Chapter 02 – The Financial Statement Auditing Environment

2-1

CHAPTER 2

THE FINANCIAL STATEMENT AUDITING ENVIRONMENT

2-1 Auditors can be classified under four types: (1) external auditors, (2) internal auditors, (3)

government auditors, and (4) forensic auditors.

2-2 Examples of compliance audits include (1) internal auditors determining whether

corporate rules and policies are being followed by departments within the organization, (2)

an examination of tax returns of individuals and companies by the Internal Revenue

Service for compliance with the tax laws, and (3) an audit under the Single Audit Act of

Examples of forensic audits include (1) an examination by an external auditor of cash

disbursements for payments to unauthorized vendors, (2) assistance by an auditor to a law

enforcement agency in tracing laundered monies by organized criminals, and (3) an

independent auditor helping identify hidden assets as part of a divorce settlement.

Student answers will likely be less detailed but should capture the general idea of each

type of audit.

2-3 During the late 1990s and early 2000s, accounting firms aggressively sought opportunities

to expand their business in nonaudit services such as consulting. This expansion from their

core audit practice, combined with allegations of auditors refusing to challenge

2-4 The accounting profession’s expansion into new areas, combined with changes in the

overall business environment, resulted in new regulations and guidelines. The scandals of

the late 1990s and early 2000s brought into question the profession’s ability to self–

Chapter 02 – The Financial Statement Auditing Environment

2-2

© 2017 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any

manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part.

reporting system and for the profession. Further, somewhat ironically, the SOX-mandated

audit of internal control over financial reporting has brought significant new revenues to

accounting firms.

2-5 Management is responsible to prepare financial statements that fairly present the

company’s financial condition and operations in accordance with established accounting

standards. Note that the auditor’s opinion explicitly states that the financial statements are

the responsibility of management. The auditor is responsible to issue an opinion in regards

to the financial statements prepared by management. In order to issue this opinion, the

2-6 The essential components of the high-level model of business offered in the chapter are:

corporate governance, objectives, strategies, processes, controls, transactions, and

financial statements. Corporate governance is carried out by management and the board of

directors in order to ensure that business objectives are carried out and that company

2-7 The information system must maintain a record of all businesses transactions. It should be

capable of producing accurate financial reports to summarize the effects of the entity’s

transactions. Among other things, internal control is required to ensure that a proper

environment is established and that transactions are appropriately conducted and recorded

2-8 The AICPA issues the following standards:

• Statements on Auditing Standards

• Statements on Standards for Attestation Engagements

• Statements on Standards for Tax Services

Chapter 02 – The Financial Statement Auditing Environment

2-3

2-9 The PCAOB is a quasi-governmental organization overseen by the SEC. It was formed to

provide governmental regulation of the standards used in conducting public company

2-10 The SEC has congressional authority from the original Securities Acts of 1933 and 1934

to establish accounting and auditing standards for publicly traded companies; however, in

the past the SEC has largely delegated this authority to other bodies, including the FASB

and the AICPA’s Auditing Standards Board. The Sarbanes-Oxley Act of 2002 gave the

2-11 The documents most frequently encountered by auditors under the Securities Exchange

Act of 1934 are forms 10-K, 10-Q, and 8-K. Forms 10-K and 10-Q are, respectively,

2-12 The four categories of Principles Underlying an Audit Conducted in Accordance with

GAAS are the purpose and premise of an audit, personal responsibilities of the auditor,

auditor actions in performing the audit, and reporting. The Principles Underlying an

2-13 GAAS is composed of three categories of standards: general standards, standards of field

work, and standards of reporting. The ten GAAS and the SAS are minimum standards of

performance because circumstances of individual engagements may require the auditor to

2-14 Independence is a fundamental principle for auditors. If an auditor is not independent of

the client, users may lose confidence in the auditor’s ability to report objectively and

truthfully on the financial statements, and the auditor’s work loses its value. From an

Chapter 02 – The Financial Statement Auditing Environment

Answers to Multiple-Choice Questions

2-15

b

2-20

a

2-16

a

2-21

a

2-17

b

2-22

c

2-18

d

2-23

c

2-19

c

Solutions to Problems

2-24

Item Number

Type of Audit

Type of Auditor

a.

Operational

Government

b.

