Case 8 Teaching Note Cooper Tire & Rubber Company in 2014

377

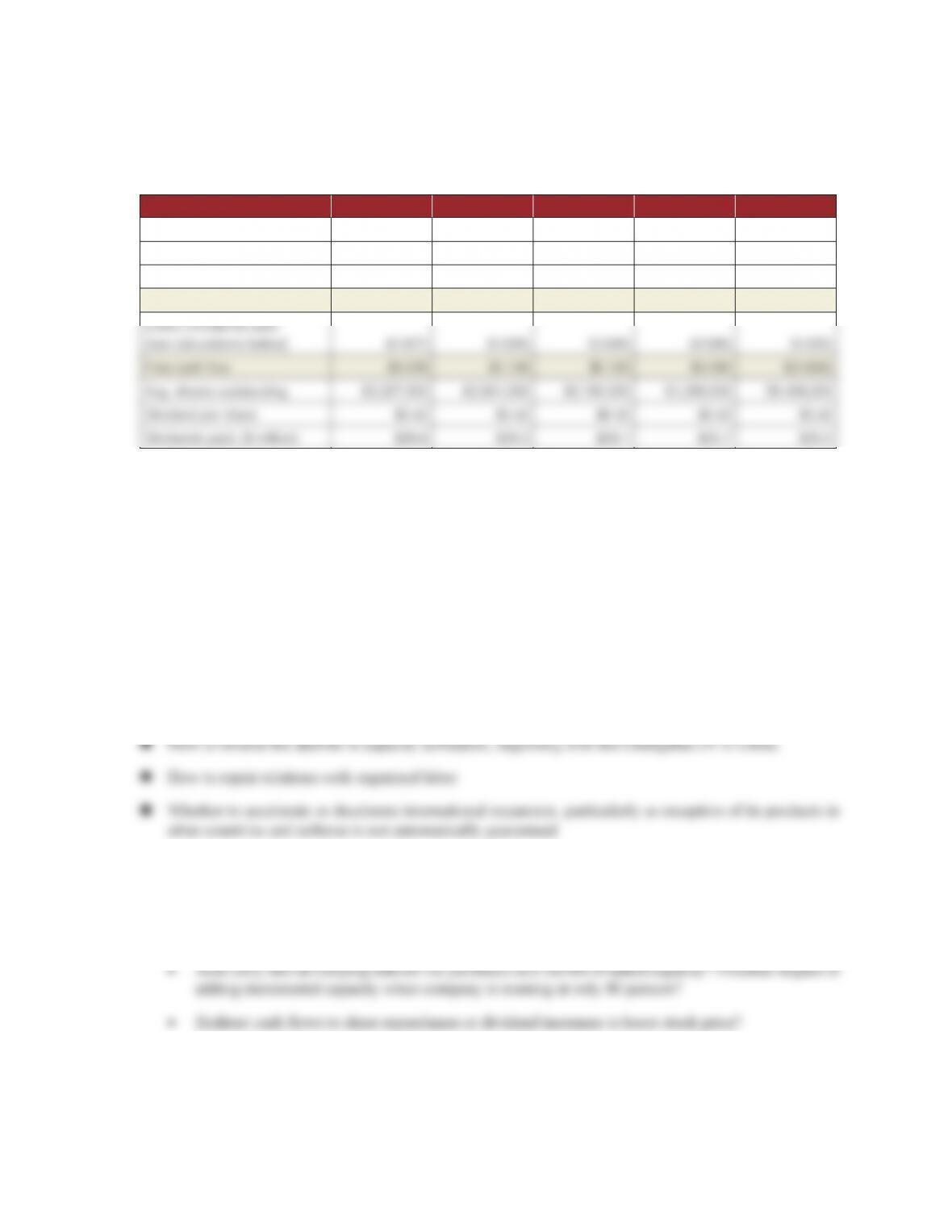

TABLE 8. Calculation of Cash Flows and Free Cash Flows

for Cooper Tire & Rubber Co.

2009–2013 ($ billions except where noted)

2013 2012 2011 2010 2009

Net income $0.111 $0.220 $0.254 $0.116 $0.089

Non-cash: Deprec. & amort. 0.135 0.129 0.123 0.124 0.124

(Less:) Capital expenditures (0.180) (0.187) (0.155) (0.120) (0.793)

Cash flow 0.065 0.162 0.221 0.120 (0.581)

Source: data in case Exhibit 1

7. What 3–4 top priority issues do CEO Roy Armes and Cooper Tire management need to

address?

