9. Due to the integrated nature of their capital markets, investors in both the U.S. and U.K.

require the same real interest rate, 2.5%, on their lending. There is a consensus in capital

markets that the annual inflation rate is likely to be 3.5% in the U.S. and 1.5% in the U.K. for the

next three years. The spot exchange rate is currently $1.50/£.

a. Compute the nominal interest rate per annum in both the U.S. and U.K., assuming that the

Fisher effect holds.

b. What is your expected future spot dollar-pound exchange rate in three years from now?

c. Can you infer the forward dollar-pound exchange rate for one-year maturity?

Solution.

a. Nominal rate in US = (1+ρ) (1+E(π$)) – 1 = (1.025)(1.035) – 1 = 0.0609 or 6.09%.

10. After studying Iris Hamson’s credit analysis, George Davies is considering whether he can

increase the holding period return on Yucatan Resort’s excess cash holdings (which are held in

pesos) by investing those cash holdings in the Mexican bond market. Although Davies would be

investing in a peso-denominated bond, the investment goal is to achieve the highest holding

period return, measured in U.S. dollars, on the investment.

Davies finds the higher yield on the Mexican one-year bond, which is considered to be

free of credit risk, to be attractive but he is concerned that depreciation of the peso will reduce

the holding period return, measured in U.S. dollars. Hamson has prepared selected economic

and financial data, given in Exhibit 3-1, to help Davies make the decision.

Selected Economic and Financial Data for U.S. and Mexico

Expected U.S. Inflation Rate 2.0% per year

Expected Mexican Inflation Rate 6.0% per year

U.S. One-year Treasury Bond Yield 2.5%

Mexican One-year Bond Yield 6.5%

Nominal Exchange Rates

Spot 9.5000 Pesos = U.S. $ 1.00

One-year Forward 9.8707 Pesos = U.S. $ 1.00

Hamson recommends buying the Mexican one-year bond and hedging the foreign currency

exposure using the one-year forward exchange rate. She concludes: “This transaction will result

in a U.S. dollar holding period return that is equal to the holding period return of the U.S. one-

year bond.”

a. Calculate the U.S. dollar holding period return that would result from the transaction

recommended by Hamson. Show your calculations. State whether Hamson’s conclusion

about the U.S. dollar holding period return resulting from the transaction is correct or

incorrect. After conducting his own analysis of the U.S. and Mexican economies, Davies

expects that both the U.S. inflation rate and the real exchange rate will remain constant over

the coming year. Because of favorable political developments in Mexico, however, he

expects that the Mexican inflation rate (in annual terms) will fall from 6.0 percent to 3.0

percent before the end of the year. As a result, Davies decides to invest Yucatan Resorts’

cash holdings in the Mexican one-year bond but not to hedge the currency exposure.

b. Calculate the expected exchange rate (pesos per dollar) one year from now. Show your

calculations. Note: Your calculations should assume that Davies is correct in his

expectations about the real exchange rate and the Mexican and U.S. inflation rates.

c. Calculate the expected U.S. dollar holding period return on the Mexican one-year bond.

Show your calculations. Note: Your calculations should assume that Davies is correct in his

expectations about the real exchange rate and the Mexican and U.S. inflation rates.

Solution:

a. The U.S. dollar holding period return that would result from the transaction recommended by

Hamson is 2.5%. The investor can buy “x” amount of pesos at the (indirect) spot exchange

be represented by the formula:

where “Spot” and “Forward” are in indirect terms. The left side of the equation represents

the holding period return for a U.S. dollar-denominated bond. If interest rate parity holds, the

Solving for YUS:

(1 + YUS) = 9.5000 × (1 + 0.065) × (1 / 9.8707)

Thus YUS = 2.5%, which is the same yield as on the one-year U.S. bond. Hamson’s

b. The expected exchange rate one year from now is 9.5931. The rate can be calculated by

using the formula:

where RUS is the real U.S. dollar exchange rate, Si is the nominal spot exchange rate in

period i, and %Δ P is the inflation rate. Note that the currency quotes are in indirect form.

Solving for S1 (the expected exchange rate one year from now):

c. The expected U.S. dollar holding period return on the Mexican one-year bond is 5.47%. The

return can be calculated as shown below, using the formula in Part A and the current spot

exchange rate and expected one-year spot exchange rate calculated in Part B.

11. James Clark is a foreign exchange trader with Citibank. He notices the following quotes.

Spot exchange rate SFr1.2051/$

Six-month forward exchange rate SFr1.1922/$

Six-month $ interest rate 2.5% per year

Six-month SFr interest rate 2.0% per year

a. Is the interest rate parity holding? You may ignore transaction costs.

b. Is there an arbitrage opportunity? If yes, show what steps need to be taken to make

arbitrage profit. Assuming that James Clark is authorized to work with $1,000,000, compute

the arbitrage profit in dollars.

