Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

Exercise 5-13 (20 minutes)

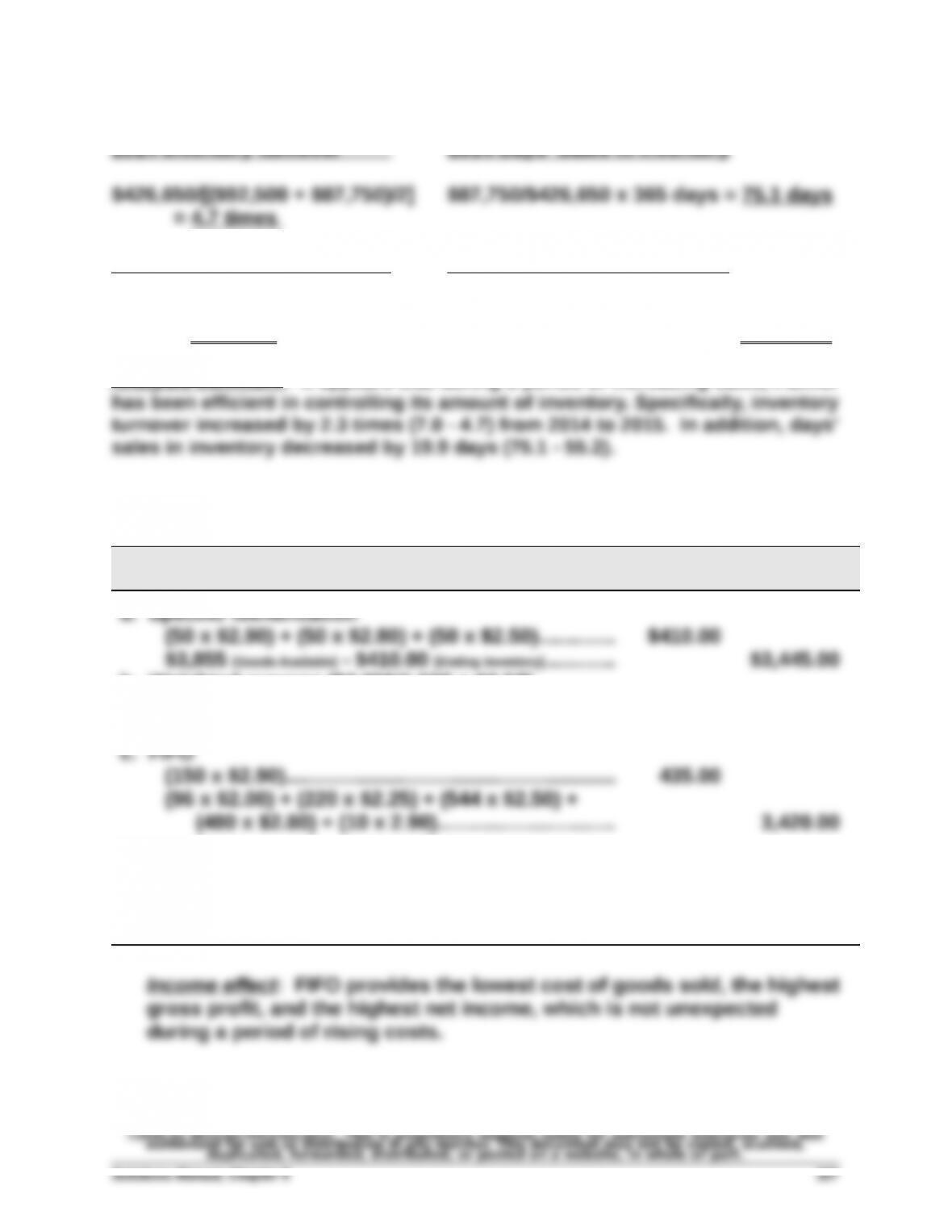

2015 Inventory turnover 2015 Days' Sales in Inventory

$643,825/[($87,750 + $97,400)/2]

= 7.0 times $97,400/$643,825 x 365 days = 55.2 days

Analysis comment: It appears that during a period of increasing sales, Palmer

Exercise 5-14A (20 minutes)

