap seller. Principal is not normally exchanged;

hence the term notional principal designates only the amount used to calculate the dollars of

interest paid. Only net payments are actually transferred.

An institution that has too many rate sensitive liabilities relative to its holdings of rate sensitive

assets is at risk from an interest rate increase (the typical position of a mortgage lender that is

funding the mortgages with deposits). This FI may seek a swap where the FI agrees to pay a

fixed rate of interest in exchange for receiving a variable rate of interest. See the swap diagram

below. If their own liability costs rise with rising interest rates, the swap payments received will

also rise but their swap outflows are fixed. Thus, profitability is protected from an interest rate

change. Large money center banks are often willing to serve as a counterparty to a bank or thrift

in need of a swap. The intermediary banks may also act as brokers by finding a suitable

counterparty.

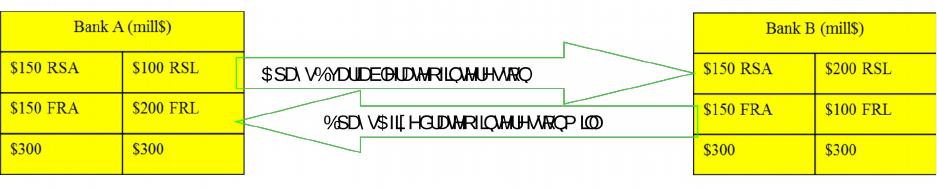

The term RSA is equal to rate sensitive assets, RSL is equal to rate sensitive liabilities, FRA and

FRL are fixed rate assets and liabilities respectively. Rate sensitive assets and liabilities are those

whose income or cost will change over some planning period if interest rates change and fixed

rate accounts will not. Any gains or losses to both banks should now be limited because both

wind up with equal amounts of rate sensitive assets and liabilities after including the effects of

the off balance sheet swap. Any profit changes due to the swap should be at least roughly offset

by offsetting changes in costs and rates of return on the balance sheet.

Credit risk exposure on a swap is less than on a loan since no principal is involved and only net

interest payments are at risk but credit risk is still present. The agent bank may guarantee swap

payments for a fee.

b. Currency Swaps

Currency swaps may be used to hedge mismatches in the currency of a FI’s assets and liabilities

or other commitments. As of June 2013 the notional principal of currency swap contracts

outstanding (adjusted for double counting) was $24.6 trillion. Note that most currency swaps do

involve swapping principal.

Fixed for fixed currency swaps involve a swap of principal and interest between two parties at a

fixed rate of exchange.

Fixed for floating currency swaps can be used to hedge both currency and interest rate

exposure simultaneously.

Teaching Tip: For example, a U.S. firm might have a British subsidiary that is earning pounds.

Suppose the subsidiary is not well known and cannot procure pound financing at an acceptable

cost, so the parent arranges variable rate dollar loans. The U.S. parent is now at risk if the pound

declines because a depreciating pound will make repaying the dollar loans more expensive.

Moreover, the loans are variable rate and cannot be fully hedged with forward contracts because

of the changing outflow amounts. The parent may arrange a swap with a counterparty where the

British subsidiary agrees to pay a fixed rate of interest (and principal when due) in pound sterling

in exchange for receiving a dollar denominated variable rate of interest (and principal).

c. Credit Swaps

BIS data indicates that credit swaps grew rapidly before the financial crisis and in 2013 there was

an estimated $21 trillion in notional principal on credit default swaps or CDS for short. This

number has been declining from its peak at $62 trillion in 2007. Losses on mortgage related

CDS written by Lehman Brothers and AIG led to the insolvency of these firms. Central clearing

houses have now been created for both Europe and the U.S. The major problem with the CDS

market was the lack of collateral and capital to back the promise to pay in the event of a default.

Clearinghouses can reduce or eliminate counterparty risk by requiring margin sufficient to back

the net value of the contract. These contracts are also employing more standardized terms.

