Chapter 11 Auditing the Purchasing Process

11-1

CHAPTER 11

AUDITING THE PURCHASING PROCESS

Answers to Review Questions

11-1 Expenses can be classified into three categories:

1. Product costs are expenses that can be matched directly with specific transactions or

events and are recognized upon recognition of the revenues. An example of a product

and equipment is an example of such an expense.

11-2 The three types of transactions that are processed through the purchasing process are:

The more common accounts affected by each major type of transaction are:

Purchase transaction:

• Accounts payable

• Inventory

Purchase return transaction:

• Purchase returns

• Purchase allowances

Chapter 11 Auditing the Purchasing Process

11-2

11-3 A purchase requisition is a request for goods and services by an authorized individual or

department within the entity. A purchase order contains the description, quality, quantity,

and other information on the goods and services being purchased. A receiving report is

documents and information more easily.

11-4 The key segregation of duties and the errors or fraud that can occur if such duties are not

segregated are:

Segregation of Duties

Possible Errors or Fraud Resulting

from Conflicts of Duties

The purchasing function should be

segregated from the requisitioning and

receiving functions.

Theft of goods and possible payment for

unauthorized purchases.

The invoice-processing function should

be segregated from the accounts payable

function.

Overpayment for goods and services or

theft of cash.

The disbursement function should be

segregated from the accounts payable

function.

Theft of cash.

The accounts payable function should

be segregated from the general ledger

function.

A defalcation that would normally be

detected by reconciling subsidiary records

with the general ledger control account.

11-5 Two inherent risk factors that directly affect the purchasing process are (1) industry–

related factors, and (2) misstatements detected in prior audits.

If the entity deals with a large number of vendors and prices tend to be relatively stable,

there is less risk that the entity’s operations will be affected by raw-material shortages or

that production costs will be difficult to control. However, if an entity is dependent on a

11-3

11-6 The following controls and related tests are utilized to ensure that the occurrence,

authorization, and completeness assertions are met for purchase transactions:

Assertion

Control Activity

Tests of Controls

Occurrence

Segregation of duties

Purchase not recorded

without approved

purchase order and

receiving report

Accounting for numerical

sequences of receiving

reports and vouchers

Cancellation of documents

Observe and evaluate proper

segregation of duties.

Test of a sample of vouchers for

the presence of an authorized

purchase order and receiving

report; if IT application, examine

application controls.

Review and test entity procedures

for accounting for numerical

sequence of receiving reports and

vouchers; if IT application,

examine application controls.

Examine paid vouchers and

supporting documents for

indication of cancellation.

Authorization

Approval of acquisitions

consistent with the entity’s

authorization dollar limits

Approved purchase

requisition and purchase

order

Competitive bidding

procedures followed

Review entity’s dollar limits

authorization for acquisitions.

Examine purchase requisitions or

purchase orders for proper

approval; if IT is used for

automatic ordering, examination of

application controls.

Review entity’s competitive

bidding procedures.

Completeness

Accounting for numerical

sequences of purchase

orders, receiving reports,

and vouchers

to vendor invoices and

entered in purchases

journal

Review and test entity’s procedures

for accounting for numerical

sequence of purchase orders,

receiving report, and vouchers; if

IT application, examine

application controls.

to their respective vendor invoices

and vouchers.

Trace a sample of vouchers to the

purchases journal.

Chapter 11 Auditing the Purchasing Process

11-4

11-7 CAATs can be used to test numerous controls in the purchasing process. For example, a

generalized audit software package can be used to account for the numerical sequence of

purchase orders, receiving reports, and vouchers. Another example involves the use of a

11-8 The analytical procedures that can be used to test accounts payable and accrued expenses

and the possible misstatements that can be detected by each analytical procedure are:

Substantive Analytical Procedure

Possible Misstatement Detected

Compare payable turnover and days

outstanding in accounts payable with

previous years’ and industry data.

