Quick Study 5-22B (15 minutes)

Goods available for sale

Inventory, January 1………………….……………..…………………………..$190,000

Cost of goods purchased (net)…………………………………….….…… 352,000

Goods available for sale (at cost)……….……………….……..….……..542,000

Quick Study 5-23 (10 minutes)

a. Both IFRS and U.S. GAAP provide broad and similar guidance on the

accounting for items and costs making up merchandise inventory.

b. Yes, companies reporting under IFRS can apply cost flow assumptions

in assigning costs to inventory. FIFO and weighted average are two

IFRS. (LIFO is not presently acceptable under IFRS.)

c. U.S. GAAP prohibits any later increase in the recorded value of

inventory that had been written down even if that decline in value is

EXERCISES

Exercise 5-1 (10 minutes)

1. The title will pass at “destination” which is Harlow Company’s

2. The consignor is Harris Company. The consignee is Harlow Company.

Exercise 5-2 (10 minutes)

Cost of inventory (estate’s contents)

Price……………………………..…………..………….….…….…….….…. $75,000

Transportation-in…………………………..……………………………… 2,400

Exercise 5-3 (45 minutes)

a. Specific identification

Ending inventory—180 units from January 30, 5 units from January 20, and 15

units from beginning inventory

Ending Cost of

Specific Identification Inventory Goods Sold

(180 x $4.50) + (5 x $5.00) + (15 x $6.00)......... $ 925

Exercise 5-3 (continued)

b. Weighted Average—Perpetual

Date Goods Purchased Cost of Goods Sold Inventory Balance

1/1 140 @ $6.00 = $ 840.00

1/10 100 @ $6.00 = $ 600.00 40 @ $6.00 = $ 240.00

1/20 60 @ $5.00 40 @ $6.00 = $ 540.00

60 @ $5.00

(avg. cost is $5.40)

