MINI CASE: DORCHESTER, LTD.

Dorchester Ltd., is an old-line confectioner specializing in high-quality chocolates. Through

its facilities in the United Kingdom, Dorchester manufactures candies that it sells throughout

Western Europe and North America (United States and Canada). With its current

manufacturing facilities, Dorchester has been unable to supply the U.S. market with more than

225,000 pounds of candy per year. This supply has allowed its sales affiliate, located in Boston,

to be able to penetrate the U.S. market no farther west than St. Louis and only as far south as

Atlanta. Dorchester believes that a separate manufacturing facility located in the United States

would allow it to supply the entire U.S. market and Canada (which presently accounts for 65,000

pounds per year). Dorchester currently estimates initial demand in the North American market

at 390,000 pounds, with growth at a 5 percent annual rate. A separate manufacturing facility

would, obviously, free up the amount currently shipped to the United States and Canada. But

Dorchester believes that this is only a short-run problem. They believe the economic

development taking place in Eastern Europe will allow it to sell there the full amount presently

shipped to North America within a period of five years.

Dorchester presently realizes £3.00 per pound on its North American exports. Once the

U.S. manufacturing facility is operating, Dorchester expects that it will be able to initially price its

product at $7.70 per pound. This price would represent an operating profit of $4.40 per pound.

Both sales price and operating costs are expected to keep track with the U.S. price level; U.S.

inflation is forecast at a rate of 3 percent for the next several years. In the U.K., long-run

inflation is expected to be in the 4 to 5 percent range, depending on which economic service

one follows. The current spot exchange rate is $1.50/£1.00. Dorchester explicitly believes in

PPP as the best means to forecast future exchange rates.

The manufacturing facility is expected to cost $7,000,000. Dorchester plans to finance this

amount by a combination of equity capital and debt. The plant will increase Dorchester’s

borrowing capacity by £2,000,000, and it plans to borrow only that amount. The local

community in which Dorchester has decided to build will provide $1,500,000 of debt financing

for a period of seven years at 7.75 percent. The principal is to be repaid in equal installments

over the life of the loan. At this point, Dorchester is uncertain whether to raise the remaining

debt it desires through a domestic bond issue or a Eurodollar bond issue. It believes it can

borrow pounds sterling at 10.75 percent per annum and dollars at 9.5 percent. Dorchester

estimates its all-equity cost of capital to be 15 percent.

The U.S. Internal Revenue Service will allow Dorchester to depreciate the new facility over a

seven-year period. After that time the confectionery equipment, which accounts for the bulk of

the investment, is expected to have substantial market value.

Dorchester does not expect to receive any special tax concessions. Further, because the

corporate tax rates in the two countries are the same–35 percent in the U.K. and in the United

States–transfer pricing strategies are ruled out.

Should Dorchester build the new manufacturing plant in the United States?

Suggested Solution to Dorchester Ltd.

Summary of Key Information

The current exchange rate in European terms is So(£/$) = 1/1.50 = .6667.

The initial cost of the project in British pounds is SoCo = £0.6667($7,000,000) =

S

The before-tax nominal contribution margin per unit at t=1 is $4.40(1.03)t-1.

It is assumed that Dorchester will be able to sell one-fifth of the 290,000 pounds of candy it

presently sells to North America in Eastern Europe the first year the new manufacturing facility

Straight line depreciation over the seven year economic life of the project is assumed: Dt =

$1,000,000 = $7,000,000/7 years.

The marginal tax rate, , is the U.K. (or U.S.) rate of 35%.

Dorchester will borrow $1,500,000 at the concessionary loan rate of 7.75% per annum.

