Case 7 Teaching Note Lagunitas Brewing Company, Inc.: 2013

355

Craft beer segment attractiveness: High

As is clear from the above, the craft beer segment is becoming far more competitive and the competition is

itself more localized than the wider beer market. The obvious question for LBC is whether there is a market

“sweet spot” between being a localized craft beer and the national big players, or if it is en route to becoming

3. How would you characterize Magee’s generic competitive strategy for the Lagunitas

brand? How well is this strategy working?

Coverage of generic strategies is in Chapter 5.

The generic competitive strategy of Lagunitas is integrated cost/focused differentiation.

From the beginning Magee has worked hard to minimize costs—from doing everything himself initially to

the introduction of technology to lessen costs and, finally, to the development of the Chicago brewery for

Resource Strengths and Competitive Capabilities

nDedicated leadership

n LBC brand strength

n Quality control

Resource Deficiencies and Competitive Liabilities

n Reliance on founder for direction

n Limited product offerings nationwide

External Market Opportunities

n Rapidly growing market for craft beers

n Promotions during special events

Case 7 Teaching Note Lagunitas Brewing Company, Inc.: 2013

356

External Threats to Lagunitas Brewing’s Future Well-Being

n Proliferation of new entrants into craft beer segment

n Environmental concerns regarding wastewater

LBC’s differentiation has been critical to its success to date. As is quoted in the case—it is what is in the

The big change that is occurring in the craft beer/microbrewing segment is the broadening of the strategy on

4. What is your assessment of LBC’s performance relative to its peers? What does a

strategic group map of the brewing industry reveal? Has LBC been successful?

You should expect class members to use some of the financial ratios in Table 4.1 of Chapter 4 in performing

calculations to determine what aspects of LBC’s financial performance might qualify as impressive. As the

company is closely-held, there is not sufficient information to permit calculation of all ratios. Students will

Students should observe that:

nThe massive growth figures for LBC relative to the industry or even the craft brewing segment would

nLBC’s ales revenues have been growing at a compound annual growth rate (CAGR) of 52% over the

nThat growth—and the fact that LBC holds a market share position as sixth largest craft brewer in the