Financial statement

External

c.

Compliance or operational or

possibly internal control

Internal or external

d.

Forensic/Financial

Internal, external, or forensic

e.

Operational

Government, external, or

internal

f.

Operational

Internal or external

g.

Compliance

Government

h.

Compliance or forensic

Government, external, or

forensic

2-25 a.

Brief Description of Generally

Accepted Auditing Standards

Sally Jones’ Actions Resulting in

Failure to Comply with Generally

Accepted Auditing Standards

General Standards:

1. The auditor must have adequate

technical training and proficiency to

perform the audit.

1. It was inappropriate for Jones to hire

the two students to conduct the

audit. The examination must be

conducted by persons with proper

education and experience in the field

of auditing. Although a junior

Chapter 02 – The Financial Statement Auditing Environment

assistant has not completed his

formal education, he may help in the

conduct of the examination as long

as there is proper supervision and

review.

2. The auditor must maintain

independence in mental attitude in all

matters relating to the audit.

2. To satisfy the second general

standard, Jones must be without bias

with respect to the client under

audit. Jones has an obligation for

fairness to the owners, management,

and creditors who may rely on the

report. Because of the financial

interest in whether the bank loan is

granted to Boucher, Jones is not

independent in either fact or

appearance with respect to the

assignment undertaken.

3. The auditor must exercise due

professional care in the performance

of the audit and the preparation of the

report.

3. This standard requires Jones to plan

and perform the audit with due care,

which imposes on Jones and

everyone in her firm a responsibility

to observe the standards of field

work and reporting. Exercise of due

care requires critical review at every

level of supervision of the work

done and the judgments exercised by

those assisting in the examination.

Jones did not review the work or the

judgments of the assistants and

clearly failed to adhere to this

standard.

Standards of Field Work:

1. The auditor must adequately plan the

work and must properly supervise

any assistants.

1. This standard recognizes that early

appointment of the auditor has

advantages for the auditor and the

client. Jones accepted the

engagement without considering the

Chapter 02 – The Financial Statement Auditing Environment

2. The auditor must obtain a sufficient

understanding of the entity and its

environment, including its internal

control, to assess the risk of material

misstatement of the financial

statements whether due to error or

fraud, and to design the nature,

timing, and extent of further audit

procedures.

2. Jones did not study the client or its

environment, including internal

control, nor did the assistants. There

appears to have been no audit

examination at all. The work

performed was more an accounting

service than it was an auditing

service.

3. The auditor must obtain sufficient

appropriate audit evidence by

performing audit procedures to afford

a reasonable basis for an opinion

regarding the financial statements

under audit.

3. Jones acquired little evidence that

would support the fairness of the

financial statements. Jones merely

checked the mathematical accuracy

of the records and summarized the

accounts. Several standard audit

procedures and techniques were

neglected.

Standards of Reporting:

1. The auditor must state in the

auditor’s report whether the financial

statements are presented in

accordance with generally accepted

accounting principles (GAAP).

1. Jones’ report made no reference to

generally accepted accounting

principles. Because Jones did not

conduct a proper examination, the

report should state that no opinion

can be expressed as to the fair

presentation of the financial

statements in accordance with

GAAP.

2. The auditor must identify in the

auditor’s report those circumstances

in which such principles have not

been consistently observed in the

current period in relation to the

preceding period.

2. Jones’ improper examination would

not enable her to determine whether

accounting principles have been

consistently applied.

3. When the auditor determines that

informative disclosures are not

reasonably adequate, the auditor

must so state in the auditor’s report.

3. Management is responsible for

adequate disclosure in the financial

statements, but when the statements

do not contain adequate disclosures

the auditor should make such

disclosures in the auditor’s report.

Both the statements and the auditor’s

report lack adequate disclosures.

Chapter 02 – The Financial Statement Auditing Environment

4. The auditor must either express an

opinion regarding the financial

statements, taken as a whole, or state

that an opinion cannot be expressed,

in the auditor’s report. When the

auditor cannot express an overall

opinion, the auditor should state the

reasons therefore in the auditor’s

report. In all cases where an auditor’s

name is associated with financial

statements, the auditor should clearly

indicate the character of the auditor’s

work, if any, and the degree of

responsibility the auditor is taking, in

the auditor’s report.

