PROBLEM SET B

Problem 8-1B (50 minutes)

Part 1

Estimated

Market Value

Percent

of Total

Apportioned

Cost

Building…………….…….…. $ 890,000 50% $ 900,000

Land……………….………….. 427,200 24 432,000

2015

Jan. 1 Buildings………….…………………..…………….….…….…….…900,000

Land………………………………………..…………………….….…..432,000

Land Improvements…………………………………….….……..252,000

To record asset purchases.

Part 2

Year 2015 straight-line depreciation on building

Part 3

Year 2015 double-declining-balance depreciation on land improvements

Part 4

Accelerated depreciation does not increase the total amount of taxes paid

over the asset’s life. Instead, it defers or postpones taxes to the later years of

an asset’s useful life. This is because accelerated methods charge a higher

Problem 8-2B (25 minutes)

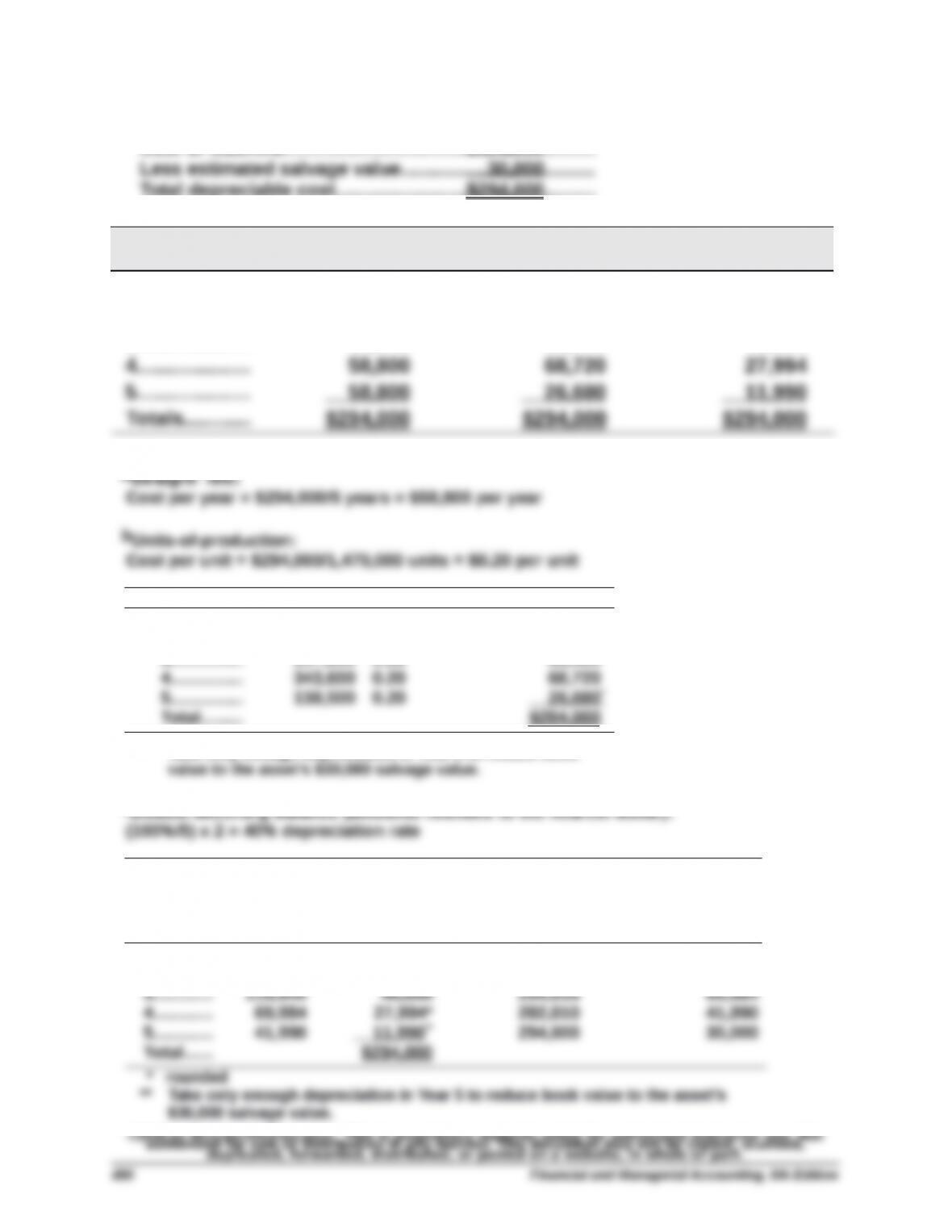

Cost of machine….…….……..…….……..…………..………...$324,000

Total depreciable cost…….…….……..…….…….…………..$294,000

Year Straight-LineaUnits-of-Productionb

Double-Declining-

Balancec

1…..….…….…. $ 58,800 $ 71,120 $129,600

2…..….…….…. 58,800 64,080 77,760

3…..….…….…. 58,800 63,400 46,656

Year Units Unit Cost Depreciation

1………...... 355,600 $0.20 $ 71,120

2………...... 320,400 0.20 64,080

3………...... 317,000 0.20 63,400

* Take only enough depreciation in Year 5 to reduce book

Year

Beginning

Book Value

Annual

Depreciation

(40% of

Book Value)

