459

– 459 –

TEACHING NOTE

CASE 14

J. Crew in 2014

Overview

In 2014, J. Crew was a $2.4 billion specialty retailer comprising 450 outlets in the U.S. and one in Canada.

J. Crew competed in the $42 million U.S. specialty retailing industry, with a focus on women’s apparel.

CEO Mickey Drexler (ex-GAP stores) was entering his second decade guiding J. Crew. Since 2003, Drexler

had masterminded J. Crew’s domestic expansion, its diversification into younger women’s apparel (Madewell),

children’s wear (Crewcuts), and wedding/special occasion wear (J. Crew Wedding). Drexler also oversaw a

turnaround in J. Crew’s direct sales via catalogue and website, which by the end of FY2013 reached $756

million, representing about 31% of company revenues. In 2011, liquidity problems and declining net income

had forced its sale to two private equity firms for $3.1 billion, including the assumption of $1.6 billion in debt.

Sales in the U.S. specialty retailing industry reached $42 billion in 2013. The industry comprised some 29,000

businesses, and anticipated a growth rate of 3.6 percent in revenues from 2013 to 2018. Demand was primarily

driven by customer demographics, disposable income, fashion trends, and brand name. The prolonged 2008

recession and lingering economic uncertainty in 2014 impacted sales and profits. Decreasing disposable income

induced consumers to purchase based on price and quality rather than on brand name, diverting sales from

specialty retailers to discounters such as Wal-Mart and Costco. Also, e-commerce retailers offered lower

prices, free shipping, and other promotions. Concentration in the industry was low, with no one retailer holding

more than an 8 percent share. The top four players—J. Crew, Ascena Retail Group, Ann, Inc., Forever 21,

and Hennes & Mauritz (H&M)—held a 20 percent share. Merger and acquisition activity began to increase

industry concentration. China and Vietnam, already major suppliers to J. Crew, were expected to manufacture

78.6 percent of all garments sold in the U.S. by 2018. Cotton, a key driver of overhead costs, had spiked in price

in 2010 due to a global shortage and stockpiling by China. As a result of these factors, competition in the market

for specialty retailing was intensifying.

Drexler and his team had reached a crossroads regarding how best to re-position the company for long-term

growth and rejuvenate interest and sales. After J. Crew changed its fashion design strategy from lines of

traditional/conservative clothing to trendier, more youthful apparel, its Fall 2013 line of women’s apparel did

not sell well, and its regular customers complained. Women’s apparel as a percentage of total revenues declined

from 58 percent in 2011 to 55 percent. J. Crew remained saddled with $1.5 billion in debt from the leveraged

buyout in 2011. At the same time, the company was reportedly about to open new stores in London, Tokyo, and

Hong Kong, places where reception of its products was not automatically guaranteed.

There’s ample detail in the case for students to evaluate:

n J. Crew’s strategy.

n The attractiveness of the company in light of recent events, its current situation and future prospects.

n The company’s financial performance.

: Will Its Turnaround

Strategy Improve Its Competitiveness?*

*This teaching note reflects the thinking and analysis of Professor Armand Gilinsky, Sonoma State University. We are most grateful

for his insight, analysis and contributions to how the case can be taught successfully.

Case 14 Teaching Note J. Crew in 2014

460

Suggestions for Using the Case

This case pairs well with material covered in Chapters 3–5. It is particularly useful for illustrating the following

concepts:

nHow to evaluate the macro- and competitive environment in which a company operates (covered in

Chapter 3)

nHow to determine whether an industry’s outlook presents a company with sufficiently attractive opportunities

for growth and profitability (also covered in Chapter 3)

nIdentifying those competitive factors or key success factors (KSF) that most affect industry members’ ability

to survive and prosper in the marketplace: (also covered in Chapter 3)

• Strategy elements

• Product attributes

• Operational approaches

• Resources and competitive capabilities—that spell the difference between being a strong competitor

and a weak competitor—and between profit and loss.

nImproving the effectiveness of the company’s customer value proposition and enhancing differentiation:

(covered in Chapter 4)

• Best practices for quality, marketing, and customer service.