4. Although Jones’ report contains an

expression of opinion, her opinion is

not based on the results of a proper

audit examination. Jones should

disclaim an opinion because she

failed to conduct an examination in

accordance with generally accepted

auditing standards.

b.

Brief Description of Principles Underlying an

Audit

Sally Jones’ Actions Resulting in Failure to

Comply with Principles Underlying an Audit

Purpose and Premise of an Audit:

An audit is to provide an opinion by an auditor on

whether financial statements are presented fairly,

in all material respects, according to the applicable

framework. Management and those charged with

governance are responsible for the preparation and

fair presentation of the financial statements and

for the design, implementation, and maintenance

of internal control over financial reporting. They

are also responsible for providing the auditor with

all information relevant to the preparation of the

financial statements.

Jones expressed an opinion regarding the financial

statements, but not on whether the financial

statements are presented fairly in accordance with

generally accepted accounting principles, or any

other financial reporting framework. Therefore, she

did not fulfill the primary purpose of the audit.

Jones did not ensure that management fulfilled its

responsibilities for the fair presentation of the

financial statements, since that requires making the

appropriate disclosures in the financial statements.

Chapter 02 – The Financial Statement Auditing Environment

Responsibilities:

Auditors are responsible for having appropriate

competence and capabilities to perform the audit;

complying with relevant ethical requirements; and

maintaining professional skepticism and

exercising professional judgment, throughout the

planning and performance of the audit.

It was inappropriate for Jones to hire the two

students to conduct the audit, because they do not

have appropriate competence and capabilities.

In order to comply with ethical requirements, Jones

must be without bias with respect to the client under

audit. Because of the financial interest in whether

the bank loan is granted to Boucher, Jones is not

independent in either fact or appearance with respect

to the assignment undertaken.

Neither Jones nor her two assistants exercised

professional skepticism or professional judgment in

performing the audit.

Performance:

The auditor must obtain reasonable assurance

about whether the financial statements as a whole

are free from material misstatement, whether due

to fraud or error. To do so, the auditor must plan

the work and supervise any assistants; determine

an appropriate materiality level; identify and

assess risks of material misstatement based on an

understanding of the entity and its environment,

including its internal control; and obtain sufficient

appropriate audit evidence about whether

misstatements exist. The auditor is unable to

obtain absolute assurance that the financial

statements are free from material misstatements.

Jones failed to supervise the assistants. The work

performed was not adequately planned.

Jones did not study the client or its environment,

including internal control, nor did the assistants.

Consequently, she could not have identified risks of

material misstatements.

Jones acquired little evidence that would support the

fairness of the financial statements. Jones merely

checked the mathematical accuracy of the records

and summarized the accounts. Several standard

audit procedures and techniques were neglected.

Reporting:

Based on an evaluation of the audit evidence

obtained, the auditor expresses an opinion in

accordance with the auditor’s findings, or states

that an opinion cannot be expressed. The opinion

states whether the financial statements are

presented fairly, in all material respects, in

accordance with the applicable financial reporting

framework.

Although Jones’ report contains an expression of

opinion, her opinion is not based on the results of a

proper audit examination. Jones should disclaim an

opinion because she failed to conduct an

examination in accordance with generally accepted

auditing standards.

Jones’ opinion made no reference to the applicable

financial reporting framework. Also, since the

financial statements did not contain adequate

disclosures, they could not have been in accordance

with any financial reporting framework.