Ending

Inventory

Cost of

Goods Sold

b. Weighted average ($3,855/1,500 = $2.57)

150 x $2.57 [rounded to cents]........................................ 385.50

$3,855 [Goods Available] - $385.50 [Ending Inventory]............ 3,469.50

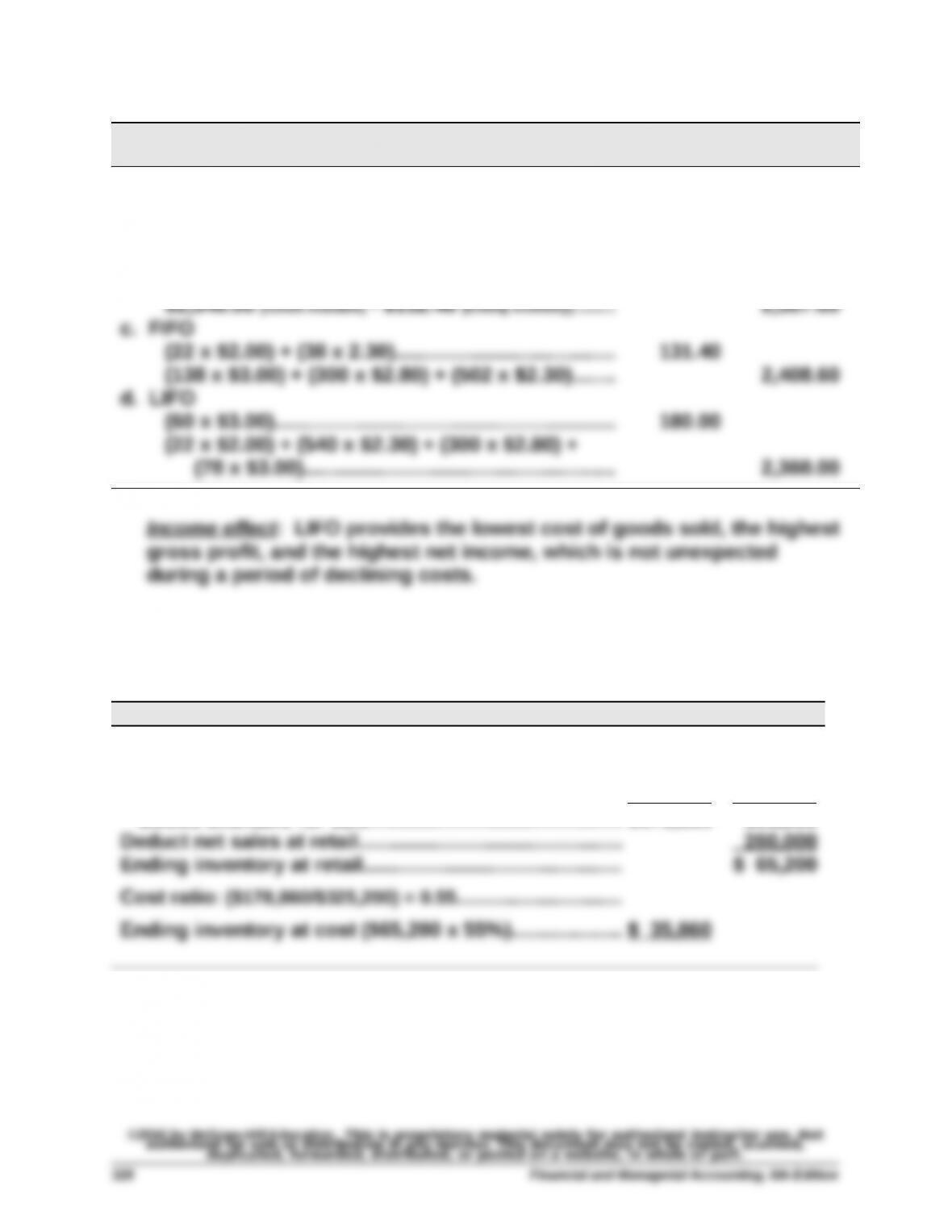

d. LIFO

(96 x $2.00) + (54 x $2.25)..................................... 313.50

(160 x $2.90) + (480 x $2.80) + (544 x $2.50) +

(166 x $2.25)..................................................... 3,541.50

Exercise 5-15A (20 minutes)

