Exercise 9-5 (20 minutes)

Subject

to Tax Rate Tax Explanation

a.

FICA––Social Security…… $ 800 6.20% $ 49.60 Full amount is subject to tax.

FICA—Medicare............. 800 1.45 11.60 Full amount is subject to tax.

SUTA….…….……….……... 600 2.90 17.40 $200 is over the maximum.

b.

FICA––Social Security…… $2,100 6.20% $130.20 Full amount is subject to tax.

FICA—Medicare............. 2,100 1.45 30.45 Full amount is subject to tax.

c.

FICA––Social Security…… $6,300 6.20% $390.60 $1,700 is over the maximum.

FICA—Medicare............. 8,000 1.45 116.00 Full amount is subject to tax.

Exercise 9-6 (10 minutes)

Sept. 30 Salaries Expense………………………………………..……. 800.00

FICA—Social Security Taxes Payable…….……. 49.60

FICA—Medicare Taxes Payable………….…….…. 11.60

To record payroll for pay period ended September 30.

Exercise 9-7 (10 minutes)

Sept. 30 Payroll Taxes Expense……………………………………… 82.20

FICA—Social Security Taxes Payable………….. 49.60

FICA—Medicare Taxes Payable…….……….……. 11.60

Exercise 9-8 (30 minutes)

1. July 31 Sales Salaries Expense……………..….……….………...200,000

Office Salaries Expense…………………..………………..160,000

FICA—Social Sec. Taxes Payable…………..….… 22,320

FICA—Medicare Taxes Payable..…….……….….. 5,220

Employee Fed. Inc. Taxes Payable…………....... 90,000

Employee State Inc. Taxes Payable………..….… 20,000

Employee Medical Insurance Payable*…......... 2,800

2. July 31 Salaries Payable…………………………………..….…….…

217,060

3. July 31 Payroll Taxes Expense…………………………….………..30,540

FICASocial Sec. Taxes Payable……............... 22,320

FICAMedicare Taxes Payable……………………. 5,220

July 31 Employee Benefits Expense…….……….…….……….. 6,600

Employee Medical Insurance Payable*…......... 4,200

4. July 31 FICASocial Security Taxes Payable……….……..…44,640

FICAMedicare Taxes Payable……………….………...10,440

Employee Fed. Income Taxes Payable………….…...90,000

Employee State Income Taxes Payable.................20,000

Employee Medical Insurance Payable…................ 7,000

Employee Life Insurance Payable….…….………...... 4,000

Exercise 9-9 (30 minutes)

a.

