CHAPTER 19

Investment Decisions: NPV and IRR

Test Questions

1. A real estate investment is available at an initial cash outlay of $10,000, and is

expected to yield cash flows of $3,343.81 per year for five years. The internal

rate of return (IRR) is approximately:

2. The net present value of an acquisition is equal to:

3. Present value:

d. Will always equal a project’s purchase price when the discount rate is the

4. The internal rate of return equation incorporates:

5. The purchase price that will yield an investor the lowest acceptable rate of return

is:

6. What term best describes the maximum price a buyer is willing to pay for a

property?

7. An income-producing property is priced at $600,000 and is expected to generate

the following after-tax cash flows: Year 1: $42,000; Year 2: $44,000; Year 3:

$45,000; Year 4: $50,000; and Year 5: $650,000. Would an investor with a

required after-tax rate of return of 15 percent be wise to invest at the current

price?

8. As a general rule, using financial leverage:

9. What is the IRR, assuming an industrial building can be purchased for $250,000

and is expected to yield cash flows of $18,000 for each of the next five years and

be sold at the end of the fifth year for $280,000?

10. Which of the following is the least true?

d. After-tax discount rates are greater than discount rates used to value before-tax

Study Questions

1. List three important ways in which DCF valuation models differ from direct

capitalization models.

Solution: Direct capitalization models require an estimate of stabilized income for

one year. DCF models require estimates of net cash flows over the entire

2. Why might a commercial real estate investor borrow to help finance an

investment even if she could afford to pay 100 percent cash?

Solution: Borrowing–i.e., the use of “other people’s money”—is also refereed to

as the use of financial leverage. If the overall return on the property exceeds the

cost of debt, the use of leverage can significantly increase the rate of return

3. Using the “CFj” key of your financial calculator determine the IRR of the

following series of annual cash flows: CF0= -$31,400; CF1 = $3,292; CF2 =

$3,567; CF3 = $3,850; CF4 = $4,141; and CF5 = $50,659.

4. A retail shopping center is purchased for $2.1 million. During the next four years,

the property appreciates at 4 percent per year. At the time of purchase, the

property is financed with a 75 percent loan-to-value ratio for 30 years at 8 percent

(annual) with monthly amortization. At the end of year 4, the property is sold

with 8 percent selling expenses. What is the before-tax equity reversion?

Solution:

Item Amount

Loan amount = 0.75 x (2,100,000) $1,575,000

Monthly payments 11,556.79

Selling price [2,100,000 x (1.04)4] 2,456,703

Net selling price 2,260,167

Before-tax equity reversion $ 744,717

N = 360 I = 8/12 PV = 1,575,000 PMT = ? FV =0

N = 312 (360-48) I = 8/12 PV = ? PMT = 11,556.79 FV =0

5. State, in no more than one sentence, the condition for favorable financial leverage

in the calculation of NPV.

Solution: Increasing the use of leverage will increase the calculated NPV if the

6. State, in no more than one sentence, the condition for favorable financial leverage

in the calculation of the IRR.

Solution: Increasing the use of leverage will increase the calculated IRR if the

7. An office building is purchased with the following projected cash flows:

• NOI is expected to be $130,000 in year 1 with 5 percent annual increases.

• The purchase price of the property is $720,000.

• 100% equity financing is used to purchase the property

• The property is sold at the end of year 4 for $860,000 with selling costs of

4 percent.

• The required unlevered rate of return is 14 percent.

a. Calculate the unlevered internal rate of return (IRR).

b. Calculate the unlevered net present value (NPV).

Solution:

Year

Purchase

Price

Net

Operating

Income

Net Sale

Proceeds

Total Cash

Flow

Present

Value at

14%

0 ($720,000) ($720,000) ($720,000)

1 130,000 130,000 114,035

2 136,500 136,500 105,032

8. With a purchase price of $350,000, a small warehouse provides for an initial

before-tax cash flow of $30,000, which grows by 6 percent per year. If the

before-tax equity reversion after four years equals $90,000, and an initial equity

investment of $175,000 is required, what is the IRR on the project? If the

required going-in levered rate of return on the project is 10 percent, should the

warehouse be purchased?

Solution:

Year

Purchase

Price

Before-Ta

x Cash

Flow

Before-Tax

Equity

Reversion

Total Cash

Flow

Present

Value at

10%

0 ($175,000) ($175,000) ($175,000)

1 30,000 30,000 27,272

The IRR is 7.84 percent. Based on a going-in levered rate of return on the project

9. You are considering the acquisition of a small office building. The purchase price

is $775,000. Seventy-five percent of the purchase price can be borrowed with a

30-year, 7.5 percent mortgage. Payments will be made annually. Up-front

financing costs will total three percent of the loan amount. The expected

before-tax cash flows from operations–assuming a 5-year holding period—are as

follows:

Year BTCF

1 $48,492

2 53,768

3 59,282

4 65,043

5 $71,058

The before-tax cash flow from the sale of the property is expected to be $295,050.

