Chapter 09 – Audit Sampling: An Application to Substantive Tests of Account Balances

CHAPTER 9

AUDIT SAMPLING: AN APPLICATION TO

SUBSTANTIVE TESTS OF ACCOUNT BALANCES

Answers to Review Questions

9-1 The steps in a statistical sampling application for substantive testing include (by phases):

Planning

1. Determine the test objectives.

2. Define the population characteristics:

o Define the population.

o Population size.

Performance

4. Select sample items.

5. Perform the audit procedures:

Evaluation

6. Calculate the projected misstatement and the upper limit on misstatement.

7. Draw final conclusions.

9-2 When monetary-unit sampling (MUS) is used, the sampling unit is defined as an

individual monetary unit (e.g., a dollar or other forms of currency). When classical

9-3 The following table shows how the desired confidence level, tolerable misstatement, and

expected misstatement are related to sample size:

Factor

Relationship to Sample Size

Desired confidence level

Direct

Tolerable misstatement

Inverse

Expected misstatement

Direct

Chapter 09 – Audit Sampling: An Application to Substantive Tests of Account Balances

9-2

Chapter 09 – Audit Sampling: An Application to Substantive Tests of Account Balances

9-3

9-4 The advantages and disadvantages of MUS are:

Advantages:

• When the auditor expects no misstatements, MUS will normally result in a smaller

sample size than classical variables sampling.

• The calculation of sample size and the evaluation of the sample results are not based on

Disadvantages:

• Selection of a zero or negative balance generally requires special design consideration.

9-5 Probability-proportional-to-size sample selection gives each individual dollar or monetary

unit in the population an equal chance of being selected. Each selected dollar represents a

group of dollars (referred to as the sampling interval). The sampling interval is

9-6 The decision rule for determining the acceptability of sample results when MUS is used

compares the tolerable misstatement (TM) to the upper misstatement limit (UML). If

UML is less than TM, the evidence supports the fair presentation of the account. If UML

9-7 Variation in the population, the risk of incorrect acceptance, and tolerable and expected

misstatement affect sample size in the following way:

• Desired confidence level: Direct-as the desired confidence level increases, the required

sample size increases.

• Risk of material misstatement: Direct-as the risk of material misstatement increases, the

• Expected misstatement: Direct-an increase in expected misstatement results in an

increase in sample size.

Chapter 09 – Audit Sampling: An Application to Substantive Tests of Account Balances

9-4

9-5

9-8 The AICPA’s audit guide describes two acceptable methods of projecting the amount of

misstatement found in a nonstatistical sample, ratio projection and difference projection.

Ratio projection determines the amount of misstatement by dividing the amount of

misstatement by the percentage of the dollars of the population included in the sample.

the population, difference projection should be used.

9-9 The advantages and disadvantages of classical variables sampling are:

Advantages:

• When the auditor expects a relatively large number of differences between book and

audited values, classical variables sampling will normally result in a smaller sample

size than MUS.

• Classical variables sampling techniques are effective for both overstatements and

Disadvantages:

• When using the approach to evaluate likely misstatements in an account or population,

some classical variables sampling techniques (e.g., difference estimation) do not work

9-10 The decision that the evidence supports or does not support the account balance using

classical variables sampling is made by determining whether the upper and lower limits

are within tolerable misstatement. If both limits are within the bounds of tolerable

Chapter 09 – Audit Sampling: An Application to Substantive Tests of Account Balances

9-6

Chapter 09 – Audit Sampling: An Application to Substantive Tests of Account Balances

Answers to Multiple-Choice Questions

Chapter 09 – Audit Sampling: An Application to Substantive Tests of Account Balances

9-8

c. The total projected misstatement for the three misstatements identified is calculated

by first computing the tainting factor as follows:

Misstatement

Number

Book

Value

Audit

Value

Tainting

Factor

1

$400

$320

.20

2

500

0

1.00

3

3,000

2,500

Not applicable, since book value

exceeds sampling interval.

Chapter 09 – Audit Sampling: An Application to Substantive Tests of Account Balances

9-9

The upper misstatement limit is calculated as follows:

Misstatement

Number

Tainting

Factor

Sampling

Interval

Projected

Misstatement

(column 2 x 3)

95%

Misstatement

Factor or

Increment (from

Table 9-3)

Upper

Misstatement

Limit

(column 2 x 3 x 5)

Basic Precision

1.0

$1,657

NA

3.0

$4,971

2

1.0

1,657

1,657

1.7 (4.7 – 3.0)

2,817

1

.20

1,657

331

1.5 (6.2 – 4.7)

497

Add misstatements

detected in logical

units greater than

the sampling

interval:

Misstatement 3

NA

1,657

500

NA

500

Upper Misstatement Limit

$8,785

NA—Not Applicable

Since the UML ($8,785) is less than the TM ($15,000), the evidence supports the fair

presentation of the account balance.