• Reallocating resources to activities that address buyers’ most important purchase criteria, which will

have the biggest impact on the value delivered to the customer

• Adopting new technologies that spur innovation, improve design, and enhance creativity.

nHow to assess a company’s internal resources and capabilities, including its value chain (also covered in

Chapter 4)

nImproving a company’s competitive position based on its generic strategy (covered in Chapter 5)

• Why some generic strategies work better in certain kinds of competitive conditions than in others.

Video for Use with the J. Crew in 2014 case. There is a 3:11 video entitled “A Cheaper J. Crew on the

Way?” that would be best viewed after students have read the case and become familiar with the industry. You

What to Tell Students in Preparing the J. Crew Case for Class. To give students guidance in what to

do and think about in preparing the J. Crew case for class discussion, we strongly recommend they master and

nProvide class members with assignment questions and insist that they prepare good notes/answers to

these questions before coming to class. Our recommended assignment questions for the J. Crew case are

To facilitate your use of assignment questions and making them available to students, we have posted a

file of the Assignment Questions contained in this teaching note on the instructor resources section of the

Case 14 Teaching Note J. Crew in 2014

461

In our experience, it is quite difficult to have an insightful and constructive class discussion of an assigned case

unless students have conscientiously have made use of pertinent core concepts and analytical tools in preparing

substantive answers to a set of well-conceived study questions before they come to class. In our classes, we

Utilizing the Guide to Case Analysis. If this is your first assigned case, you may find it beneficial to have

class members read the Guide to Case Analysis that immediately follows Case 31 in the text. The content of this

Suggested Assignment Questions for an Oral Team Presentation or Written Case Analysis. We

believe that, as fashion and clothes are quite popular with students and they are familiar with the industry, the J.

Crew case is quite well-suited for written assignments and oral team presentations. Our suggested assignment

questions are as follows:

nMickey Drexler, CEO of J. Crew, has employed you as a consultant to assess the company’s overall

situation and recommend a set of actions to improve its future prospects. Please prepare a report to J. Crew

management that includes: (1) an evaluation of J. Crew’s current strategy, (2) an assessment of J. Crew’s

strengths, weaknesses, opportunities and threats, (3) an assessment of the primary components of J. Crew’s

nPrepare a brief 1–2 page report to J. Crew CEO Mickey Drexler outlining the 3–4 top priority issues that

J. Crew management needs to address. Make explicit the actions you thinks management should initiate to

address these issues and sustain J. Crew future growth and profitability. Your report should contain detailed

Assignment Questions

1. How strong are the competitive forces confronting J. Crew in the market for specialty retail? Do a five-forces

analysis to support your answer.

2. What does your strategic group map of the specialty retail industry look like? Is J. Crew well positioned?

Why or why not?

3. What do you see as the key success factors in the market for specialty retailers?

4. What does a SWOT analysis reveal about the overall attractiveness of J. Crew’s situation?

5. What are the primary components of J. Crew’s value chain?

6. What are the key elements of J. Crew’s strategy?

7. Which one of the five generic competitive strategies discussed in Chapter 5 most closely approximates the

competitive approach that J. Crew is employing?

Case 14 Teaching Note J. Crew in 2014

462

8. What do the data in case Exhibit 1 and 2 reveal about J. Crew’s financial and operating performance?

9. What 3–4 top priority issues do CEO Mickey Drexler and J. Crew management need to address?

10. What recommendations would you make to J. Crew CEO Mickey Drexler? At a minimum, your

recommendations should cover what to do about each of the top priority issues identified in question 9.

Teaching Outline and Analysis

1. How strong are the competitive forces confronting J. Crew in the market for specialty

retailers? Do a five-forces analysis to support your answer.

to

Rivalry

Among

Competing

Competitive pressures coming from the

Competitive pressures coming

Substitutes

for Specialty

Retailers

Threat of New

that shop at

stemming

stemming

The case provides an opportunity to introduce or review the five-forces model of competition for specialty

retailing companies that primarily but not exclusively serve the women’s fashion apparel segment.

nRivalry among competing specialty retailers—a moderate to strong competitive force

Case 14 Teaching Note J. Crew in 2014

463

Rivalry is growing more intense in the $42 billion specialty retailing industry.

