Problem 5-9AB (25 minutes)

Part 1

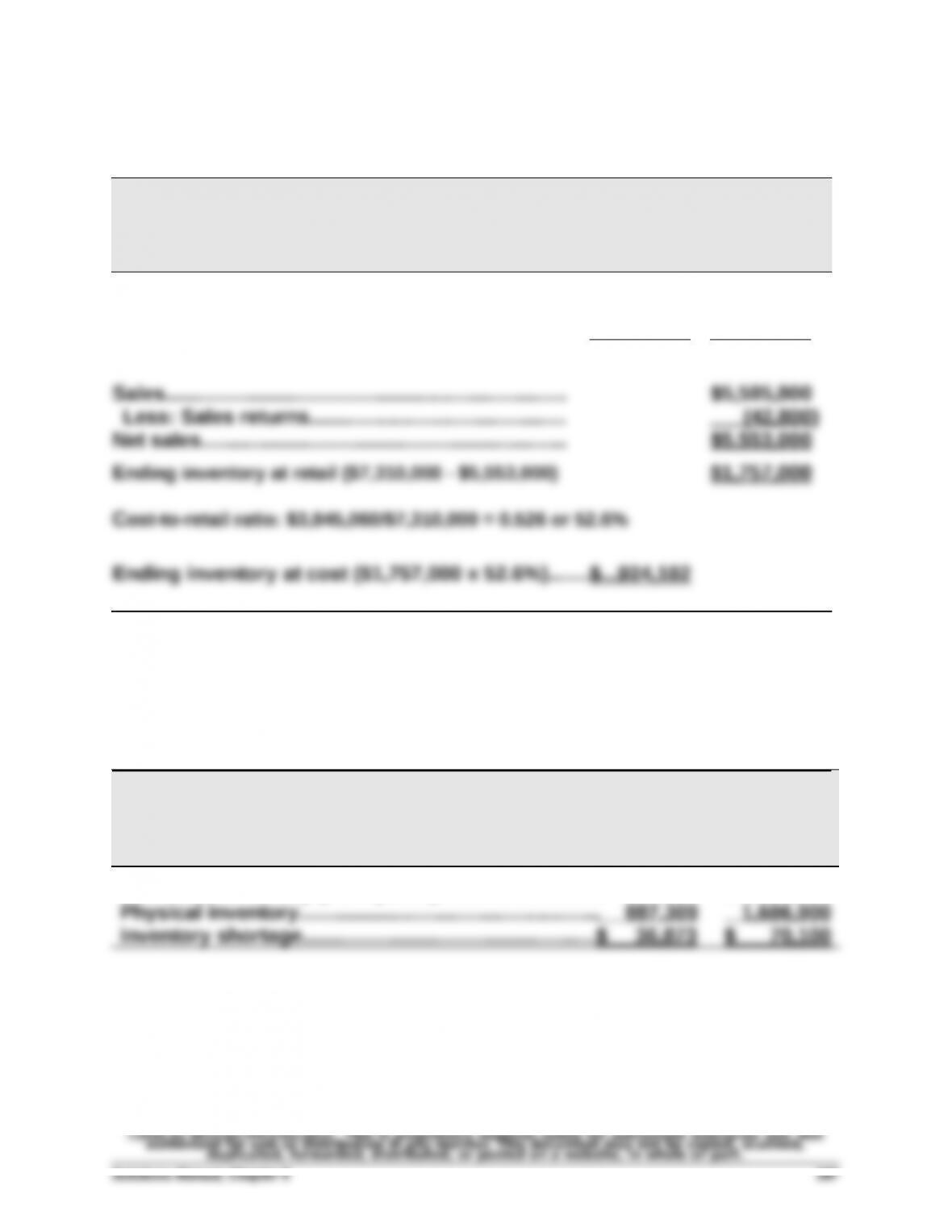

ALASKA COMPANY

Estimated Inventory

December 31

At Cost At Retail

Goods available for sale

Beginning inventory………………………….…….…... $ 469,010 $ 928,950

Cost of goods purchased…………….….……..……. 3,376,050 6,381,050

Goods available for sale

……………………………….

