Chapter 09 – Audit Sampling: An Application to Substantive Tests of Account Balances

9-13

To compute the upper error limit in IDEA, follow the steps outlined in the Chapter 9

IDEA problems and solutions available on the book’s online learning center,

McGraw-Hill Connect. The warning at the bottom of the screen refers to the way

“High Value” items are handled in the evaluation. For very large items that can be

the account contains a misstatement greater than $212,500.

9-23 a. Using Table 8-5 with a desired confidence level of 95% (risk of incorrect acceptance

= 5%); tolerable misstatement = 4% ($360,000 $9,000,000); expected misstatement

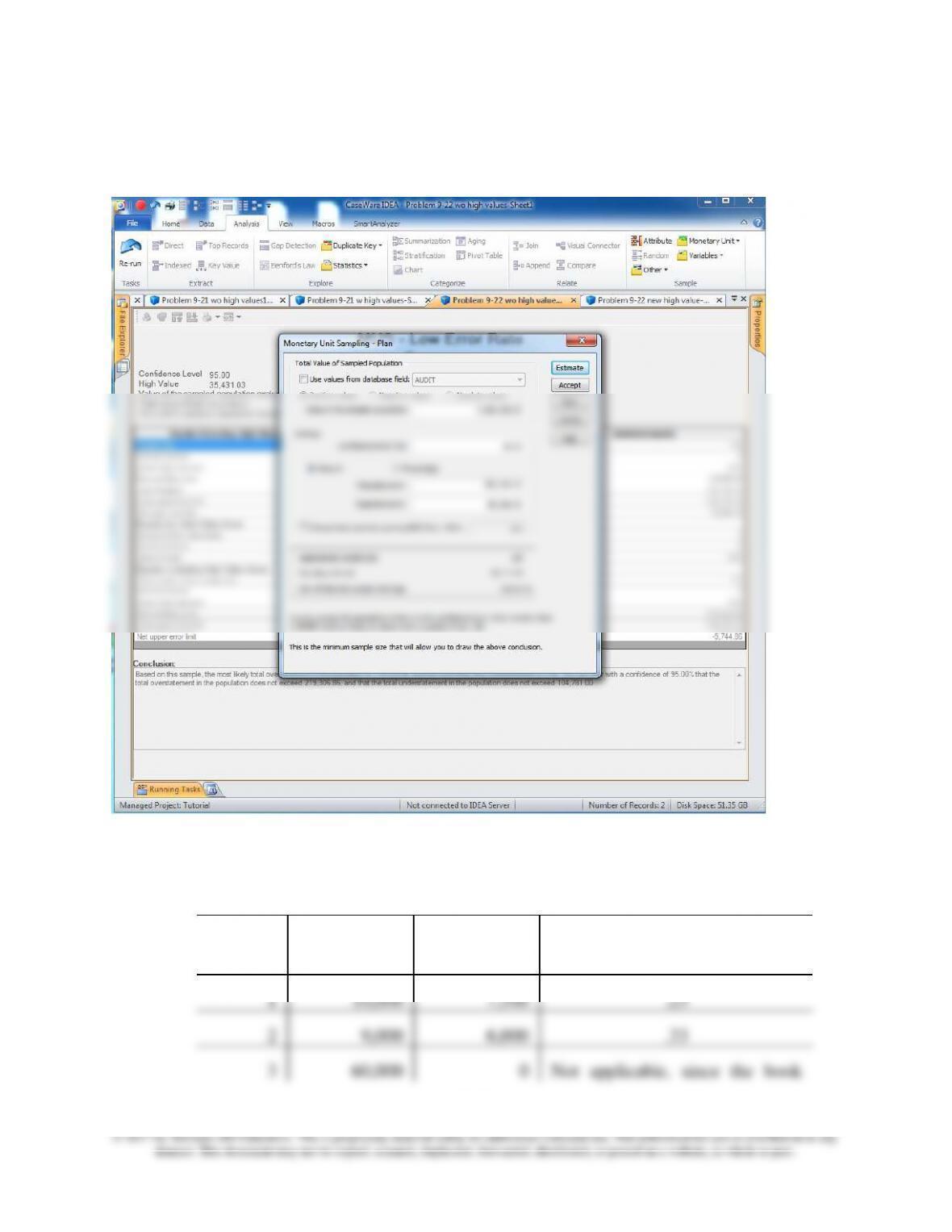

uncheck the box “Use values from database field.”

