Case 6 Teaching Note lululemon athletica, Inc., in 2014

338

3. What do you see as the key success factors in the market for performance-based yoga

and fitness apparel?

Class members who have done some good strategic analysis and thinking should be able to make a convincing

argument for why one or more of the following qualify as being key success factors in the marketplace for

nGood product design and styling capabilities—competitors will have to stay on the cutting edge in

using high-tech moisture-wicking performance fabrics that are of good quality, that are comfortable

nStrong distribution capabilities—having good access to the buyers of performance sports apparel

is a must. This can mean having a sizable chain of company-owned retail stores or selling through

nCapabilities in building and maintaining a strong brand image and reputation—many buyers of such

nCapabilities to increase geographic coverage—being a market leader in performance-based yoga and

4. What does a SWOT analysis reveal about the overall attractiveness of lululemon’s

situation?

lululemon’s Resource Strengths and Competitive Assets

nThe company’s lineup of stylish, premium-priced yoga and fitness apparel that offers performance, fit,

and comfort

nA contingent of fitness-conscious women who view lululemon products as “must have”

nA core competence in designing stylish, appealing yoga and fitness apparel items (although there is

some reason to wonder if this core competence has not eroded rather than strengthened in the past year

or so)

Case 6 Teaching Note lululemon athletica, Inc., in 2014

339

lululemon’s Resource Weaknesses and Competitive Liabilities

nEntrenched founder—Chip Wilson—who has problems with the media and who cannot let go of a

strategy

nRecent managerial turmoil and turnover and loss of faith among key stakeholders

nSupply chain management and quality control has recently been exposed as flawed in recent months

lululemon’s Market Opportunities

nOpening lululemon athletic stores in more geographic areas and in more countries

nGrowing sales at the company’s website

The External Threats to lululemon’s Future Well-Being

nDamage control and efforts to improve both design function and supply chain prove to be of little

consequence in the marketplace; important stakeholders are not mollified

nInvestors continue lackluster confidence in LULU stock, resulting in further price drops or share price

stagnation

Conclusions regarding the attractiveness of lululemon’s overall situation:

lululemon’s overall situation is unattractive, at least for the time being. Formerly, lululemon was an up-and-

coming company with potent resource strengths that were producing gains in sales and good profitability. It

had made a name for itself and developed a loyal clientele of enthusiastic customers. It had a differentiated

Case 6 Teaching Note lululemon athletica, Inc., in 2014

340

Competitor pressure is intensifying from both new entrants and incumbents. Absent needed focus on the

On balance, lululemon’s future outlook for growth and profitability seems bright—unless the new

5. What are the primary components of lululemon’s value chain?

Four primary value chain components stand out:

1. Product design and styling

2. Supply chain management

• handling the outsourcing of production to contract manufacturers and

6. What are the key elements of lululemon’s strategy?

Class members should be expected to identify the following key elements of lululemon’s strategy:

nGrow the store base in North America, primarily the United States.

nOpen additional stores outside of North America (Australia / New Zealand, Asia, and Europe)

nIncrease awareness of the lululemon brand and apparel line via showrooms and e-commerce marketing

channels

nIncorporate next-generation fabrics and technologies in the company’s products to strengthen consumer

association of the lululemon brand with technically-advanced apparel products and enable lululemon

Case 6 Teaching Note lululemon athletica, Inc., in 2014

341

nMarket lululemon products to select yoga studios, health clubs and fitness centers as a way to gain the

implicit endorsement of local fitness instructors and personnel for lululemon branded apparel, familiarize

the customers of these establishments with the lululemon brand, and give them an opportunity to

conveniently purchase lululemon apparel

nUse contract manufacturers to produce lululemon products.

nMaintain limited store inventories of most lululemon apparel items (so as to never have to put unsold

nThe company’s goal was to sell all of its products at full price

nSpecial colors and seasonal items were in stores for only a limited time—such products were on three,

six, or 12-week life cycles so that frequent shoppers could always find something new. Store inventories

If you have previously covered the Under Armour case, this may be the perfect time to ask the class to

compare and contrast lululemon’s strategy with that of Under Armour.