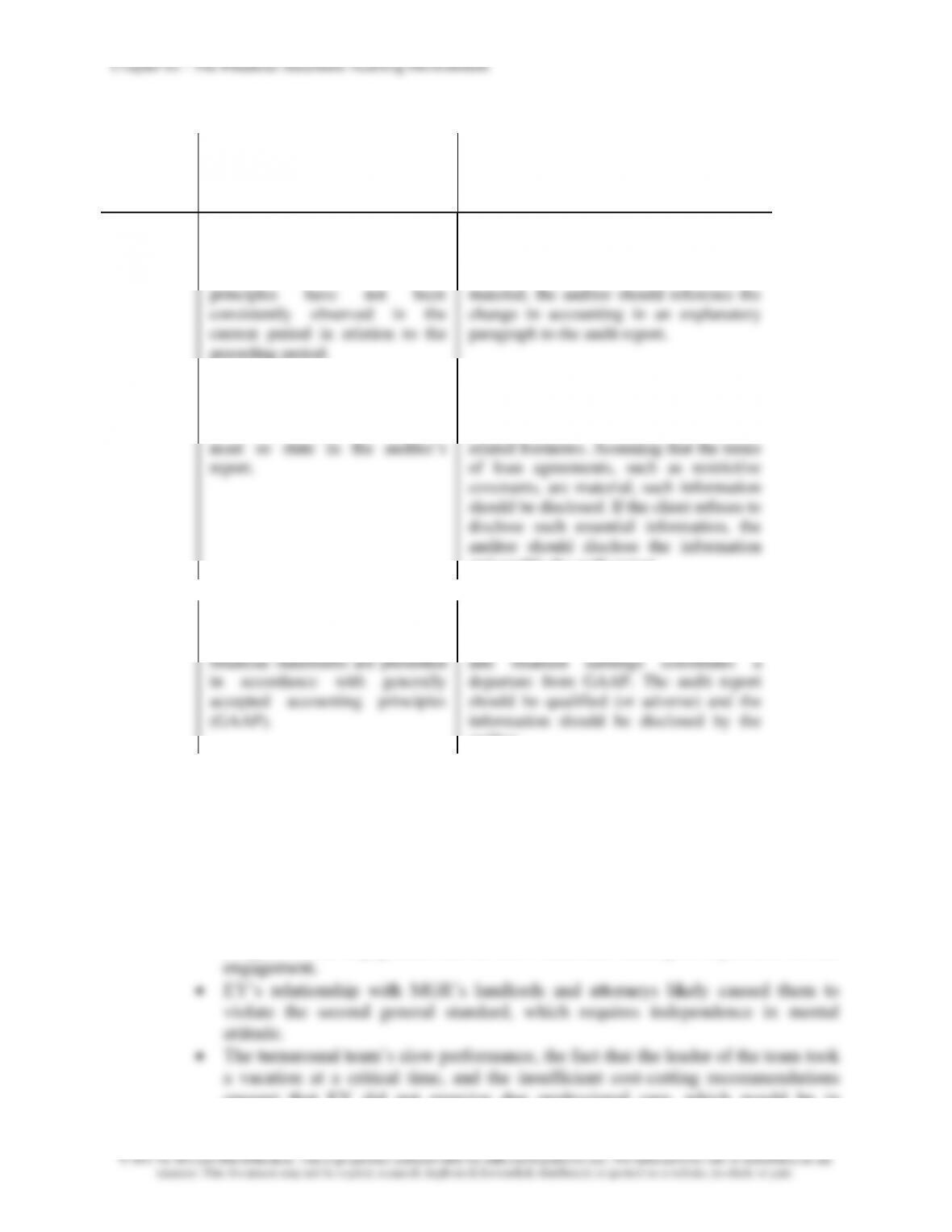

2-26

Situation

Applicable

GAAS of

Reporting

Discussion of Relationship

of Client Situation to

Standard of Reporting

a.

The auditor must identify in the

auditor’s report those

circumstances in which such

principles have not been

consistently observed in the

current period in relation to the

preceding period.

A change in accounting principle affects

the consistent application of the

accounting principle. If the change is

material, the auditor should reference the

change in accounting in an explanatory

paragraph to the audit report.

b.

When the auditor determines that

informative disclosures are not

reasonably adequate, the auditor

must so state in the auditor’s

report.

Information essential to a fair presentation

in conformity with GAAP must be

disclosed in the financial statements or the

related footnotes. Assuming that the terms

of loan agreements, such as restrictive

covenants, are material, such information

should be disclosed. If the client refuses to

disclose such essential information, the

auditor should disclose the information

and qualify the audit report.

c.

The auditor must state in the

auditor’s report whether the

financial statements are presented

in accordance with generally

accepted accounting principles

(GAAP).

The improper presentation of material

amounts of minority interest in net income

and retained earnings constitutes a

departure from GAAP. The audit report

should be qualified (or adverse) and the

information should be disclosed by the

auditor.

Solutions to Discussion Cases

2-27 Merry-Go-Round Part I.

a. EY is alleged to have violated all three general standards as well as one, and perhaps

two, of the standards of field work.

