CHAPTER 20

Income Taxation and Value

Test Problems

1. Taxable income from the rental of actively managed depreciable real estate is

classified as:

2. Under current federal income tax law, what is the shortest cost recovery period

available to investors purchasing commercial rental property?

3. If an investor is a “dealer” with respect to certain real estate, that real estate is

classified (by the IRS) as being held:

4. When a property is sold for less than its adjusted basis, its depreciation (wear and

tear) was:

5. For tax purposes, a substantial real property improvement (CAPX) made after the

initial purchase is:

6. What percent of the income from residential rental property must be derived from

the leasing of units occupied by tenants as housing in order for the entire

depreciable basis to be depreciated using a 27 ½ year cost recovery period?

7. In 2012 you purchased a small office building for $450,000, which you financed

with a $337,500 fixed-rate, 25 year mortgage. Up-front financing costs totaled

$6,750. How much of this upfront financing expense could be written off against

ordinary income in 2012?

8. If the investor is in the 33% income tax bracket, how much will a tax credit of

$2,000 save the investor in taxes?

9. Which of the following best describes the taxation of gain and losses from the sale

of Section 1231 assets?

10. Which of the following statements is false?

d. Net passive activity losses can be used to offset dividend income from a real

Study Questions

1. Why do investors generally care whether the IRS classifies cash expenditures as

operating expenses rather than capital expenditures?

Solution: Operating expenses are generally deductible for income tax purposes in

the year they are paid. Capital expenditures are added to the tax basis of a

2. How are the discount points associated with financing an income property

handled for tax purposes?

Solution: All up-front financing costs are amortized over the life of the loan used

to finance the purchase. If the loan is prepaid before the end the loan term, the

3. What will be the taxes due on sale? Assume 6% selling costs, 33% percent

ordinary income tax rate, a 15 percent capital gains tax rate, and a 25 percent

recapture rate.

Solution:

Annual depreciation deduction = $750,000 x (1/27.5) = $27,272.73

Sale Price $1,270,000

Net Sale Proceeds 1,193,800

Taxable Gain 330,164

Capital Gain 193,800

Taxes Due on Sale $63,161

4. What will be the after-tax equity reversion (cash flow) from the sale?

Solution:

Net Sale Proceeds $1,193,800

Before-Tax Equity Reversion 555,665

After-Tax Equity Reversion $492,504

*(N=25*12, I=7/12, PV=-700,000, and FV=0) results in a monthly payment of

$4,947.45 and a yearly payment of $59,369 ($4,947.45 x 12). The remaining loan

5. Over the entire five-year holding period, how much were your taxes from rental

operations reduced by the annual depreciation deductions? Ignore the increased

taxes due on sale.

Solution: The amount of taxes saved from the annual tax depreciation is the total

6. What are the four classifications of real estate holdings for tax purposes? Which

classifications of property can be depreciated for tax purposes?

Solution: The four classes of real estate holdings for tax purposes are (1) real

estate held as a personal residence; (2) real estate held for sale to others, or dealer

7. What is your annual depreciation deduction? Ignore the mid-month convention.

Solution: The annual depreciation deduction is $36,364.64 (adjusted basis of

8. If you never sold the property, what would be the present value of the annual tax

savings from depreciation?

Solution: The present value of the annual tax savings from depreciation is

9. If you sold the property at the end of five years, what would be the present value

of the depreciation deductions, net of all taxes due on sale?

Solution:

After-tax value of annual depreciation deduction = $36,364.64 x 0.28 = $10,182

Total depreciation over 5 years = 5 x $36,364.64 = $181,823

Depreciation recapture tax at end of year 5 = $181,823 x 0.25 = $45,456

The NPV of the depreciation deductions over 5-year holding period is $9,339

10. Black Acres Apartment, Inc needs to compute taxable income (TI) for the

preceding year and wants your assistance. The effective gross income (EGI) was

$52,000; operating expenses were $19,000; $2,000 was put into a fund for future

replacement of stoves and refrigerators; debt service was $26,662, of which

$25,126 was interest; and the deprecation deduction was $17,000. Compute the

taxable income from operations:

Solution:

Effective Gross Income $52,000

Less: Operating Expenses (19,000)

Net Operating Income 31,000

Add: CAPX 2,000

Taxable Income (Loss) $(9,126)

11. You are considering the purchase of a small apartment complex.

a. Calculate the mortgage payment, the interest deduction, the depreciation

deduction, and the amortized financing costs for the first year of

operations.

b. What will be your net equity investment at “time zero”?

c. Estimate the after-tax cash flow from the first year of operations.