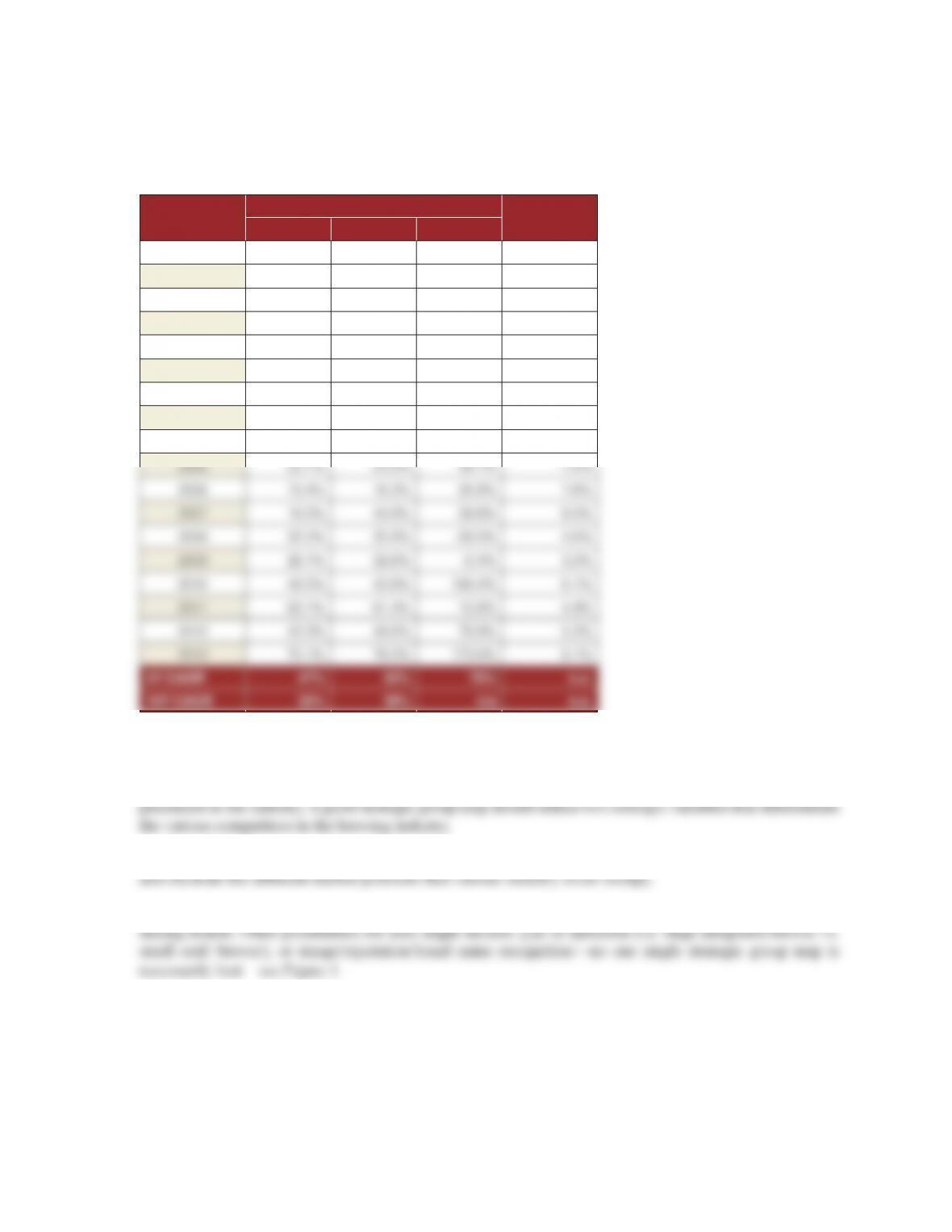

Table 2 presents calculations of LBC’s annual (year-on-year) growth rates in capacity, sales revenues, net

Case 7 Teaching Note Lagunitas Brewing Company, Inc.: 2013

357

TABLE 2. Selected Performance Data for Lagunitas Brewing Co.,

1996–2013

(Data prior to 1996 were not available)

Year

—Year on Year Growth, %— Return

on Sales, %Capacity Sales Profits

1996 58.5% 58.5% n.a. n.a.

1997 55.4% 55.4% n.a. n.a.

1998 23.8% 27.9% n.a. n.a.

1999 38.4% 41.1% n.a. n.a.

2000 20.8% 22.3% n.a. n.a.

2001 11.5% 13.6% n.a. n.a.

2002 20.6% 22.8% n.a. n.a.

2003 4.3% 6.8% n.a. n.a.

2004 8.2% 9.5% n.a. 5.9%

Calculated from case Exhibit 4.

Students should also be able to prepare a strategic group map of the U.S. beer industry as a component

of Lagunitas’ competitive strength. Strategic group maps are beneficial for determining relative company

Students can choose among any of several strategic variables to divide the beer industry into strategic groups

We have chosen to employ geographic scope (in distribution) and the degree of product differentiation

Case 7 Teaching Note Lagunitas Brewing Company, Inc.: 2013

358

FIGURE 1. Strategic Group Map of the U.S. Beer Industry

High

DIFFERENTIATION

DISTRIBUTION

Low

National

Global

Local

A-B

(InBev)

SAB Miller

Molson/Coors

Craft

brewers

LBC &

micros

Boston

Beer

Based on the strategic group map above, one can see that LBC is not alone in its segment and faces stiff

competition from Boston Beer, and to a lesser extent, from rivals in the craft beer segment.

5. What recommendations would you make concerning expansion and the construction

of the new brewery? How will Magee ensure consistency of the Lagunitas brand across

multiple breweries?

nLBC needs to go to significant lengths to make sure that the beer brewed in Chicago tastes exactly like

the beer brewed in Petaluma by ensuring that the water used is consistent in profile.

n This, along with the head brewer at least initially commuting between the breweries to oversee

production, should ensure product consistency.

Case 7 Teaching Note Lagunitas Brewing Company, Inc.: 2013

359

6. What are the risks that Magee faces in expanding the brand away from a craft orientation

toward ‘playing against the largest breweries’ on a national scale?

The principal danger for LBC is potential damage to the brand and culture of the business as it grows

exponentially outside of its “home territory” in Petaluma, CA.

