CHAPTER 7 FUTURES AND OPTIONS ON FOREIGN EXCHANGE

ANSWERS & SOLUTIONS TO END–OF-CHAPTER QUESTIONS AND PROBLEMS

QUESTIONS

1. Explain the basic differences between the operation of a currency forward market and a

futures market.

Answer: The forward market is an OTC market where the forward contract for purchase or sale

of foreign currency is tailor-made between the client and its international bank. No money

changes hands until the maturity date of the contract when delivery and receipt are typically

2. In order for a derivatives market to function most efficiently, two types of economic agents

are needed: hedgers and speculators. Explain.

Answer: Two types of market participants are necessary for the efficient operation of a

derivatives market: speculators and hedgers. A speculator attempts to profit from a change in

the futures price. To do this, the speculator will take a long or short position in a futures contract

depending upon his expectations of future price movement. A hedger, on-the-other-hand,

3. Why are most futures positions closed out through a reversing trade rather than held to

delivery?

Answer: In forward markets, approximately 90 percent of all contracts that are initially established

result in the short making delivery to the long of the asset underlying the contract. This is natural

because the terms of forward contracts are tailor-made between the long and short. By contrast,

4. How can the FX futures market be used for price discovery?

Answer: To the extent that FX forward prices are an unbiased predictor of future spot exchange

rates, the market anticipates whether one currency will appreciate or depreciate versus another.

Because FX futures contracts trade in an expiration cycle, different contracts expire at different

periodic dates into the future. The pattern of the prices of these contracts provides information

5. What is the major difference in the obligation of one with a long position in a futures (or

forward) contract in comparison to an options contract?

Answer: A futures (or forward) contract is a vehicle for buying or selling a stated amount of

foreign exchange at a stated price per unit at a specified time in the future. If the long holds the

contract to the delivery date, he pays the effective contractual futures (or forward) price,

regardless of whether it is an advantageous price in comparison to the spot price at the delivery

6. What is meant by the terminology that an option is in-, at-, or out-of-the-money?

Answer: A call (put) option with St > E (E > St) is referred to as trading in-the-money. If St E

7. List the arguments (variables) of which an FX call or put option model price is a function.

How does the call and put premium change with respect to a change in the arguments?

Answer: Both call and put options are functions of only six variables: St, E, ri, r$, T and .

When all else remains the same, the price of a European FX call (put) option will increase:

When r$ and ri are not too much different in size, a European FX call and put will increase in

price when the option term-to-maturity increases. However, when r$ is very much larger than ri,

a European FX call will increase in price, but the put premium will decrease, when the option

PROBLEMS

1. Assume today’s settlement price on a CME EUR futures contract is $1.3140/EUR. You have

a short position in one contract. Your performance bond account currently has a balance of

$1,700. The next three days’ settlement prices are $1.3126, $1.3133, and $1.3049. Calculate

the changes in the performance bond account from daily marking-to-market and the balance of

the performance bond account after the third day.

2. Do problem 1 again assuming you have a long position in the futures contract.

Solution: $1,700 + [($1.3126 – $1.3140) + ($1.3133 – $1.3126) + ($1.3049 – $1.3133)] x

With only $562.50 in your performance bond account, you would experience a margin call

3. Using the quotations in Exhibit 7.3, calculate the face value of the open interest in the

September 2013 Swiss franc futures contract.

Solution: 4,207 contracts x SF125,000 = SF525,875,000, where SF125,000 is the contract size

4. Using the quotations in Exhibit 7.3, note that the September 2013 Mexican peso futures

contract has a price of $0.07713 per MXN. You believe the spot price in September will be

$0.08365 per MXN. What speculative position would you enter into to attempt to profit from

your beliefs? Calculate your anticipated profits, assuming you take a position in three contracts.

What is the size of your profit (loss) if the futures price is indeed an unbiased predictor of the

future spot price and this price materializes?