Solution:

a. Annual mortgage payment: $65,575 (N=25, I=8, PV=-700,000, and FV=0)

Interest Deduction in year 1 = 0.08 x $700,000 = $56,000

b. The net equity investment at time zero is $325,000 (Down payment of

c. The after-tax cash flow is calculated below:

Tax Calculations

Gross Potential Income $175,000

Effective Gross Income 154,000

Less: Operating Expenses (36,000)

Net Operating Income 116,000

Add: Capital Expenditures 2,000

Taxable Income 33,727

x 35%

Cash Calculations

Net Operating Income 116,000

Before Tax Cash Flow 50,425

After-tax Cash flow 38,620

12. Compute the after-tax cash flow from the sale of the following nonresidential

property.

a. Compute the annual depreciation expense.

b. Compute the adjusted basis at the time of sale (after two years).

c. Compute the tax liability from sale.

d. Compute the after-tax cash flow (equity reversion) from sale.

Solution:

a. Annual depreciation expense: $9,807.69 (Depreciable Basis =

0.85 x

b. Total depreciation over 2-year holding period = 2 x $9,807.69 = $19,615

Adjusted basis at the time of sale: $460,385 ($450,000 acquisition price,

c. Computation of Tax Liability:

The book says the market value of the property increased to $472,500 over

the two year holding period and that selling costs at that time will be 6

Selling Price $510,000

Net Sale Proceeds 494,700

Taxable Gain 34,315

Capital Gain 14,700

Capital Gain Tax @ 15% 2,205

Total Taxes $7,109

d. After-tax cash flow:

Net Sale Proceeds $494,700

Before-Tax Equity Reversion 140,424

After-tax Equity Reversion $133,315

13. A real estate investor is considering the purchase of a small office building. The

following assumptions are made:

Answer the following questions for the first year of operations:

e. What is the equity (cash) down payment required at “time zero”?

f. What is the annual tax depreciation deduction?

g. What is the total debt service in year 1?

h. What is the estimated net operating income?

Solution:

a. The equity (cash) down payment required at “time zero” is $193,750 (0.25

b. The annual tax depreciation deduction is $14,904 (Depreciable basis of

c. The amount of the debt service is 4,682.51 per month, or 56,190 per year.

d. The estimated net operating income is $148,950.

Less: Vacancy and Collection Losses (51,000)

Effective Gross Income 289,000

Net Operating Income $148,950

14. Compute the after-tax cash flows and after-tax equity reversion for the holding

period.

Solution:

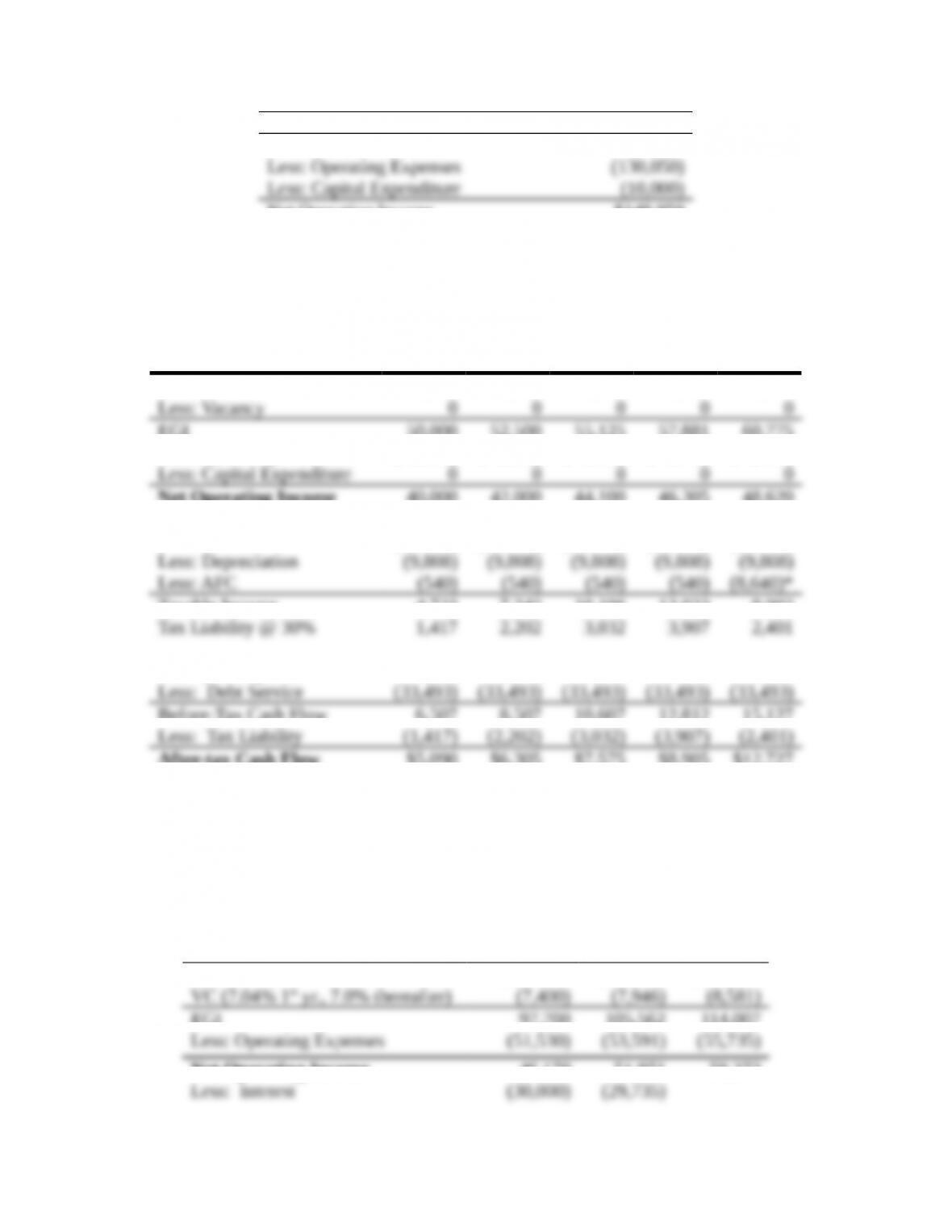

Year 1 Year 2 Year 3 Year 4 Year 5

PGI $50,000 $52,500 $55,125 $57,881 $60,775

EGI 50,000 52,500 55,125 57,881 60,775

Less: Operating Expenses (10,000) (10,500) (11,025) (11,576) (12,155)

Net Operating Income 40,000 42,000 44,100 46,305 48,620

Add: Capital Expenditures 0 0 0 0 0

Less: Interest (24,929) (24,310) (23,646) (22,934) (22,171)

Taxable Income 4,723 7,342 10,106 13,023 8,002

Net Operating Income 40,000 42,000 44,100 46,305 48,620

Before-Tax Cash Flow 6,507 8,507 10,607 12,812 15,127

After-tax Cash Flow $5,090 $6,305 $7,575 $8,905 $12,727

* includes amortization of remaining up-front financing costs

15. Assuming a two-year holding period, should the investor make this investment

given a required levered, after-tax, rate of return of 14 percent?

Solution: The after- tax cash flows are calculated below:

Year 1 Year 2 Year 3

PGI $105,100 $113,508 $122,589

EGI 97,700 105,562 114,007

Net Operating Income 46,170 51,971 58,273

Less: Depreciation (10,897) (10,897)

Taxable Income 5,272 11,339

Net Operating Income 46,170 51,971

Before-Tax Cash Flow 12,903 18,661

After-Tax Cash Flow $11,383 $15,486

Selling Price ( 58,273/0.10 Cap Rate) $582,730

Net Sale Proceeds 541,939

Taxable Gain 63,734

Capital Gain 41,939

Taxes Due on Sale $11,740

Before-Tax Equity Reversion 173,824

After-tax Equity Reversion $162,085

The cash flow stream is as follows:

Year

After-Tax

Cash Flows

After-Tax Equity

Reversion

Total Cash

Flow

0 (125,000) (125,000)

These cash flows are discounted at the levered, after-tax, required rate of