• The industry is mature; revenues are forecasted to grow by 3.6 percent from 2013–2018

• The number of stores is forecasted to grow at 2.3 percent per year from 2013–2018, from about

54,600 to 61,200 outlets in the U.S.

Rivalry is centered on three main factors:

• Relative price

Students should be pressed to identify several rivalry-related competitive pressures at work in specialty

• Efforts of rivals to expand their product lines and offer a broader selection of apparel, primarily to

• Active efforts on the part of the specialty retailers to build and strengthen the appeal of their product

• The prospects for increased consolidation via acquisition and merger; Ascena Retail Group

• The top four players held about 20 percent of the market.

• Rivals needed to be at the forefront of fashion trends and also anticipate what consumers’ demands

Factors that are acting to moderate industry rivalry:

• Differentiation that exists among the different brands of specialty retail chains (as concerns product

selection, brand image, quality, design, celebrity customers, and styling)—such differentiation

Case 14 Teaching Note J. Crew in 2014

464

• Globalization offering higher growth opportunities to the chains because there should be sufficient

untapped demand in international markets to enable each rival to grow sales/market share without

On the whole, we believe it is fair to say that the competitive pressures associated with rivalry among the

specialty retail chains are moderate to strong and growing stronger. Class members should recognize that

the case indicates the competitive pressures associated with rivalry are so potent as to make it difficult for

nCompetitive pressures associated with the threat of new entry into the specialty retailer market—a

strong competitive force

In assessing this competitive force, students should draw upon the information in Figure 3.5 in Chapter

3 (and the related text discussion).

Factors that are acting to intensify the threat of entry:

• There are low barriers to entry.

• Access to prime locations such as a shopping malls or a freestanding building that provides good

visibility, curb appeal, and accessibility is generally available.

• Access to domestic and global markets via e-commerce direct sales is potentially unlimited.

Factors that are acting to moderate or weaken the threat of entry:

• Due to cultural and physiological differences among consumers in many nations, customer

acquisition costs are rising as the market for specialty apparel brands globalizes

Case 14 Teaching Note J. Crew in 2014

465

On the whole, we believe it is fair to say that the competitive pressures that impact the threat of entry into

the specialty retail industry are strong.

nCompetitive pressures associated with substitutes for specialty retailer operators—a strong

competitive force

In assessing this competitive force, students should draw upon the information in Figure 3.6 in Chapter

3 (and the related text discussion).

Factors that are acting to intensify competitive pressures due to substitution threats:

• During the height of the 2008–09 global economic recession, many consumers turned to deep

• Consumer access to specialty apparel via e-commerce direct sales is virtually unlimited.

• At the high end of the market, there are numerous designers whose collections are available at

• At the budget-conscious end, there is always the do-it-yourself (DIY) option.

We do not think there are many factors that act to moderate or weaken competitive pressures due to

substitution threats to specialty retailing, therefore, the threat of substitutes is a potent force.

nCompetitive pressures associated with the bargaining power of suppliers to specialty retailers—a

weak to moderate competitive force

In assessing this competitive force, students should draw upon the information in Figure 3.7 in Chapter

3 (and the related text discussion).

• Increases in outsourcing to China and Vietnam—forecasted to provide 78.6 percent of apparel to

specialty retailers by 2018

• Cotton price spikes, as in 2010 when China cornered the market, causing a shortage of this vital raw

material in apparel and ratcheting up retailers’ overhead costs

Factors that are acting to moderate or weaken competitive pressures due to the bargaining power of

suppliers to specialty retailers:

Case 14 Teaching Note J. Crew in 2014

466

On balance, we view the bargaining power of suppliers as being moderate to low.

nCompetitive pressures associated with the bargaining power of buyers from specialty retailers—a

strong competitive force, depending on the location of buyer

In assessing this competitive force, students should draw upon the information in Figure 3.8 in Chapter

3 (and the related text discussion).

