Chapter 6

Cash and Internal Controls

QUESTIONS

2. Internal control procedures become especially critical when the manager of a business

3. Responsibility for related transactions should be divided so that the work of one

department or individual acts as a check on that of another.

4. Separation of custody from recordkeeping of an asset encourages the asset custodian to

collusion necessary if an asset is to be stolen and the theft concealed in the records.

5. If individual departments were permitted to deal directly with suppliers, the amount of

amounts purchased and the resulting liabilities.

6. The limitations of internal control arise from two sources: the human element (human

error or human fraud) and the cost-benefit principle.

8. A petty cash receipt is a document stating that a payment has been made from petty

9. Depositing all receipts on the day of receipt (1) creates an independent record of the

the money for a period of time before depositing it.

10. During the year ended September 28, 2013, cash (and equivalents) of $33,774 million is

11. Google’s net income for 2013 was $12,920 million. Further, it reported a net increase in

cash (and equivalents) of $4,120 million. These two figures are different because (1) net

affect income, except through annual depreciation over the life of the asset.

12. Samsung’s cash (liquid assets) at December 31, 2013, equals 16,284,780 (all in KRW₩

millions). It is the fourth largest current asset and makes up about 14.7% of its current

assets.

13. Samsung’s cash and equivalents decreased by 2,506,680 million during 2013;₩

specifically, from 18,791,460 to 16,284,780 (all in KRW millions). Its statement of₩ ₩

QUICK STUDIES

Quick Study 6-1 (10 minutes)

1. True

Quick Study 6-2 (10 minutes)

Quick Study 6-3 (10 minutes)

a. False

d. False

Quick Study 6-4 (10 minutes)

1. (a) Petty Cash…………………………..……..…….…….…. 150

Cash…………………………………….……………... 150

To establish the petty cash fund.

To reimburse the petty cash fund.

2. Answers: a and c. The Petty Cash account is credited when:

Quick Study 6-5 (15 minutes)

Bank or Book Side Add or Subtract Adjusting Entry or Not

a. (1) Book (2) Add (3) Adjusting entry required

b. (1) Book (2) Subtract (3) Adjusting entry required

Quick Study 6-6 (25 minutes)

NOLAN COMPANY

Bank Reconciliation

June 30, 2015

Bank statement balance.... $21,332 Book balance……………………………………………………..........................$22,352

Add: Add:

Quick Study 6-7 (15 minutes)

a. A bank reconciliation is a formal review process that requires the person to

precisely identify all transactions and events, and their amounts, that

b. A bank reconciliation has the potential to uncover several kinds of frauds

or errors that an online review is unlikely to reveal. Those include the

following:

A company makes a deposit to its account but that deposit is incorrectly

added to another company’s account. A bank reconciliation would

The bank incorrectly pays a common vendor’s bill from the company’s

cash account, when that vendor should have been paid from some other

company’s account. Common vendors include utilities (light, heat,

person doing the online review remembers all amounts written to all

payees or that the amount is especially huge so that it is obvious. A

bank reconciliation would readily identify this bank error.

“jump out”; the only potential way of uncovering this error would be if

the person doing the review remembered the exact amounts of all bills

from all vendors during the period of the bank statement (not likely).

Numerous other examples can be listed…

Quick Study 6-8 (15 minutes)

