Case 21 Teaching Note PepsiCo’s Diversification Strategy

566

There’s ample room for judgmental differences regarding selection of the factors, the weights, and the

ratings used to draw a 9-cell GE matrix depicting PepsiCo’s portfolio. Therefore you should expect that

student opinions will vary and the matrices they come up with will vary. In this instance, however, the

variations should not be very great since it is clear that the industries represented in PepsiCo’s portfolio are

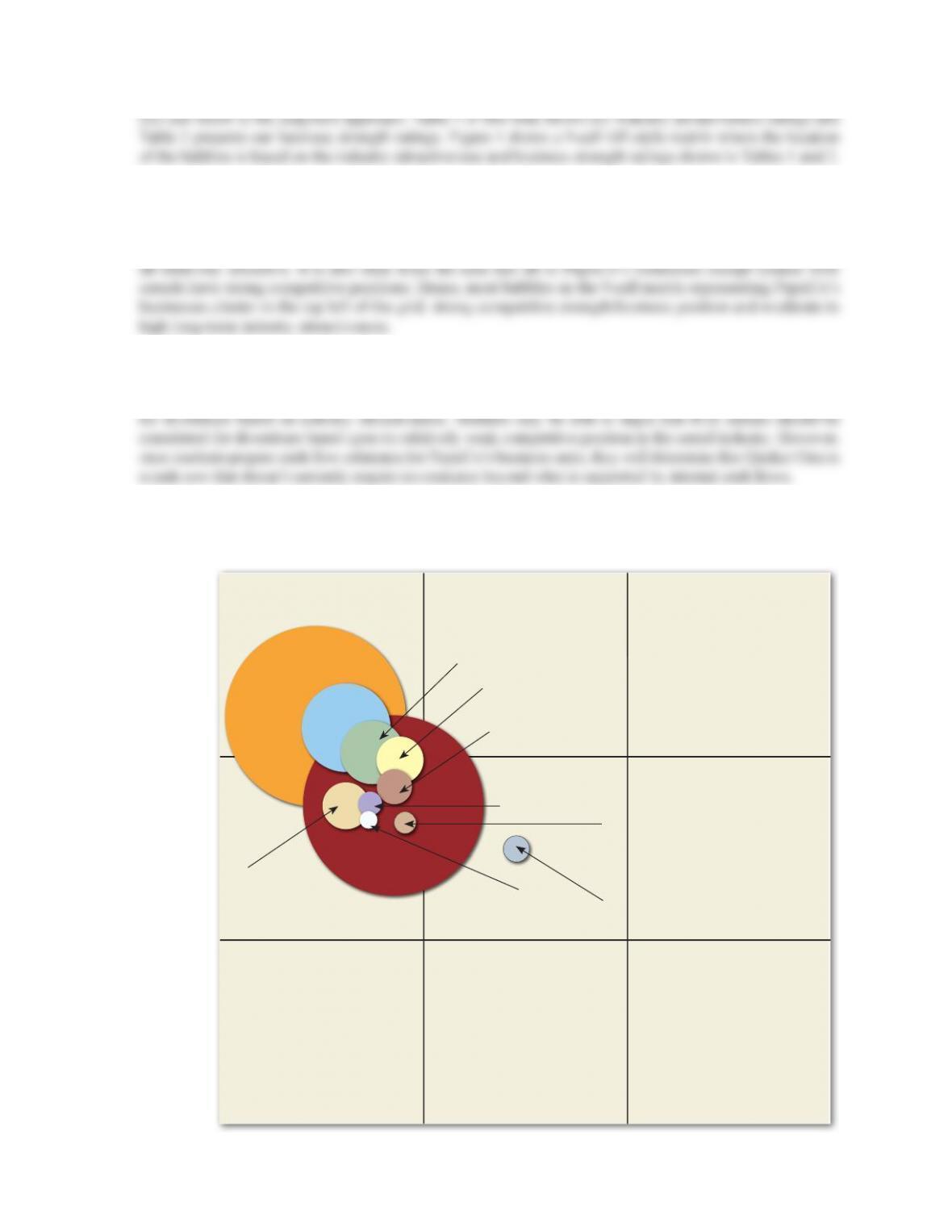

The 9-cell GE-style matrix analysis (Figure 1) indicates that PepsiCo’s portfolio consists chiey of “grow

and build” businesses that should be given a high priority for investment. Students should conclude that RTE

cereals should be given a medium investment priority. None of PepsiCo’s business units need to be considered