$3,845,060 $7,310,000

Part 2

Estimated physical inventory at cost: $1,686,900 x 52.6% = $887,309

ALASKA COMPANY

Inventory Shortage

December 31

At Cost At Retail

Estimated inventory (from part 1)………………………..$ 924,182 $ 1,757,000

Problem 5-10AB (25 minutes)

WAYWARD COMPANY

Estimated Inventory at March 31

Goods available for sale

Inventory, January 1………………….….….….….……..$ 302,580

Cost of goods purchased……………………………….. 941,040

Goods available for sale…………………………………. 1,243,620

Less estimated cost of goods sold

Estimated March 31 inventory…………………….….….$ 449,805

PROBLEM SET B

Problem 5-1B (40 minutes)

1. Compute cost of goods available for sale and units available for sale

Beginning inventory………..….….……... 20 units @ $3,000 $ 60,000

April 6…………………………………………… 30 units @ $3,500 105,000

2. Units in ending inventory

Problem 5-1B (Continued)

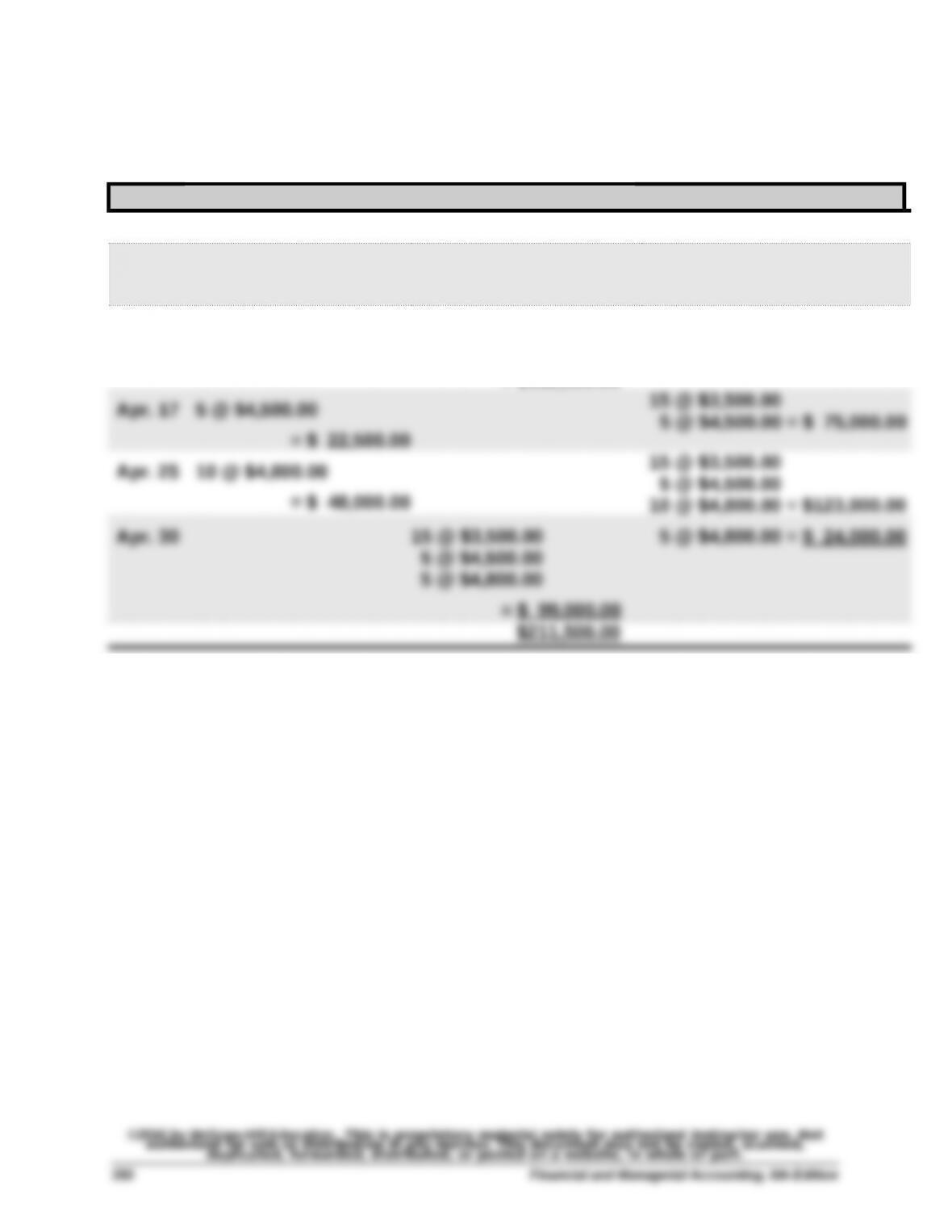

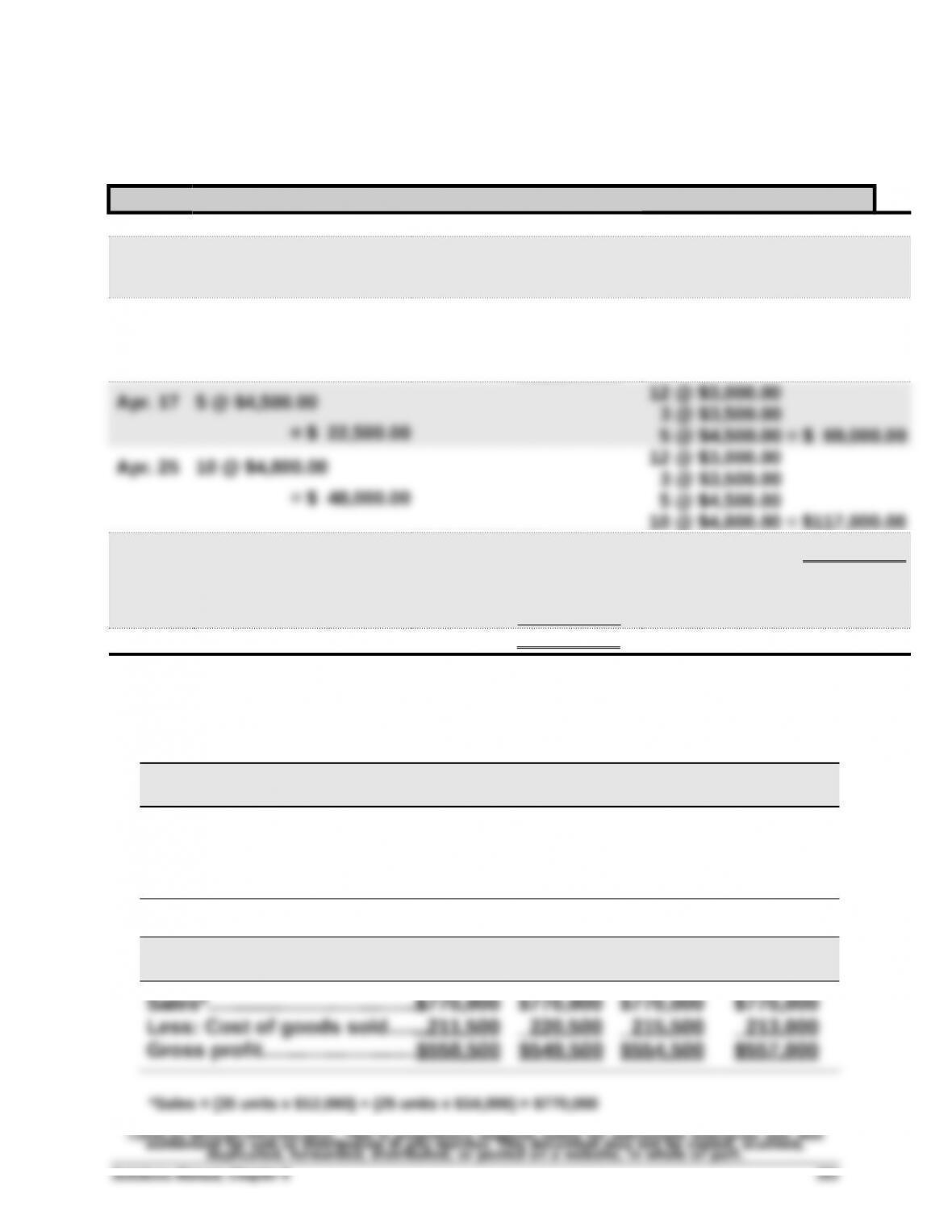

3a. FIFO perpetual

Date Goods Purchased Cost of Goods Sold Inventory Balance

Apr. 1 20 @ $3,000.00 = $ 60,000.00

Apr. 6 30 @ $3,500.00

= $105,000.00

20 @ $3,000.00

30 @ $3,500.00 = $165,000.00

Apr. 9 20 @ $3,000.00

15 @ $3,500.00

= $112,500.00

15 @ $3,500.00 = $ 52,500.00

15 @ $3,500.00

Problem 5-1B (Continued)