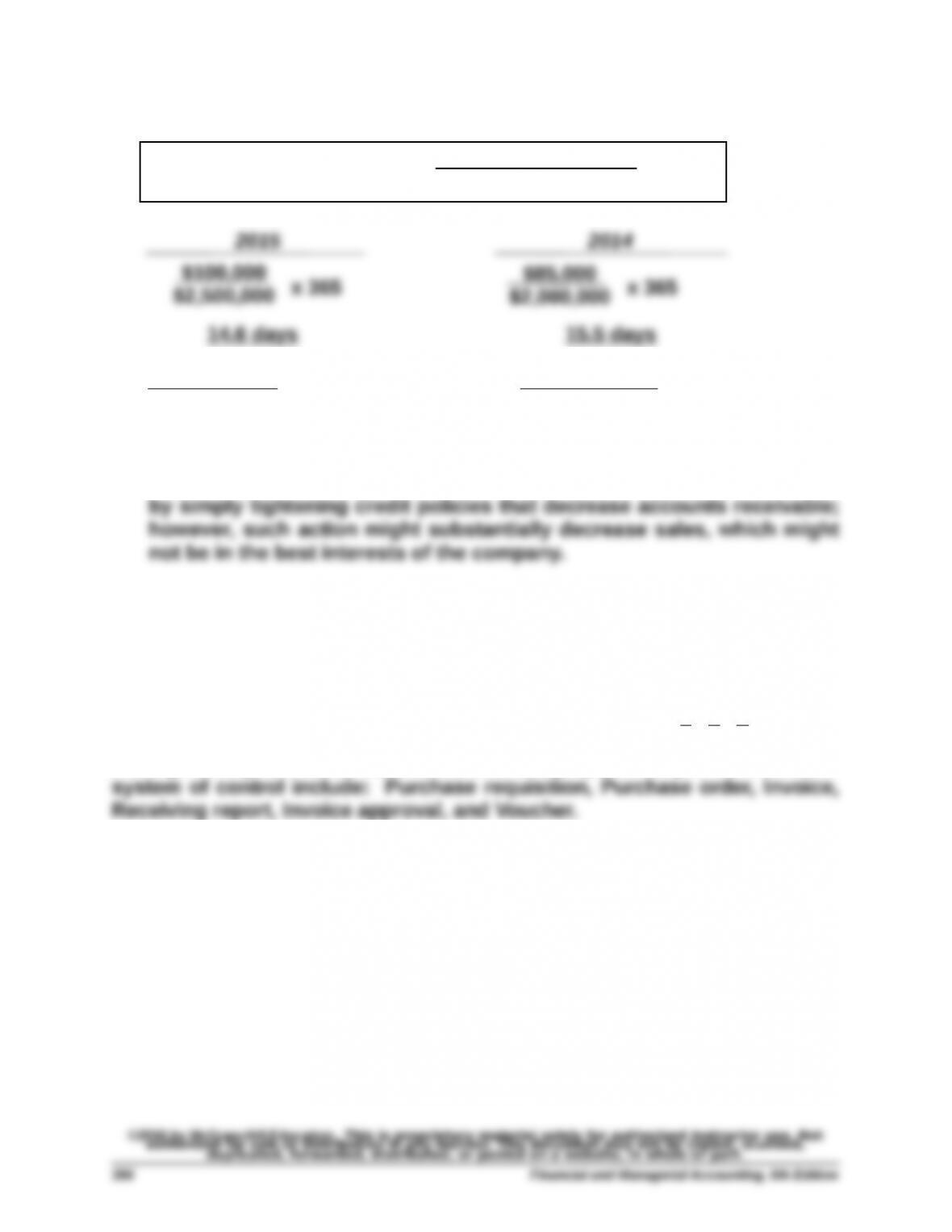

Days’ sales uncollected = x 365

Accounts receivable

Net sales

Quick Study 6-10B (15 minutes)

(a) A Discounts Lost account is employed with the Net Method of recording

purchases of inventory.

(b) The advantage of this method is that the Discounts Lost account

highlights for management (on the income statement) the costs

Quick Study 6-11 (10 minutes)

a. The purposes and principles of internal control systems are

fundamentally the same for accounting systems reporting under IFRS

b. Internal controls for cash are fundamentally the same worldwide.

EXERCISES

Exercise 6-1 (10 minutes)

Evaluation

The company’s internal control system failed to require separation of asset

custody from asset recordkeeping.

Principles Ignored

(1) The recordkeeper should not have been allowed to sign the company’s

checks.

Exercise 6-2 (15 minutes)

1. A cash register (with a locked record) should be used at the sales stand

—it should also be anchored to the stand. If a cash register cannot be

used, the total sales value of the towels, coolers, and sunglasses given

2. The employee should sign a receipt for the total amount of cash he or

she is given each weekend. Each time the employee makes a

purchase, he or she should obtain a signed sales receipt for the

Exercise 6-3 (10 minutes)

1. A liquid asset refers to an asset that can be readily converted into

another type of asset or be used to satisfy an obligation. A cash

2. Companies usually invest idle cash in cash equivalents to earn a higher

return on these assets.

3. Effective cash management applies the following five principles:

a. Encourages collection of receivables.

Exercise 6-4 (15 minutes)

(a) Internal Control Problems

(1) A major internal control problem is that the recordkeeper (who has

(2) The recordkeeper might also delay recording a cash receipt from a

customer until more cash comes in at a later date from a second

(3) The recordkeeper also could pocket cash and claim that a payment was

never received and apparently lost in the mail.

(b) Internal Control Recommendations

(1) If only one person is present when the mail is opened, that person may

steal cash and claim it was never received. If possible, two people

(2) It is important the recordkeeper not have physical control over cash.

Exercise 6-5 (20 minutes)

1.

Sept. 9 Petty Cash…………….………………………..…….…….…. 350

Cash…………………………………..……………….……. 350

To establish a $350 petty cash fund.

2.

Sept. 30 Merchandise Inventory*……………….……….…….….. 40

Postage Expenses…………….……………………….…… 123

3.

Oct. 1 Petty Cash…………………..……………………….….…….. 50

Cash…………………………………..……………….……. 50

To increase the petty cash fund to $400.