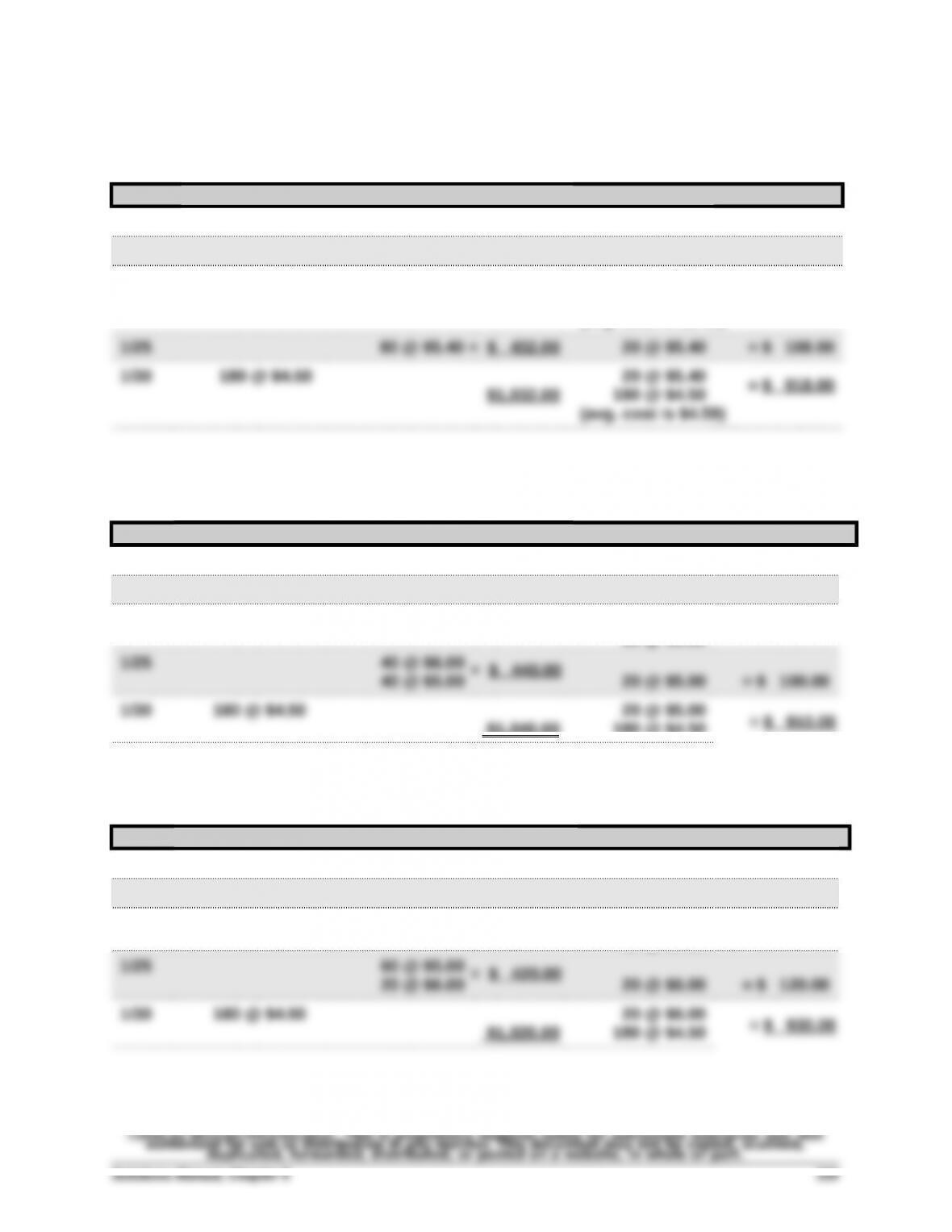

c. FIFO—Perpetual

Date Goods Purchased Cost of Goods Sold Inventory Balance

1/1 140 @ $6.00 = $ 840.00

1/10 100 @ $6.00 = $ 600.00 40 @ $6.00 = $ 240.00

1/20 60 @ $5.00 40 @ $6.00 = $ 540.00

60 @ $5.00

$1,040.00 180 @ $4.50

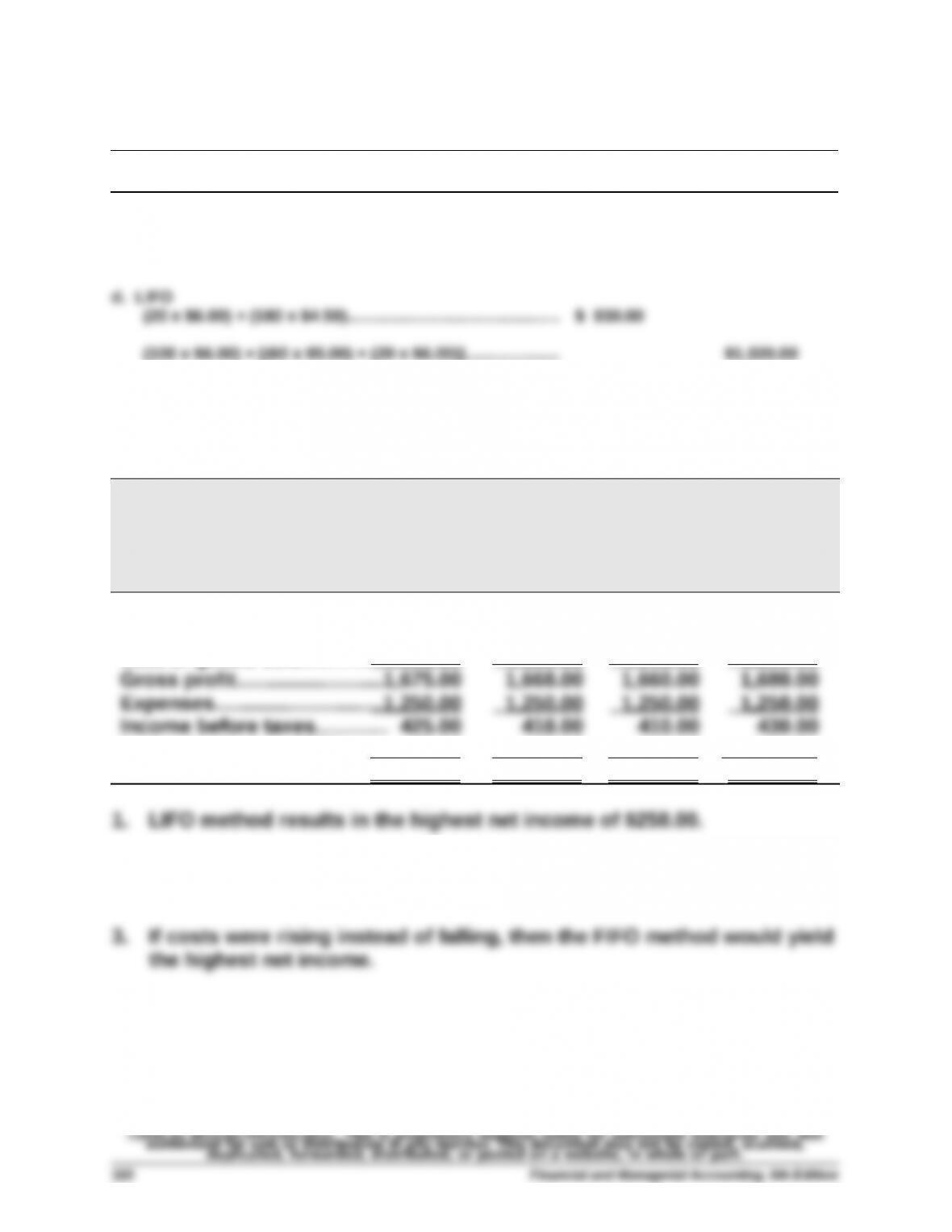

d. LIFO—Perpetual

Date Goods Purchased Cost of Goods Sold Inventory Balance

1/1 140 @ $6.00 = $ 840.00

1/10 100 @ $6.00 = $ 600.00 40 @ $6.00 = $ 240.00

1/20 60 @ $5.00 40 @ $6.00 = $ 540.00

60 @ $5.00

20 @ $6.00 20 @ $6.00 = $ 120.00

1/30 180 @ $4.50 20 @ $6.00 = $ 930.00

$1,020.00 180 @ $4.50

©2016 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not

authorized for sale or distribution in any manner. This document may not be copied, scanned,

duplicated, forwarded, distributed, or posted on a website, in whole or part.

Solutions Manual, Chapter 5 319

Exercise 5-3 (Concluded)

Alternate Solution Format for FIFO and LIFO Perpetual

Ending Cost of

Computations Inventory Goods Sold

c. FIFO

(180 x $4.50) + (20 x $5.00)……….………..………….…………. $ 910.00

(100 x $6.00) + (40 x $6.00) + (40 x $5.00)…………..….….. $1,040.00

Exercise 5-4 (20 minutes)

LAKER COMPANY

Income Statements

For Month Ended January 31

Specific

Identification

Weighted

Average FIFO LIFO

Sales……………..….…….….……$2,700.00 $2,700.00 $2,700.00 $2,700.00

(180 units x $15 price)

Cost of goods sold……..….… 1,025.00 1,032.00 1,040.00 1,020.00

Income tax expense (40%)….…..

