CHAPTER 8

Valuation Using the Income Approach

Test Problems

1. Which of the following expenses is not an operating expense?

d. Mortgage payment.

2. An overall capitalization rate (Ro) is divided into which type of income or cash flow

to obtain an indicated market value?

a. Net operating income (NOI).

3. Which of the following types of properties probably would not be appropriate for

income capitalization?

e. Public school.

4. Estimated capital expenditures

d. are subtracted to compute NOI in a below-line treatment.

5. An appraiser estimates that a property will produce NOI of $25,000 in perpetuity, yo

is 11 percent, and the constant annual growth rate in NOI is 2.0 percent. What is the

estimated property value?

a. $277,778.

6. If a comparable property sells for $1,200,000 and the effective gross income of the

property is $12,000 per month, the effective gross income multiplier (EGIM) is

b. 8.33

7. Which of the following statements regarding capitalization rates on commercial real

estate investments is the most correct?

b. Cap rates vary positively with the perceived risk of the investment.

8. The methodology of appraisal differs from that of investment analysis primarily

regarding

e. Point of view.

Use the following information to answer questions 9-10.

You have just completed the appraisal of an office building and have concluded that the

market value of the property is $2,500,000. You expect Potential Gross Income (PGI) in the

first year of operations to be $450,000; vacancy and collection losses to be 9 percent of PGI;

operating expenses to be 38 percent of Effective Gross Income (EGI), and capital

expenditures to be 4 percent of EGI.

9. What is the implied going-in capitalization rate?

10. What is the effective gross income multiplier (EGIM)?

Study Questions

1. Data for five comparable income properties that sold recently are shown below:

Property NOI Sale Price Overall Rate

A $ 57,800 $ 566,600 0.1020

B 49,200 496,900 0.0990

C 63,000 630,000 0.1000

D 56,000 538,500 0.1040

E 58,500 600,000 0.0975

What is the indicated overall rate (RO)?

Solution: The indicated overall cap rate of 10.05 percent is the simple average of the

2. Why is the market value of real estate determined partly by the lender’s requirements

and partly by the requirements of equity investors?

Solution: Real estate investments are frequently financed using a combination of

equity and mortgage debt. A real estate investment can be viewed as a joint

investment made by both the lender and equity investor, and therefore, both parties’

3. Assume a reserve for non-recurring capital expenditures is to be included in the pro

forma for the subject property. Explain how an above-line treatment of this

expenditure would differ from a below-line treatment.

Solution: In an above-line treatment, the reserve for non-recurring capital

expenditures would be taken out in the calculation of net operating income (i.e.,

4. Use the following property data:

Cash flow from operations:

Year 1 2 3 4 5

NOI $150,000 $150,000 $150,000 $150,000 $150,000

Debt Service $125,000 $125,000 $125,000 $125,000 $125,000

Cash Flow at sale:

Sale Price: $2,000,000

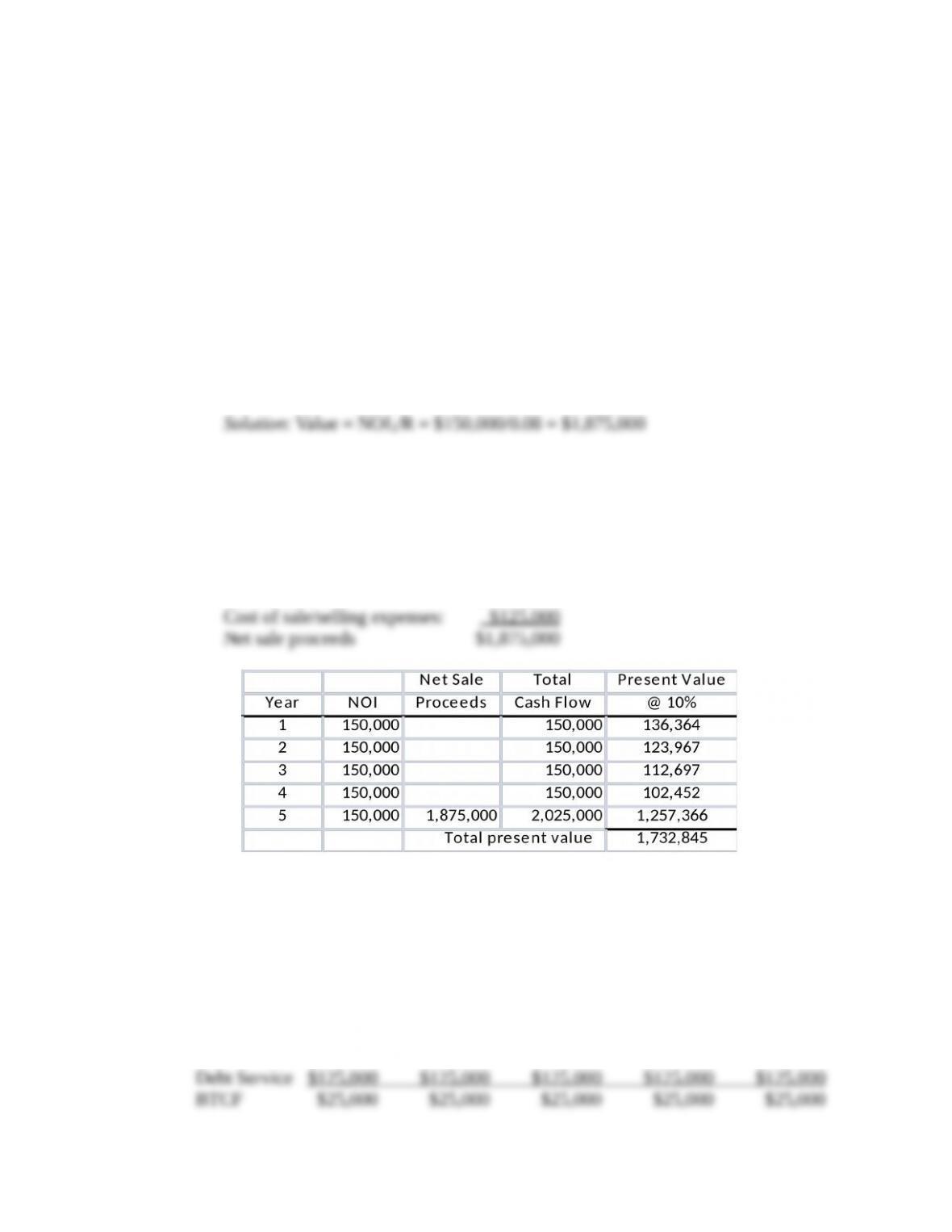

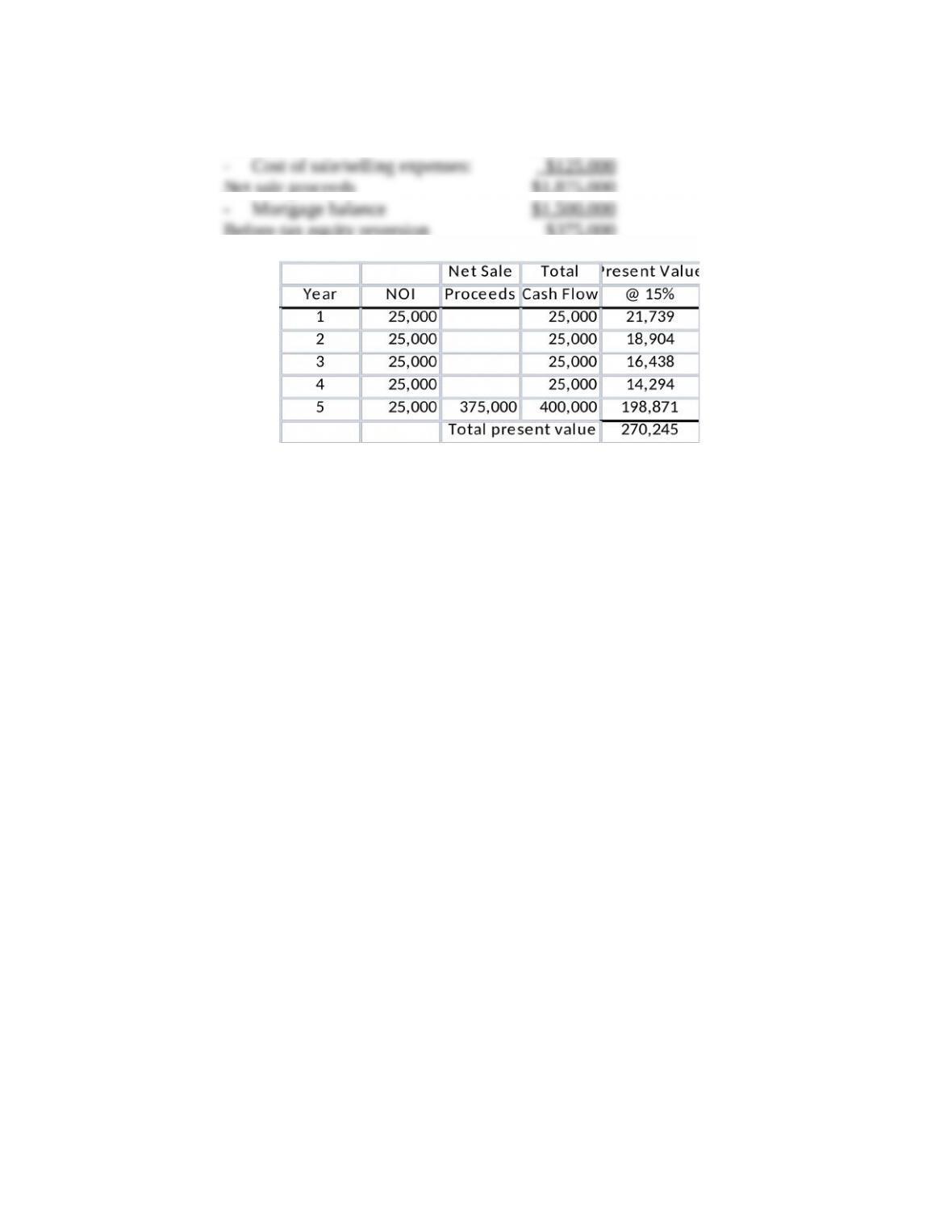

Cost of sale: $125,000

Mortgage balance: $1,500,000

a. Assuming the going-in capitalization rate is 8.00 percent, compute a value for the

property using direct capitalization.

b. Assuming the required yield/return on unlevered cash flows is 10 percent, and

that the property will be held by a buyer for five years, compute the value of the

property based on discounting unlevered cash flows.

Solution:

Sale Price: $2,000,000

c. Assuming the relevant required yield/return on levered cash flows is 15 percent,

and that the property will be held by a buyer for five years, what is the present

value of the levered cash flows?

Solution:

Year 1 2 3 4 5

NOI $150,000 $150,000 $150,000 $150,000 $150,000

Sale Price: $2,000,000

Net sale proceeds $1,875,000

Before-tax equity reversion $375,000

5. Given the following owner’s income and expense estimates for an apartment

property, formulate a reconstructed operating statement. The building consists of 10

units that could rent for $550 per month each.

Owner’s Annual Income Statement

Rental income (last year) $60,600

Less: Operating & capital expenses

Power $2,200

Heat 1,700

Janitor 4,600

Water 3,700

Maintenance 4,800

Reserve for capital expenditures 2,800

Management 3,000

Tax depreciation 5,000

Mortgage payments 6,300

Estimating vacancy and collection losses at 5 percent of potential gross income,

reconstruct the operating statement to obtain an estimate of NOI. Assume an