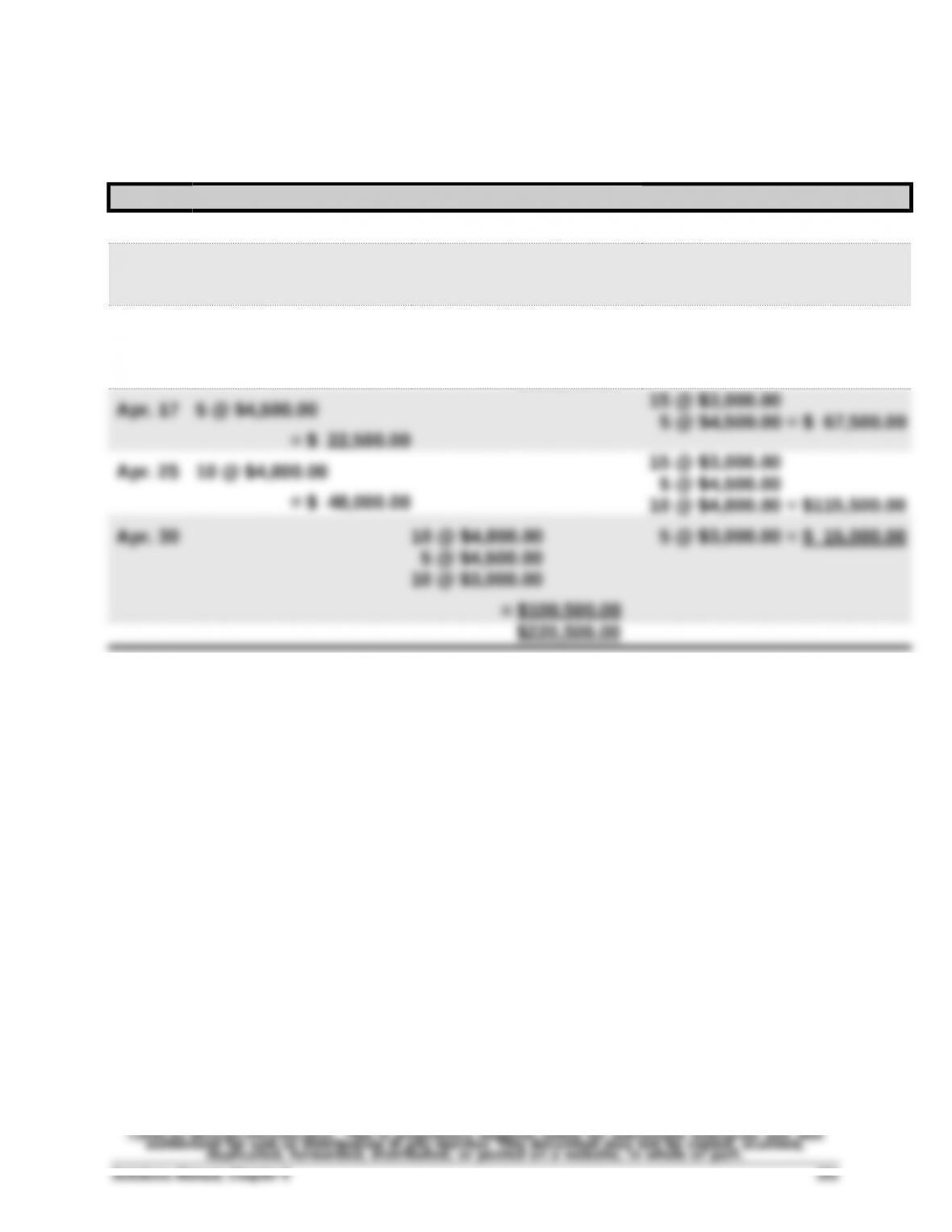

3b. LIFO perpetual

Date Goods Purchased Cost of Goods Sold Inventory Balance

Apr. 1 20 @ $3,000.00 = $ 60,000.00

Apr. 6 30 @ $3,500.00

= $105,000.00

20 @ $3,000.00

30 @ $3,500.00 = $165,000.00

Apr. 9 30 @ $3,500.00

5 @ $3,000.00

= $120,000.00

15 @ $3,000.00 = $ 45,000.00

15 @ $3,000.00

Problem 5-1B (Continued)