The answer, of course, is that lululemon’s primary distribution channel is its chain of company-owned and

-operated retail stores, while Under Armour’s primary distribution channel is selling to third-party retailers

There are a couple of other significant strategy differences:

nUnder Armour’s strategy includes an initiative to rapidly grow its presence in more and more countries

nUnder Armour makes significant use of celebrity endorsements and sponsorship of sporting events to

By contrast:

nlululemon recruits local yoga and fitness instructors to be ambassadors of the lululemon brand—

nThis brings into question luluemon’s strategy to broaden its product line into competitive sports such

7. Which one of the five generic competitive strategies discussed in Chapter 5 most

closely approximates the competitive approach that lululemon is employing?

We think lululemon’s strategy is drifting from a focused to a broad differentiation strategy. The company’s

strategy to move to a broader product line signals its intent to transition to a broad differentiation strategy.

Case 6 Teaching Note lululemon athletica, Inc., in 2014

342

8. What do the data in case Exhibit 1 reveal about lululemon’s financial and operating

performance?

You should expect students to use the financial ratios in Table 4.1 of Chapter 4 in performing calculations

to determine which aspects of lululemon’s financial performance might be characterized as impressive,

improving, or not. In addition to the ratios in Table 4.1, students will also need to calculate compound average

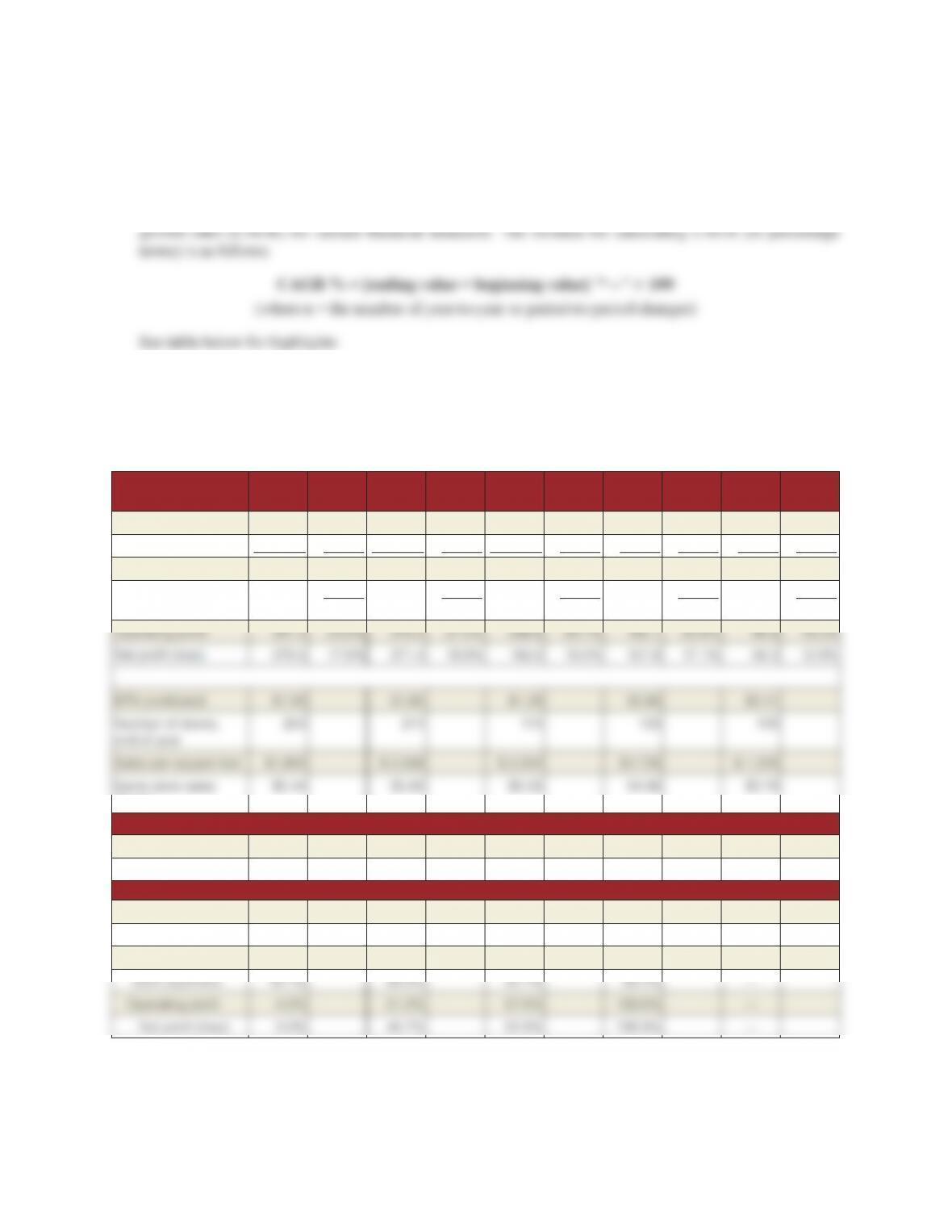

Financial Assessment Statistics and Financial Ratios for

lululemon athletica, Inc., Fiscal Years 2009-2013

(all amounts in $ millions except EPS)

Income statements 2013

% of

Total 2012

% of

Total 2011

% of

Total 2010

% of

Total 2009

% of

Total

Net revenues $1,591.2 100.0% $1,370.4 100.0% $1,000.8 100.0% $711.7 100.0% $452.9 100.0%

Cost of Goods sold 751.1 47.2% 607.5 44.3% 431.6 43.1% 316.8 44.5% 229.8 50.7%

Gross profit 840.1 52.8% 762.9 55.7% 569.2 56.9% 394.9 55.5% 223.1 49.3%

Selling, general, and

admin expenses

448.7 28.2% 386.4 28.2% 282.3 28.2% 212.8 29.9% 136.2 30.1%

($ mil.)