FIGURE 1. Assessment of Strategic Fit Potentials Between

PepsiCo’s Business Units

Frito-Lay

Strong Weak

Competitive Strength/Business Position

Long–Term Industry Attractiveness

High

Pepsi-Cola

Gatorade

Aquana

Tropicana/

Dole/SoBe

Lipton/

SoBe Teas

Quaker

Oatmeal

Rice-A-Roni

Starbucks

Frappucino

Quaker Cereal

Aunt Jemima

Medium

Low

6.7

3.3

6.7 3.3

Case 21 Teaching Note PepsiCo’s Diversification Strategy

567

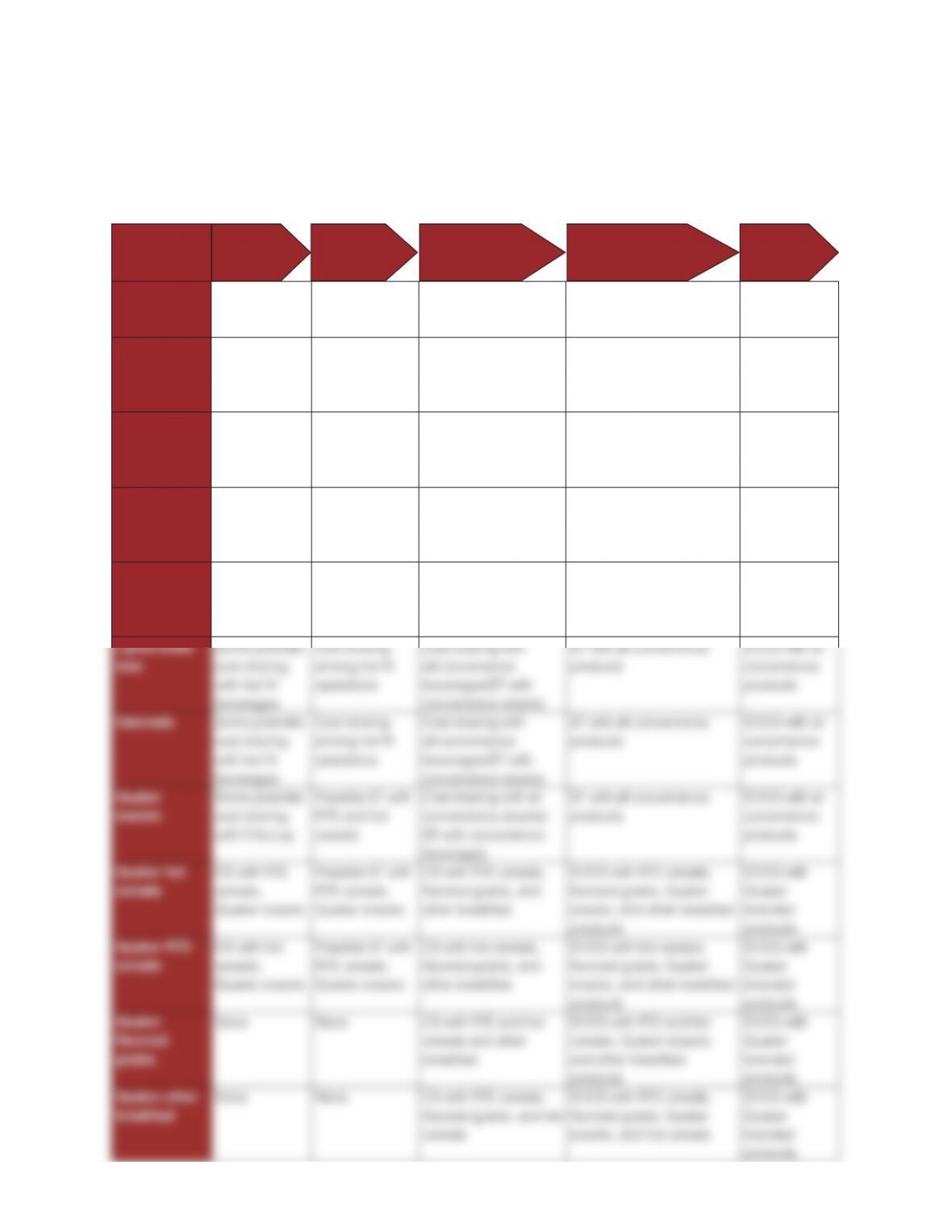

5. Does PepsiCo’s portfolio exhibit good strategic fit? What value-chain match-ups do

you see? What opportunities for skills transfer, cost sharing, or brand sharing do you

see?