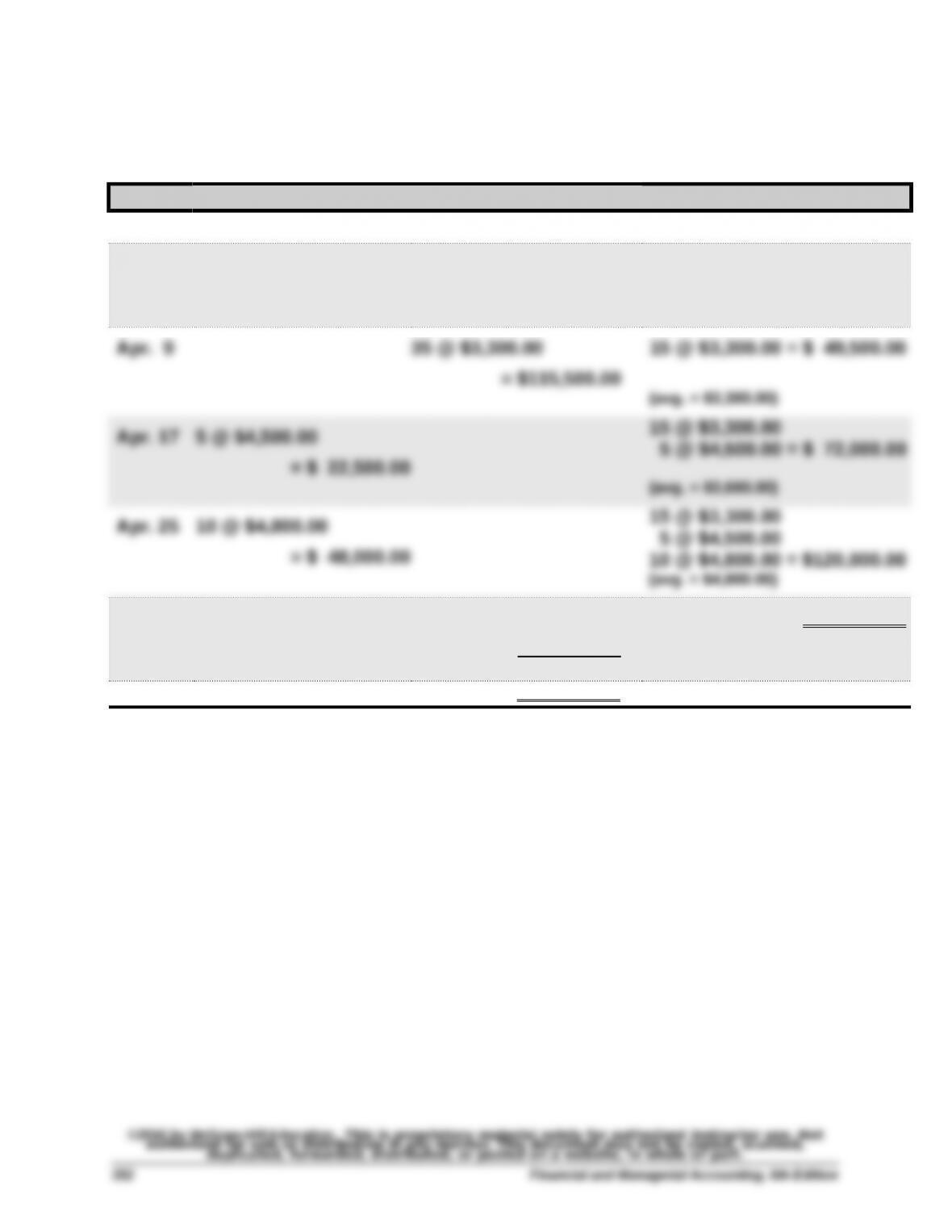

3c. Weighted Average perpetual

Date Goods Purchased Cost of Goods Sold Inventory Balance

Apr. 1 20 @ $3,000.00 = $ 60,000.00

Apr. 6 30 @ $3,500.00

= $105,000.00

20 @ $3,000.00

30 @ $3,500.00 = $165,000.00

(avg. = $3,300.00)

Apr. 30 25 @ $4,000.00

= $100,000.00

5 @ $4,000.00 = $ 20,000.00

(avg. = $4,000.00)

$215,500.00

Problem 5-1B (Concluded)

3d. Specific Identification

Date Goods Purchased Cost of Goods Sold Inventory Balance

Apr. 1 20 @ $3,000.00 = $ 60,000.00

Apr. 6 30 @ $3,500.00

= $105,000.00

20 @ $3,000.00

30 @ $3,500.00 = $165,000.00

Apr. 9 8 @ $3,000.00

27 @ $3,500.00

= $118,500.00

12 @ $3,000.00

3 @ $3,500.00 = $ 46,500.00

12 @ $3,000.00

Apr. 30 12 @ $3,000.00

3 @ $3,500.00

10 @ $4,800.00

= $ 94,500.00

5 @ $4,500.00 = $ 22,500.00

$213,000.00

Specific identification—Alternative Computation

Cost of goods sold—20 [8+12] units from beginning inventory, 30 [27+3] units from