4-Year CAGR%

Net Revenues 36.9%

Net Profit 48.0%

Percentage Growth, Year-over-Year

Net revenues 16.1% 36.9% 40.6% 57.1% —

Cost of Goods sold 23.6% 40.8% 36.2% 37.9% —

Gross profit 10.1% 34.0% 44.1% 77.0% —

Case 6 Teaching Note lululemon athletica, Inc., in 2014

343

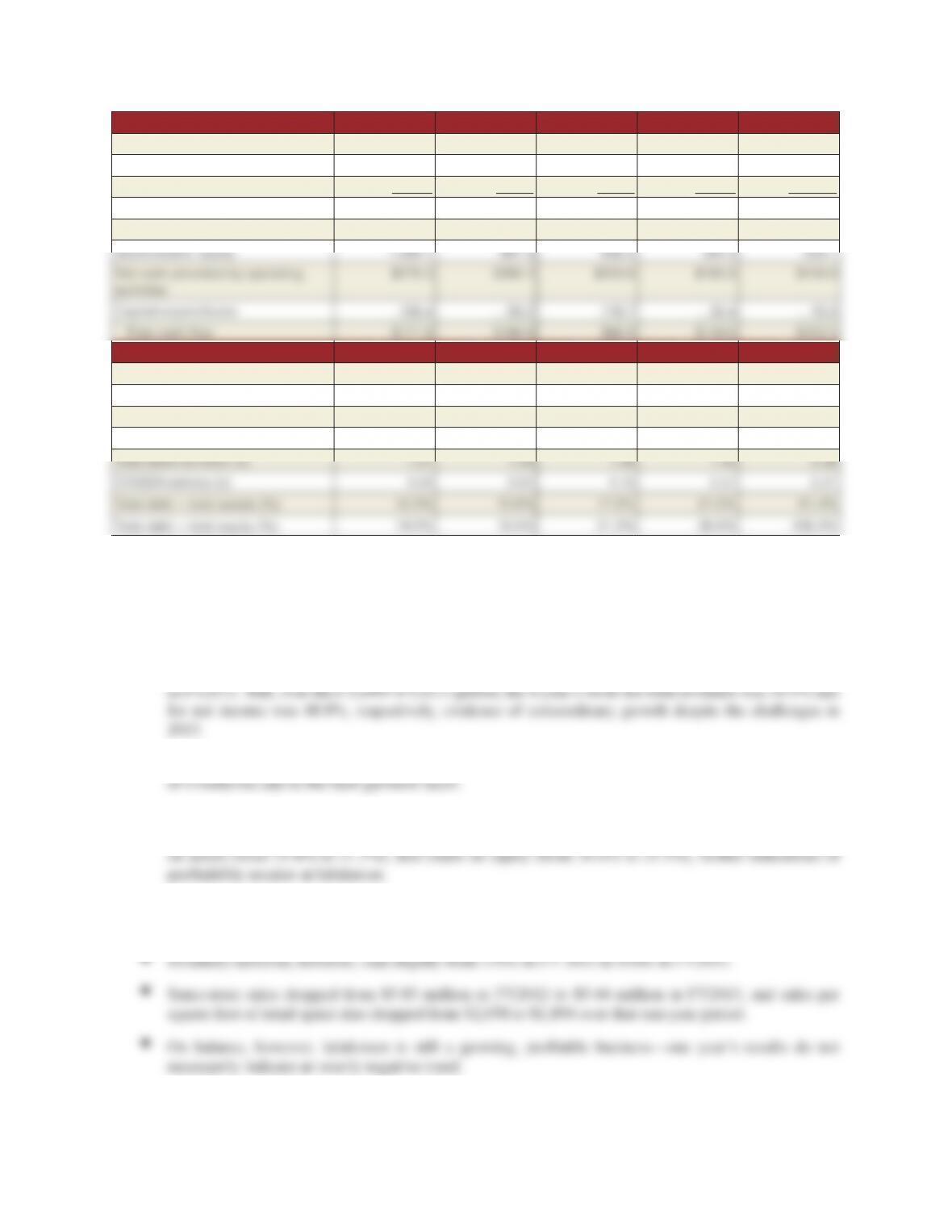

Balance Sheet 2013 2012 2011 2010 2009

Cash and cash equivalents $698.6 $590.2 $409.4 $316.3 $159.6

Inventories 186.1 155.2 104.1 57.5 44.1

Other 365.3 305.7 221.1 125.5 1,046.3

Total assets 1,250.0 1,051.1 734.6 499.3 1,250.0

Total debt 153.3 163.8 128.4 105.0 1,016.9

Financial Ratios 2013 2012 2011 2010 2009

Return on sales, % 17.6% 19.8% 18.5% 17.1% 12.9%

Return on assets, % 22.4% 25.8% 25.2% 24.4% 4.7%

Op. return on assets, % 31.3% 35.8% 39.1% 36.5% 7.0%

Return on equity % 25.5% 30.6% 30.5% 30.9% 25.0%

The following aspects of lululemon’s financial and operating performance ought to be identified by class

members:

From FY2012 to FY2013, growth rates in just about all revenue and profitability categories slackened

considerably, with the sole exception of Cost of Goods Sold, which grew at 23.6% in FY 2013 vs. 36.9%

Gross margins dropped from 55.7% in FY2012 to 52.8% in FY2013, most likely reflecting a markdown

Net income as a percentage of sales (or return on sales) dropped from 19.8 % in FY 2012 to 17.6% in

FY2013, and there were similar declines in returns on assets (from 25.8% to 22.4%), operating returns

Total asset turnover dropped slightly between FY2012 to FY2013, from 1.30x to 1.27x, reflective of

declining revenue growth in relation to the number of new outlets opened in the year (43).