Solution:

a. For six months, iSFr = 1.0% and i$ = 1.25%. the spot exchange rate is $0.8298/SFr and the

b. Because IRP is not holding, there is an arbitrage possibility: Because 1.0125 < 1.02095, we

can say that the SFr interest rate quote is more than what it should be as per the quotes for

Borrow $1,000,000 for six months at 1.25%. Need to pay back $1,000,000 × (1 +

0.0125) = $1,012,500 six months later.

Convert $1,000,000 to SFr at the spot rate to get SFr 1,205,100.

12. Suppose you conduct currency carry trade by borrowing $1 million at the start of each year

and investing in New Zealand dollar for one year. One-year interest rates and the exchange rate

between the U.S. dollar ($) and New Zealand dollar (NZ$) are provided below for the period

2000 – 2009. Note that interest rates are one-year interbank rates on January 1st each year, and

that the exchange rate is the amount of New Zealand dollar per U.S. dollar on December 31

each year. The exchange rate was NZ$1.9088/$ on January 1, 2000. Fill out the columns (4) –

(7) and compute the total dollar profits from this carry trade over the ten-year period. Also,

assess the validity of uncovered interest rate parity based on your solution of this problem. You

are encouraged to use Excel program to tackle this problem.

(1) (2) (3) (4) (5) (6) (7)

Year iNZ$ i$SNZ$/$ iNZ$ – i$eNZ$/$ (4)-(5) $ Profit

2000 6.53 6.50 2.2599

2001 6.70 6.00 2.4015

2002 4.91 2.44 1.9117

2003 5.94 1.45 1.5230

2004 5.88 1.46 1.3845

2005 6.67 3.10 1.4682

2006 7.28 4.84 1.4182

2007 8.03 5.33 1.2994

2008 9.10 4.22 1.7112

2009 5.10 2.00 1.3742

Data source: Datastream.

Solution:

(1) (2) (3) (4) (5) (6) (7)

Year iNZ$ i$SNZ$/$ iNZ$ – i$eNZ$/$ (4)-(5) $ Profit

2000 6.53 6.50 2.2599 0.03 18.40 -18.37 -183655

2001 6.70 6.00 2.4015 0.7 6.27 -5.57 -55680

2002 4.91 2.44 1.9117 2.47 -20.40 22.87 228676

Notes:

1. Interest rates are interbank 1-year rates on January 1st of each year and measured in percent

terms.

If uncovered interest rate parity holds, profit from carry trade should be insignificantly different

from zero. But since the profit in column (7) substantially differs from zero each year, uncovered

IRP does not appear to hold.