Periodic Inventory

Ending

Inventory

Cost of

Goods Sold

a. Specific Identification

(50 x $2.80) + (10 x $2.00)..................................... $160.00

$2,540.00 [Goods Available] - $160.00 [Ending Inventory]....... $2,380.00

b. Weighted Average ($2,540.00/1,000 = $2.54)

(60 x $2.54)............................................................. 152.40

Exercise 5-16B (20 minutes)

At Cost At Retail

Goods available for sale

Beginning inventory................................................... $ 63,800 $128,400

Cost of goods purchased........................................... 115,060 196,800

Goods available for sale............................................. $178,860 325,200

Exercise 5-17B (20 minutes)

Goods available for sale

Inventory, January 1......................................................$ 225,000

Net cost of goods purchased*...................................... 802,250

Goods available for sale...............................................1,027,250

Exercise 5-18 (15 minutes)

1. Samsung generally applies the (weighted) average cost assumption when

transit.

2. Under IFRS, Samsung would reverse inventory valuation losses if

inventory values increased in subsequent periods. Specifically, it would

PROBLEM SET A

Problem 5-1A (40 minutes)

1. Compute cost of goods available for sale and units available for sale

Beginning inventory............................100 units @ $50.00 $ 5,000

March 5................................................400 units @ $55.00 22,000

2. Units in ending inventory

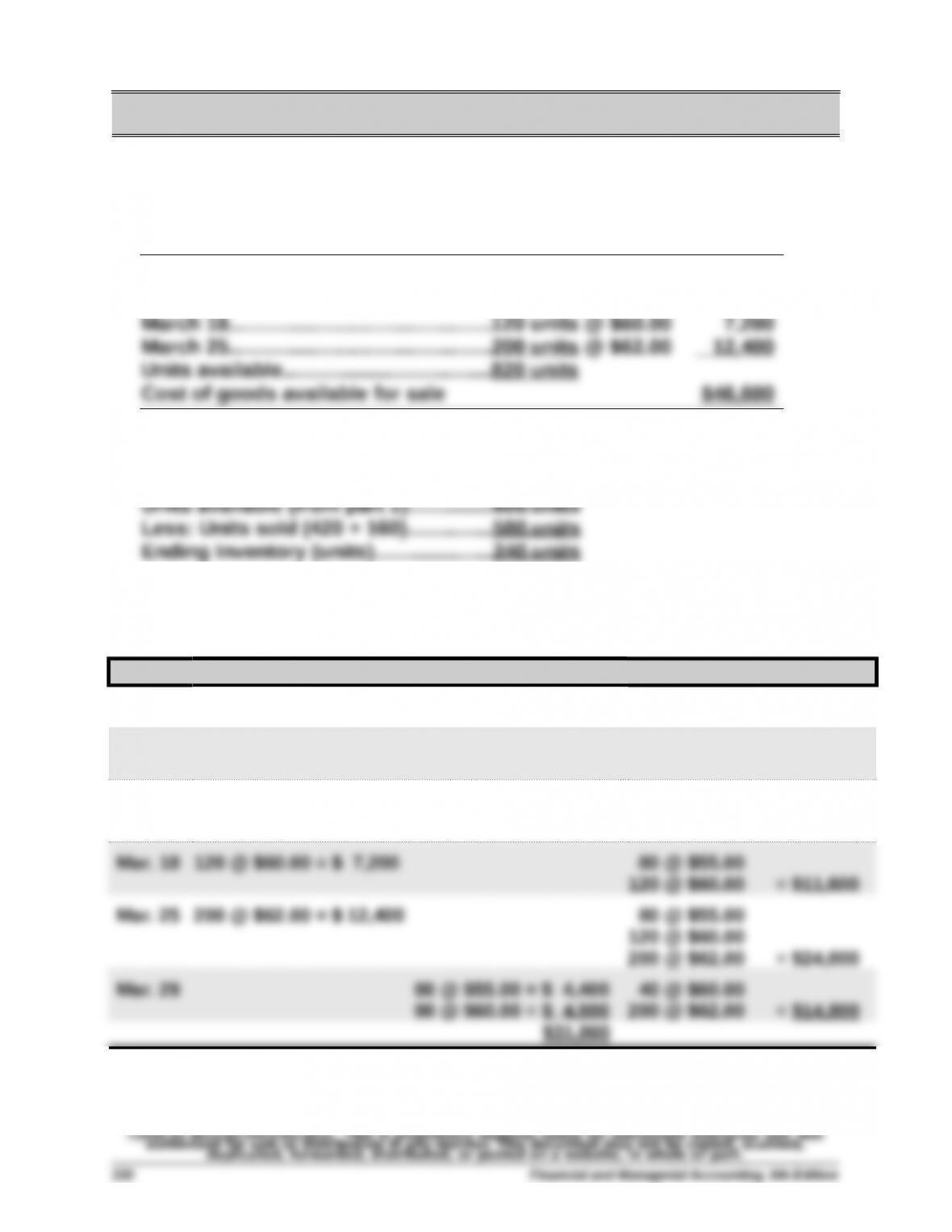

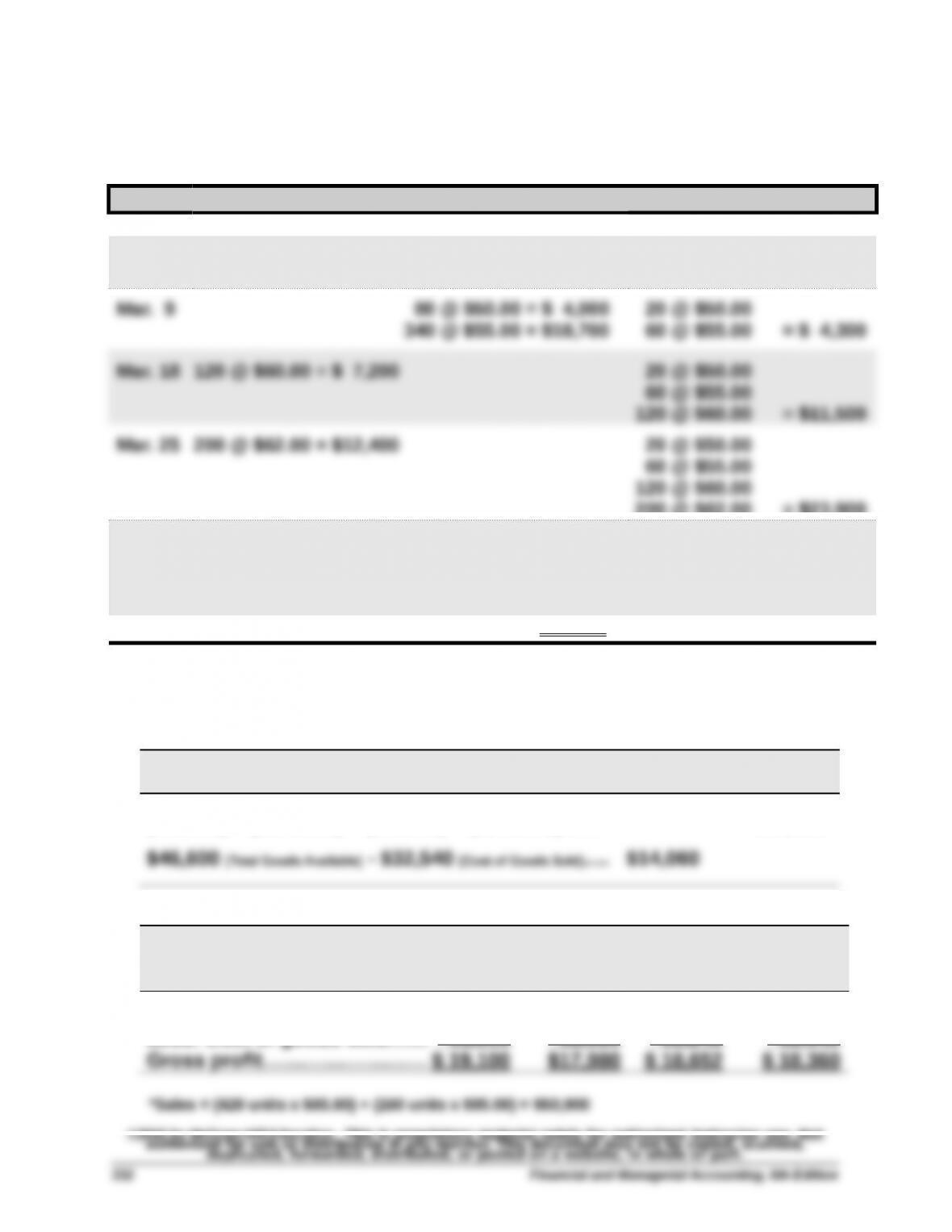

3a. FIFO perpetual

Date Goods Purchased Cost of Goods Sold Inventory Balance

Mar. 1 100 @ $50.00 = $5,000

Mar. 5 400 @ $55.00 = $22,000 100 @ $50.00

400 @ $55.00 = $27,000

Mar. 9 100 @ $50.00 = $ 5,000

320 @ $55.00 = $17,600

80 @ $55.00 = $ 4,400

Problem 5-1A (Continued)