Case 6 Teaching Note lululemon athletica, Inc., in 2014

344

Advanced students may observe that:

Free cash flows (Net cash provided by operating activities—Capital expenditures) continue to be robust.

Based on the table below, free cash flows appear to sufficient to fund future expansion at an approximate

cost of $2.5 million per new store. Also, lululemon has unused debt capacity to aid in that expansion—

2014 2013 2012 2011

Number of stores @end of period 254 211 174 133

Incremental # of stores in year 43 37 41 23

Cap Exp. $106.4 $93.2 $116.7 $30.4

Est. Cost per new store ($ mill.)

9. What 3-4 top priority issues do CEO Laurent Potdevin and lululemon management need

to address?

We think it is always a good idea to push the class for their assessment of what issues management needs

to address before proceeding to ask for action recommendations. Issue identification (or compilation of a

“what I’d do if I were in her/his shoes” list) is a way for students to draw conclusions from all the preceding

analysis, plus it sets the stage for what actions need to be taken.

In lululemon’s case, we see several high-priority issues meriting priority consideration:

nHow to repair the damage from the March 2013 luon recall, the company’s glacially slow response, and

nHow fast and how far to expand lululemon’s product offerings into additional sports apparel and

recreational apparel categories? Should the company continue to focus mainly on yoga and related

nHow rapidly and by what means to expand the distribution of lululemon products to foreign markets

outside North America and in which countries/geographic regions should it concentrate its foreign

nIn foreign country markets, should lululemon continue to avoid the use of franchising and open only

company-owned and -operated retail stores?

nShould lululemon consider selling to independent third party retailers as a third distribution channel,

especially as a means of entering foreign markets?

Case 6 Teaching Note lululemon athletica, Inc., in 2014

345

10. What recommendations would you make to incoming lululemon CEO Laurent Potdevin?

At a minimum, your recommendations should cover what to do about each of the top

priority issues identified in question 9.

Students should be pressed to offer practical action recommendations to address the issues identified in the

prior question. In our view, most all of the front-burner issues at lululemon relate to the inextricable linkage

between its product design function, sourcing and quality control functions, brand image and equity, and

Clearly, in the near-term, the new executive team at lululemon needs to focus on repairing the damage from

the product recall in existing retail markets, and on rapid expansion of retail outlets in markets outside of

Founder Chip Wilson’s continued role as board chairman surely needs to be re-evaluated.

A good case can be made that Wilson needs to step aside, or perhaps even leave the company entirely. His

philosophy—regarding how plus-size women are not suited to lululemon’s apparel—and pronouncements

that plus-size women may have been the cause of its recent problems are likely to have offended some

fraction of the company’s customers and contributed to the sales falloff. At least some students should

There are issues that Potdevin and Tara Poseley (the new Chief Product Officer) must resolve in order

that the business be able to sustain future growth, much less return to lululemon’s prior position as the

unquestioned fast-growing category leader.

The following recommendations seem to us to be actions that students might reasonably propose:

There are several key strategy elements that lululemon management might think about modifying:

nRe-build consumer trust in the lululemon brand and enhance the company’s brand reputation by:

• Becoming more inclusive to women of all shapes and sizes via design changes

• Offering free replacement products or full refund guarantees on all products

nReconsider use of the luon fabric, possibly reformulating or phasing it out, and continue to seek out

innovative fabrics for fitness apparel that enhance performance, comfort, and product quality and to

Case 6 Teaching Note lululemon athletica, Inc., in 2014

346

nContinue to use contract manufacturers to produce lululemon products—integrating backward into

manufacturing should be avoided (What are the benefits? Is it too risky? Will it avoid a repeat of the luon

nFocus on stellar quality, stellar execution, and building stellar relationships with consumers of all shapes

and sizes.