We think it is always a good idea to push the class for their assessment of what issues management needs

to address before proceeding to ask for action recommendations. Issue identification (or compilation of a

“what I’d do if I were in her/his shoes” list) is a way for students to draw conclusions from all the preceding

analyses, plus it sets the stage for what actions need to be taken.

In Cooper Tire’s case, we see several high-priority issues meriting priority consideration:

n How best to put the failed merger in the “rear view mirror,” re-position Cooper Tires for long-term

growth, and rejuvenate interest and sales

n Where to direct future capital investment given strong cash ows, cash position, and unused debt

capacity

• Build on lucrative sales to the OEM markets (having begun with two Ford models)? Potential

impact of taking this action on current relationships with independent dealers worldwide?

Case 8 Teaching Note Cooper Tire & Rubber Company in 2014

378

8. What recommendations would you make to Cooper Tire CEO Roy Armes? At a minimum,

your recommendations should cover what to do about each of the top priority issues

identified in question 7.

n Forget about striving for market share (which drove the merger attempt with Apollo Tyres), and instead

make the focus a return to profitable growth

n Move upscale and continue introduction of premium tires emphasizing product differentiation

attributes—quality, performance, and safety

n Continue monitoring costs via:

• tight controls over capital spending,

• restructuring the organization,

9. [Optional question for adopters wishing to pair this case with materials in Chapter

6] How have Cooper Tire’s business strategy choices strengthened or weakened its

competitive position in the automotive tire industry? That is, what are the benefits and

drawbacks of the approaches taken to increasing Cooper Tire’s global scope?

Cooper Tire’s ability to achieving and sustaining a competitive advantage in the replacement segment of the

fiercely competitive automotive tire industry may well be confounded by the following factors:

n Chronic industry overcapacity, which has driven the wave of cross-border consolidation via acquisitions

by the largest producers

n Highly fragmented industry below the “top tier”—1,000 producers

n Prohibitive transportation costs—exacerbated if the points of sale are distant from the point of

manufacture

Case 8 Teaching Note Cooper Tire & Rubber Company in 2014

379

n Ease of buyers (independent dealers and vehicle owners) switching from one producer to another—

competition is based on price; most successful brands have a high price/performance ratio.

These are mitigated somewhat by the following factors:

n Industry maturity, exacerbated by unfavorable economic cycles for capital equipment

n Technological advances in production such as automation, robotics, ERP, GIS, and wireless technology

will in future not only lower costs of production and after-market service, but also lengthen product

lives, limiting replacement sales

n Lack of available mechanized substitutes that perform the same functions

On balance, due to the above factors, to achieve a competitive advantage, a producer of automotive tires

must compete via achieving economies of both scale (vertically) and scope (horizontally).

Vertical scale refers to the ability of a firm like Cooper Tire to capture higher value added across activities

such as investing in research and development (R&D) to improve product innovation and design; investing

Horizontal scope refers to the range of product and service segments that a firm like Deere serves within its

focal market, which is considerable due to its presence in nearly every sector of agricultural and construction

machinery. Increasing a company’s horizontal scope can strengthen its business and increase its profitability

Case 8 Teaching Note Cooper Tire & Rubber Company in 2014

380

TABLE 9. Appraising Cooper Tire & Rubber Company’s Horizontal

Diversification Strategies

Strategic intent Plusses Minuses

Leverage global scale economies to

improve efficiency

Reduced transport costs, increased

effectiveness of dealerships &

aftermarket support, retailing-

financing division accounts for >90%

of sales across 40 countries

Highly dependent on favorable

balances of trade, weak U.S. dollar,

government subsidies & interest

rates

Heighten product differentiation via

Integrity & quality

Fundamental to strategy & to protect

global market leadership position

Unclear if culture & values will be

shared & implemented by operators

of manufacturing facilities in

emerging markets such as China,

Mexico, and Serbia

10. [Optional question for adopters wishing to pair this case with materials in Chapter

7] Is Cooper Tire’s international strategy best characterized as a multi-domestic

strategy, global strategy, or transnational strategy? What are the pros and cons of each

approach?

Any business contemplating globalization must make decisions regarding:

n The need to balance the cost of doing so with the multi-brand and multi-positioning (differentiation)

sides of its business model,

n The need to be responsive to local market vs. global market characteristics

Case 8 Teaching Note Cooper Tire & Rubber Company in 2014

381

Students should be directed to carefully review Figure 7.2 in the text:

n An international/global strategy is a strategy for competing in two or more countries simultaneously.

n A multi-domestic strategy is one in which a company varies its product offering and competitive

n A transnational strategy (sometimes called “glocalization”) incorporates elements of both a globalized

and a localized approach to strategy making.