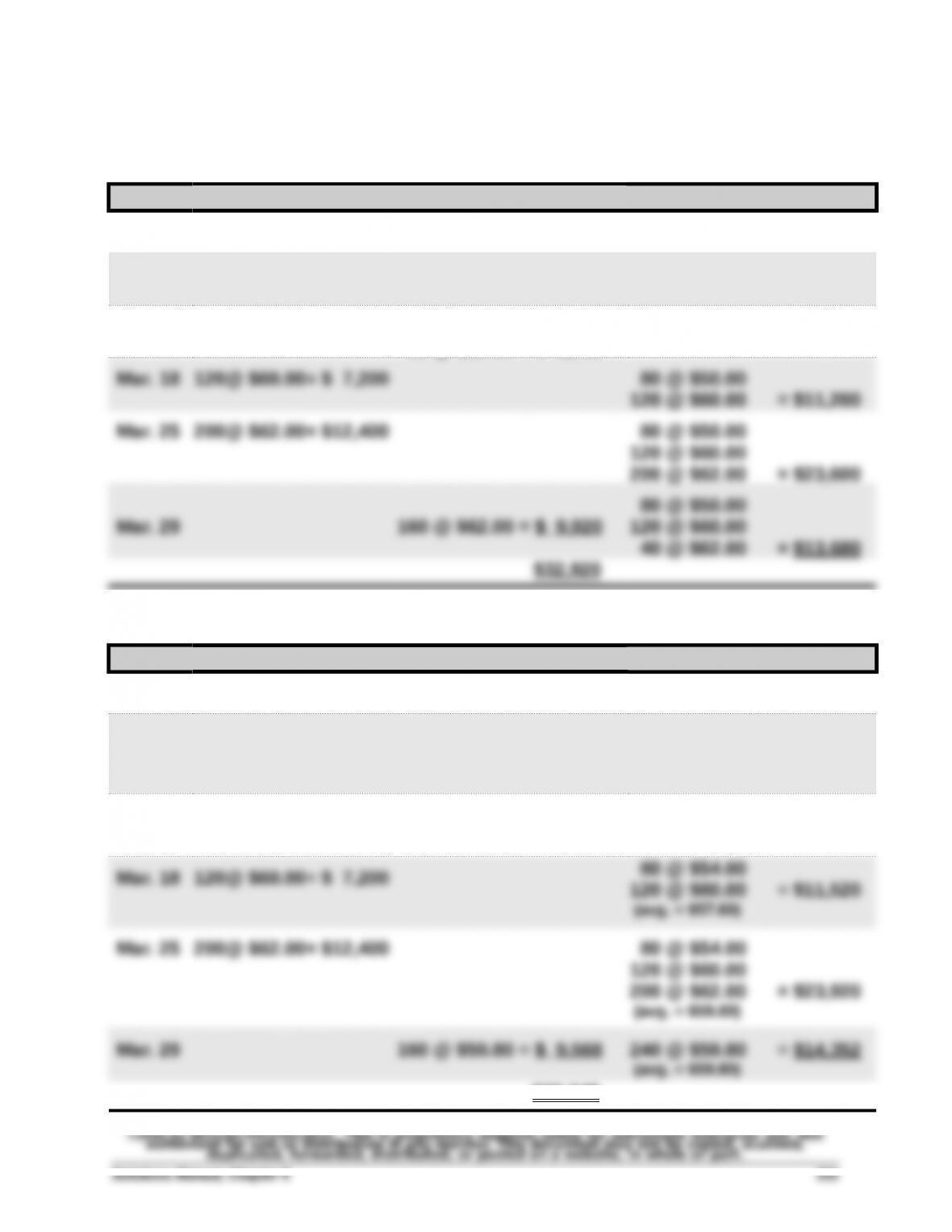

3b. LIFO perpetual

Date Goods Purchased Cost of Goods Sold Inventory Balance

Mar. 1 100 @ $50.00 = $ 5,000

Mar. 5 400@ $55.00= $22,000 100 @ $50.00

400 @ $55.00 = $27,000

Mar. 9 400 @ $55.00 = $22,000

20 @ $50.00 = $ 1,000

80 @ $50.00 = $ 4,000

3c. Weighted Average perpetual

Date Goods Purchased Cost of Goods Sold Inventory Balance

Mar. 1 100 @ $50.00 = $ 5,000

Mar. 5 400@ $55.00= $22,000 100 @ $50.00

400 @ $55.00 = $27,000

(avg. = $54.00)

Mar. 9 420 @ $54.00 = $22,680 80 @ $54.00 = $ 4,320

(avg. = $54.00)

$32,248

Problem 5-1A (Concluded)

3d. Specific Identification

Date Goods Purchased Cost of Goods Sold Inventory Balance

Mar. 1 100 @ $50.00 = $ 5,000

Mar. 5 400 @ $55.00 = $22,000 100 @ $50.00

400 @ $55.00 = $27,000

200 @ $62.00 = $23,900

Mar. 29 40 @ $60.00 = $ 2,400

120 @ $62.00 = $ 7,440

20 @ $50.00

60 @ $55.00

80 @ $60.00

80 @ $62.00 = $14,060

$32,540

Specific identification—Alternative Computation

Cost of goods sold—80 units from beginning inventory, 340 units from March 5

purchase, 40 units from March 18 purchase, and 120 units from March 25 purchase

Ending Cost of

Specific Identification Inventory Goods Sold

(80x$50) + (340x$55) + (40x$60) + (120x$62)........ $32,540

4.

FIFO LIFO

Weighted

Average

Specific

Identifi-

cation

Sales*....................................... $50,900 $50,900 $50,900 $50,900

Less: Cost of goods sold....... 31,800 32,920 32,248 32,540

Problem 5-2A (40 minutes)

1. Compute cost of goods available for sale and units available for sale

Beginning inventory............................100 units @ $50.00 $ 5,000

2. Units in ending inventory

3.

Periodic Inventory

Ending

Inventory

Cost of

Goods Sold

a. FIFO

(200 x $62.00) + (40 x $60.00)............................... $14,800.00

(100 x $50.00) + (400 x $55.00) + (80 x $60.00).. . $31,800.00

b. LIFO

(100 x $50.00) + (140 x $55.00)............................. $12,700.00

(200 x $62.00) + (120 x $60.00) + (260 x $55.00). $33,900.00

Problem 5-2A (Concluded)

4.

FIFO LIFO

Weighted

Average

Specific

Identifi-

cation

Sales*.......................................$50,900.00 $50,900.00 $50,900.00 $50,900.00

Problem 5-3A (40 minutes)

