Suggested Solution to Sundance Sporting Goods, Inc.

Note to Instructor: It is not necessary to assign the entire case problem. Parts a. and b.i. can

a. Below is the consolidated balance sheet for the MNC prepared according to the current rate

method prescribed by FASB 52. Note that the balance sheet balances. That is, Total Assets

Consolidated Balance Sheet for Sundance Sporting Goods, Inc. its Mexican and Canadian

Affiliates,

December 31, 2013: Pre-Exchange Rate Change (in 000 Dollars)

Sundance, Inc.

(parent)

Mexican

Affiliate

Canadian

Affiliate

Consolidated

Balance

Sheet

Assets

Cash $ 1,500 $ 430 $ 960 $ 2,890

Accounts receivable 2,100a849e1,200f4,149

Inventory 5,000 1,879 2,000 8,879

Investment in Mexican

affiliate

–b– – –

Long-term debt 9,000 2,121 1,840 12,961

Common stock 5,000 –b–c5,000

b,cThe investment in the affiliates cancels with the net worth of the affiliates in the consolidation.

eThe Mexican affiliate has sold on account A120,000 of merchandise to an Argentine import

house. This is carried on the Mexican affiliate’s books as Ps396,000 (= A120,000 x

Ps3.30/A1.00).

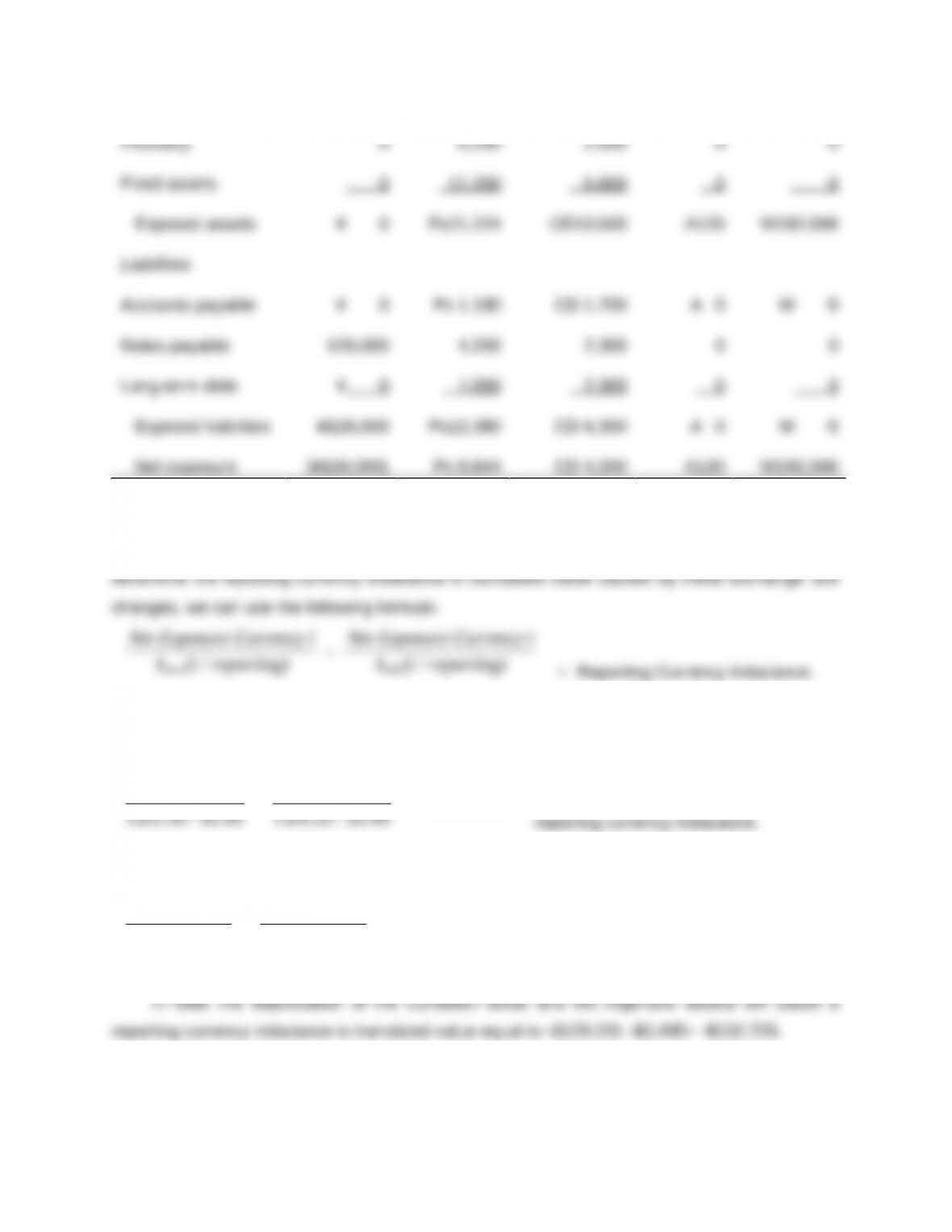

b. i. Below is presented the translation exposure report for the Sundance MNC. Note, from the

report that there is net positive exposure in the Mexican peso, Canadian dollar, Argentine

austral and Korean won. If any of these exposure currencies appreciates (depreciates) against

the U.S. dollar, exposed assets denominated in these currencies will increase (fall) in translated

