CHAPTER 15

Mortgage Calculations and Decisions

Test Problems

1. The most common adjustment interval on an adjustable rate mortgage (ARM)

once the interest begins to change has been:

2. A characteristic of a partially amortized loan is:

3. If a mortgage is to mature (i.e. become due) at a certain future time without any

reduction in the original principalbalance, this is called:

4. The dominant loan type originated by most financial institutions is the:

5. Which of the following statements is true about 15-year and 30-year

fixed-payment mortgages?

d. Assuming they can afford the payments on both mortgages, borrowers usually

6. Adjustable rate mortgages (ARMs) commonly have all the following except:

7. The required calculation of the annual percentage rate (APR) by the lender is a

result of:

8. On a level-payment loan with 12 years (144 payments) remaining, at an interest

rate of 9 percent, and with a payment of $1,000, the current balance is:

9. On the following loan, what is the best estimate of the effective borrowing cost if

the loan is prepaid six years after origination?

Loan: $100,000

Interest rate: 7 percent

Term: 180 months

Up-front costs: 7 percent of loan amount

10. Lender’s yield differs from effective borrowing cost (EBC) because:

c. EBC accounts for additional third party up-front expenses that lender’s yield

Study Questions

1. Calculate the original loan size of a fixed-payment mortgage if the monthly

payment is $1,581.59, the annual interest is 5.0%, and the original loan term is 15

years.

Solution: Rounding to the nearest whole dollar, the original size of the loan is

calculator:

N = 180 I = 5/12 PV = ? PMT =$1,581.59 FV = 0

2. For a loan of $100,000, at 4 percent annual interest for 30 years, find the balance

at the end of 4 years and 15 years assuming monhly payments.

Solution: The loans balance at the end of 4 years and 15 years is $92,513.56 and

First, the loan payment must be calculated. The loan payment is $477.4153, as

solved below:

N = 360 I = 4/12 PV = -$100,000 PMT =? FV = 0

N = 312 I = 4/12 PV = ? PMT =$477.4153 FV =0

N = 180 I = 4/12 PV = ? PMT =$477.4153 FV = 0

3. On an adjustable rate mortgage, do borrowers always prefer smaller (tighter) rate

caps that limit the amount the contract interest rate can increase in any given year

or over the life of the loan?

Solution: Borrower preference is dependent, at elast in part, on their expectations

of future interest rates. Borrowers choosing ARMs with price caps are charged a

4. Consider a $75,000 mortgage loan with an annual interest rate of 4%. The loan

term is 7 years, but monthly payments will be based on a 30-year amortization

schedule. What is the monthly payment? What will be the required balloon

payment at the end of the loan term?

Solution: The monthly payment is $358.06 and the balloon payment is

The payment is calculated using the following calculator keystrokes:

N = 360 I = 4/12 PV = -$75,000 PMT =? FV = 0

the following calculator keystrokes:

N = 276 I = 4/12 PV = ? PMT =358.06 FV = 0

5. A mortgage banker is originating a level-payment mortgage with the following

terms:

Annual interest rate: 9 percent

Loan term: 15 years

Payment frequency: monthly

Loan amount: $160,000

Total up-front financing costs (including discount points): $4,000

Discount points to lender: $2,000

a. Calculate the annual percentage rate (APR) for Truth-in-Lending purposes.

b. Calculate the lender’s yield with no prepayment.

c. Calculate the lender’s yield with prepayment is five years.

d. Calculate the effective borrowing costs with prepayment in five years.

Solution:

calculator keystrokes:

N = 180 I = .75 PV = -$160,000 PMT =? FV = 0

N = 180 I = ? PV = -$156,000 PMT =$1,622.83 FV = 0

N = 180 I = ? PV = -$158,000 PMT =$1,622.83 FV = 0

c. In order to calculate the lender’s yield, the loan balance remaining at the end

N = 120 I = .75 PV = ? PMT =$1,622.83 FV = 0

The remaining balance is $128,108.67. With this information, the lender’s yield

N = 60 I = ? PV = -$158,000 PMT =$1,622.83 FV =$128,108.67

N = 60 I = ? PV = -$156,000 PMT =$1,622.83 FV =$128,108.67

6. Give some examples of up-front financing costs associated with residential

mortgages. What rule can one apply to determine if a settlement (closing) cost

should be included in the calculation of the effective borrowing costs?