Substantial cost sharing and skills transfer opportunities exist between PepsiCo’s beverage brands and

between its various snack brands, but there appear to be less strategic fit opportunities across business

platforms. The operating processes vary greatly between hot fill beverage bottling, soft drink concentrate

production, grain-based food products production, and snack food production. Students may suggest that

beyond PepsiCo’s corporate-wide purchases for ingredients and packaging materials, it is unlikely that

PepsiCo management shares market research and relies heavily on marketing innovations to position their

brands in each market in which it competes. Consumers in each of these markets have much in common

and it should be expected that PepsiCo managers share skills and information in crafting and implementing

the strategies of each of the businesses. Some students may point to the company’s Power of One strategy

that allows its products to be cross-marketed in retail locations as an example of marketing-related strategic

fit. The Quaker Oats integration produced a number of noteworthy strategic fit successes, including $160

The operations, sales and marketing, and advertising/promotion of Quaker’s hot and RTE cereals, avored

grains, and other breakfast products have little in common with value chain activities of PepsiCo’s convenience

Case 21 Teaching Note PepsiCo’s Diversification Strategy

568

FIGURE 2. Assessment of Strategic Fit Potentials Between Pepsico’s

Business Units

CS = cost sharing benefits ST = skills transfer opportunities

Value Chain Activities

Business Unit

Pepsi Cola None None None Cross-selling with Frito-

Lay products/ST with all

convenience products

ST/CS with all

convenience

products

Frito-Lay Some potential

cost sharing

with Quaker

Snacks

None Cost sharing with all

convenience snacks/

ST with convenience

beverages

Cross-selling with Pepsi

products/ST with all

convenience products

ST/CS with all

convenience

products

Tropicana/

Dole/SoBe

Some potential

cost sharing

with hot fill

beverages

Cost sharing

among hot fill

operations

Cost sharing with

all convenience

beverages/ST with

convenience snacks

ST with all convenience

products

ST/CS with all

convenience

products

Aquafina None Cost sharing

among hot fill

operations

Cost sharing with

all convenience

beverages/ST with

convenience snacks

ST with all convenience

products

ST/CS with all

convenience

products

Starbucks

Frappucino

None Cost sharing

among hot fill

operations

Cost sharing with

all convenience

beverages/ST with

convenience snacks