Accumulated

Depreciation

at the End of

the Year

Ending Book Value

($324,000 Cost less

Accumulated

Depreciation)

1…......... $324,000 $129,600 $129,600 $194,400

2…......... 194,400 77,760 207,360 116,640

Problem 8-3B (45 minutes)

Part 1

Land

Building

B

Building

C

Land

Improve-

ments B

Land

Improve-

ments C

Purchase price*..........$ 868,000 $527,000 $155,000

Demolition……..…........ 122,000

Land grading……......... 174,500

Allocation of

purchase price

Appraised

Value

Percent

of Total

Apportioned

Cost

Land……….……..…............…...... $ 795,200 56% $ 868,000

Part 2

2015

Jan. 1 Land………………………………………………….………..…. 1,164,500

Building B…………………………………..………………..… 527,000

Building C…………………………………..………………..… 1,458,000

Part 3

2015

Dec. 31 Depreciation Expense—Building B………………….….…….…….

…………………………………………………….…………………………………

…………………………………………………….…………………………………

28,500

31 Depreciation Expense—Building C……….…….….......60,000

Accumulated Depreciation—Building C………..… 60,000

31 Depreciation Expense–Land Improvements B..….…

…………………………………………………….………………….….

31,000

31 Depreciation Expense–Land Improvements C….…..

…………………………………………………….………………….….

10,350

Problem 8-4B (50 minutes)

2014

Jan. 3 Equipment……..………………………………….………..….…... 1,850

Cash………………………………………………………………. 1,850

To record betterment of van.

Dec. 31 Depreciation Expense—Equipment……………………….5,124*

Accumulated Depreciation—Equipment…..……... 5,124

To record depreciation.

*2014 depreciation after January 3rd betterment

Total original cost……………………………………………………….…..$27,670

2015

May 10 Repairs Expense—Equipment…………….…….….……... 800

Cash………………………………………………………………. 800

To record ordinary repair on van.

Dec. 31 Depreciation Expense—Equipment………………………. 3,760

Accumulated Depreciation—Equipment…..……... 3,760

To record depreciation.

*2015 depreciation after 1/1 extraordinary repair

Total cost ($29,520 + $2,064)…………………………………………………………………..$31,584

Problem 8-5B (40 minutes)