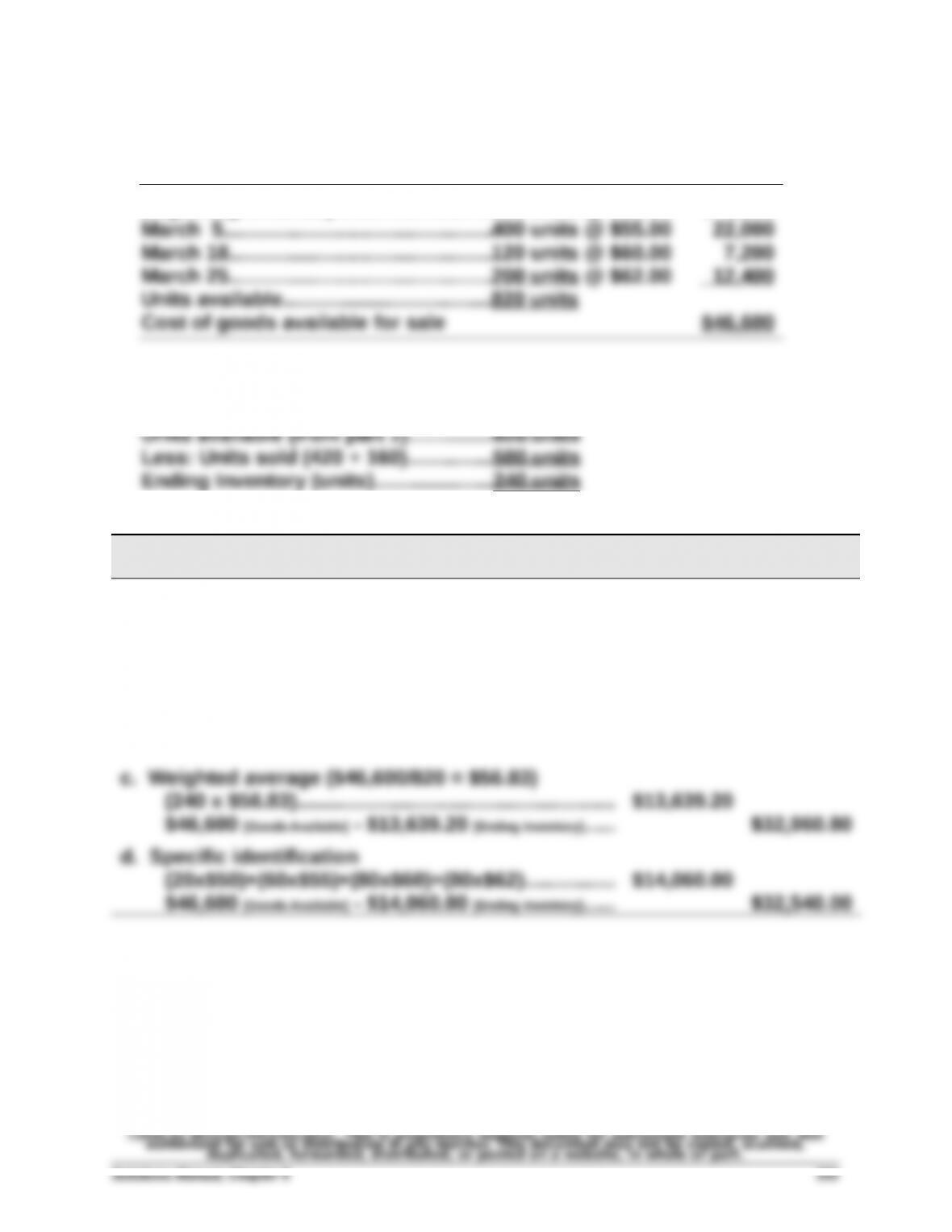

1. Calculate cost of goods available for sale and units available for sale

Beginning inventory............................ 600 units @ $45.00 $27,000

Feb. 10.................................................. 400 units @ $42.00 16,800

Mar. 13.................................................. 200 units @ $27.00 5,400

2. Units in ending inventory

Units available (from part 1)............................1,800

Problem 5-3A (Continued)