Factors that are acting to intensify competitive pressures due to the bargaining power of specialty retail

customers:

• Buyers have many choices among specialty retailers, and switching costs are non-existent.

• Price and image and design are the main determinants of purchasing behavior, followed by location

and breadth of product line.

A factor that acts to weaken competitive pressures from customers for specialty retailers:

• Although people can choose to make their own apparel at home, despite the relative ease of entry into

Conclusions concerning the Overall Strength of All Five Competitive Forces in specialty

retailing: The collective strength of the five competitive forces facing J. Crew, Ann Inc., Ascena, Forever

2. What does your strategic group map of the specialty retail industry look like? Is J. Crew

well positioned? Why or why not?

Strategic group maps are beneficial for determining relative company placement in the industry. A good

Students can choose among any of several strategic variables or dimensions to divide the specialty retail

Based on the information about the four main rivals provided in the case, we have chosen to employ image/

fashion focus (timeless/conservative vs. youthful/trendy) price point (i.e., low, moderate or upper tier) and

scope of used by specialty retailers. Other possibilities for axes might include: geographic coverage (i.e.

Case 14 Teaching Note J. Crew in 2014

467

Note: It is not possible nor necessarily desirable to include Wal-Mart and Costco, prominent deep discount

rivals mentioned in the case, due to the limited information provided not to mention their vastly broader

product lines, larger scale, and expanded scope of operations relative to the specialty retailers under focus.

To set the stage and help students provide some context and data for creating a strategic group map using