ST with all convenience

products

ST/CS with all

convenience

products

Purchasing Operations Distribution Sales & Marketing Advertising

/Promotion

Case 21 Teaching Note PepsiCo’s Diversification Strategy

569

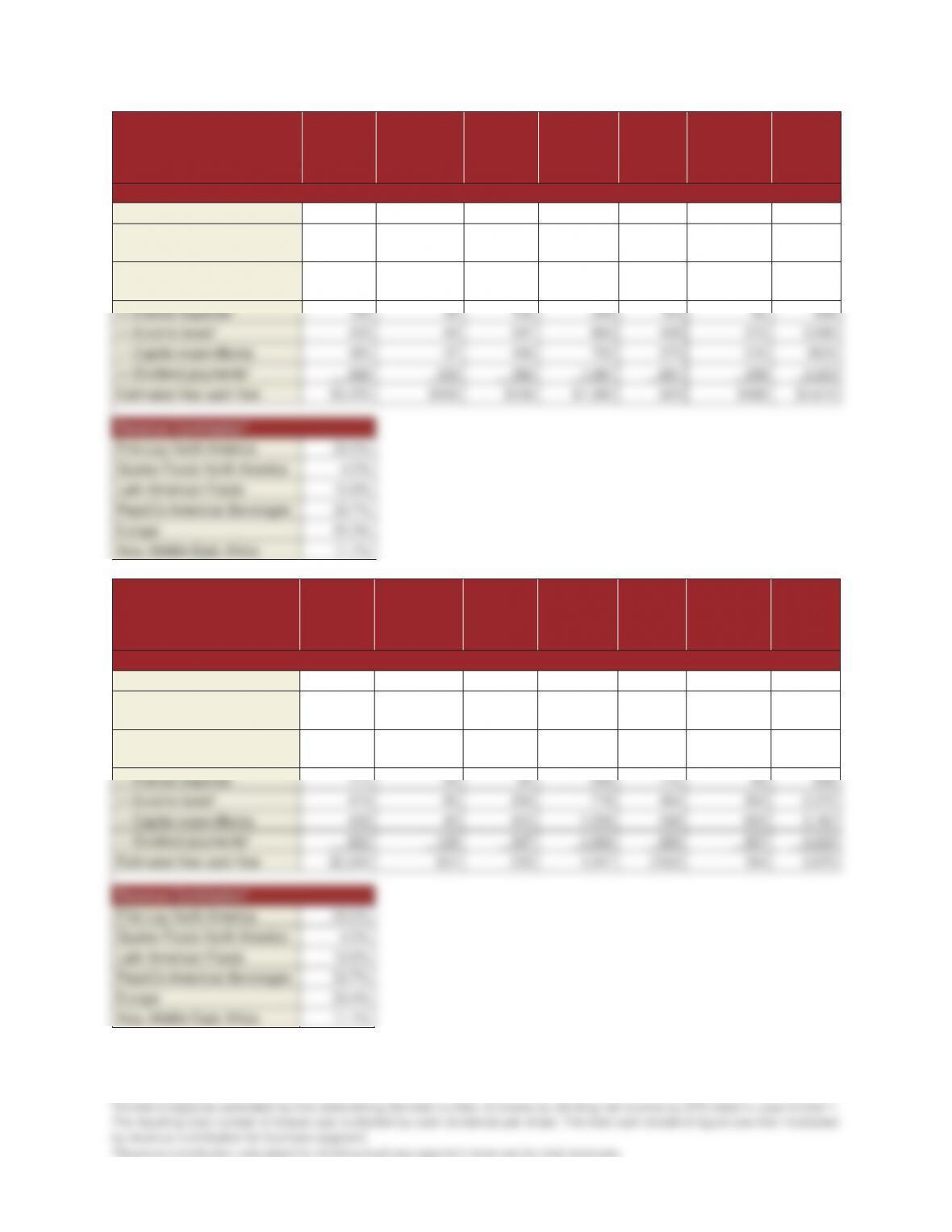

6. Does PepsiCo’s portfolio exhibit good resource fit? What are the cash flow characteristics

of each of PepsiCo’s four segments? Which businesses are the strongest contributors

to PepsiCo’s free cash flows?

Students who have completed the assignment questions posted on the Student Edition of the OLC should

recognize that the portfolio has very good resource fit, with all of the company’s businesses except Europe

offering ample cash ows to fund internal investments. The cash ow estimates in Table 3 indicate that

all business units generated free cash ows each year between 2011 and 2013, except Europe (negative in

In addition, students should approve of the operating profit margins of the company’s North American

businesses (Frito-Lay North America and Quaker Foods North America) presented in Table 4. Even though

Quaker Oats’ brands compete in mature processed food categories that offer little growth potential, the

TABLE 3. Estimated Cash Flow for Pepsico’s Business Units, 2011–2013

Frito-Lay

North

America

Quaker

Foods

North

America

Latin

American

Foods

PepsiCo

Americas

Beverages Europe

Asia

Middle East

Africa

Total

Division

2013

Operating profit $3,877 $617 $1,242 $2,955 $1,293 $1,174 11,158

+Depreciation/other

amortization 430 51 253 863 525 283 2,553

+Amortization of intangible

assets 7 — 8 58 32 5110

1

Revenue Contribution

4

Frito-Lay North America 21.3%

Quaker Foods North America 3.9%

Latin American Foods 12.6%

Case 21 Teaching Note PepsiCo’s Diversification Strategy

570

Frito-Lay

North

America

Quaker

Foods

North

America

Latin

American

Foods

PepsiCo

Americas

Beverages Europe

Asia

Middle East

Africa

Total

Division

2012

Operating profit $3,646 $695 $1,059 $2,937 $1,330 $1,330 10,414

+Depreciation/other

amortization 445 53 248 855 522 305 2,570

+Amortization of intangible

assets 7 — 10 59 36 7119

1

Frito-Lay

North

America

Quaker

Foods

North

America

Latin

American

Foods

PepsiCo

Americas

Beverages Europe

Asia

Middle East

Africa

Total

Division

2011

Operating profit $3,621 $797 $1,078 $3,273 $1,210 $1,210 $10,866

+Depreciation/other

amortization 458 54 238 865 522 350 2,604

+Amortization of intangible

assets 7 — 10 65 39 12 133

1

1Interest expense estimated by multiplying total interest expense listed in case Exhibit 3 by revenue contribution for business

segment.