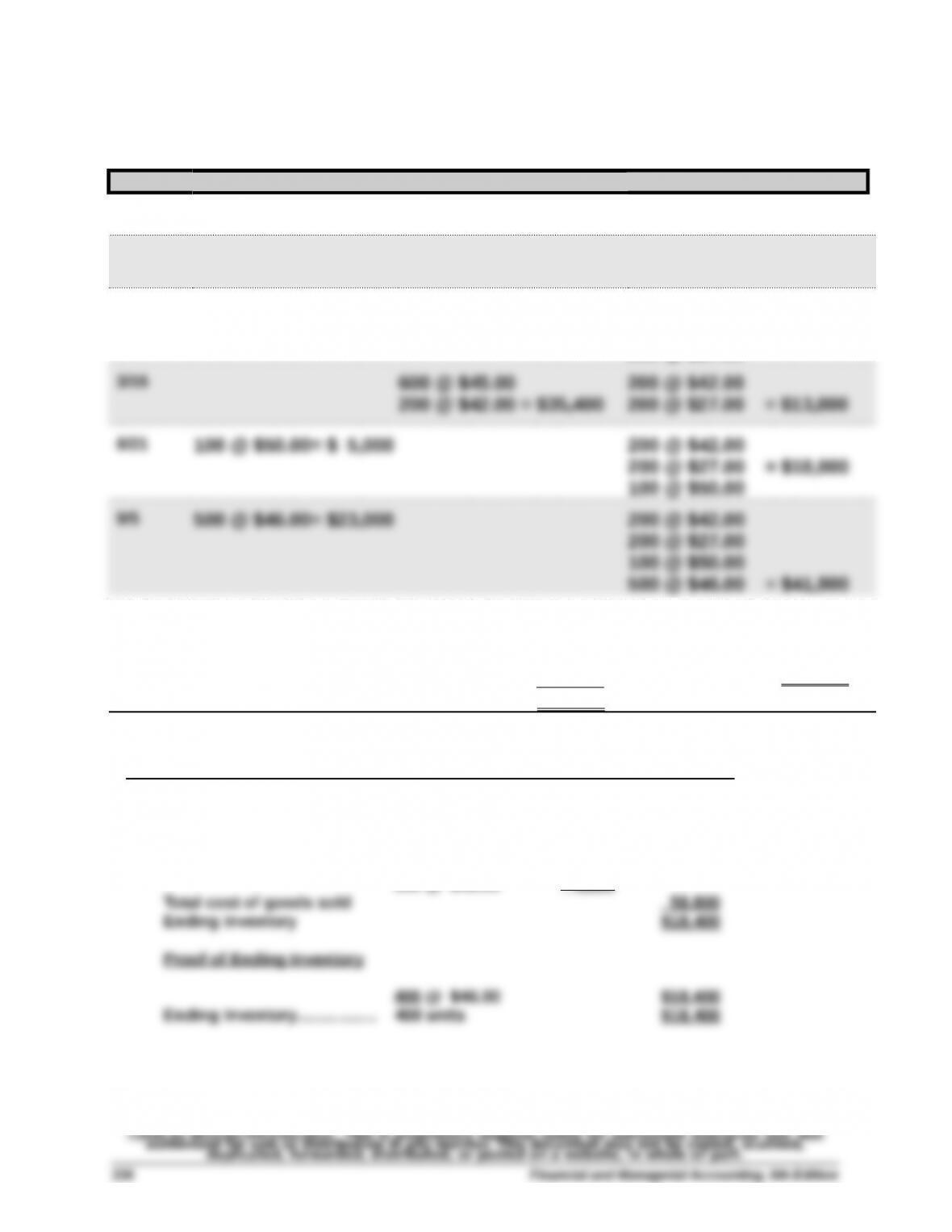

3a. FIFO perpetual

Date Goods Purchasd Cost of Goods Sold Inventory Balance

1/1 600 @ $45.00 = $27,000

2/10 400 @ $42.00= $16,800 600 @ $45.00

400 @ $42.00 = $43,800

3/13 200 @ $27.00= $ 5,400 600 @ $45.00

400 @ $42.00 = $49,200

200 @ $27.00

9/10 200 @ $42.00

200 @ $27.00

100 @ $50.00

100 @ $46.00 = $23,400 400 @ $46.00 = $18,400

$58,800

FIFO Alternate Solution Format

Cost of goods available for sale $77,200

Less: Cost of sales 600 @ $45.00 $27,000

400 @ $42.00 16,800

200 @ $27.00 5,400

100 @ $50.00 5,000

100 @ $46.00 4,600