There are two types of CDS. In a Total Return CDS, one party pays either a fixed or a variable

rate of interest to the seller and the counterparty makes floating rate payments representing the

total return (interest and principal value changes) on an underlying credit instrument. Values of

the total return CDS respond to more than changes in underlying default risk. In a Pure CDS the

protection buyer will make a fixed periodic payment to the protection seller and the protection

seller will pay the protection buyer if a credit event occurs.1 If the CDS is cash settled the

protection seller will pay the buyer the drop in price of the reference entity credit. If the CDS is

physical settled the buyer delivers the underlying bond or loan, and the seller pays the par value

of the security. Since no economic tie is required between the protection buyer and the reference

entity credit the notional principal outstanding on CDS can be far larger than the underlying

credit. Protection sellers can generate premium income with only a minimal upfront capital

requirement if the seller has a strong credit rating. This leads to the possibility of the creation of

an excessive amount of CDS. The top sellers of CDS have been hedge funds seeking additional

income, although insurers have been net sellers as well. If either the protection seller’s credit

standing or the reference entity’s credit rating drops, the buyer may require more collateral which

can pressure sellers financially. In early 2008 during the financial crisis the costs of this type

insurance rose dramatically. For instance, the cost to insure against a Citigroup debt issue default

increased from $9,700 in June 07 to $72,000 in January 2008 to $190,000 in March 2008,

reflecting the greater probability of default (source follows).2

1 The ‘credit event’ is typically default. For more information see the CBOT website file titled

“CDR Liquid 50 TM NAIG Index Futures FAQs.”

2 For more information see, “Swap Skirmish: Risks Hidden, Says Hedge Fund Citigroup, Wachovia Face Lawsuits

Involving Credit Derivatives,” by Susan Pulliam, Serena Ng & Tom Mcginty, The Wall Street Journal Online,

March 4, 2008; Page C1 and “New Spasm Jolts Credit Markets: Bankers Rattled As Turmoil Returns To

Short-Term Loans,” by Liz Rappaport, Joellen Perry And Deborah Lynn Blumberg, The Wall Street Journal

Online, March 6, 2008; Page A1.

Credit swaps allow a loan originator to shift the risk of a loan default to a swap seller. This may

allow more credit formation and generate faster economic growth, but it may also lead to an

erosion of underwriting standards. This undoubtedly occurred prior to the financial crisis of

2007-2008 and was a significant cause of the problems that ensued in mortgages.

d. Swap Markets

Swap dealers greatly facilitate the market for swaps. Large commercial banks and investment

banks are the primary swap dealers. Swap dealers usually guarantee payments on both sides of

the swap (for a fee). Dealers book their own swaps and keep a ‘swap book’ to facilitate

management of their net payment obligations. Regulators have worried that the swap market is

largely unregulated and some of the specific terms of swap agreements may not be publicly

available. Since the swap market involves U.S. banks, swap market activities are indirectly

regulated through the normal bank regulatory process. The Basle accord also specifies capital

requirements to offset the risks associated with swaps. As a result of the financial crisis swaps

will be more regulated. Although details are not available as of this writing it is likely that credit

default swaps will have either collateral requirements and/or be required to clear on an exchange.

6. Caps, Floors and Collars

Caps, floors and collars are options on interest rates. The majority of these contracts have

between 1 and 5 year maturities, although some have longer expirations.

Cap: A cap is an OTC call option on interest rates. Conceptually, it may also be thought of as

a put option on bond prices. If interest rates rise above a specified minimum (the strike

“price” or “cap rate”), the seller of the cap pays the buyer the difference between the market

interest rate and the strike interest rate times the notional value. Settlement (payment) dates

may be at the end of contract, annually, or at other times negotiated by the parties.

Floor: A floor is an OTC put option on interest rates. Conceptually, it may also be thought of

as a call option on bond prices. If interest rates fall below a specified minimum (the strike

“price” or “floor rate”), the seller of the floor pays the buyer the difference between the strike

and the market interest rate times the notional value.

Collar: A collar is a simultaneous position in a cap and a floor. If a FI is at risk from rising

(falling) interest rates they may wish to buy a cap (floor). To offset some of the cost of

purchasing the cap (floor) the FI may simultaneously sell a floor (cap).