April 6 purchase, and 10 units from April 25 purchase

Ending Cost of

Specific Identification Inventory Goods Sold

(20 x $3,000) + (30 x $3,500) + (10 x $4,800)….….…. $213,000

$235,500 [Total Goods Available] – $213,000 [Cost of Goods Sold]. . $22,500

4.

FIFO LIFO

Weighted

Average

Specific

Identification

1. Compute cost of goods available for sale and units available for sale

Beginning inventory………..….….……... 20 units @ $3,000 $ 60,000

April 6…………………………………………… 30 units @ $3,500 105,000

2. Units in ending inventory

3.

Periodic Inventory

Ending

Inventory

Cost of

Goods Sold

a. FIFO

(5 x $4,800)…………………………….………………………… $24,000.00

(20x$3,000)+(30x$3,500)+(5x$4,500)+(5x$4,800)... $211,500.00

b. LIFO

(5 x $3,000)…………………………….….…….…….….……. $15,000.00

(15x$3,000)+(30x$3,500)+(5x$4,500)+(10x$4,800). $220,500.00

Problem 5-2B (Concluded)

4.

FIFO LIFO

Weighted

Average

Specific

Identifi-

cation

Sales*………………………….……..$770,000 $770,000 $770,000.00 $770,000

Problem 5-3B (40 minutes)