Chapter 09 – Audit Sampling: An Application to Substantive Tests of Account Balances

9-14

The output from IDEA is provided below:

b. The upper misstatement limit is calculated as follows:

Overstatement Errors

Error

Number

Book Value

Audit Value

Tainting Factor

1

10,000

7,500

.25

2

9,000

6,000

.33

3

60,000

0

Not applicable, since the book

Chapter 09 – Audit Sampling: An Application to Substantive Tests of Account Balances

9-15

value exceeds the sampling

interval.

4

800

640

.20

Error Number

Tainting

Factor

Sampling

Interval

Projected

Misstatement

(column 2 x 3)

95%

Misstatement

Factor or

Increment (from

Table 9-3)

Upper

Misstatement

Limit

(column 2 x 3

x 5)

Basic Precision

1.0

$57,692

NA

3.0

$173,076

2

.33

57,692

19,038

1.7 (4.7 – 3.0)

32,365

1

.25

57,692

14,423

1.5 (6.2 – 4.7)

21,635

4

.20

57,692

11,538

1.4 (7.6 – 6.2)

16,153

Add misstatements

detected in logical

units greater than

the sampling

interval:

Error 3

NA

57,692

60,000

NA

60,000

Upper Misstatement Limit

$303,229

NA—Not Applicable

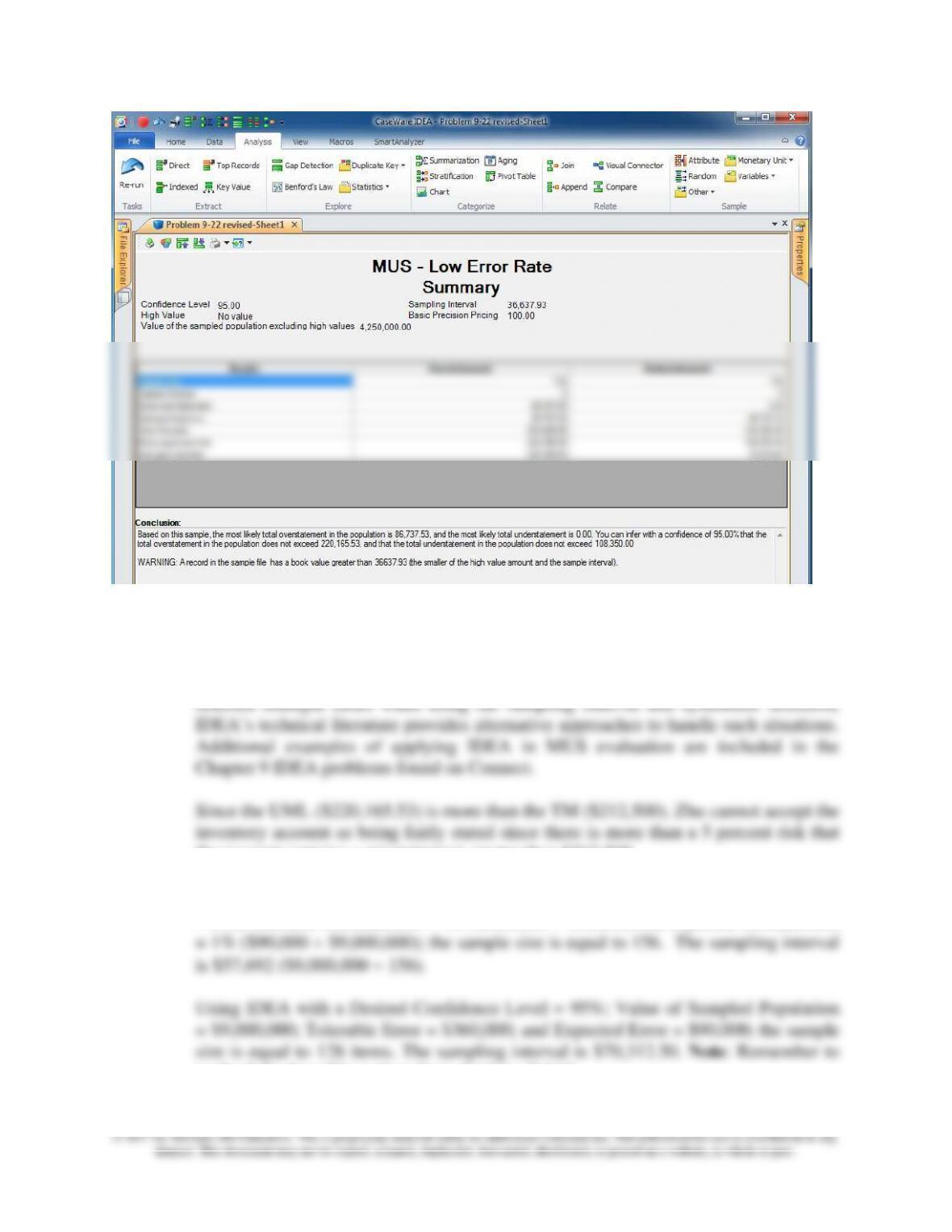

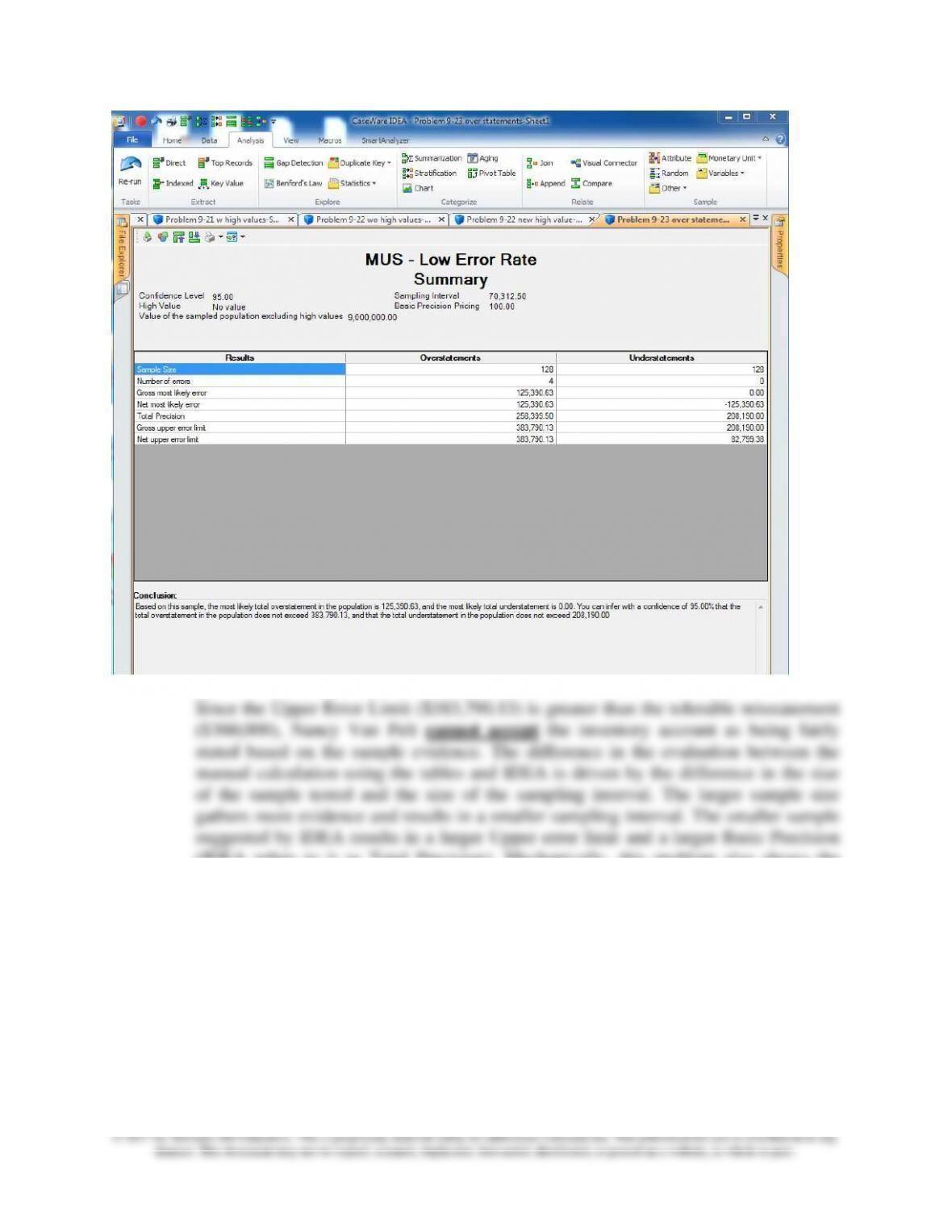

Since the UML ($303,229) is less than the tolerable misstatement ($360,000), Nancy

Van Pelt can accept the inventory account as being fairly stated since there is only a 5

percent risk that the account contains a misstatement greater than $360,000.

Chapter 09 – Audit Sampling: An Application to Substantive Tests of Account Balances

9-16

(IDEA refers to it as Total Precision). Mechanically, this problem also shows the

influence of the size of the sampling interval. Because the $60,000 item is smaller

than the sampling interval in the IDEA calculation, that error results in an error

projection (most likely error) and contributes to the upper error limit or allowance for

sampling risk more than just the known error in that sample item. On the other hand,

when using the tables, the sample size is larger and the sampling interval is $57,692.

As such, all items greater than the interval will be tested and therefore the known

error associated with the $60,000 item is added to the UML, but it requires no

additional margin for sampling risk when using the tables.

Chapter 09 – Audit Sampling: An Application to Substantive Tests of Account Balances

9-17

c. The calculation of the adjustment for the understatement errors is as follows:

Understatement Errors

Error Number

Book Value

Audit Value

Tainting Factor

5

6,000

6,500

-.083

6

750

800

-.067

Adjustment for Understatement Errors

Tainting

Factor

Sampling

Interval

Projected

Misstatement

-.083

57,692

-4,788

-.067

57,692

-3,865

Adjustment to Most Likely Error

(and UML)*

-8,653

* As noted in the textbook, some auditors adjust down both the Most Likely Error and

the UML. Note that IDEA reports both the unadjusted Gross Most Likely Error and

the adjusted Net Most Likely Error. Similarly, IDEA reports both the Gross Upper

Error Limit and the Net Upper Error Limit.