Compare current-year balances in accounts

payable and accruals with prior years’

balances.

Compare amounts owed to individual vendors

in the current year’s accounts payable

listing to amounts owed in prior years.

Compare purchase returns and allowances as a

percentage of revenue or cost of sales to

prior years’ and industry data.

Under- or overstatement of

liabilities and expenses

Under- or overstatement of

liabilities and expenses

Under- or overstatement of

liabilities and expenses

Under- or overstatement of

purchase returns

11-9 The following audit procedures may be used as part of the search for unrecorded

liabilities:

• Ask management about control activities used to identify unrecorded liabilities and

accruals at the end of an accounting period.

• Examine the files of unmatched purchase orders, receiving reports, and vendor

invoices for any unrecorded liabilities.

11-5

11-10 The following are examples of disclosures for the purchasing process and related

accounts:

• Payables by type (trade, officers, employee, affiliate, etc.).

• Costs by reportable segment of the business.

11-11 Accounts payable confirmations are generally used less frequently than accounts

receivable confirmations because the auditor can test accounts payable by examining

vendor invoices and monthly vendor statements. Since these documents originate from

Both positive and negative confirmations are used for accounts receivable. Lastly,

accounts payable confirmations are generally mailed at year-end rather than at an interim

date because of the auditor’s concerns about unrecorded liabilities. Accounts receivable

confirmations are sent at both dates.

11-12 Some of the typical procedures that might be applied to the audit of the tax provision by

the auditors and/or tax specialist include:

• Compare the size and trend in the tax provision and related balance sheet accounts

over time.

• Perform walkthroughs and test the design and operating effectiveness of internal

appropriate disclosure and accounting under ASC 740.

• Consider the realizability of net deferred tax assets and adequacy of related valuation

allowances.

• Test the reconciliation of income taxes payable, deferred income tax assets/liabilities

(including any related valuation allowances), and tax liabilities to supporting

Chapter 11 Auditing the Purchasing Process

11-6

documentation, including the general ledger, financial statements, and related footnote

disclosure.

• Ensure proper documentation in the audit working papers to allow for reperformance

of the audit procedures applied to the tax accounts.

Answers to Multiple-Choice Questions

11-13

c

11-19

c

11-14

c

11-20

d

11-15

b

11-21

c

11-16

d

11-22

c

11-17

b

11-23

a

11-18

b

Solutions to Problems

11-24 This is a relatively straightforward analytical procedures problem. Here are some of the

concerns the auditor might have about potential misstatements in both accounts:

• Both inventory and accounts payable have increased significantly in absolute dollar

terms from 2014 to 2015.

value and (2) there are unrecorded accounts payable. Other misstatements are

possible.

11-25 The internal control activities that most likely would provide reasonable assurance that

specific control objectives for management assertions regarding purchases and accounts

payable will be achieved are:

• The purchasing, receiving, and accounts payable functions are segregated.

Requisitioning Department:

Chapter 11 Auditing the Purchasing Process

11-7

• The adequacy of each vendor’s past record as a supplier is verified.

Receiving Department:

Accounts Payable Department:

• Requisitions, purchase orders, and receiving reports are matched with vendor invoices

as to quantity and price.

treasurer.