1. Compute cost of goods available for sale and units available for sale

Beginning inventory………..….….……... 150 units @ $300 $ 45,000

May 6………………..………………..……..…. 350 units @ $350 122,500

2. Units in ending inventory

Units available (from part 1)…………….….……..680 units

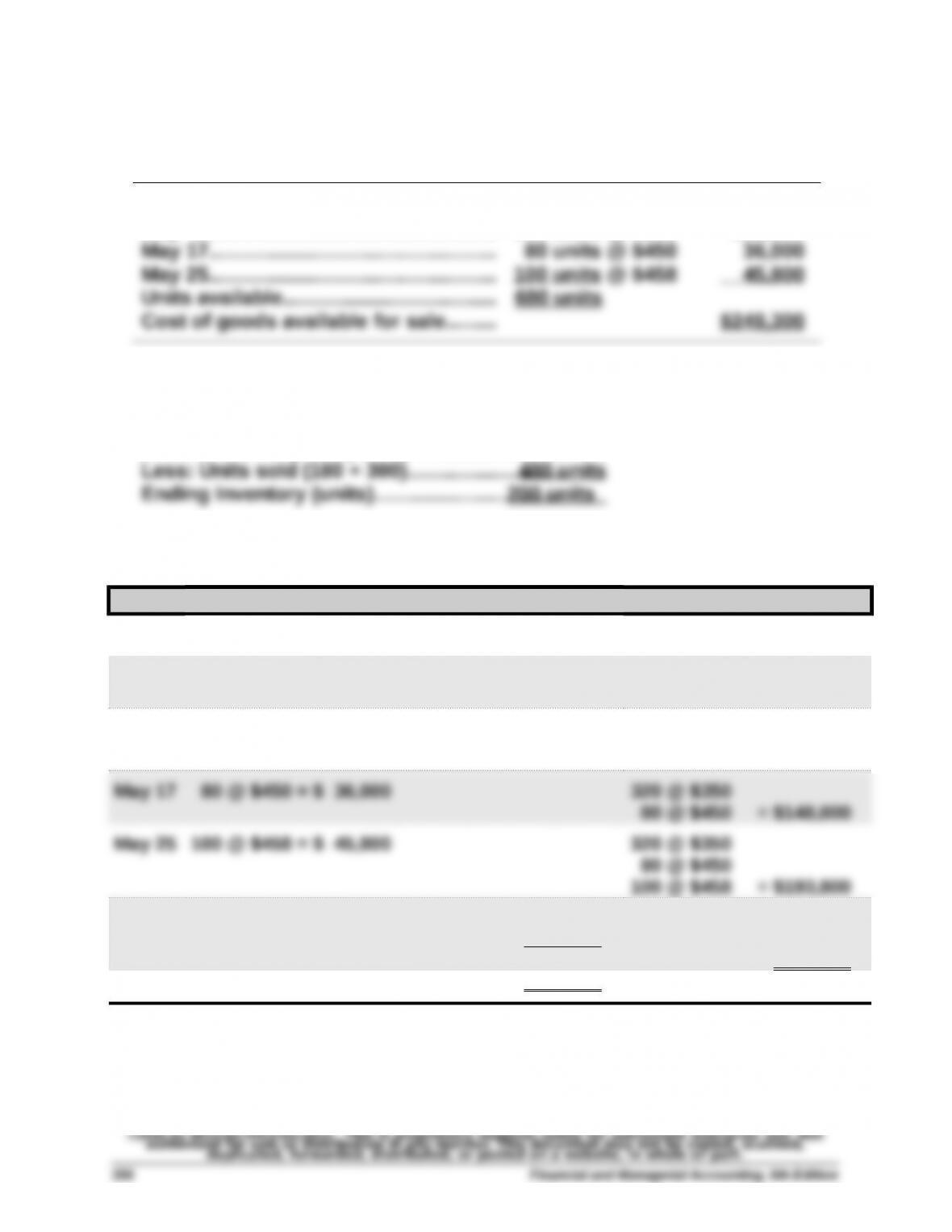

3a. FIFO perpetual

Date Goods Purchased Cost of Goods Sold Inventory Balance

May 1 150 @ $300 = $ 45,000

May 6 350 @ $350 = $122,500 150 @ $300

350 @ $350 = $167,500

May 9 150 @ $300 = $ 45,000

30 @ $350 = $ 10,500

320 @ $350 = $112,000

May 30 300 @ $350 = $105,000

20 @ $350

80 @ $450

100 @ $458 = $ 88,800

$160,500