above-line treatment of CAPX. Remember, there may be items in the owner’s

statement that should not be included in the reconstructed operating statement. Using

the NOI and a Ro of 11.0 percent, calculate the property’s indicated market value.

Round your answer to the nearest $1,000.

Solution:

Reconstructed Operating Statement

PGI: (10 units x $550 x 12) $66,000

Less: Vacancy Loss (at 5 percent) (3,300)

EGI: 62,700

Less: Operating Expenses

Power $2,200

Heat 1,700

Note: Mortgage payments and depreciation are not included in the calculation of the

property’s NOI.

The indicated value of the property is $362,727 ($39,900 / 0.11), which rounds to

$363,000.

6. You have been asked to estimate the market value of an apartment complex that is

producing annual net operating income of $44,500. Four highly similar and

competitive apartment properties within two blocks of the subject property have sold

in the past three months. All four offer essentially the same amenities and services as

the subject. All were open-market transactions with similar terms of sale. All were

financed with 30-year fixed-rate mortgages using 70 percent debt and 30 percent

equity. The sale prices and estimated first-year net operating incomes were as

follows:

Comparable 1: Sale price $500,000; NOI $55,000

Comparable 2: Sale price $420,000; NOI $50,400

Comparable 3: Sale price $475,000; NOI $53,400

Comparable 4: Sale price $600,000; NOI $69,000

What is the indicated value of the subject property using direct capitalization?