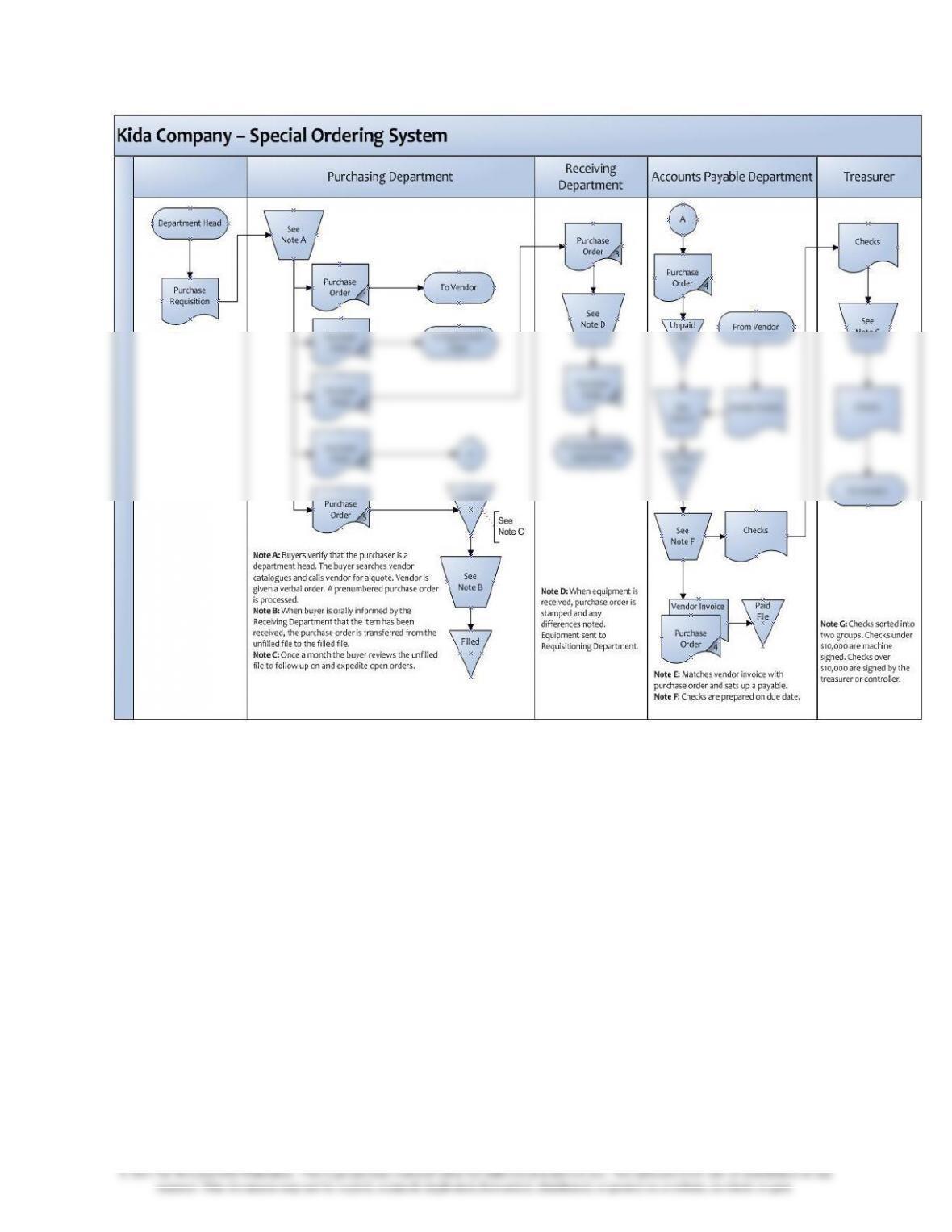

11-26 a. The flowchart for Kida Company is shown below:

Chapter 11 Auditing the Purchasing Process

11-8

Chapter 11 Auditing the Purchasing Process

11-9

b. Kida Company’s major internal control weaknesses are:

Purchasing:

• The buyer does not verify that the department head’s request is within budget

limitations.

Receiving:

• Receiving clerk does not make blind counts for all special equipment or at least for

large-dollar items.

department is not obtained before the payable is recorded.

• No alphabetic file of vendors from which purchases are made is maintained.

Treasurer:

• Documentation supporting the checks is not sent by the accounts payable

department to the cashier in order for the cashier or treasurer to be assured that the

check is for properly authorized and received equipment.

• The controller is authorized to sign checks.

11-27 1. Test of details of transactions (substantive test of transactions).