Optimally, Dorchester should borrow the remaining funds it needs, £1,000,000, in pounds

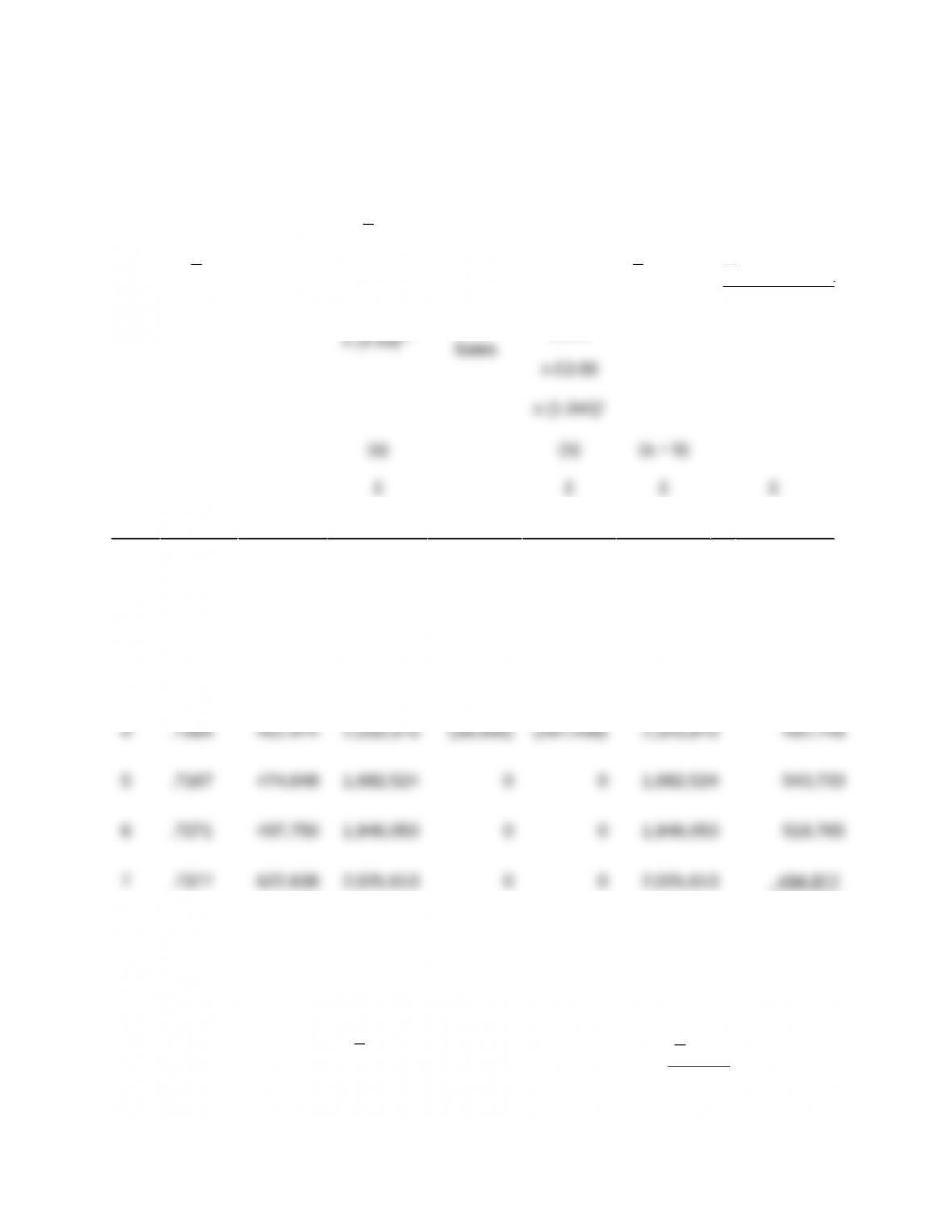

Calculation of the Present Value of the After-Tax Operating Cash Flows

Year

(t)

t

S

Quantity

t

S

x

Quantity

x $4.40

Quantity

Lost

Quantity

Lost

Sales

tt

SOCF

)

