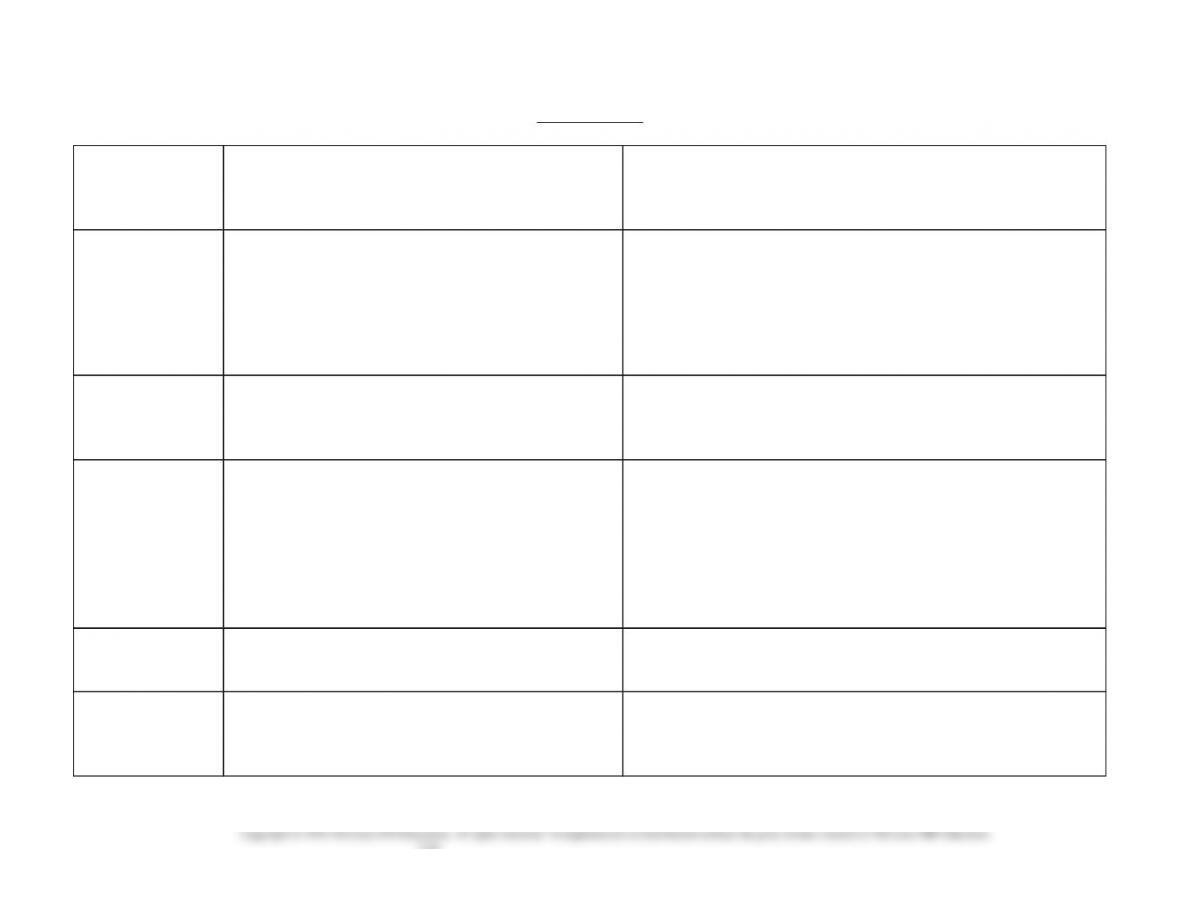

VISUAL # 7-1

METHODS OF ACCOUNTING FOR BAD DEBTS

DIRECT WRITE-OFF METHOD

Accounts for bad debts from an uncollectible account

receivable at the time account is determined to be

uncollectible.

ALLOWANCE METHOD

At the end of each accounting period,

bad debts expense is

estimated and recorded.