What is the net present value of this investment, assuming a 12 percent required

rate of return on levered cash flows? What is the levered internal rate of return?

Year

Equity

Investment BTCF BTER

Total Cash

Flow

Present Value

at 12%

0 ($211,188) ($211,188) ($211,188)

1 $48,492 48,492 43,296

2 53,768 53,768 42,864

10. You are considering the purchase of an apartment complex. The following

assumptions are made:

• The purchase price is $1,000,000.

• Potential gross income (PGI) for the first year of operations is projected to

be $171,000.

• PGI is expected to increase at 4 percent per year.

• No vacancies are expected.

• Operating expenses are estimated at 35 percent of effective gross income.

Ignore capital expenditures.

• The market value of the investment is expected to increase 4 percent per

year.

• Selling expenses will be 4 percent.

• The holding period is 4 years.

• The appropriate unlevered rate of return to discount projected NOIs and

the projected NSP is 12 percent.

• The required levered rate of return is 14 percent.

• 70 percent of the acquisition price can be borrowed with a 30-year,

monthly payment mortgage.

• The annual interest rate on the mortgage will be 8.0 percent.

• Financing costs will equal 2 percent of the loan amount.

• There are no prepayment penalties.

a. Calculate net operating income (NOI) for each of the four years.

Solution:

Item 1 2 3 4

PGI $171,000 $177,840 $184,954 $192,352

EGI 171,000 177,840 184,954 192,352

NOI $111,150 $115,596 $120,220 $125,029

b. Calculate the net sale proceeds from the sale of the property.

Solution:

Item Amount

Selling price [1,000,000 x (1.04)4] $1,169,859

c. Calculate the net present value of this investment, assuming no mortgage

debt. Should you purchase? Why?

Solution:

Item Cash Flow Present Value at 12%

Initial Outflow Yr. 0 -$1,000,000 -$1,000,000

NOI Yr.1 111,150 99,241

NOI Yr.2 115,596 92,152

d. Calculate the internal rate of return of this investment, assuming no debt.

Should you purchase? Why?

Solution: IRR = 14.22 percent. Purchase because unlevered required rate

e. Calculate the monthly mortgage payment. What is the total per year?

Solution: Monthly payment = $5,136.35 as calculated below:

f. Calculate the loan balance at the end of years 1, 2, 3, and 4. (Note: the

unpaid mortgage balance at any time is equal to the present value of the

remaining payments, discounted at the contract rate of interest.)

Solution:

Unpaid mortgage balance in year 1 = $694,152

Unpaid mortgage balance in year 2 = $687,820

g. Calculate the amount of principal reduction achieved during each of the

four years.

Solution:

Principal reduction in year 1 = $700,000 – $694,152 = $5,848

Principal reduction in year 2 = $694,152 – $687,820 = $6,332

h. Calculate the total interest paid during each of the four years. (Note:

Remember that debt service equals principal plus interest.)

Solution:

Interest paid in year 1 = $61,636 – $5,848 = $55,788

Interest paid in year 2 = $61,636 – $6,332 = $55,304

i. Calculate the levered required initial equity investment.

Solution:

Loan amount (0.70 x $1,000,000) = $700,000

j. Calculate the before-tax cash flow (BTCF) for each of the four years.

Solution:

Item 1 2 3 4

NOI $111,150 $115,596 $120,220 $125,029

k. Calculate the before-tax equity reversion (BTER) from the sale of the

property.

Solution:

Item Amount

Net selling price $1,123,065

l. Calculate the levered net present value of this investment. Should you

purchase? Why?

Solution:

Item Cash Flow

Present

Value at

14%

BTCF Yr.1 $49,514 $43,433

BTCF Yr.2 53,960 41,520

BTCF Yr.3 58,584 39,543

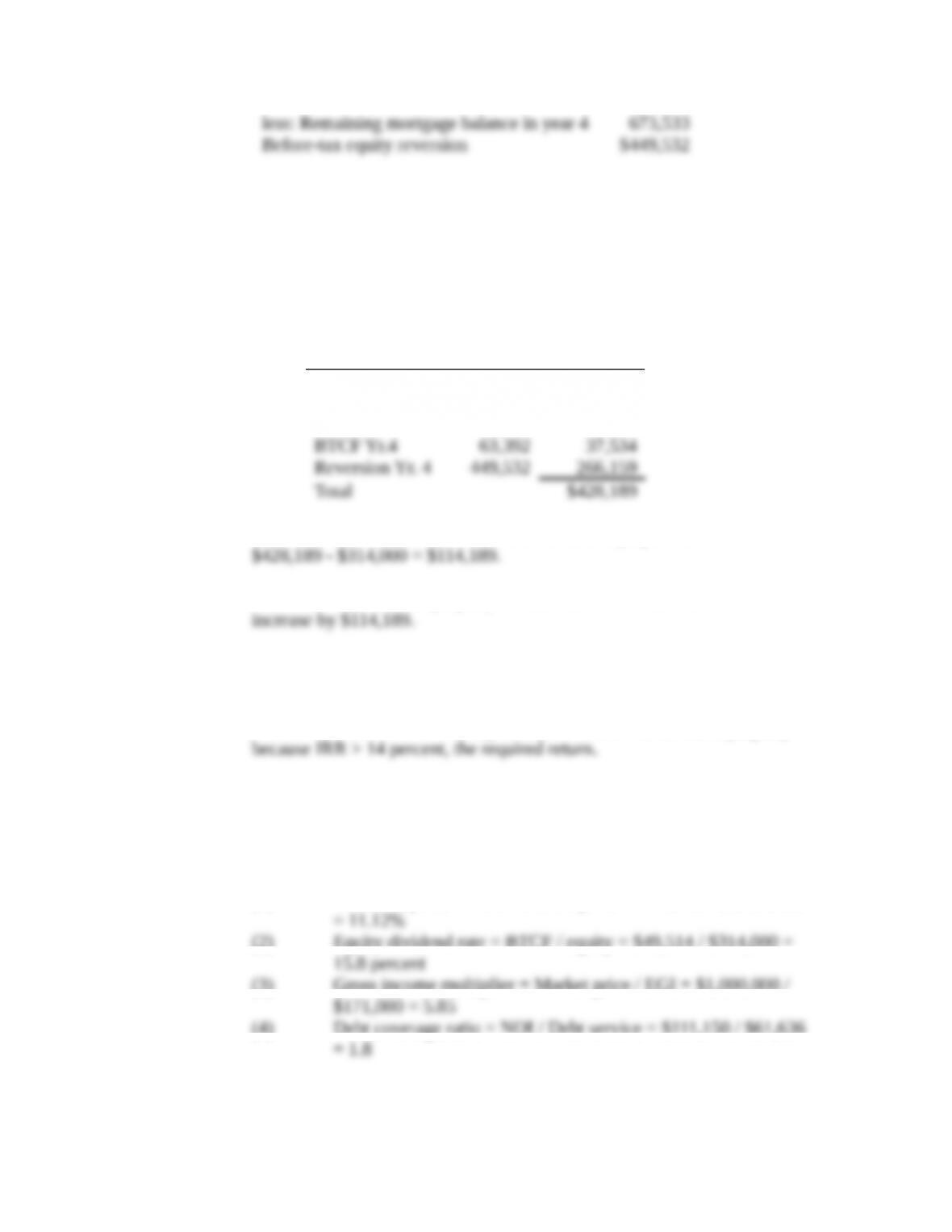

NPV = Present value of the cash flows less the equity investment:

Decision: Purchase the property because the NPV > 0; wealth will

m. Calculate the levered internal rate of return of this investment (assuming

no debt and no taxes). Should you purchase? Why?

Solution: Levered IRR = 25.02 percent; Decision: Purchase the property

n. Calculate, for the first year of operations, the: (1) overall (cap) rate of

return, (2) equity dividend rate, (3) gross income multiplier, (4) debt

coverage ratio.

Solution:

(1) Overall cap rate = NOI / Market price = $111,150 / $1,000,000

(2) Equity dividend rate = BTCF / equity = $49,514 / $314,000 =

(3) Gross income multiplier = Market price / EGI = $1,000,000 /

(4) Debt coverage ratio = NOI / Debt service = $111,150 / $61,636

11. The expected before-tax IRR on a potential real estate investment is 14 percent.

The expected after-tax IRR is 10.5 percent. What is the effective tax rate on this

investment?

12. An office building is purchased with the following projected cash flows:

• NOI is expected to be $130,000 in year 1 with 5 percent annual increases.

• The purchase price of the property is $720,000.

a. Calculate the unlevered internal rate of return (IRR).

Year 1 Year 2 Year 3 Year 4 Year 5

NOI $130,000 $136,500 $143,325 $150,491 $158,016

Sale price $860,000

b. Calculate the unlevered net present value (NPV).

Again, with a cash outflow of $720,000 at time zero (CF0), a required unlevered rate