• They violated the first general standard in the sense that it appeared that the staff

assigned to the engagement did not have sufficient training or experience for the

Chapter 02 – The Financial Statement Auditing Environment

2-10

violation of the third general standard.

• Poor staff assignments, the leader’s vacation, and the use of inexperienced

an effective implementation strategy, which would be in violation of the third

standard of fieldwork.

b. EY is alleged to have violated the Principles of responsibilities and performance.

• They violated the Principle of responsibilities in the sense that it appeared that the

staff assigned to the engagement did not have sufficient training or experience for

assistants were not properly supervised, which violates the Principle of

performance. Also, the inadequate nature of EY’s recommendations suggests that

they likely did not gain a sufficient understanding of the entity and its operations.

c. There are arguments both for and against having formal standards for CPAs who

consult. Advantages include potential increase in public trust, some assurance that a

sense that CPAs would be subject to standards that constrain their activities or

perhaps result in their not being able to compete with non-CPAs in the area of fees.

Note that CPAs face certain restrictions in providing consulting services to audit

clients. These restrictions are covered in a later chapter.

2-28 Merry-Go-Round Part II.

a. In one sense, EY acted unethically. That is, it should have disclosed the nature of

these relationships to MGR. In another sense, it is difficult to ascertain whether these

relationships caused EY to act unethically. Specifically, was EY’s advice affected by

Chapter 02 – The Financial Statement Auditing Environment

2-11

losing business from Rouse. Its relationship with Swidler could have made EY feel

that it could not lose the engagement under any circumstances, thereby possibly

explaining its apparently lackadaisical attitude towards the engagement.

Solutions to Internet Assignments

2-29 A search of the GAO’s homepage will identify recent audits conducted by this agency.

2-30 a. According to its website, the AICPA’s mission is to “provide members with the

resources, information, and leadership that enable them to provide valuable services in

the highest professional manner to benefit the public as well as employers and clients.”

b. The SEC’s website states that its mission is “to protect investors, maintain fair, orderly,

attempt to restore confidence in the capital markets, Congress passed the Securities Act

of 1933. One year later, the SEC was created by the Securities Exchange Act of 1934.

d. The PCAOB’s website provides information on the Board’s organization, policies, and

standards. It also indicates that the Board uses an expert advisory group to help the Board

develop standards. Though many observers dispute this claim, the Board asserts that its

the Chief Auditor is responsible for developing these standards.

e. The International Auditing Practices Committee (IAPC) was founded in 1978. During

its first meeting, the group agreed to issue its publications as guidelines rather than

standards. The IAPC’s initial work focused on three areas: object and scope of audits of

financial statements, engagement letters, and general auditing guidelines. During this

Chapter 02 – The Financial Statement Auditing Environment

2-12

concern, and management representations.

Auditing, or ISAs, were born.

In 2001, IAPC was renamed as the International Auditing and Assurance Standards

Board (IAASB). The IAASB then embarked on its first joint project with a national

standard setter, the AICPA, which resulted in the development of the suite of audit risk

standards.

In 2003, IFAC approved a series of reforms designed to strengthen the IAASB’s

standard-setting processes so that it are properly responsible to the public interest. By

2007, the IAASB had become arguably the most transparent auditing standard setter in

the world.

To encourage greater use of its standards and facilitate translation, in 2004 the IAASB

launched a project designed to improve the clarity of its pronouncements. It revised its

drafting conventions to make the ISAs more readily understood. By the end of 2008, the

IAASB had approved all final redrafted auditing standards. The IAASB is currently

working on revising its standards for assurance engagements other than audits.

f. The IASB is the independent accounting standard-setting body of the IFRS Foundation.

The IASB is composed of 16 experts with an appropriate mix of recent practical

All meetings of the IASB are held in public and are broadcast through the internet. In

fulfilling its standard-setting duties, the IASB follows a thorough, open and transparent

process of which the publication of consultative documents, such as discussion papers

Chapter 02 – The Financial Statement Auditing Environment

2-13

and exposure drafts for public comment is an important component. The IASB engages

closely with stakeholders around the world, including investors, analysts, regulators,

business leaders, accounting standard-setters, and the accountancy profession.

The SEC has not yet reached a decision as to how, or even whether, the U.S. will adopt