Solution:

The abstracted going-in capitalization rates from the four properties are listed below:

Comparable 1: 0.110

Comparable 2: 0.120

The simple average of the four comparable cap rates is 0.114. Thus, the indicated

7. You are estimating the value of a small office building. Suppose the estimated NOI

for the first year of operations is $100,000.

a. If you expect that NOI will remain constant at $100,000 over the next 50 years and

that the office building will have no value at the end of 50 years, what is the present

value of the building assuming a 12.2% discount rate? If you pay this amount, what

is the indicated initial cap rate?

Solution: The present value, using a financial calculator, is $817,078.

The initial (going-in) cap rate is $100,000/$817,078 = 12.24%

b. If you expect that NOI will remain constant at $100,000 forever, what is the value

of the building assuming a 12.2% discount rate? If you pay this amount, what is the

indicated initial cap rate?

Solution: The value of the building with NOI remaining constant at $100,000 is

calculated using the formula for a perpetuity, which is $100,000/0.122, or $819,672.

c. If you expect the initial $100,000 NOI will grow forever at a 3% annual rate, what

is the value of the building assuming a 12.2% discount rate? If you pay this amount,

what is the indicated initial cap rate?

Solution: The capitalization rate consists of a required IRR on equity and a growth

rate. Applying the general constant-growth formula and assuming that the growth

8. Describe the conditions under which the use of effective gross income multipliers to

value the subject property is appropriate.

Solution: The use of gross income multipliers is predicated on two primary

assumptions. First, it is assumed that the operating expense percentage of the subject

9. In what situations or for which types of properties might discounted cash flow

analysis be preferred to direct capitalization?

Solution: Direct capitalization is dependent on information obtained from sales of

properties that are deemed to be comparable to the subject property. Identifying

comparable properties is particularly difficult with commercial real estate

10. What is the difference between a fee simple estate and a leased fee estate?

Solution: A fee simple estate is the highest form of property ownership. It is complete

ownership of a property without regard to leases. A leased fee estate is ownership of a

11. What is the difference between contract rent and market rent? Why is this distinction

more important for investors purchasing existing office buildings than for investors

purchasing existing apartment complexes?

Solution: Contract rent refers to the actual rent paid under existing lease contracts

executed between owners and tenants. Market rent refers to the potential rental

income a property could receive on the open market as of the effective date of an

12. Estimate the market value of the following small office building. The property has

10,500 square feet of leasable space that was leased to a single tenant on January 1,

four years ago. Terms of the lease call for rent payments of $9,525 per month for the

first five years, and rent payments of $11,325 per month for the next five years. The

tenant must pay all operating expenses.

During the remaining term of the lease, there will be no vacancy and collection

losses; however, upon termination of the lease it is expected that the property will be

vacant for three months. When the property is released under short-term leases, with

tenants paying all operating expenses, a vacancy and collection loss allowance of 8

percent per year is anticipated.

The current market rental for properties of this type under triple net leases is $11 per

square foot, and this rate has been increasing at a rate of 3 percent per year. The

market discount rate for similar properties is about 11 percent, the “going-in” cap rate

is about 9 percent, and terminal cap rates are typically 1 percentage point above

going-in cap rates.

Prepare a spreadsheet showing the rental income, expense reimbursements, NOIs, and

the net proceeds from the sale of the property at the end of an 8-year holding period.

Then use the information provided to estimate the market value of the property.

Solution: The fifth year of the 10-year lease is the first year of analysis. The problem

calls for an 8-year analysis–one for the last year of the 1st 5-year period, five for the

second 5-year period, one to allow the vacancy and collection loss to achieve a

Yr. 1 Yr. 2 Yr. 3 Yr. 4 Yr. 5 Yr. 6 Yr. 7 Yr. 8 Yr. 9

Contract Rent 114,300 135,900 135,90

0

135,90

0

135,900 135,90

0

Market Rent 115,500 118,965 122,534 126,21

0

129,996 133,89

6

137,913 142,05

0

146,311

0

0

0

6

Sale price at the end of Yr. 8: = [NOI (yr9) / Terminal cap rate]

Cash Flows: CF1 = 114,300

CF2 = 135,900

CF3 = 135,900

PV of Cash Flows @ 11 percent = $1,246,090