Translation Exposure Report for Sundance Sporting Goods, Inc. and its Mexican and Canadian

Affiliates, December 31, 2013 (in 000 Currency Units)

Japanese

Yen

Mexican

Peso

Canadian

Dollar

Argentin

e

Austral

Korean

Won

Assets

Cash ¥ 0 Ps 1,420 CD 1,200 A 0 W 0

Accounts receivable 0 2,404 1,200 120 192,000

b. ii. The problem assumes that Canadian dollar depreciates from CD1.25/$1.00 to

CD1.30/$1.00 and that the Argentine austral depreciates from A1.00/$1.00 to A1.03/$1.00. To

From the translation exposure report we can determine that the depreciation in the

Canadian dollar will cause a

CD4,200,000

CD1.30 / $1.00 – CD4,200,000

CD1.25 / $1.00 = – $129,231

reporting currency imbalance.

Similarly, the depreciation in the Argentine austral will cause a

A120,000

A1.03 / $1.00 – A120,000

A1.00 / $1.00 = – $3,495

reporting currency imbalance.

c. The new consolidated balance sheet for Sundance MNC after the depreciation of the

Canadian dollar and the Argentine austral is presented below. Note that in order for the new

consolidated balance sheet to balance after the exchange rate change, it is necessary to have a

Consolidated Balance Sheet for Sundance Sporting Goods, Inc. its Mexican and Canadian

Affiliates,

December 31, 2013: Post-Exchange Rate Change (in 000 Dollars)

Sundance, Inc.

(parent)

Mexican

Affiliate

Canadian

Affiliate

Consolidate

d

Balance

Sheet

Assets

Cash $ 1,500 $ 430 $ 923 $ 2,853

Accounts receivable 2,100a845e1,163f4,108

Inventory 5,000 1,879 1,923 8,802

Total liabilities and net

worth

$35,465

a$2,500,000 – $400,000 (= Ps1,320,000/(Ps3.30/$1.00)) intracompany loan = $2,100,000.

b,cThe investment in the affiliates cancels with the net worth of the affiliates in the consolidation.

dThe parent owes a Japanese bank ¥126,000,000. This is carried on the books as $1,200,000

(=¥126,000,000/(¥105/$1.00)).

eThe Mexican affiliate has sold on account A120,000 of merchandise to an Argentine import

d. i. The transaction exposure report for Sundance, Inc. and its two affiliates is presented below.

The report indicates that the Ps1,320,000 accounts receivable due from the Mexican affiliate is

not also a translation exposure because this is netted out in the consolidation. However, the

Transaction Exposure Report for Sundance Sporting Goods, Inc. and

its Mexican and Canadian Affiliates, December 31, 2013

Affiliate Amount Account

Translation

Exposure

Parent Ps1,320,000 Accounts

Receivable

No

d. ii. Since transaction exposure may potentially result in real cash flow losses while translation

exposure does not have an immediate direct effect on operating cash flows, we will first address

The parent firm can pay off the ¥126,000,000 loan from the Japanese bank using funds

from the cash account and money from accounts receivable that it will collect. Additionally, the

parent firm can collect the accounts receivable of Ps1,320,000 from its Mexican affiliate that is

carried on the books as $400,000. In turn, the Mexican affiliate can collect the A120,000

The elimination of these transaction exposures will affect the translation exposure of

Sundance MNC. A revised translation exposure report follows.

Revised Translation Exposure Report for Sundance Sporting Goods, Inc. and its Mexican and

Canadian Affiliates, December 31, 2013 (in 000 Currency Units)

Japanese

Yen

Mexican

Peso

Canadian

Dollar

Argentine

Austral

Korean

Won

Assets

Cash ¥ 0 Ps 484 CD 1,512 A 0 W 0

Accounts

0 2,404 1,200 0 0

Long-term debt 0 7,000 2,300 0 0

Exposed

liabilities

¥ 0 Ps12,380 CD6,300 A 0 W 0

Net exposure ¥ 0 Ps 7,908 CD4,512 A 0 W 0

Note from the revised translation exposure report that the elimination of the transaction

exposure will also eliminate the translation exposure in the Japanese yen, Argentine austral and

The remaining translation exposure can be hedged using a balance sheet hedge or a

derivatives hedge. Use of a balance sheet hedge is likely to create new transaction exposure,