As LBC seemingly has lesser aspirations about craft beer and more about becoming a major national brewer,

there is a danger that it will come to look increasingly similar to those large corporate brewers that are mass-

market companies. That is, shift from a focused differentiation to a broad (mass-market) differentiation

nThe rise of craft beer can to some extent be seen as a market reaction against large corporate beer makers

nThe LBC brand has traditionally been seen as somewhat “counter-culture” (in that it originated in

However, it is important to remember the scale that is being dealt with by LBC. Chicago would be a second

site.

nLBC’s capacity in 2012 was just over 1/10th of the largest craft brewing company (Boston) as seen in

case exhibit 5.

nEven with Chicago operating at maximum capacity, LBC would be a long way (in terms of size) from

Wrapping up the case: Most all of the front-burner issues at LBC relate to the inextricable linkage between

external market pressures to continue rapid growth while using sourcing and quality control functions to rein in

Epilogue

With a $25 million, 300,000 square-foot brewery expansion in Chicago set to open in December 2013, Lagunitas

became a case-study in the surging popularity, although the brewery “is far from alone,” said Tony Magee,

founder of the brewery who spoke at the November 12, 2013 North Bay Beer, Cider, and Spirits conference, as

reported by the North Bay Business Journal on November 18, 2013.

“Lagunitas and other craft breweries will be the next Anheuser,” Mr. Magee said, referring to the giant InBev-

owned Anheuser-Busch that currently dominates the beer market.

“It’s really something bigger than Lagunitas,” he added, noting that the beer giants have been forced to compete

with craft brews by either acquiring established brands like Blue Moon or Shock Top or making variations to

appeal to consumers increasingly attracted to a different style of beer.

Case 7 Teaching Note Lagunitas Brewing Company, Inc.: 2013

360

Tony Magee is chief executive officer and president of Lagunitas Brewing Co., which he founded in 1993 in west

Marin County. It has since grown into the largest brewery in the North Bay and the sixth-largest craft brewery in

the U.S. in sales volume, according to the Brewers Association. The company produced 265,420 barrels of beer

in 2012. Mr. Magee, a Chicago native, brewed his first home batch in January 1993, and Lagunitas brewed its

first in December that same year. Before brewing, Mr. Magee studied music composition and worked in sales,

ranging from luggage to commercial printing. “I graduated from high school in the bottom one-fourth of my

class and later dropped out of college after four years when they told me I had three years left to go,” he said.

His favorite beer: “Lagunitas IPA, of course, with Anchor Steam a close second.”

According to a later February 10, 2014 report in in the North Bay Business Journal, Sonoma County, California,

where LBC is based, now had 21 craft breweries, which together with cider-makers and distilleries added $123

million to the county’s economy in 2012, according to a recently released map by the Sonoma County Economic

Development Board and a groundbreaking study of the sector released last year. Three of those breweries have

opened since June, with indication that yet more were in the works.

Demand for those high-end brews had so far left plenty of room for new entrants to the marketplace in California,

the largest producer of craft beer in the country. Over 300 new breweries opened in 2012, contributing to a 20

percent increase in production volume state-wide, according to the most recent data from the nonprofit California

Craft Brewers Association.

Locally made hard ciders and craft bourbons and gins were similarly gaining a strong foothold in the craft

market, panelists said, similarly capitalizing on Sonoma County’s love for all things made local—as long as it’s

good.

“There’s a high level of gastronomic appreciation,” said Ron Lindenbusch of Lagunitas.

David Cordtz, who founded Sonoma Cider in Healdsburg in 2013, said he and others are looking to emulate the

success of the county’s breweries. “We hope to take a page out of the craft beer industry,” he said.

Banks and other financiers also increasingly saw value in a well-made craft beer or spirit, pumping more capital

into a business that once seemed fringe and disparate. Similarly, financial backers weren’t too concerned about

market saturation, considering the size of the beer market, at $100 billion.

According to a report from Frank, Rimmerman + Co., CPAs, traditional brands such as Budweiser “are

experiencing massive volume declines, creating opportunities for craft beer (and wine) to increase market share

as consumers seek more avorful alternatives.”

“Most breweries are asset-rich,” said Brian Mulvaney, senior banker with Bank of America Merrill Lynch,

noting that brewery tanks and other expensive equipment are viewed as attractive collateral given the demand

for craft beer.

Richard Norgrove, owner and president of Healdsburg-based Bear Republic, which was started in 1995, agreed

that the market was increasingly favorable, both in terms of demand and available capital.

“The market will expand,” Mr. Norgrove said. “But you still need to make a great product.”