K

+(

)–(

OCF

S

t

ud

t

t

1

1

1 .6764 390,000 1,160,702 (232,000) (727,320) 433,382 244,955

2 .6863 409,500 1,273,673 (174,000) (570,037) 703,636 345,832

3 .6963 429,975 1,397,548 (116,000) (397,126) 1,000,422 427,566

3,068,576

Calculation of the Present Value of the Depreciation Tax Shields

Year

(t)

t

S

Dt

)

i

+(

D

S

t

d

t

t

1

$ £

1 .6764 1,000,000 213,761

2 .6863 1,000,000 195,837

1,168,146

Calculation of the Present Value of the Concessionary Loan Payments

Year

(t)

t

S

(a)

Principal

Payment

(b)

$

It

(c)

$

tt

SLP

(a) x (b + c)

£

tt

d

t

SLP

(1+ i)

£

1 .6764 214,286 116,250 223,574 201,873

2 .6863 214,286 99,643 215,449 175,654

3 .6963 214,286 83,036 207,025 152,402

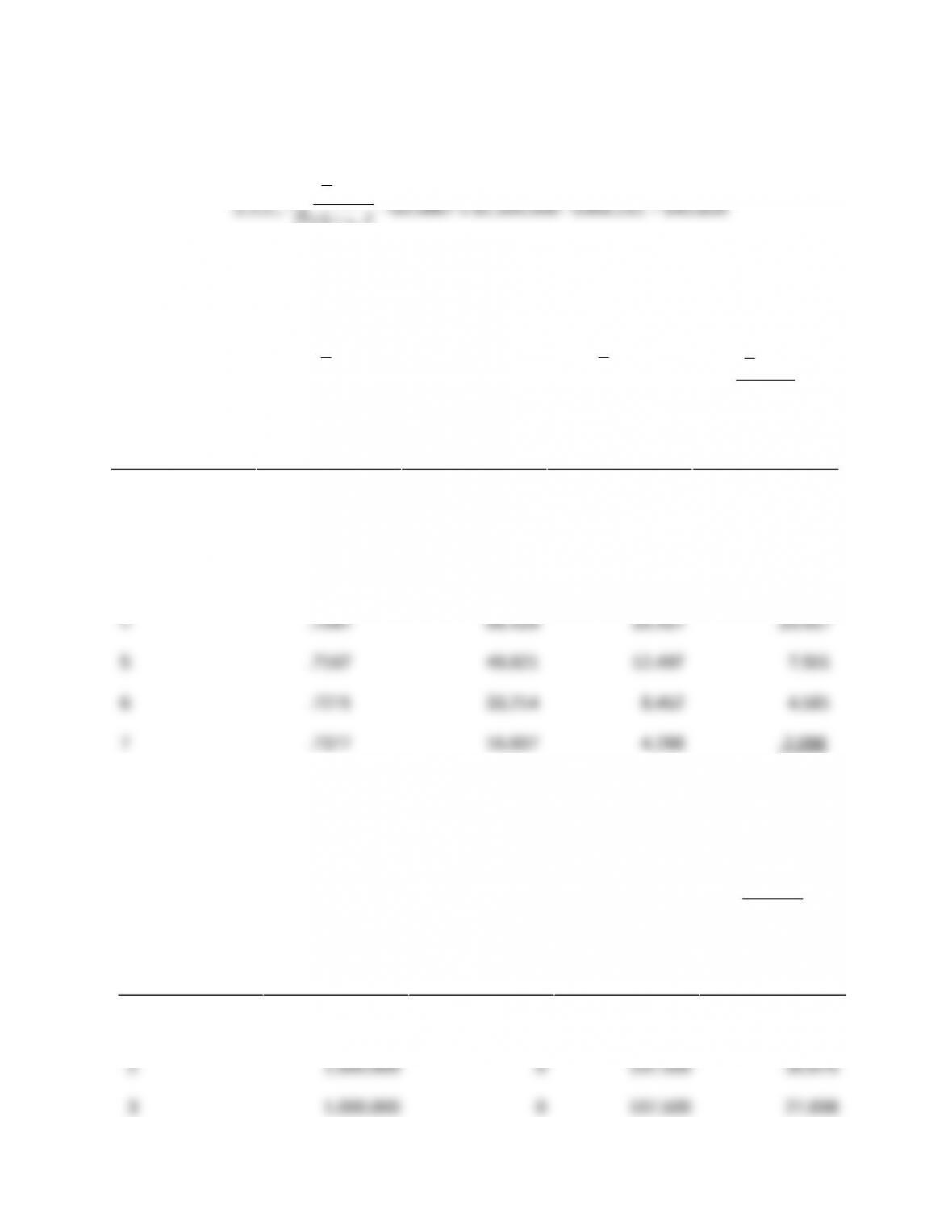

Calculation of the Present Value of the Benefit from the Concessionary Loan

)

i

+(

LP

S

–

CLS t

d

t

t

T

1=t

oo 1

=£0.6667 x $1,500,000 – £956,211 = £43,839

Calculation of the Present Value of the Interest Tax Shields

from the $1,500,000 Concessionary Loan

Year

(t)

t

S

(a)

It

(b)

$

tt

SI

(a x b x )

£

tt

d

t

SI

(1+ i)

£

1 .6764 116,250 27,521 24,850

2 .6863 99,643 23,935 19,514

3 .6963 83,036 20,236 14,897

84,357

Calculation of the Present Value of the Interest Tax Shields from the £1,000,000 Bond Issue

Year

(t)

Outstanding

Loan

Balance

Principal

Payment

Interest

Payment

)

i

+(

I

t

d

t

1

£ £ £ £

1 1,000,000 0 107,500 33,973

4 1,000,000 0 107,500 25,009

5 1,000,000 0 107,500 22,582

178,738

Dorchester should not go ahead with its plans to build a manufacturing plant in the U.S. unless

the terminal value is likely to be large enough to yield a positive APV. The terminal value of the

Since the terminal value is expected to be substantial, and the initial cost of the project is

MINI-CASE: STRIK-IT-RICH GOLD MINING COMPANY

The Strik-it-Rich Gold Mining Company is contemplating expanding its operations. To do so it