Solution: Examples of upfront costs include discount points, loan origination fee,

loan application and documentation preparation fees, appraisal fees, credit check

The effective borrowing cost calculation should not include expenses that would

7. A homeowner is attempting to decide between a 15-year mortgage loan at 3.5

percent and a 30-year loan at 4.00 percent. Assume the up-front costs of the two

alternatives are equal. What would you advise? What would you advise if the

borrower also has a large amount of credit card debt outstanding at a rate of 15

percent?

Solution: If the borrower does not have a significant amount of debt at a rate well

above the rates on the loan, then the difference in mortgage rates should be

viewed as a maturity premium difference, and the borrower can consider the loans

as equivalent on a purely financial basis. If the borrower owes significant

8. Suppose a one-year ARM loan has a margin of 2.75, an initial index of 3.00

percent, a teaser rate for the first year of 4.00 percent, and a cap of 1.00 percent.

If the index rate is 3.00 percent at both the beginning and the end of the first year,

what will be the interest rate on the loan in year two? If there is more than one

possible answer, what does the outcome depend on?

Solution: If the periodic cap applies to the teaser rate, the interest rate in year two

9. Assume the following for a one-year rate adjustable rate mortgage loan that is tied

to the one-year Treasury rate:

Loan amount: $150,000

Annual rate cap: 2%

Life-of-loan cap: 5%

Margin: 2.75%

First-year contract rate: 5.50%

One-year Treasury rate at end of year 1: 5.25%

One-year Treasury rate at end of year 2: 5.50%

Loan term in years: 30

Given these assumptions, calculate the following:

a. Initial monthly payment

b. Loan balance end of year 1

c. Year 2 contract rate

d. Year 2 monthly payment

e. Loan balance end of year 2

f. Year 3 contract rate

g. Year 3 payment

Solution:

as calculated below:

N = 360 I = .4583 PV = -$150,000 PMT =? FV =0

N = 348 I = .4583 PV = ? PMT =$851.68 FV =0

c. Assuming the annual cap applies to the teaser rate, the interest rate in year

d. With a remaining term of 29 years, interest rate of 7.5 percent and a

N = 348 I = .6250 PV = -$147,979 PMT =? FV =0

N = 336 I = .6250 PV = ? PMT =$1,044.32 FV =0

g. The year three payment, based on a balance of $146,496, remaining term

10. Assume the following:

Loan Amount: $100,000

Interest rate: 10 percent annually

Term: 15 years, monthly payments

a. What is the monthly payment?

b. What will be the loan balance at the end of nine years?

c. What is the effective borrowing cost on the loan if the lender charges 3

points at origination and the loan goes to maturity?

d. What is the effective borrowing cost on the loan if the lender charges 3

points at origination and the loan is prepaid at the end of year 9?

Solution:

N = 180 I = 10/12=0.8333 PV = -$100,000 PMT =? FV =0

N = 72 (180-108) I = 10/12= 0.8333 PV = ? PMT =$1,074.605 FV =0

c. The effective borrowing cost of the loan, with financing costs of 3

N = 180 I = ? PV = $97,000 PMT =-$1,074.61 FV =0

d. The effective borrowing cost of the loan, with financing costs of 3 points,

N = 108 I = ? PV = $97,000 PMT =-$1,074.61 FV =-58,006

11. For a 30-year loan with a face value of 150,000, 5 percent annual interest, and

monthly payments find the monthly payment and remaining mortgage balance at

the end of year 5 and 20, and 30.

N = 360 I/YR = 5/12 PV = 150,000 PMT = ? FV = 0

N = 300 I/YR = 5/12 PV = ? PMT = 805.232 FV = 0

N = 120 I/YR = 5/12 PV = ? PMT = 805.232 FV = 0

12. Consider a 20-year loan with a monthly payment of $1,897.95 and an annual

interest rate of 4.5 percent. What was the original loan size?

N = 240 I/YR = 4.5/12 PV = ? PMT = 1,897.95 FV = 0

13. You are considering buying a $200,000 house with a 5 percent down payment, a

30-year mortgage, a fixed annual rate of 4.5 percent, and monthly payments.

What is the monthly payment? What is the monthly payment times 12? What is

the annual payment assuming payments are made annually instead of monthly?