Year-end No adjusting entry

Adjusting entry required:

Bad Debt Expense XXX

Allowance for Uncollectible Accounts XXX

(The amount is an estimate based on a percentage of sales or a

percentage of outstanding accounts receivable. If the estimate is based

on sales, the full estimate is used in the adjusting entry. If the estimate

is based on accounts receivable the allowance account balance is

brought to the amount of the estimate.)

When an account is

determined to be

uncollectible

Write-off entry required:

Bad Debts Expense XXX

Accounts Receivable/Customer XXX

(The amount is the balance of the uncollectible account.)

Write-off entry required:

Allowance for Uncollectible Accounts XXX

Accounts Receivable/Customer XXX

(The amount is the balance of the uncollectible account.)

When an account

previously written

off is recovered

1. Reinstate account by reversing write-off:

Accounts Receivable/Customer XXX

Bad Debts Expense XXX

(The amount is the account balance that was written off.)

2. Record collection on account normally:

Cash XXX

Accounts Receivable/Customer XXX

(The amount is the amount collected.)

1. Reinstate account by reversing write-off:

Accounts Receivable/Customer XXX

Allowance for Uncollectible Accounts XXX

(The amount is the account balance that was written off.)

2. Record collection on account normally:

Cash XXX

Accounts Receivable/Customer XXX

(The amount is the amount collected.)

Advantages: Does not require adjusting entry.

Does not require year-end estimating of

uncollectibles.

Matches expense against related revenues.

Reports the net realizable accounts receivable on the balance

sheet (a more accurate reporting of assets).

Disadvantages: Violates matching (expense recognition) principle,

therefore only allowed if qualified under

materiality principle. (Permitted if a business

anticipates an immaterial amount of uncollectibles.)

Requires adjusting entry.

Requires year-end estimating of uncollectibles.