nRe-think the move to a broad differentiation strategy. A case can be made that straying very far from

designing and marketing apparel items that are not complementary or “similar” to what is worn for

yoga and related kinds of workout/fitness/recreational activities pits luluemon in head-on competition

with much larger, better capitalized rivals, such as Nike and Adidas-Reebok, that have proven design

capabilities and impeccable brand equity. In our view, lululemon has no business in designing/marketing

nContinue to expand into additional foreign countries and geographic regions of the world as fast as

internally generated funds will permit. We suspect expansion into Europe should carry a higher priority

than expansion into Asia (with the possible exception of Japan). However, there seems to be ample

opportunity to continue to open the majority of the company’s new retail stores in the United States

for several more years at least. There should be room in the U.S. market for 250–350 lululemon stores

before having to worry much about lululemon stores cannibalizing sales from one another because the

The case does not provide enough information for students to offer sound recommendations about

which European countries or Asian countries should carry the highest priority for expansion. But

because of the logistics costs of supplying foreign store locations with lululemon products and also

introducing customers to the lululemon brand, we suspect that lululemon’s strategy of entering Europe

nBased on the company’s prior retrenchment from franchising, it makes sense to continue to avoid

franchising and to stick with opening only company-owned and -operated retail stores. lululemon seems

nWe suspect most class members will be hesitant to recommend adding third-party retailers as a new

distribution channel for lululemon products. There does not seem to be any compelling reason to expand

Case 6 Teaching Note lululemon athletica, Inc., in 2014

347

While independent retailers could be used as a distribution channel in the markets of foreign countries, it

is doubtful that such would prove to be as profitable or as effective from a brand-building standpoint as

opening company-owned stores. Using lululemon stores and recruiting fitness instructors as lululemon

Epilogue

On August 7, 2014. The company announced that Chip Wilson and Advent had entered into an agreement under

which Advent would acquire approximately 50% of Mr. Wilson’s ownership in lululemon, or approximately

13.85% of the Company’s outstanding shares, for approximately $845 million. The transaction received the full

support of the lululemon Board of Directors.

In its 10-Q filing on September 11, 2014, lululemon management wrote:

Fiscal 2014 is a transitional year, as we focus on building a scalable foundation to support and drive growth in

our businesses. In addition to our plans for North American and international expansion, we are also focused

on initiatives related to help boost our brand experience, connecting with our guests and communities, and

creating innovative, technical and beautiful product. We continue to invest in our product quality and supply

chain, as we believe this is the foundation of our guest loyalty. Our focus on building foundation will also

extend to our other categories, including our men’s and ivivva business, where we see potential for future

expansion. We believe our strong cash flow generation, solid balance sheet and healthy liquidity provide us

with the financial flexibility to execute the initiatives which we believe will continue to lead our profitable

growth.

Throughout the first two quarters of fiscal 2014, we were able to grow our e-commerce business, which

we believe has further increased our brand awareness and has made our product available in new markets,

including those outside of North America. Net revenue from our direct to consumer channel increased 25%

and, represented 16.7% of total revenue in the first two quarters of fiscal 2014 compared to 15.0% of total

revenue in the same period of the prior year. Continuing increases in traffic on our e-commerce website lead

us to believe that there is potential for our direct to consumer segment to become an increasingly substantial

part of our business and we plan to continue to commit a significant portion of our resources to further

developing this channel.

We increased our store base through execution of our real estate strategy, when and where we saw

opportunities for success. We opened seven net new corporate-owned stores during the second quarter of

fiscal 2014. We also opened our East Coast distribution center in Columbus, Ohio during the second quarter

of fiscal 2014. Where we find opportunities for growth through opening showrooms, or other community

presence efforts, we expect to expand our store base and therefore our business. Our growth strategy relies

on expansion in North America, particularly in the United States. We also believe that international growth

is an opportunity and are expanding our foothold in markets by establishing local community connections,

distributing to strategic sales partners and opening showrooms where we believe we can successfully seed

the markets.