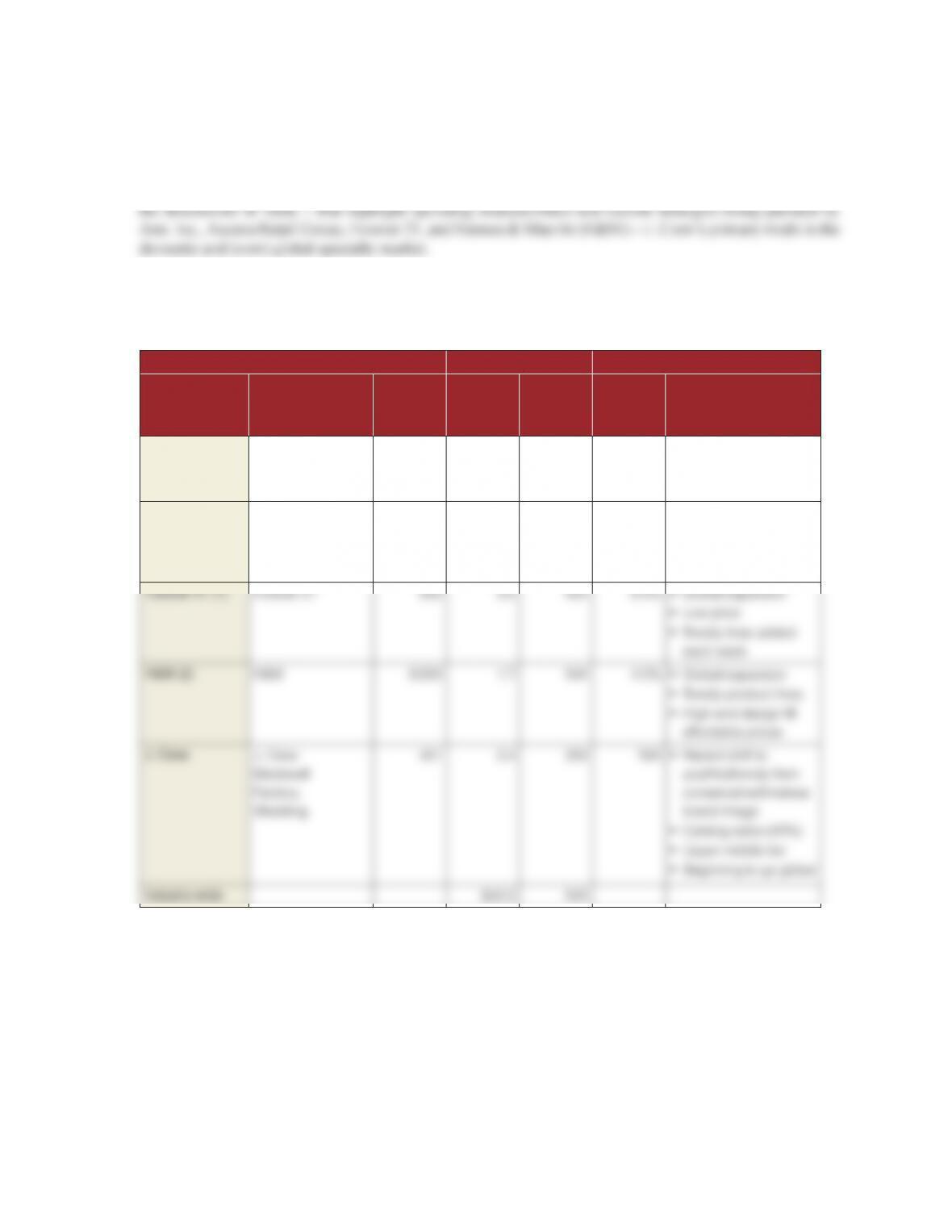

TABLE 1. Operating Highlights and Key Strategies of the Major Rivals

in the Specialty Retail in 2013

—FY 2013—

Company

Key

brands

Total

# stores

Rev.

($ billion)

Oper.

inc.

($ million)

Market

share,

%

Strategy

elements

Ann Inc. Ann Taylor, Loft,

Factory

1,000 $2.6 $189 5.6%

•

New stores

•

New trendy lines

•

Upper moderate price

Ascena

Retail

Group

Lane Bryant

Dress Barn,

Justice, Catherine,

Charming Shoppes

3.900 3.4 101 7.1%

•

Diversified portfolio

•

Merger & acquisition

•

Moderate price

•

Trendy lines

Notes

(1) U.S. revenues for Forever 21 approximately 50% of this total, or $1.5 billion.

(2) H&M’s U.S. revenues only.