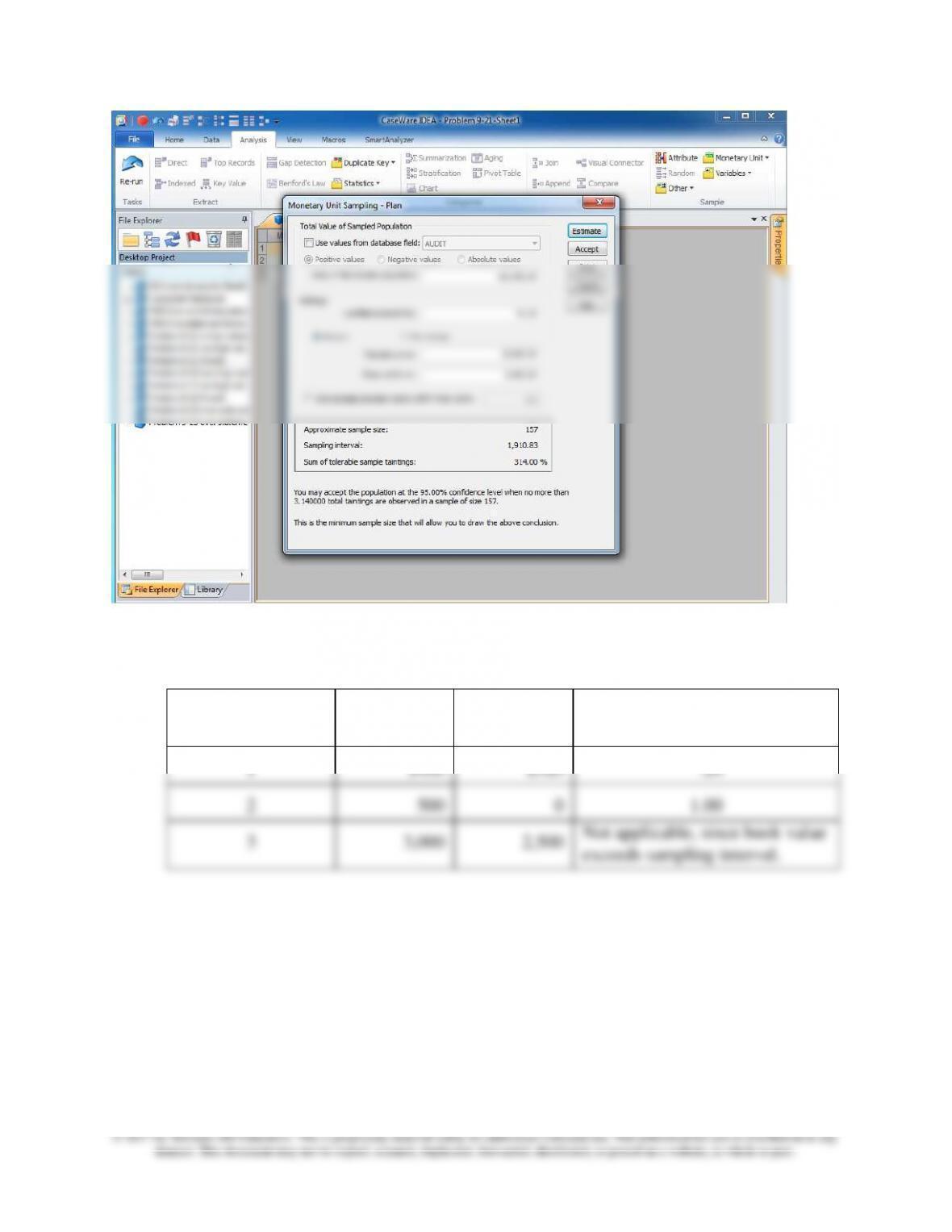

Using IDEA and the IDEA sample size calculated by in part (b), the Upper Error Limit is

$9,655.64 and the Most Likely Error is $2,611.46. Since the Upper Error Limit is less than

the TM ($15,000), the evidence supports the fair presentation of the account balance. The

Chapter 09 – Audit Sampling: An Application to Substantive Tests of Account Balances

9-10

The warning at the bottom of the screen refers to the way “High Value” items are handled

in the evaluation. For very large items that can be selected multiple times when using the

sampling interval and systematic selection, IDEA’s technical literature provides

alternative approaches to handle such situations. Additional examples of applying IDEA

in MUS evaluation are included in the Chapter 9 IDEA problems found in Connect.