Solution: 30 years is 360 months, and the monthly interest rate is 4.5/12. The loan

N = 360 I/YR=4.5/12 190,000 PMT = ? FV = 0

N = 30 I/YR=4.5 190,000 PMT = ? FV = 0

14. Consider a $200,000 mortgage loan with an annual interest rate of 7 percent. The

loan term is 8 years but the monthly payment is based on a 25-year amortization

period. Find the monthly payment and the balloon payment at the end of the loan

term.

N R PV FV PMT

300 0.5833 200,000 0 ?

N = 204 I/YR = 7/12 PV = 0 PMT = 1,413.56 FV = 0

15. Assume a $175,000 mortgage loan and 10-year term. The lender is charging an

annual interest rate of 6 percent and 4 discount points at origination. What is the

monthly payment assuming that it based on an amortization period of 30 years?

What will be the required balloon payment at the end of the 10 year? What is the

effective borrowing cost on the loan if it is held to maturity?

N = 360 I/YR = 6/12 PV = 175,000 PMT = ? FV = 0

N = 240 I/YR =0.5 PV = ? PMT = 1,049.21 FV = 0

The effective borrowing cost on the loan if the lender charges 4 points at

origination

N = 120 I/YR = ? PV = 168,000 PMT = -1,049.21 FV = -146,450

16. Assume that you have purchased a home and can qualify for a $200,000 loan. You

have narrowed your mortgage search to the following two options:

Mortgage A

Loan term: 30 years

Annual interest rate: 6 percent

Monthly payments

Up-front financing costs: $5,000

Discount points: 3

Mortgage B

Loan term: 15-years

Annual interest rate: 5.5 percent

Monthly payments

Up-front financing costs: $7,000

Discount points: 3

Based on the effective borrowing cost, which loan would you choose?

N = 360 I/YR = 6/12 PV = 200,000 PMT = ? FV =0

N =360 I/YR = ? PV = 189,000 PMT = -1,199.10 FV = 0

N = 180 I/YR = 5.5/12 PV = 200,000 PMT = ? FV = 0

N = 180 I/YR = ? PV = 187,000 PMT = -1,634.17 FV = 0

PV = ($200,000 x 0.97) – $7,000

EBC = 0.5459 monthly x 12 = 6.55%; so mortgage A has a slightly lower EBC

17. Consider a 25-year loan with an annual interest rate of 7 percent and monthly

payments of $1,201.53. The discount points charged by the lender at origination

are 3 percent and the cost of borrower title insurance and mortgage insurance are,

respectively, 0.5 percent and 2.0 percent of the loan amount. Additional fees paid

to other third parties (i.e., not the lender) will equal $4,000. What is the loan

amount? What is the lender’s yield/IRR? What is the effective borrowing cost

(EBC)?

N = 300 I/YR = 7/12 PV = ? PMT = 1,201.53 FV = 0

N R PV FV PMT

N = 300 I/YR = ? PV = -164,900 PMT = 1,201.53 FV = 0

N R PV FV PMT

N = 300 I/YR = ? 156,650 PMT = 1,201.53 FV = 0

18. Consider a one-year, $150,000 ARM with a 30-year amortization period. The

index rate is currently 3.75 percent and you estimate that it will increase by 25bp

(0.25%) each year for the following 2 years. The fixed margin is 225bp (2.25%),

but the lender is offering a teaser rate of 5 percent for the first year of the

mortgage.

a) Calculate the contract rate, remaining loan balance, and monthly payment

for each of the three years.