Case 14 Teaching Note J. Crew in 2014

468

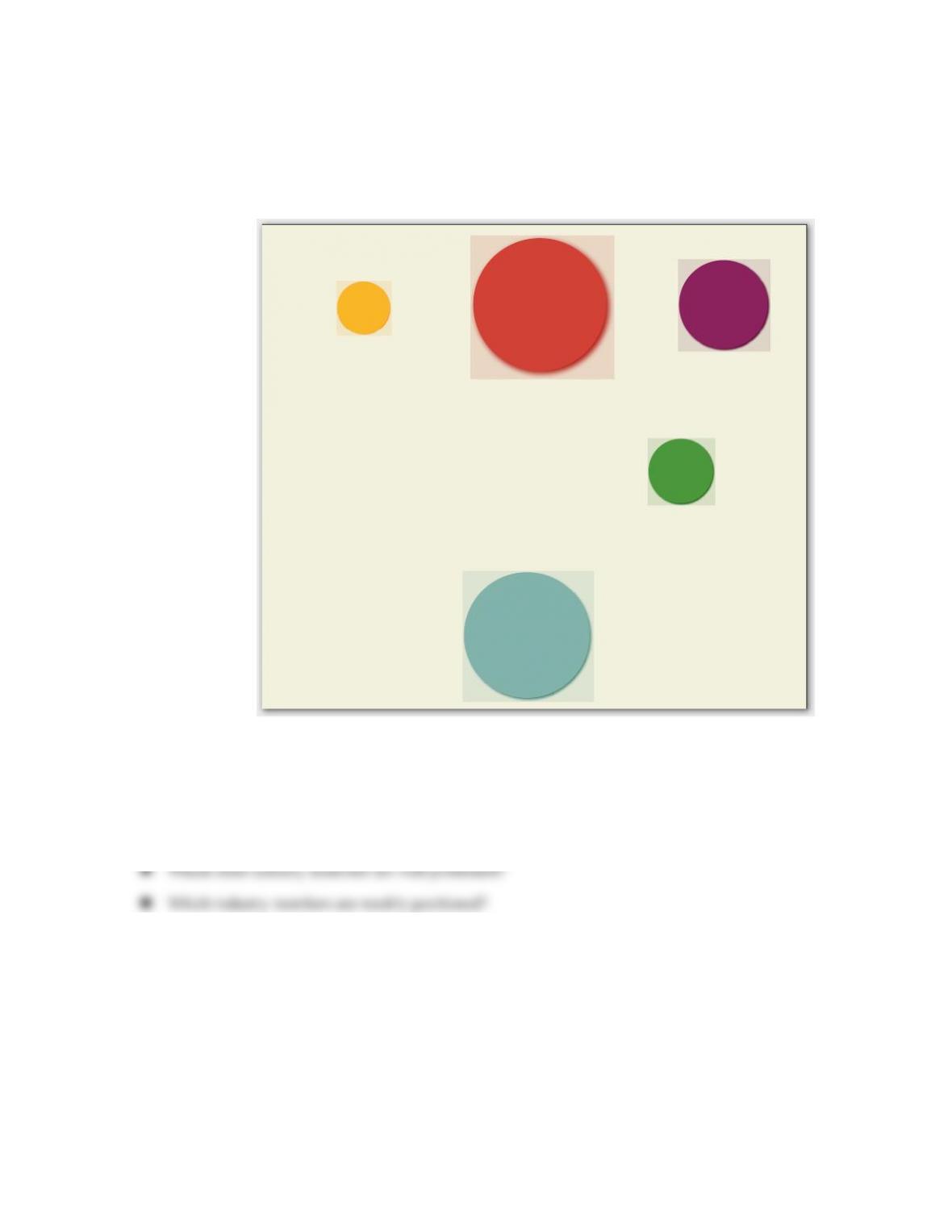

Figure 1 presents a representative strategic group map for the specialty retailing industry.

FIGURE 1. A Representative Strategic Group Map of the Specialty

Retailing Industry

Forever

21

High

Relative Price

Image/Fashion

Focus

Low

Youthful/

Trendy

Timeless/

Conservative

H & M

J. Crew

Ann

Ascena

Once students have come up with a map, then we think you should press them for their evaluation of what

we learn from the map. Any of the following questions can be posed to help draw out their views:

nHow well is J. Crew positioned?

The point here is that students should not stop their analysis with just drawing a strategic group map. The

most important part of strategic group mapping is to draw some conclusions about the story the map tells.

On the whole, we find J. Crew’s position on the map to be a mixed blessing:

nIts image, product offerings, and distribution channel strategy are relatively distinct from those of its key

rivals.

Case 14 Teaching Note J. Crew in 2014

469

nJ. Crew caters to several segments besides women’s apparel—notably, children and weddings. Yet those

• Most children’s clothing is purchased in summer during back-to-school promotions and to a lesser

nAlthough rival chains have brand-name reputations and brand-name recognition, their price points tend

to be either higher or lower than J. Crew.

nJ Crew has shifted away from timeless, conservative apparel to more youthful, trendy lines, where

Despite its catalog sales and direct e-commerce sales growth, J. Crew, by contrast to its rivals, has had

apparent problems maintaining its fashion focus on preppy, conservative clothing.

3. What do you see as the key success factors in the market for specialty retail apparel?

Listing industry Key Success Factors (KSFs) should be an enjoyable part of the class discussion—we like

to have students help generate the list and then remind them that they are unlikely to remember more than

TABLE 2. Key Success Factors in the Specialty Retail Industry

KEY SUCCESS FACTOR

Relative price

Brand image

Fashion design

Location

Narrowing down the list of priority factors is often subject to debate, but students tend to agree that relative

price and brand image are vital for all players in the market, typically followed by a debate as to