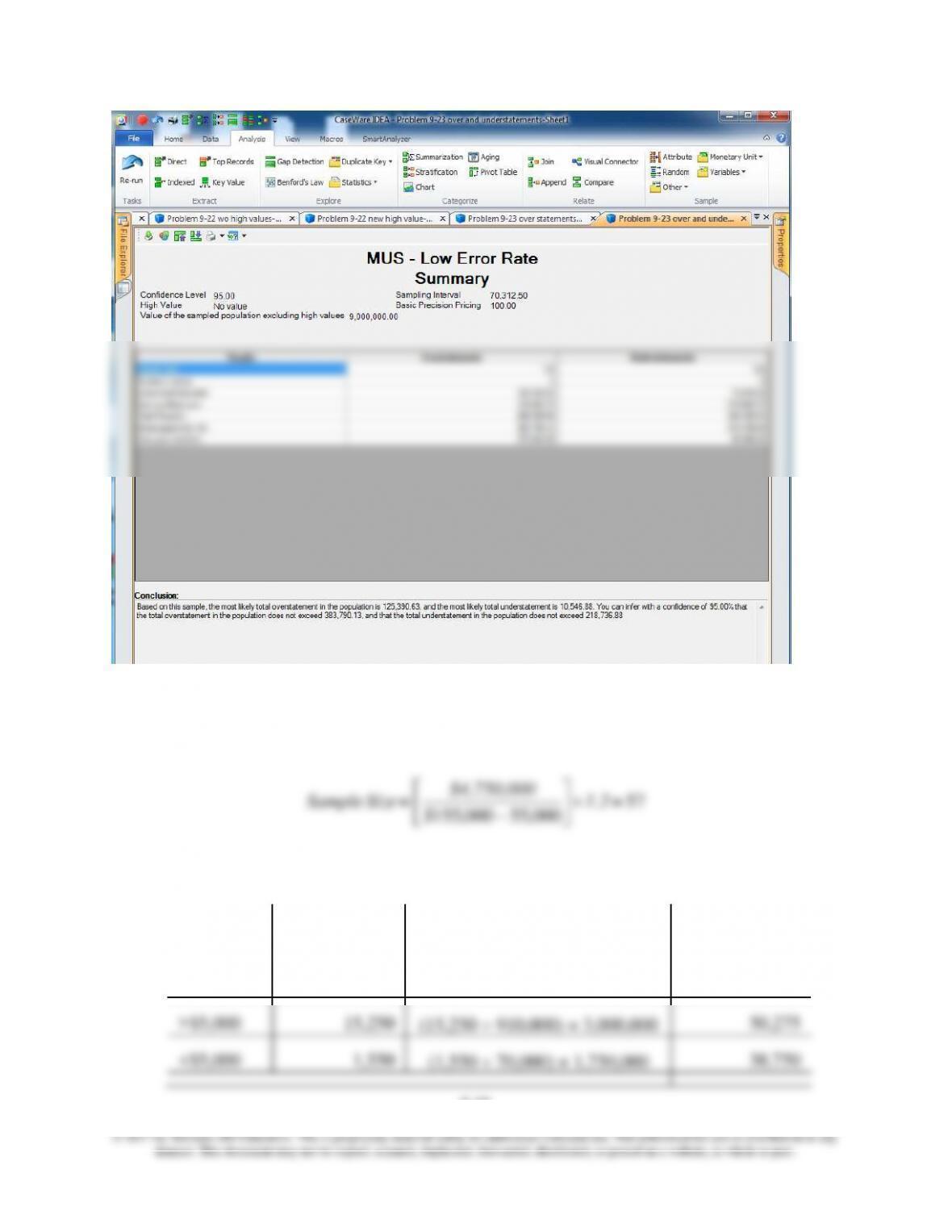

Using IDEA and the results from parts (a) and (b), the Gross Most Likely Error is

$125,390.63 and the Net Most Likely Error is $114,843.75. The Gross Upper Error

Limit is $383,790.13 and the Net Upper Error Limit is $373,243.25. Adjustment to

the most likely error is –$10,546.88 ($125,390.63 – $114,843.75) and the same

adjustment is made to the upper error limit.

The output from IDEA is provided below:

Chapter 09 – Audit Sampling: An Application to Substantive Tests of Account Balances

9-18

9-24 a. Remove the 10 accounts greater than $50,000 (total value $750,000) from the

sampling population because they will be the subject of 100% testing. Sample size is

calculated as follows:

b. The projected misstatement for the accounts receivable account is:

Strata

Amount of

Misstatement

Ratio of Misstatements in

Stratum Tested

Projected

Misstatement

>$50,000

$ 3,500

NA 100% of Strata Tested

$ 3,500

>$5,000

15,250

(15,250 910,000) × 3,000,000

50,275

<$5,000

1,550

(1,550 70,000) × 1,750,000

38,750

57

000,55000,155 = 1.2

$

$4,750,000

= SizeSample

−

Chapter 09 – Audit Sampling: An Application to Substantive Tests of Account Balances

9-19

Total projected misstatement

$ 92,525

Since the projected misstatement, $92,525, is significantly greater than the

expected misstatement, $55,000, Gren should conclude that there is an unacceptably

high risk that the true misstatement exceeds the tolerable misstatement (i.e., must

consider the original allowance for sampling risk of $100,000 ($155,000 – 55,000)).