7-8

7-9

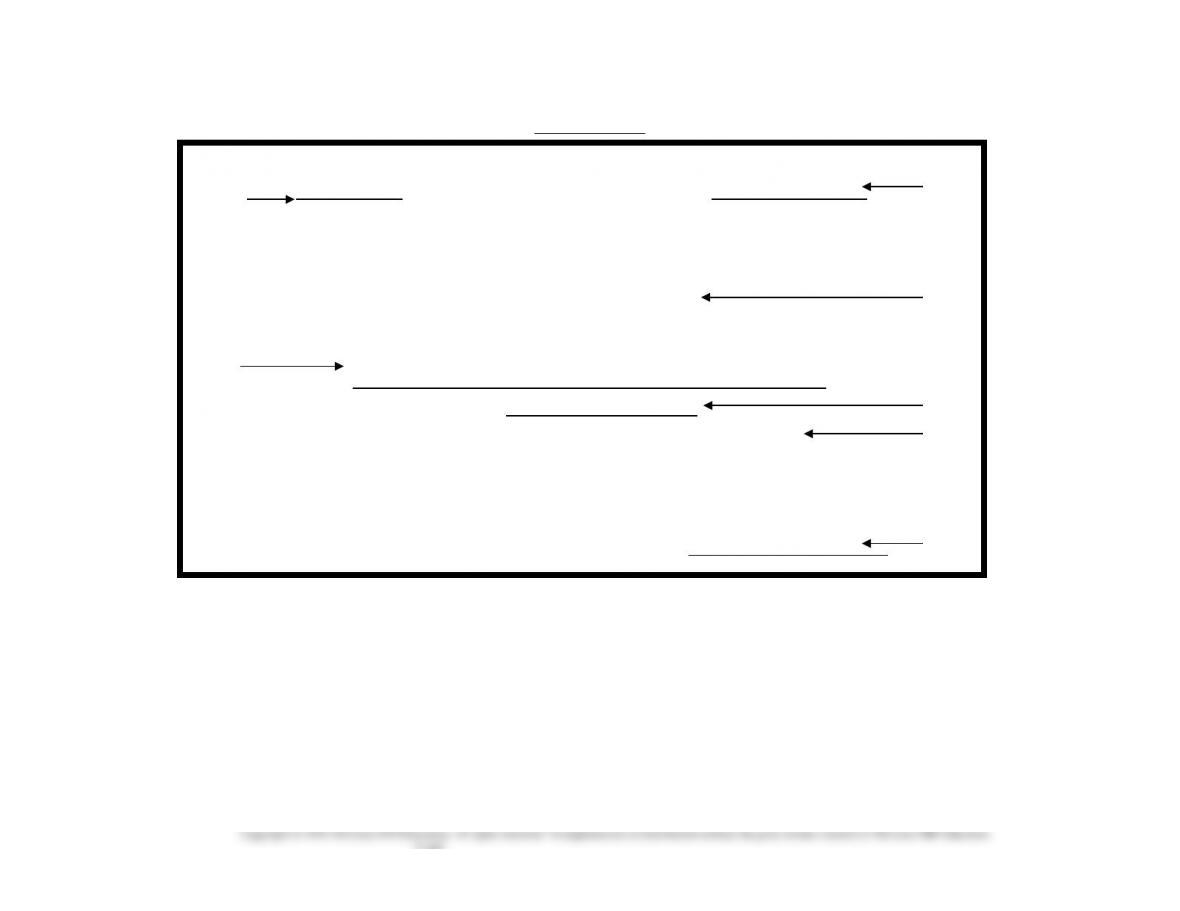

VISUAL #7-2

PROMISSORY NOTE

(6) $2,000.00 April 15, 2011 (1)

Amount Date

For value received, I promise to pay to the order of

Plexi-Plus Supply Co. (2)

Tobay, New York

(7)

Two thousand and no/100 ——————-Dollars

on June 14, 2011 (3)

plus interest at the annual rate of 9 percent.

(4)

Scott Cooke (5)

for Tobay Surfer Inc.

7-10

Alternate Demonstration Problem

Chapter 7

At the end of the year, the M. I. Wright Company showed the following

selected account balances:

Sales (all on credit)…………..……………..……………..….……….……….….$300,000

Accounts Receivable……………..……………..……………….….……….…… 800,000

Allowance for Doubtful Accounts…………………….………………………. 38,000

Required:

1. Assume the company estimates that 1% of all credit sales will not be

collected.

a. Prepare the proper journal entry to recognize the expense

involved.

b. Present the balances in Accounts Receivable and Allowance for

Doubtful Accounts as they would appear on the balance sheet.

Also show the net realizable Accounts Receivable.

2. Assume the company estimates that 5% of its accounts receivable

will never be collected.

a. Prepare the proper journal entry to recognize the expense

involved.

b. Present the balances in Accounts Receivable and Allowance for

Doubtful Accounts as they would appear on the balance sheet.

Also show the net realizable Accounts Receivable.

3. Under assumptions 1 and 2 above, give the proper journal entries for

the following events.

June 3 John Shifty, who owes us $500, informs us that

he is broke and cannot pay. We believe him.

Nov. 9 We learned that John Shifty has won the lottery and

is willing to pay off all his old debts.

Solution: Alternate Demonstration Problem

Chapter 7

1a. Bad Debts Expense………………………….….….… 3,000

Allowance for Doubtful Accounts………..… 3,000

($ 300,000 X 1 %)

($ 800,000 X 5 % less $38,000)

2b. Accounts Receivable………………..….…….……..$800,000

Less: Allowance for Doubtful Accounts........ 40,000

Estimated Realizable A/R……….……….…........$760,000

3. Both assumptions 1 and 2 above represent the allowance method of

accounting for uncollectibles. The only difference is in the approach

Note: There would be a closing entry for the Bad Debts Expense

since it is an expense account just like any other expense account.

There would be no closing entry for the Allowance for Doubtful

Accounts since it is not a temporary account. It is a contra-asset

account, contra to Accounts Receivable.