Our net revenue increased from $1.4 billion in fiscal 2012 to $1.6 billion in fiscal 2013, representing an

annual growth rate of 16%. Our net revenue also increased from $344.5 million in the second quarter of

fiscal 2013 to $390.7 million in second quarter of fiscal 2014, representing an 13% increase, and total

comparable sales, which includes comparable store sales and direct to consumer, decreased 1% in the second

quarter of fiscal 2014 compared to the second quarter of fiscal 2013. Excluding the effect of foreign currency

fluctuations, total comparable sales would have remained flat. Our ability to open new stores has been driven

by increasing demand for our technical athletic apparel and a growing recognition of the lululemon athletica

brand. We believe our superior products, strategic store locations, inviting guest experience, and distinctive

corporate culture are responsible for our strong financial performance.

Case 6 Teaching Note lululemon athletica, Inc., in 2014

348

We have three reportable segments: corporate-owned stores, direct to consumer and other. We report our

segments based on the financial information we use in managing our businesses. While we prepare financial

information for each corporate-owned store, we have aggregated all of the corporate-owned stores into one

reportable segment due to the similarities in the economic and other characteristics of these stores. Our direct

to consumer segment accounted for 16.2% of our net revenue in second quarter of fiscal 2014, compared to

14.3% in the second quarter of fiscal 2013. Our other segment, consisting of sales from company-operated

showrooms, sales to wholesale accounts, outlets and warehouse sales, accounted for less than 10% of our

net revenue in the first two quarters of fiscal 2014 and fiscal 2013.

Results of Operations—Thirteen-Week Results

The following table summarizes key components of our results of operations for the thirteen weeks ended

August 3, 2014 and August 4, 2013. The operating results are expressed in dollar amounts. The percentages

are presented as a percentage of net revenue.

Thirteen Weeks Ended 8/3/14 and 8/4/13 (Percentages)

(In thousands) 2014 2013 2014 2013

Net revenue $390,708 $344,513 100.0 100.0

Cost of goods sold 193,401 158,558 49.5 46.0

Gross profit 197,307 185,955 50.5 54.0

Selling, general and administrative expenses 129,419 106,969 33.1 31.1

Income from operations 67,888 78,986 17.4 22.9

Other income (expense), net 1,890 1,295 0.5 0.4

Income before provision for income taxes 69,778 80,281 17.9 23.3

Provision for income taxes 21,030 23,816 5.4 6.9

Net income $48,748 $56,465 12.5 16.4

Net Revenue

Net revenue increased $46.2 million, or 13%, to $390.7 million for the second quarter of fiscal 2014 from

$344.5 million for the second quarter of fiscal 2013. Assuming the average exchange rates for the second

quarter of fiscal 2014 remained constant with the average exchange rates for the second quarter of fiscal

2013, our net revenue would have increased $51.3 million, or 15%.

The net revenue increase was driven by sales from new stores opened and the growth of our direct to

consumer segment. Total comparable sales, which includes comparable store sales and direct to consumer

decreased 1% in the second quarter of fiscal 2014 compared to the second quarter of fiscal 2013. Excluding

the effect of foreign currency fluctuations, total comparable sales would have remained flat.

Pertinent Analyst Comment Corinna Freedman, an analyst at Wedbush Securities in New York, said in a

phone interview with Lindsey Rupp of Bloomberg News, on March 27, 2014:

…product and supply chain issues have been plaguing the company for the past year. It is an extremely

competitive landscape, and operating at that premium price point is going to require stellar execution.

For the latest information on developments at lululemon athletica, please visit the Investor Relations section at

www.lululemon.com and check out the company’s recent press releases and financial results.