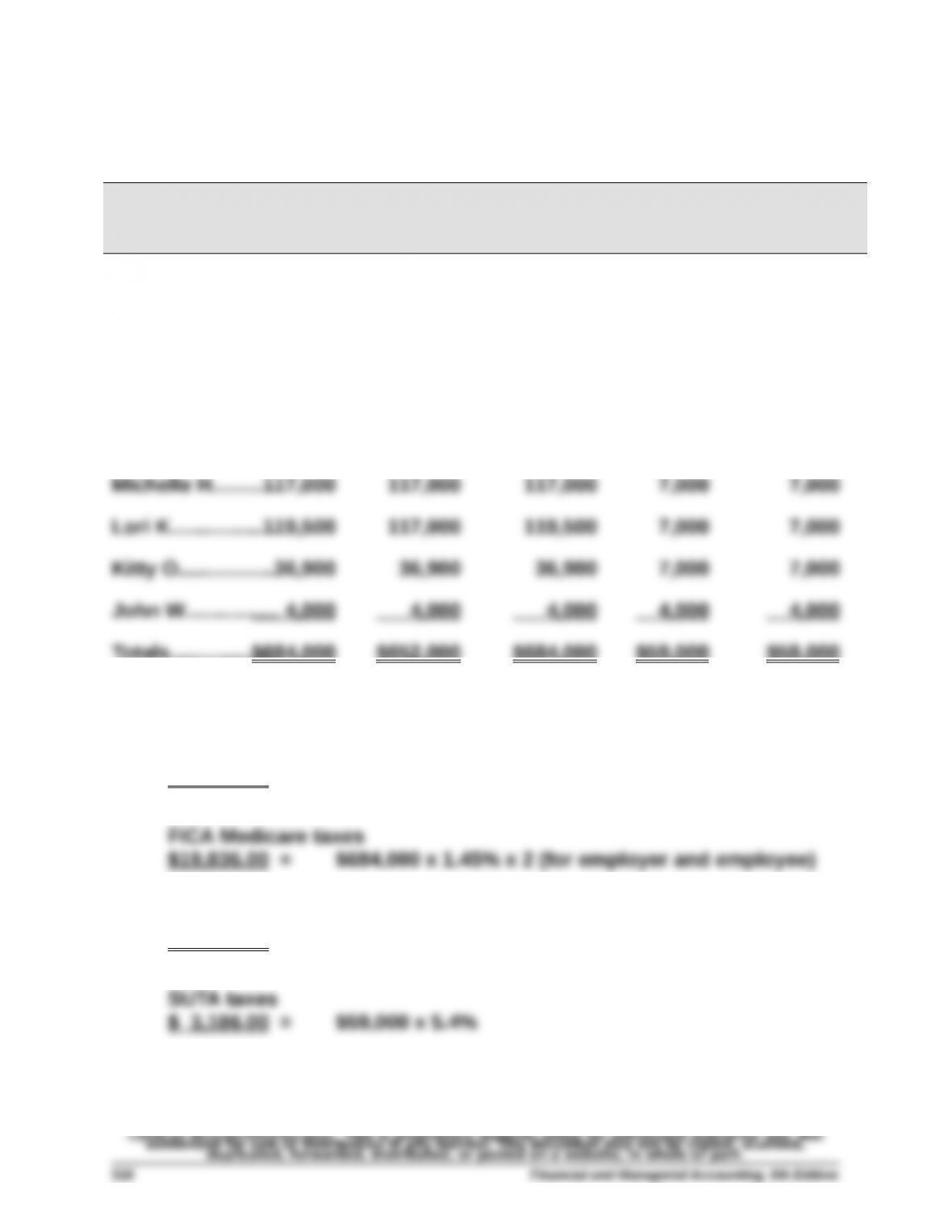

Employee

Cumulative

Pay

Pay Subject to

FICA Social

Security

Pay Subject

to FICA

Medicare

Pay Subject

to FUTA

Taxes

Pay Subject

to SUTA

Taxes

Ken S….…….........$ 6,000 $ 6,000 $ 6,000 $ 6,000 $ 6,000

Tim V………………..60,200 60,200 60,200 7,000 7,000

Steve S................87,000 87,000 87,000 7,000 7,000

Ann T….…............146,500 117,000 146,500 7,000 7,000

Kathleen K………..106,900 106,900 106,900 7,000 7,000

Totals……….…......$684,000 $652,000 $684,000 $59,000 $59,000

b. FICA Social Security taxes

$80,848.00 = $652,000 x 6.2% x 2 (for employer and employee)

FUTA taxes

$ 354.00 = $59,000 x 0.6%

Exercise 9-10 (25 minutes)

1. Warranty Expense = 4% of dollar sales = 4% x $6,000 = $240

2. The December 31, 2015, balance of the liability equals the expense

3. The company should report no additional warranty expense in 2016 for

this copier.

4. The December 31, 2016, balance of the Estimated Warranty Liability

account equals the 2016 beginning balance minus the costs incurred in

2016 to repair the copier:

5. Journal entries

2015 (a)

Aug. 16 Cash…………..…………………….……………………………... 6,000

Sales……….……………………..……………..…….…….. 6,000

To record cash sale of copier.