TABLE 10. Globalization Strategies of Key Rivals in Agriculture &

Construction Equipment

Strategy/

Company (HQ)

Potential

Advantages Potential Disadvantages Challenges for Rival

Multi-domestic

Bridgestone

(JP)

Groupe Michelin, (FR)

+

Ability to customize

product offerings and

marketing in accordance

with local responsiveness

–

Inability to realize location

economies

–

Failure to exploit

experience-curve effects

–

Failure to transfer

distinctive competencies

to foreign markets

?

JV and alliances meet

needs for localization in

emerging markets but do

not address need for cost

reductions

Global/International

+

Transfer of distinctive

competencies to foreign

–

Lack of local

responsiveness

?

Continuously driven

by pressures for cost

Case 8 Teaching Note Cooper Tire & Rubber Company in 2014

382

Superior students should weigh the advantages and disadvantages of various strategies (international/global,

The appropriateness of those strategies varies from industry to industry, depending upon the extent of pressures

for cost reductions and local responsiveness. International and global strategies tend to be least appropriate

Students should be reminded that building an organization capable of supporting a transnational strategy is

a complex and challenging task: implementation problems are often associated with creating the requisite

Epilogue

According to an August 7, 2014 report in the Wall Street Journal, Cooper Tire said its second-quarter profit

climbed 7.6% as the company benefited from strong increases in volume across most regions and a decline in

some expenses. The company’s revenue far outpaced analysts’ expectations.

“We continued our strong performance in what is usually a seasonally weak quarter, posting very good volume

growth in most geographic regions,” Chief Executive Roy Armes said. He added the lower raw material costs

results in decreased pricing, but the company experienced global unit growth of 10%.

Separately, the company also unveiled an accelerated share repurchase program with J.P. Morgan Chase Bank.

Under the agreement, Cooper said it would buy back $200 million of its shares, and will receive about 5.6

million shares at the beginning of the program.

In May 2014, Cooper Tire said it was aiming for annual net sales of $5 billion to $6 billion in the long term,

though the future ownership of its Chinese joint venture may affect some of the details of how and when it will

reach its goals.

In January, Ohio-based Cooper Tire reached an agreement with the joint venture and its labor union to begin the

process to determine whether Cooper Tire or Chengshan Group Company Ltd. will take control of the venture.

The Chinese venture was a hurdle in Cooper Tire’s failed sale to Indian suitor Apollo Tyres Ltd. last year. In

December 2013, Cooper Tire officially terminated its sale to Apollo after months of delay during which Apollo

sought to reduce the price.

During the second quarter of 2014, net sales from Cooper Tire’s international tire operations slid 8% to $327

million, despite higher unit volume in Asia and Western Europe, which was offset in part by weakness in Russia

and Eastern Europe .North America tire operations net sales rose 3% to $639 million, as shipments jumped 9%

year-over-year. Overall, Cooper Tire posted a profit of $38.2 million, or 59 cents a share, up from $35.5 million,

or 55 cents a share, a year earlier. Selling, general and administrative expenses fell 12% to $71.3 million. Net

sales ticked up 0.5% to $888.7 million. Analysts surveyed by Thomson Reuters had projected revenue of $863

million a share. Raw material prices fell 1% during the second quarter, and Cooper Tire expected them to be at

during the third quarter of fiscal 2014.

On August 23, 2014, the Wall Street Journal reported that Cooper Tire had unveiled the valuation of its joint

venture with Chengshan Group Company Ltd., marking a step forward as the companies seek to resolve its

future ownership. The venture, known as Cooper Chengshan Tire Company Ltd., was valued at about $440

million by an independent firm responsible for determining a fair market value for the venture on a stand-alone

basis, Cooper Tire said.

Case 8 Teaching Note Cooper Tire & Rubber Company in 2014

383

“We look forward to final resolution of the ownership of CCT as Cooper Tire continues to pursue our growth

plans for China,” said Cooper Tire Chief Executive and Chairman Roy Armes.

The venture’s facility in Rongcheng, China, was a source of contention in Cooper Tire’s failed $2.2 billion

merger with Indian suitor Apollo Tyres Ltd. The merger fell apart in December after the factory in eastern China

revolted, with workers going on strike soon after the merger was originally announced in June.