170.00 167.20 164.00 172.00

Net income…………..…….…….$ 255.00 $ 250.80 $ 246.00 $ 258.00

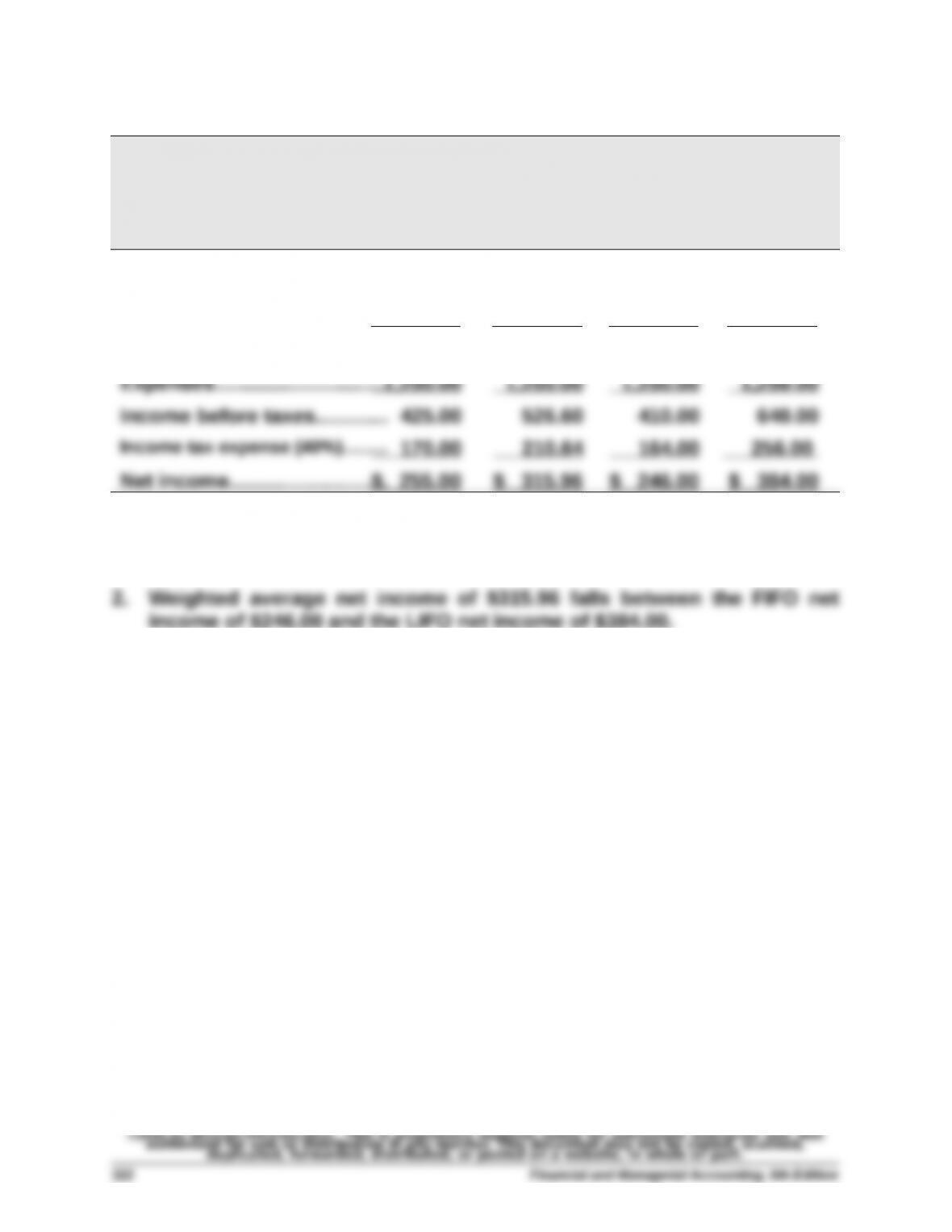

2. Weighted average net income of $250.80 falls between the FIFO net

income of $246.00 and the LIFO net income of $258.00.

Exercise 5-5A (35 minutes)

Ending Cost of

Periodic Inventory Computations Inventory Goods Sold

a. Specific Identification—Periodic

b. Weighted Average—Periodic

($1,950 / 380 units = $5.13* average cost per unit)

c. FIFO—Periodic

(180 x $4.50) + (20 x $5.00)……………….…………..…$ 910.00

d. LIFO—Periodic

(140 x $6.00) + (60 x $5.00)……………….…………..…$1,140.00

(180 x $4.50)……………………………..….….….…….….. $ 810.00

*rounded to dollars and cents

Exercise 5-6 (20 minutes)

LAKER COMPANY

Income Statements

For Month Ended January 31

Specific

Identification

Weighted

Average FIFO LIFO

Sales……………..….…….….……$2,700.00 $2,700.00 $2,700.00 $2,700.00

(180 units x $15 price)

Cost of goods sold……..….… 1,025.00 923.40 1,040.00 810.00

Gross profit………………………1,675.00 1,776.60 1,660.00 1,890.00

1. LIFO method results in the highest net income of $384.00.

income of $246.00 and the LIFO net income of $384.00.

3. If costs were rising instead of falling, then the FIFO method would yield

the highest net income.