Aug. 16 Cost of Goods Sold………..…………………………..……. 4,800

Merchandise Inventory……..…………….….…….… 4,800

To record cost of August 16 sale.

(b)

Exercise 9-11 (15 minutes)

1. B = 0.03 ($500,000 – B)

2.

2015

Dec. 31 Employee Bonus Expense……………..…….……... 14,563

3.

2016

Jan. 19 Bonus Payable…………………………..……….………. 14,563

Exercise 9-12 (10 minutes)

[Note: All entries dated December 31, 2015.]

1. Vacation Benefits Expense……………….….….……….…… 3,200

[20 employees x 1 day x $160].

2. Warranty Expense……………………………………..…….……. 18,000

Estimated Warranty Liability……………..…….….……. 18,000

Exercise 9-13 (10 minutes)

[Note: All entries dated December 31, 2015.]

1. No adjusting entry is required since it is not probable that the supplier will

2. No adjusting entry can be made since the loss cannot be reasonably

in the notes to the financial statements.

Exercise 9-14 (15 minutes)

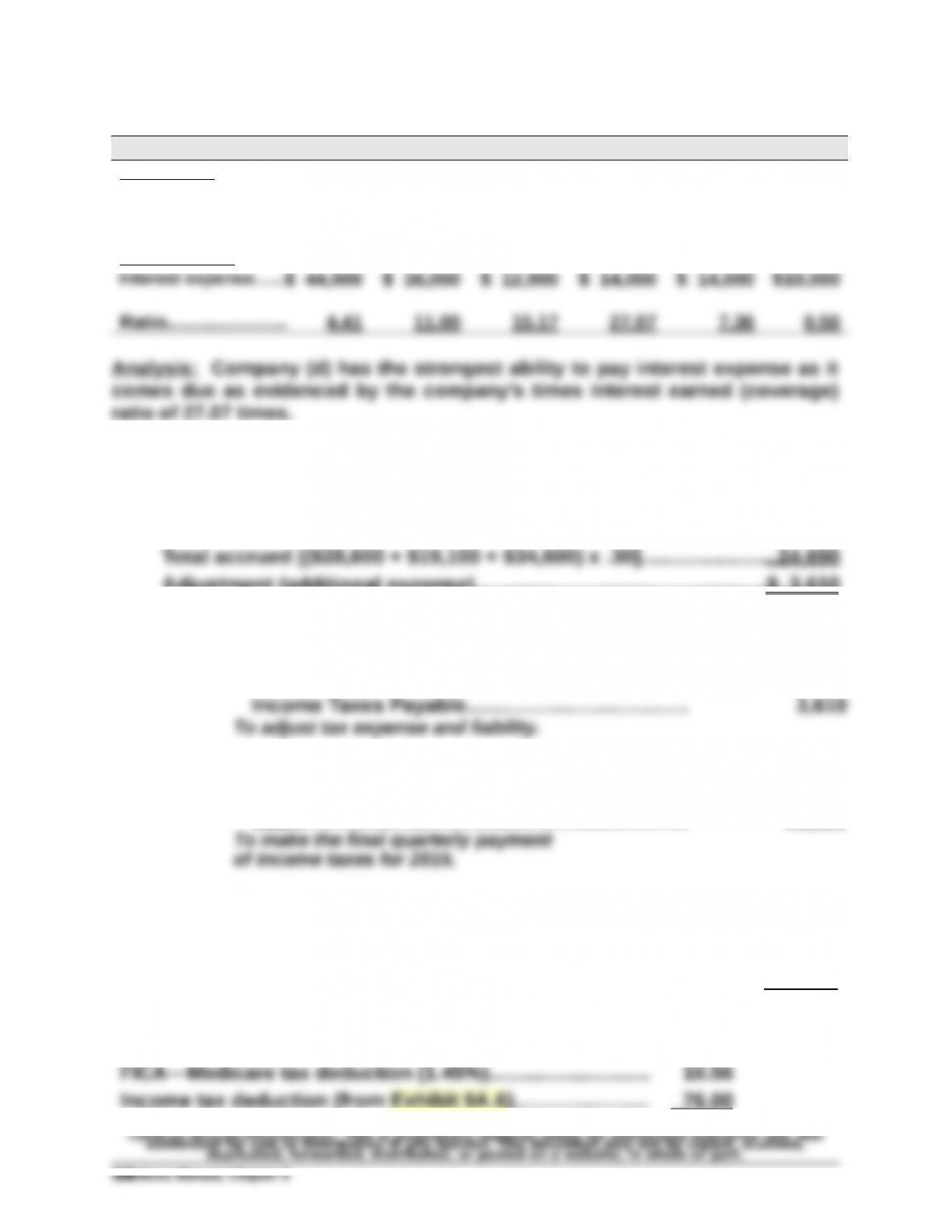

(a) (b) (c) (d) (e) (f)

Numerator

Income before

interest & taxes.....$194,000 $176,000 $182,000 $379,000 $103,000 $ 5,000

Denominator

Exercise 9-15B (25 minutes)

1. Income Taxes Payable (target balance)…………………….……….………...$28,300

Adjustment (additional expense)…………..………………………………….….$ 3,610

2.

2015 (a)

Dec. 31 Income Tax Expense………….………………..…….…….. 3,610

2016 (b)

Jan. 20 Income Taxes Payable…………………………….…….…. 28,300

Cash…………………………………..…………………….… 28,300

Exercise 9-16A (15 minutes)

Regular pay (40 hours @ $14)…………..……….…….………... $560.00

Overtime premium pay (8 hours @ [$14 x 150%])........... 168 .00

Gross pay…………..………………………….……….……….……… 728.00

FICA—Social Security tax deduction (6.2%)………….….... $ 45.14

Exercise 9-17 (30 minutes)