2Income tax expense estimated by multiplying total income tax expense listed in case Exhibit 3 by revenue contribution for

business segment.

Case 21 Teaching Note PepsiCo’s Diversification Strategy

571

TABLE 4 Operating Profit Margins by PepsiCo Business Segment,

2011–2013

2013 2012 2011

Frito-Lay North America 27.5% 26.9 27.2

Quaker Foods North America 23.6% 26.4% 30.0%

Latin American Foods 14.9% 13.6% 15.1%

Calculated from case Exhibit 7.

7. Based on the preceding analysis, what is your overall evaluation of PepsiCo’s business

portfolio in 2013? Does the portfolio provide the company’s shareholders with an

opportunity for above-average market returns?

Students will likely commend Roger Enrico, Steve Reinemund, and Indra Nooyi for their efforts as CEO to

build shareholder value. Enrico’s spin-off of the company’s restaurants, IPO of its bottling operations, and

acquisitions of Tropicana, Cracker Jack, and Quaker Oats contributed to more than a 100% increase in the

company’s share price between 1997 and late 2008. Stock price performance has been equally impressive

over the past four years (2011–2014) with an increase of over 50%—see case Exhibit 2. With the exception

There is some question concerning the ability to gain synergistic benefits between some of Quaker’s

food businesses and PepsiCo’s convenience food and beverage businesses, but the cash ow analysis and

operating profit margins presented in Tables 3 and 4 suggest that these businesses do have the ability to

8. What strategic actions should Indra Nooyi take to sustain the corporation’s impressive

financial and market performance? Should its free cash flows be used to fund

additional share repurchase plans, pay higher dividends, make acquisitions, expand

internationally, or for other purposes? What other strategic actions should be pursued

by corporate level management?

Students may struggle with what moves are needed next at PepsiCo, but should be able to recommend most

of the following:

nStudents will likely have mixed opinions about PepsiCo’s international business units. Some will argue

for divestiture of Europe based on its relatively low contribution to corporate profits (9% in 2013).

Case 21 Teaching Note PepsiCo’s Diversification Strategy

572

However, Europe contributes over 20% of PepsiCo’s net revenues and with the weakening of the Euro

nThe company should capitalize on its recent reorganization to further internationalize Quaker Oats’

brands. The new organizational structure creating the PepsiCo Americas Foods division should make

nSimilarly, students should recognize the importance of exploiting PepsiCo’s new organizational structure

to further internationalize Gatorade. Gatorade’s sales outside the United States should benefit from

nStudents are also likely to suggest that PepsiCo push Propel and Aquafina into additional markets in

nStudents may recommend that the company divest its Quaker RTE cereals, avored grains, and other

breakfast products because of low industry growth rates. However, students should not be too forceful

nStudents should suggest that the company should utilize its free cash ows to support the ongoing $15

nThere doesn’t seem to be a strong reason for students to recommend that PepsiCo undertake a major

nStudents will likely recommend that the company continue to develop BFY and GFY snacks and

beverages.

nStudents should also recommend that PepsiCo Europe pursue more aggressive efforts to capture strategic

nPepsiCo International should also make greater use of the company’s Power of One strategy in

Epilogue

In 2014, PepsiCo’s strategies appeared to be performing well. PepsiCo’s top managers expected the company’s

portfolio of snack, beverages, and grocery items to generate cash ows sufficient to reinvest in its core businesses,

provide cash dividends to shareholders, fund a $15 billion share buy-back plan and pursue acquisitions that would

provide attractive returns. However, the relatively low profit margins of the company’s international businesses

dictated continued examination of its strategy and operations to exploit strategic fits among the company’s

international business units.

You can check for the company’s latest financial reports and press releases at its investor web site (www.pepsico.

com).