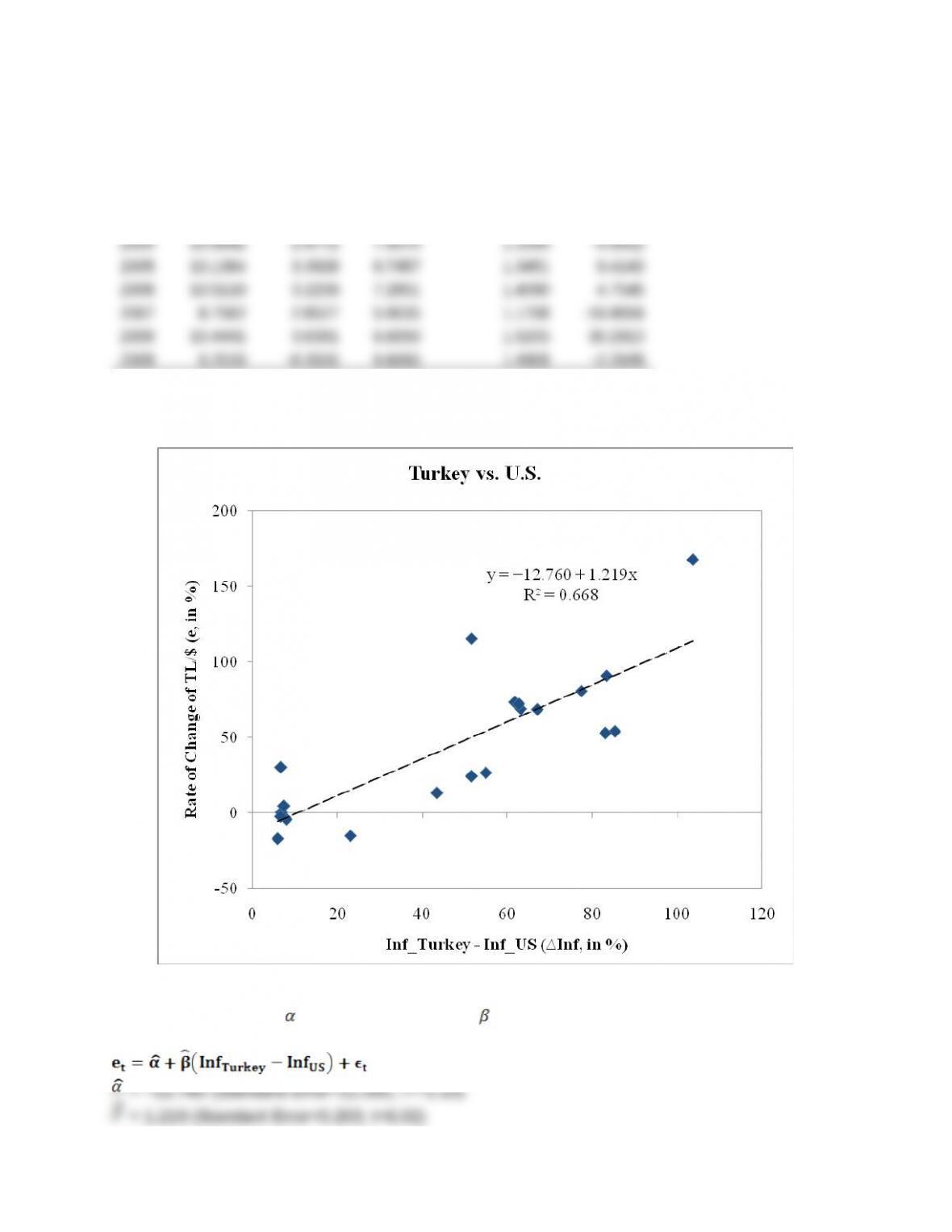

Mini Case: Turkish Lira and the Purchasing Power Parity

Veritas Emerging Market Fund specializes in investing in emerging stock markets of the world.

Mr. Henry Mobaus, an experienced hand in international investment and your boss, is currently

interested in Turkish stock markets. He thinks that Turkey will eventually be invited to negotiate

its membership in the European Union. If this happens, it will boost the stock prices in Turkey.

But, at the same time, he is quite concerned with the volatile exchange rates of the Turkish

currency. He would like to understand what drives the Turkish exchange rates. Since the

inflation rate is much higher in Turkey than in the U.S., he thinks that the purchasing power

parity may be holding at least to some extent. As a research assistant for him, you were

assigned to check this out. In other words, you have to study and prepare a report on the

following question: Does the purchasing power parity hold for the Turkish lira-U.S. dollar

exchange rate? Among other things, Mr. Mobaus would like you to do the following:

1. Plot past annual exchange rate changes against the differential inflation rates between

Turkey and the U.S. for the last 20 years.

2. Regress the annual rate of exchange rate changes on the annual inflation rate differential to

estimate the intercept and the slope coefficient, and interpret the regression results.

Data source: You may download the annual inflation rates for Turkey and the U.S., as well as

the exchange rate between the Turkish lira and US dollar from the following source:

http://data.un.org. For the exchange rate, you are advised to use the variable code 186 AE ZF.

Solution:

Data obtained from http://data.un.org

Inf_TK (%)

(1)

Inf_US (%)

(2)

∆Inf

(1)-(2)

S(TL/$)

End-of-year rate

∆St/St-1 (%)

:= et

1989 0.0023

1990 60.3127 5.3980 54.9147 0.0029 26.6406

1991 65.9694 4.2350 61.7344 0.0051 73.3720

1992 70.0728 3.0288 67.0440 0.0086 68.5938

1993 66.0971 2.9517 63.1454 0.0145 68.9838

1999 64.8675 2.1880 62.6795 0.5414 72.1660

2000 54.9154 3.3769 51.5385 0.6734 24.3785

2001 54.4002 2.8262 51.5740 1.4501 115.3493

2002 44.9641 1.5860 43.3781 1.6437 13.3485

2003 25.2964 2.2701 23.0263 1.3966 -15.0307

Solution:

1. In the current solution, we use the annual data from 1990 to 2009.

2. We regress the rate of exchange rate changes (e) on the inflation rate differential and

estimate the intercept ( ) and slope coefficient ( ):

The estimated intercept is insignificantly different from zero, whereas the slope coefficient is

positive and significantly different from zero. In fact, the slope coefficient is insignificantly