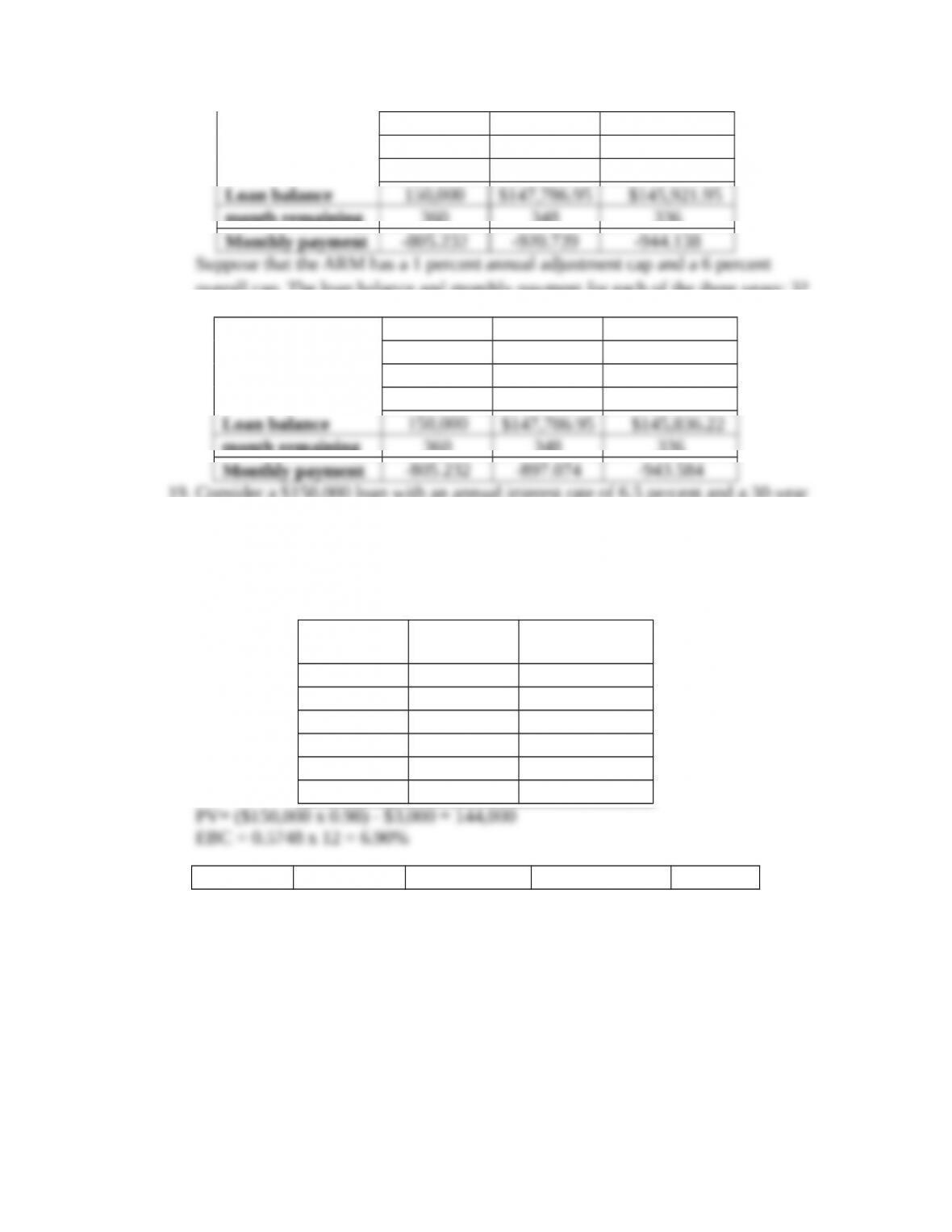

b) Suppose that the ARM has a 1 percent annual adjustment cap and a 6

percent overall cap. What is the loan balance and monthly payment for

each of the three years?

The contract rate, remaining loan balance, and monthly payment for each of the

three years

Beginning of Year 1 2 3

Index 3.75 4 4.25

Margin 2.25 2.25 2.25

Contract rate 5 6.25 6.5

month remaining 360 348 336

overall cap. The loan balance and monthly payment for each of the three years: 3?

Beginning of Year 1 2 3

Index 3.75 4 4.25

Margin 2.25 2.25 2.25

Contract rate 5 6.00 6.50

month remaining 360 348 336

19. Consider a $150,000 loan with an annual interest rate of 6.5 percent and a 30-year

term. Discount points are equal to 2 percent. All other up-front financing costs to

be paid by the borrower total $3,000. Compute the monthly payment and the loan

balance at the end of months 1-6. What is the effective borrowing cost (EBC)

assuming the loan remains outstanding to maturity?

Month Monthly

Pmt Loan balance

1 948.102 149,864.40

2 948.102 149,728.06

3 948.102 149,590.99

4 948.102 149,453.17

5 948.102 149,314.60

6 948.102 149,175.29

N = 360 I/YR = ? PV = 144,000 PMT = -948.10 FV = 0