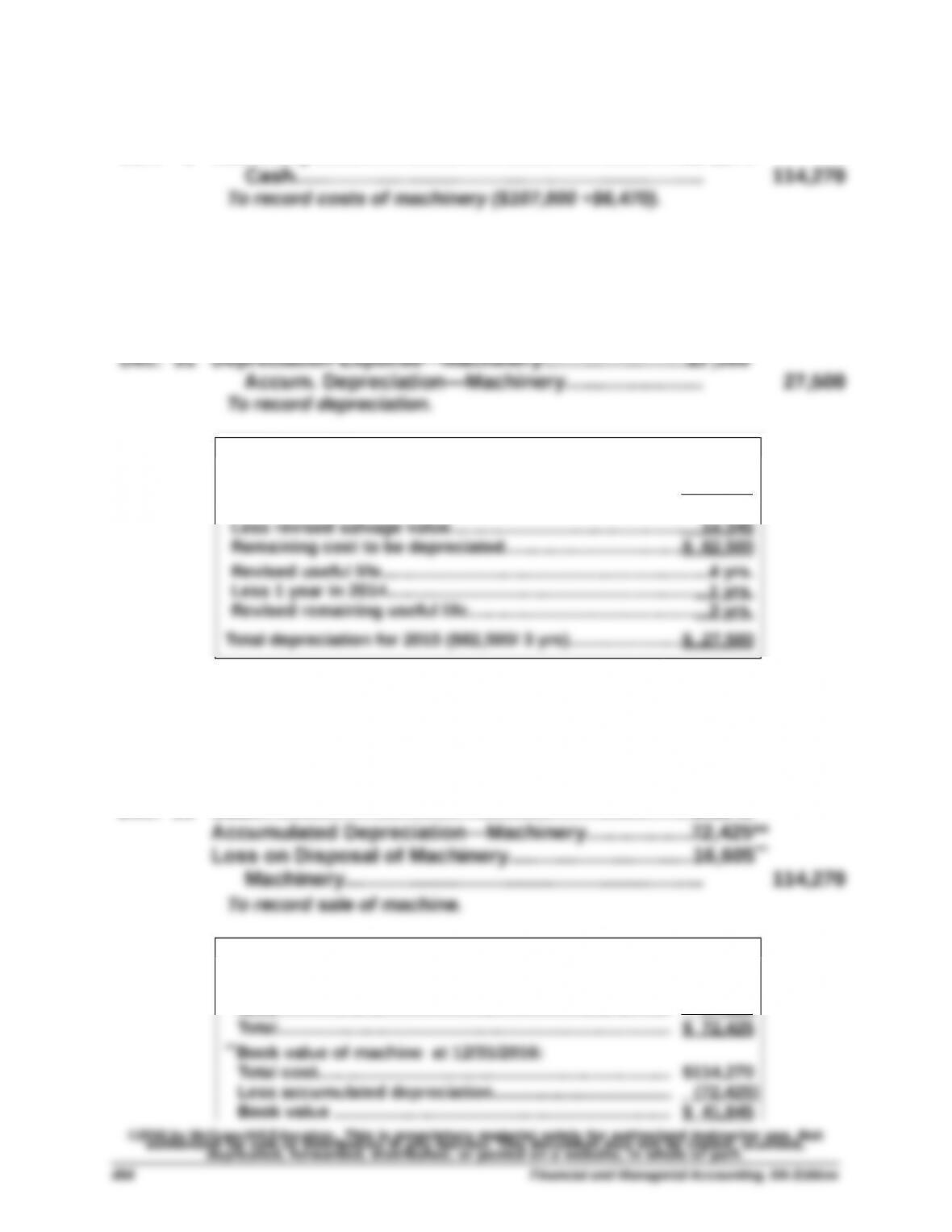

2014

Jan. 1 Machinery…………..……………….………………….…………...114,270

Dec. 31 Depreciation Expense—Machinery..….….…….….…….17,425

Accumulated Depreciation—Machinery…………… 17,425

To record depreciation [($114,270-$9,720)/6].

2015

*2015 depreciation:

Total cost…………………………………..………………………....…………$114,270

Less accumulated depreciation (from 2014)………..……..……... 17,425

Book value…………………………………..…………………………………..96,845

2016

Dec. 31 Depreciation Expense—Machinery…..….…….….……..27,500

Accumulated Depreciation—Machinery…………… 27,500

To record depreciation.

Dec. 31 Cash…………………………………………….……………………... 25,240

**Accumulated depreciation on machine at 12/31/2016:

2014………………………………………..…………………………….. $ 17,425

2015………………………………………..…………………………….. 27,500

2016………………………………………..…………………………….. 27,500

Problem 8-6B (20 minutes)

To record machinery costs.

Jan. 4 Machinery………………………….…….…….…….….…….… 4,600

Cash……………………………………….…….…….….….. 4,600

To record machinery costs.

2. a. First year

Dec. 31 Depreciation Expense—Machinery..….…….….…….....20,000

Accumulated Depreciation—Machinery…………… 20,000

To record depreciation [($158,110-$18,110)/7 =

$20,000].

b. Sixth year

3. Accumulated depreciation at the date of disposal

a. Sold for $28,000 cash

Dec. 31 Cash………………………………..…………………..……………...28,000

Loss on Sale of Machinery…………….………………….….10,110

Accumulated Depreciation—Machinery….................120,000

Machinery……..……………………………………………….. 158,110

b. Sold for $52,000 cash

Dec. 31 Cash………………………………..…………………..……………...52,000

Accumulated Depreciation—Machinery….................120,000

Machinery……..……………………………………………….. 158,110

Gain on Sale of Machinery………..…….….….…….… 13,890

Problem 8-7B (20 minutes)

a.

Feb. 19 Mineral Deposit…………..………………………………………..5,400,000

Cash………………………………………………………………. 5,400,000

To record purchase of mineral deposit.

b.

Mar. 21 Machinery……….…………………………………..……………….400,000

Cash………………………………………………………………. 400,000

To record costs of machinery.

c.

Dec. 31 Depletion Expense—Mineral Deposit………………….…342,900

d.

Dec. 31 Depreciation Expense—Machinery..….…….….…….....25,400

Analysis Component

Similarities—Amortization, depletion, and depreciation are similar in that

Differences—They are different in that they apply to different types of long–