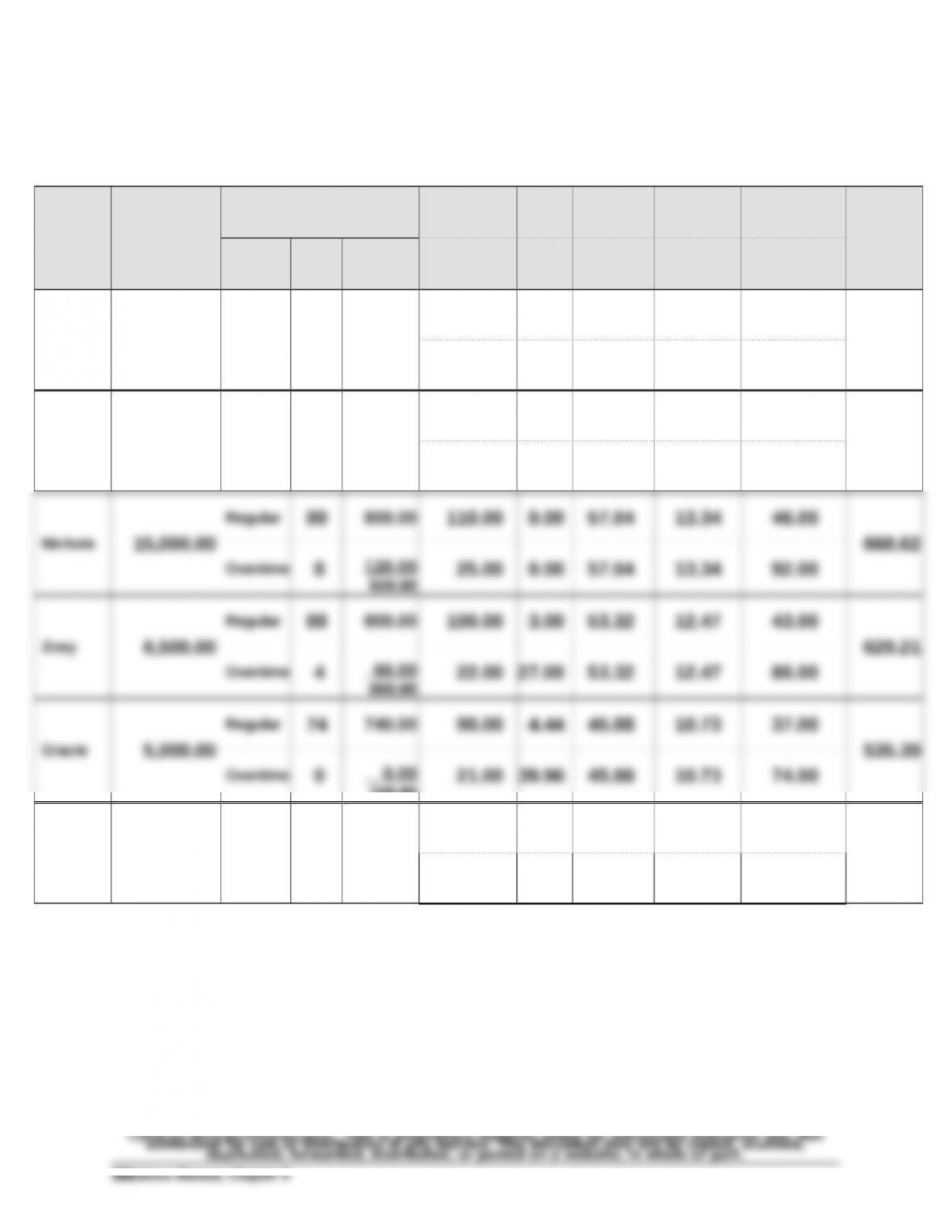

(a)

Employe

e

Cumulative

Pay (Excludes

Current Period)

Current Period Gross Pay FIT

Withholding FUTA FICA S.S.

Employee

FICA

Medicare

Employee

Employee—

Benefits Plan

Withholding Employee

Net Pay

Pay

Type

Pay

Hours Gross Pay SIT

Withholding SUTA FICA S.S.

Employer

FICA

Medicare

Employer

Employer—

Benefits Plan

Expense

Kathleen 115,200.00 Salary — 7,000.00

2,000.00 0.00 111.60 101.50 350.00

4,136.90

300.00 0.00 111.60 101.50 700.00

Anthony 6,800.00 Salary — 500.00

80.00 1.20 31.00 7.25 25.00

336.75

20.00 10.80 31.00 7.25 50.00

Regular 80 800.00 110.00 0.00 57.04 13.34 46.00

740.00

Totals 148,500.00 10,020.00

2,380.00 8.64 298.84 145.29 501.00

6,306.87

388.00 77.76 298.84 145.29 1,002.00

Exercise 9-17 (concluded)

(b)

Aug 31 Salaries (or Wages) Expense……….…….…….……….10,020.00

FICA—Social Sec. Taxes Payable…………..….… 298.84

FICA—Medicare Taxes Payable..…….……….….. 145.29

Employee Fed. Inc. Taxes Payable…………....... 2,380.00

To record payroll for period.

(c)

Aug 31 Salaries (or Wages) Payable……………………………..

6,306.87

(d)

Aug 31 Payroll Taxes Expense………………………….…………..530.53

FICASocial Sec. Taxes Payable……............... 298.84

FICAMedicare Taxes Payable……………………. 145.29

Federal Unemployment Taxes Payable……...... 8.64

(e)

Aug 31 FICASocial Security Taxes Payable…….………..…

597.68

FICAMedicare Taxes Payable……………….………...290.58

Employee Fed. Income Taxes Payable………….…...

2,380.00

Employee State Income Taxes Payable.................

388.00

Employee Benefits Plan Payable………………….……1,503.00