9-25 a. The calculation of the sample size for Wang’s test of Cougar Goldust is:

Sample size

43

000,10000,35

64.1000,4 =

–

25 xx

=

2

.03, round to 44

b. The calculation of the sample results is as follows:

Sample Size = 400

100 = 4

Thus, the average misstatement in a bin based on the sample data is an overstatement

of 4 ounces. Next, the mean misstatement is projected to the population:

Projected population = Population size x Mean misstatement

misstatement (in sampling units) per sampling item

16,000 ounces = 4,000 x 4

The allowance for sampling risk is represented by the confidence bound. To calculate the

confidence bound, the auditor first calculates the standard deviation and then uses the

equation shown below, using the CC value for the level of desired confidence.

SD = Total squared audit difference – sample size x mean difference per samplingitem2

( )

sample size – 1

( )

4

100 – 17,856

2

where N = population size (in sampling units)

Chapter 09 – Audit Sampling: An Application to Substantive Tests of Account Balances

9-20

n = sample size

CC = Confidence Coefficient

SD = Standard Deviation of Audit Differences

For Cougar Goldust, the confidence bound is 8,403 ounces and the confidence

interval is calculated as follows:

Confidence interval = Projected population misstatement + Confidence bound

records are fairly stated with a 90 percent confidence level.

9-26 The calculation of the sample results for Hipp Supply Company is as follows:

The calculation of the mean misstatement per sampling item is:

Mean Misstatement per sampling item

= Total audit difference

SampleSize = $481

100 = $4.81

Thus, the average misstatement for an inventory item based on the sample data is an

overstatement of $4.81. Next, the mean misstatement is projected to the population as

follows:

The allowance for sampling risk is represented by the confidence bound. To calculate the

confidence bound, the auditor first calculates the standard deviation and then uses the

equation shown below, using the CC value for the level of desired confidence.

SD = Total squared audit difference – sample size x mean difference per samplingitem2

( )

sample size – 1

Chapter 09 – Audit Sampling: An Application to Substantive Tests of Account Balances

9-21

100

n

where N = population size (in sampling units)

CC = Confidence Coefficient

SD = Standard Deviation of Audit Differences

n = sample size

For Hipp Supply Company, the confidence bound is $1,283 and the confidence interval is

calculated as follows:

Confidence interval = Projected Population Misstatement + Confidence bound

Solutions to Discussion Cases

9-27 The incorrect assumptions, statements, and inappropriate applications of sampling are as

follows:

• Classical variables sampling is not designed for tests of controls.

• MUS uses each dollar in the population, not each account, as a separate sampling

unit.

• MUS is not efficient if many misstatements are expected because the sample size can

misstatement for this difference was actually $2,500 ($1,000/$4,000 x $10,000

sampling interval).

• The difference in the understated account (recorded amount of $1,900 and audited

Chapter 09 – Audit Sampling: An Application to Substantive Tests of Account Balances

9-22

was erroneous.

9-28 a. While Doug’s selection method is not random, judgmentally “targeting” items for

testing is acceptable under auditing standards and it may be preferable if there is

Chapter 09 – Audit Sampling: An Application to Substantive Tests of Account Balances

9-23

b. Because the items selected were not identified randomly, Doug cannot use statistical

sampling methods to quantify sampling risk or evaluate his results. His “sample”

accounts for 66% ($720,000/$1,090,000) of ending inventory and even though it isn’t

technically appropriate to project the results from the “sample,” in practice auditors

and are less likely to contain misstatements), it appears reasonable to conclude he has

sufficient evidence to consider the balance fairly stated.