will need to purchase land that its geologists believe is rich in gold. Strik-it-Rich’s management

believes that the expansion will allow it to mine and sell an additional 2,000 troy ounces of gold

per year. The expansion, including the cost of the land, will cost $2,500,000. The current price

of gold bullion is $1,400 per ounce and one-year gold futures are trading at $1,484 =

$1,400(1.06). Extraction costs are $1,050 per ounce. The firm’s cost of capital is 10%. At the

current price of gold, the expansion appears profitable: NPV = ($1,400 – 1,050) x 2,000/.10 –

$2,500,000 = $4,500,000. Strik-it-Rich’s management is, however, concerned with the

possibility that large sales of gold reserves by Russia and the United Kingdom will drive the

price of gold down to $1,100 for the foreseeable future. On the other hand, management

believes there is some possibility that the world will soon return to a gold reserve international

monetary system. In the latter event, the price of gold would increase to at least $1,600 per

ounce. The course of the future price of gold bullion should become clear within a year. Strik-it-

Rich can postpone the expansion for a year by buying a purchase option on the land for

$250,000. What should Strik-it-Rich’s management do?

Suggested Solution to Strik-it-Rich Gold Mining Company

There is considerable risk in expanding operations at the present time, even though the NPV

based on the current price of gold is a positive $4,500,000. If the price of gold falls to $1,100

per ounce, the NPV = ($1,100 – 1,050) x 2000/.10 – $2,500,000 = -$1,500,000. On-the-other-

hand, if the price of gold increases to $1,600, the NPV is a very attractive NPV = ($1,600 –

Thus, the value of the timing option to postpone the decision one year is:

C = .7680($8,500,000)/(1.06) = $6,158,491.

Since this amount is substantially in excess of the $250,000 cost of the purchase option on the

land, Strik-it-Rich’s management should definitely take advantage of the timing option it is