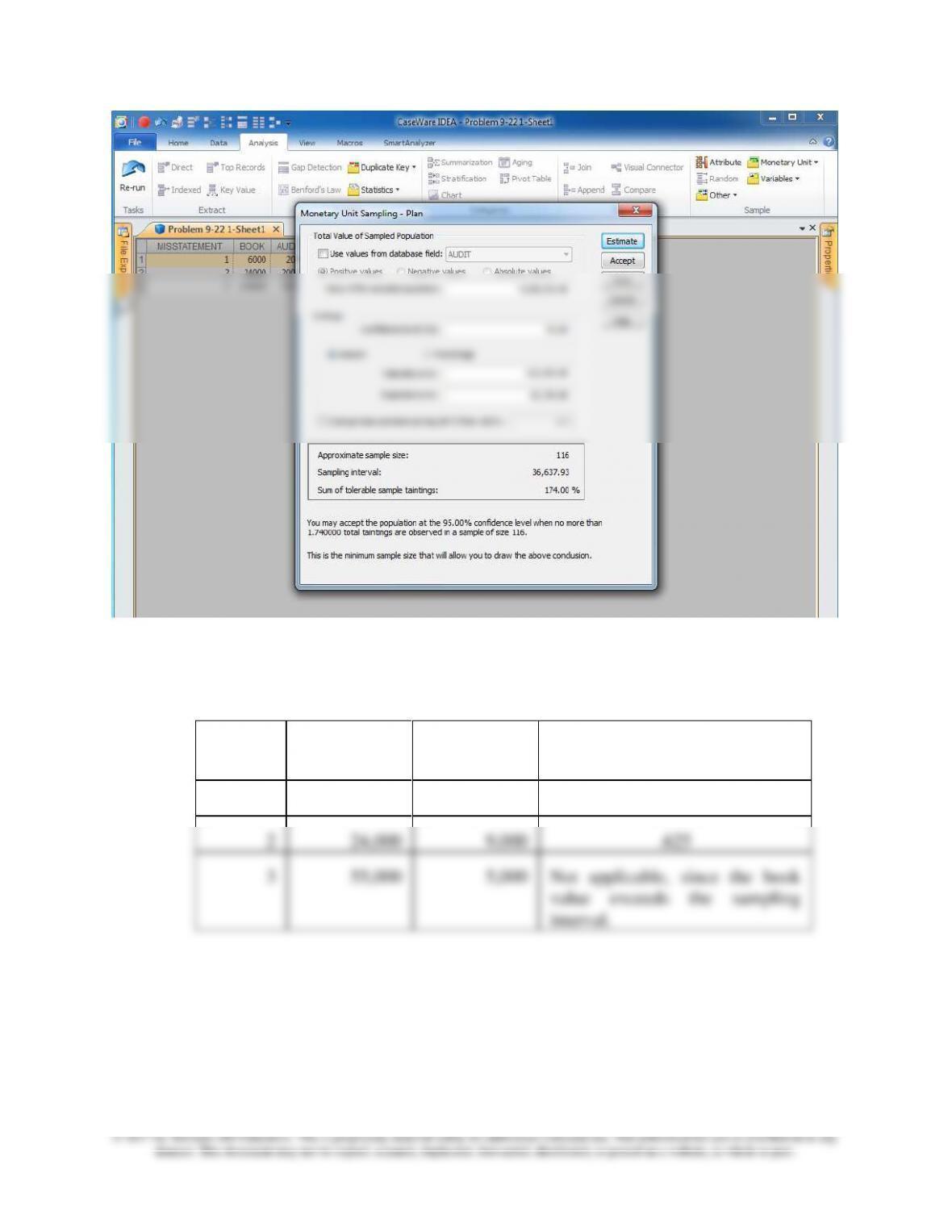

9-22 a. Using Table 8-5 with a desired confidence level = 95% (risk of incorrect acceptance

= 5%); tolerable misstatement = 5% ($212,500 $4,250,000); expected misstatement

= 1.5% ($63,750 $4,250,000); the sample size is equal to 124. The sampling

uncheck the box “Use values from database field.”

The output from IDEA is provided below:

Chapter 09 – Audit Sampling: An Application to Substantive Tests of Account Balances

9-11

b. The upper misstatement limit is calculated as follows:

Overstatement Errors

Error

Number

Book Value

Audit Value

Tainting Factor

1

6,000

1,000

.883

2

24,000

9,000

.625

3

55,000

5,000

Not applicable, since the book

value exceeds the sampling

interval.

Chapter 09 – Audit Sampling: An Application to Substantive Tests of Account Balances

9-12

Error Number

Tainting

Factor

Sampling

Interval

Projected

Misstatement

(column 2 x 3)

95%

Misstatement

Factor or

Increment (from

Table 9-3)

Upper

Misstatement

Limit

(column 2 x 3

x 5)

Basic Precision

1.0

$34,274

NA

3.0

$102,822

1

.883

34,274

28,550

1.7 (4.7 – 3.0)

48,535

2

.625

34,274

21,421

1.5 (6.2 – 4.7)

32,132

Add misstatements

detected in logical

units greater than

the sampling

interval:

Error 3

NA

34,274

50,000

NA

50,000

Upper Misstatement Limit

$233,489

NA—Not Applicable

Since the UML ($233,489) is more than the TM ($212,500), Zhu cannot accept the

inventory account as being fairly stated since there is more than a 5 percent risk that

the account contains a misstatement greater than $212,500.