Solution: If you expect the Mexican peso to rise from $0.07713 to $0.08365 per MXN, you

Your anticipated profit from a long position in three contracts is: 3 x ($0.08365 – $0.07713)

If the futures price is an unbiased predictor of the expected spot price, the expected spot

price is the futures price of $0.07713 per MXN. If this spot price materializes, you will not have

5. Do problem 4 again assuming you believe the September 2013 spot price will be $0.07061

per MXN.

Solution: If you expect the Mexican peso to depreciate from $0.07713 to $0.07061 per MXN,

Your anticipated profit from a short position in three contracts is: 3 x ($0.07713 – $0.07061)

If the futures price is an unbiased predictor of the future spot price and this price

6. Using the market data in Exhibit 7.6, show the net terminal value of a long position in one

100 Aug Japanese yen European call contract at the following terminal spot prices (stated in

U.S. cents per 100 yen): 91, 95, 100, 105, and 109. Ignore any time value of money effect.

Solution: The net terminal value of one call contract is:

[Max[ST – E, 0] – Ce] x JPY1,000,000/100 ÷ 100¢, where JPY1,000,000 is the contract size of

one JPY contract.

At 91: [Max[91 – 100, 0] – 2.83] x JPY1,000,000/100 ÷ 100¢ = -$283

7. Using the market data in Exhibit 7.6, show the net terminal value of a long position in one

100 Aug Japanese yen European put contract at the following terminal spot prices (stated in

U.S. cents per 100 yen): 91, 95, 100, 105, and 109. Ignore any time value of money effect.

Solution: The net terminal value of one put contract is:

At 91: [Max[100 – 91, 0] – 1.97] x JPY1,000,000/100 ÷ 100¢ = $703

At 95: [Max[100 – 95, 0] – 1.97] x JPY1,000,000/100 ÷ 100¢ = $303

8. Assume that the Japanese yen is trading at a spot price of 92.04 cents per 100 yen. Further

assume that the premium of an American call (put) option with a striking price of 93 is 2.10

(2.20) cents. Calculate the intrinsic value and the time value of the call and put options.

Solution: Premium – Intrinsic Value = Time Value

9. Assume spot Swiss franc is $0.7000 and the six-month forward rate is $0.6950. What is the

minimum price that a six-month American call option with a striking price of $0.6800 should sell

for in a rational market? Assume the annualized six-month Eurodollar rate is 3 ½ percent.

Solution:

Ca Max[(70 – 68), (69.50 – 68)/(1.0175), 0]

10. Do problem 9 again assuming an American put option instead of a call option.

11. Use the European option-pricing models developed in the chapter to value the call of

problem 9 and the put of problem 10. Assume the annualized volatility of the Swiss franc is 14.2

percent. This problem can be solved using the FXOPM.xls spreadsheet.

Solution:

d1 = [ln(69.50/68) + .5(.142)2(.50)]/(.142).50 = .2675

N(d1) = .6055

N(d2) = .5664

12. Use the binomial option-pricing model developed in the chapter to value the call of problem 9.

The volatility of the Swiss franc is 14.2 percent.

Solution: The spot rate at T will be either 77.39¢ = 70.00¢(1.1056) or 63.32¢ = 70.00¢(.9045),

where u = e.142.50 = 1.1056 and d = 1/u = .9045. At the exercise price of E = 68, the option will

The hedge ratio is h = (9.39 – 0)/(77.39 – 63.32) = .6674.

Thus, the call premium is:

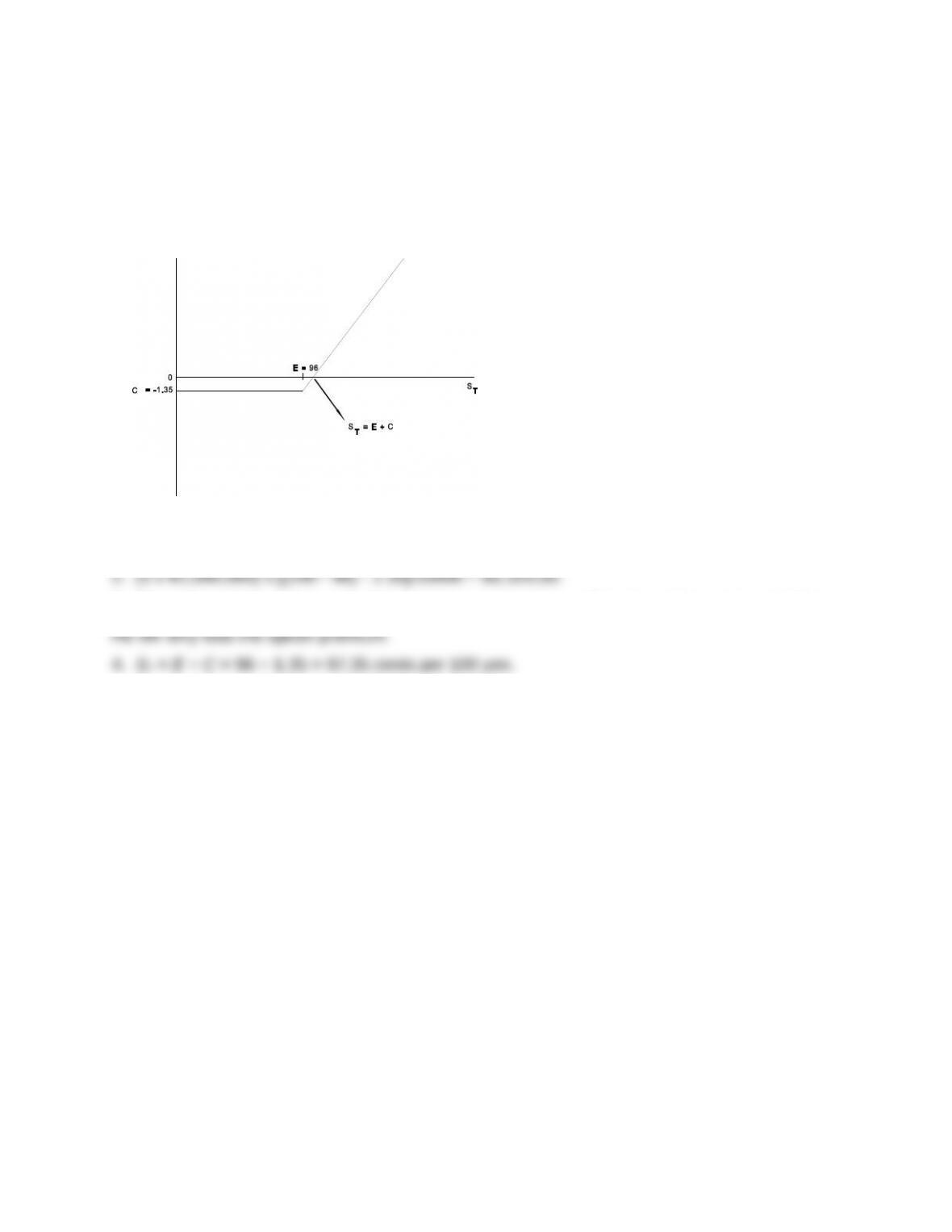

A speculator is considering the purchase of five three-month Japanese yen call options with

a striking price of 96 cents per 100 yen. The premium is 1.35 cents per 100 yen. The spot price

is 95.28 cents per 100 yen and the 90-day forward rate is 95.71 cents. The speculator believes

the yen will appreciate to $1.00 per 100 yen over the next three months. As the speculator’s

assistant, you have been asked to prepare the following:

1. Graph the call option cash flow schedule.

2. Determine the speculator’s profit if the yen appreciates to $1.00/100 yen.

3. Determine the speculator’s profit if the yen only appreciates to the forward rate.

4. Determine the future spot price at which the speculator will only break even.

Suggested Solution to the Options Speculator:

1. +

–

3. Since the option expires out-of-the-money, the speculator will let the option expire worthless.