2. Tests of details of transactions (cutoff test).

11–10

11-28 The substantive audit procedures Coltrane should apply to Jang’s trade accounts payable

balances include the following:

• Foot the schedule of the trade accounts payable.

• Agree the total of the schedule to the general ledger trial balance.

payables.

• Perform cutoff tests.

• Perform analytical procedures.

Confirm or verify recorded accounts payable balances by:

• Reviewing the voucher register or subsidiary accounts payable ledger and consider

• Testing a sample of unconfirmed balances by examining the related vouchers,

invoices, purchase orders, and receiving reports.

Perform a search for unrecorded liabilities by:

• Examining files of receiving reports unmatched with vendors’ invoices and searching

• Inquiring of key employees about additional sources of unprocessed invoices or

other trade payables.

11-29 a. 3

Chapter 11 Auditing the Purchasing Process

11-30

a.

No adjustment is needed. The goods were received before December 31, 2015

and recorded in the Purchases Journal in December.

b.

An adjustment is required. The $45,000 payment covers a 3-month period

starting on December 1, 2015. The total amount was charged to consulting

expenses, while only 1 month of services was used by year-end. The entry to

correct is:

Prepaid Consulting Expenses 30,000

Consulting Expenses 30,000

c.

No adjustment is needed. The goods were received before December 31, 2015

and recorded in the Purchases Journal in December.

d.

No adjustment is needed. The truck was received in 2016 as evidenced by RR#

49746 and recorded in the Purchases Journal in January.

e.

An adjustment is required. The paper products were received in December

2015 as evidenced by the RR# 49743 (RR #49745 is the last receiving report in

December). Thus, these goods should have been recorded in December 2015. The

entry to correct is:

Supplies 42,000

Accounts Payable 42,000

f.

An adjustment is required. The telephone bill applies to December 2015 and the

$32,450 should be an accrued expense. The entry to correct is:

Telephone expense 32,450

Accrued Expenses 32,450

Solution to Discussion Case

11-31 a. The accounts payable audit procedures should be directed toward searching for

proper inclusion of all accounts payable and ascertaining that recorded amounts are

reasonably stated because the primary audit purpose is to reveal any possible

material understatements.

The principal objectives of the accounts payable examination are:

1. To determine adequacy of internal control for processing and payment of

Chapter 11 Auditing the Purchasing Process

11–12

b. Mincin is not required to use accounts payable confirmation procedures. The auditor,

with three exceptions, is required to obtain direct confirmation of accounts

receivable, since the primary audit test is for possible material overstatements and

generally the entity has available only internal documents such as sales invoices. For

accounts payable, however, the auditor can examine external evidence such as

vendor invoices and vendor statements that substantiate the accounts payable

balance. Although not required, the accounts payable confirmation is often used. The

auditor might consider such use when:

1. Internal controls are weak.

7. Change in personnel or management behavior related to payables.

c. A selection technique using the large dollar balances of accounts is generally used

when the primary audit objective is to test for overstatements (e.g., accounts

receivable audit work). Accounts with zero balances or relatively small balances

would not be subjected to selection under such an approach. When auditing accounts

payable, the auditor is primarily concerned with the possibility of unrecorded

payables or understatement of recorded payables. Selection of accounts with

relatively small or no balances for confirmation is the more efficient direction of

testing, since understatements are more likely to be detected when examining such

accounts.

When selecting accounts payable for confirmation, the following procedures

could be followed:

1. Analyze the accounts payable population and stratify it into accounts with large

balances, accounts with small balances, accounts with zero balances, etc.

2. Use a sampling technique that selects items based on criteria other than the dollar

8. Select accounts secured by pledged assets.

Chapter 11 Auditing the Purchasing Process

11–13

© 2017 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any

manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part.

Solution to Internet Assignments

11-32 It may be difficult to get information directly on some of EarthWear’s competitors.

Lands’ End and Timberland are publicly traded companies. Eddie Bauer, L.L. Bean and

11-33 A search of the SEC’s website should identify a recent company that has been cited by