With the valuation of the venture, Chengshan now has 45 days to decide to purchase Cooper Tire’s 65% interest

or opt to sell its own 35% interest to Cooper Tire. If it doesn’t move on either option, Cooper Tire has said it

had the right to purchase Chengshan’s 35% interest. In the event that neither company makes a move, the joint

venture will continue as currently structured, Cooper Tire has said. Even if Chengshan did buy its stake in the

joint venture, Cooper Tire has said CCT still would produce Cooper Tire-brand products for a minimum of three

years.

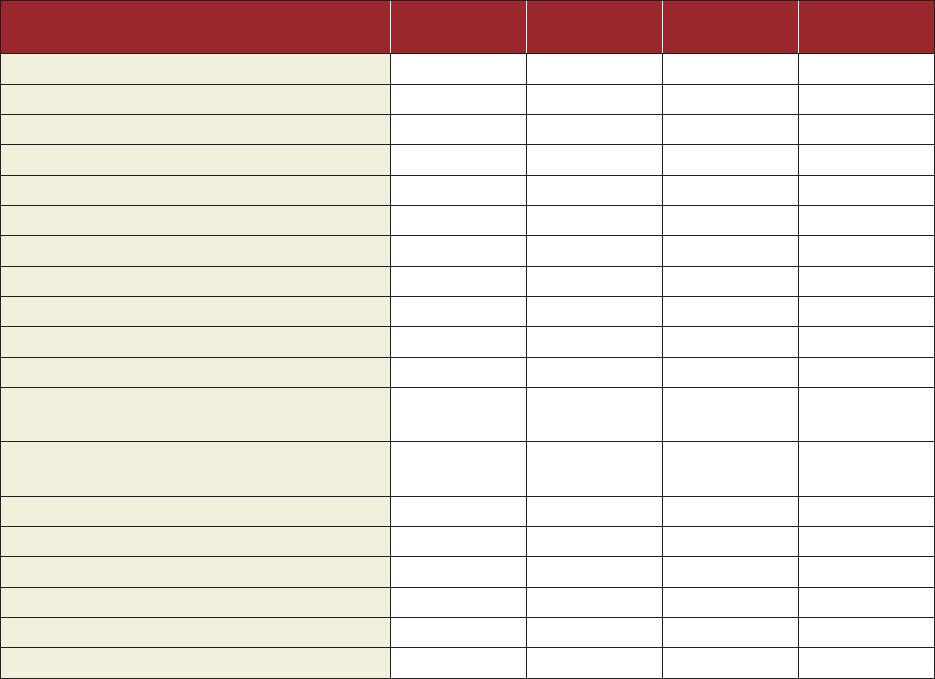

Table 11 presents a Financial Summary for Cooper Tire & Rubber Company for the first six months of 2014

compared to the first six months of 2013.

TABLE 11. Financial Summary for Cooper Tire & Rubber Company

First Six Months 2013 and First Six Months 2014

All figures in $000 except per share data

06/30/2014

2nd Quarter

06/30/2013

2nd Quarter

03/31/2014

1st Quarter

03/31/2013

1st Quarter

Net sales $888,685 $884,126 $796,458 $861,681

Cost of products sold 740,816 733,966 649,116 703,763

Gross profit (loss) 147,869 150,160 147,342 157,918

Selling, general & administrative expense 71,280 80,994 66,431 61,254

Operating profit (loss) 76,589 69,166 80,911 96,664

Interest expense 6,792 7,231 7,118 7,101

Interest income 270 141 513 296

Other income (expense) 477 -834 -11 595

Income (loss) before income taxes 70,544 61,242 74,295 90,454

Income tax expense (benefit) 25,786 19,642 22,567 27,617

Net income (loss) 44,758 41,600 51,728 62,837

Net loss (income) attributable to noncontrolling

interests -6,576 -6,114 -6,294 -6,757

Net income (loss) attributable to Cooper Tire &

Rubber Company 38,182 35,486 45,434 56,080

Weighted average shares outstanding—basic 63,537 63,342 63,399 63,226

Weighted average shares outstanding—diluted 64,481 64,142 64,338 64,184

Year end shares outstanding 63,594 63,313 63,457 63,313

Net income (loss) per share—basic $0.60 $0.56 $0.72 $0.89

Net income (loss) per share—diluted $0.59 $0.55 $0.71 $0.87

Dividends per share $0.11 $0.11 $0.11 $0.11