Exercise 5-7 (20 minutes)

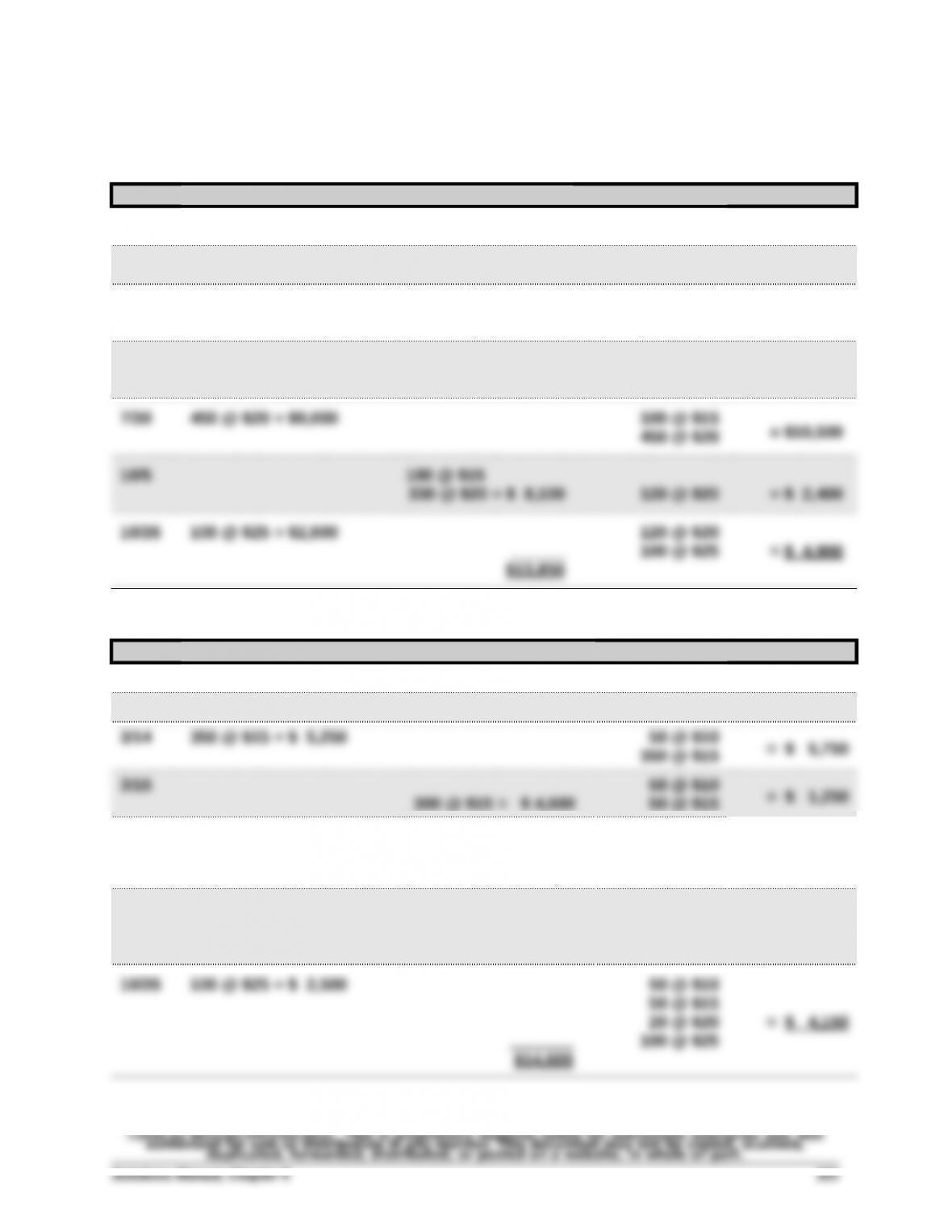

a. FIFO—Perpetual

Date Goods Purchased Cost of Goods Sold Inventory Balance

1/1 200 @ $10 = $ 2,000

1/10 150 @ $10 = $ 1,500 50 @ $10 = $ 500

3/14 350 @ $15 = $5,250 50 @ $10 = $ 5,750

350 @ $15

3/15 50 @ $10 100 @ $15 = $ 1,500

250 @ $15 = $ 4,250

b. LIFO—Perpetual

Date Goods Purchased Cost of Goods Sold Inventory Balance

1/1 200 @ $10 = $ 2,000

1/10 150 @ $10 = $ 1,500 50 @ $10 = $ 500

7/30 450 @ $20 = $ 9,000 50 @ $10

50 @ $15 = $ 10,250

450 @ $20

10/5 50 @ $10

430 @ $20 = $8,600 50 @ $15 = $ 1,650

20 @ $20

Exercise 5-7 (Concluded)

Alternate Solution Format

Ending Cost of

Inventory Goods Sold

a. FIFO

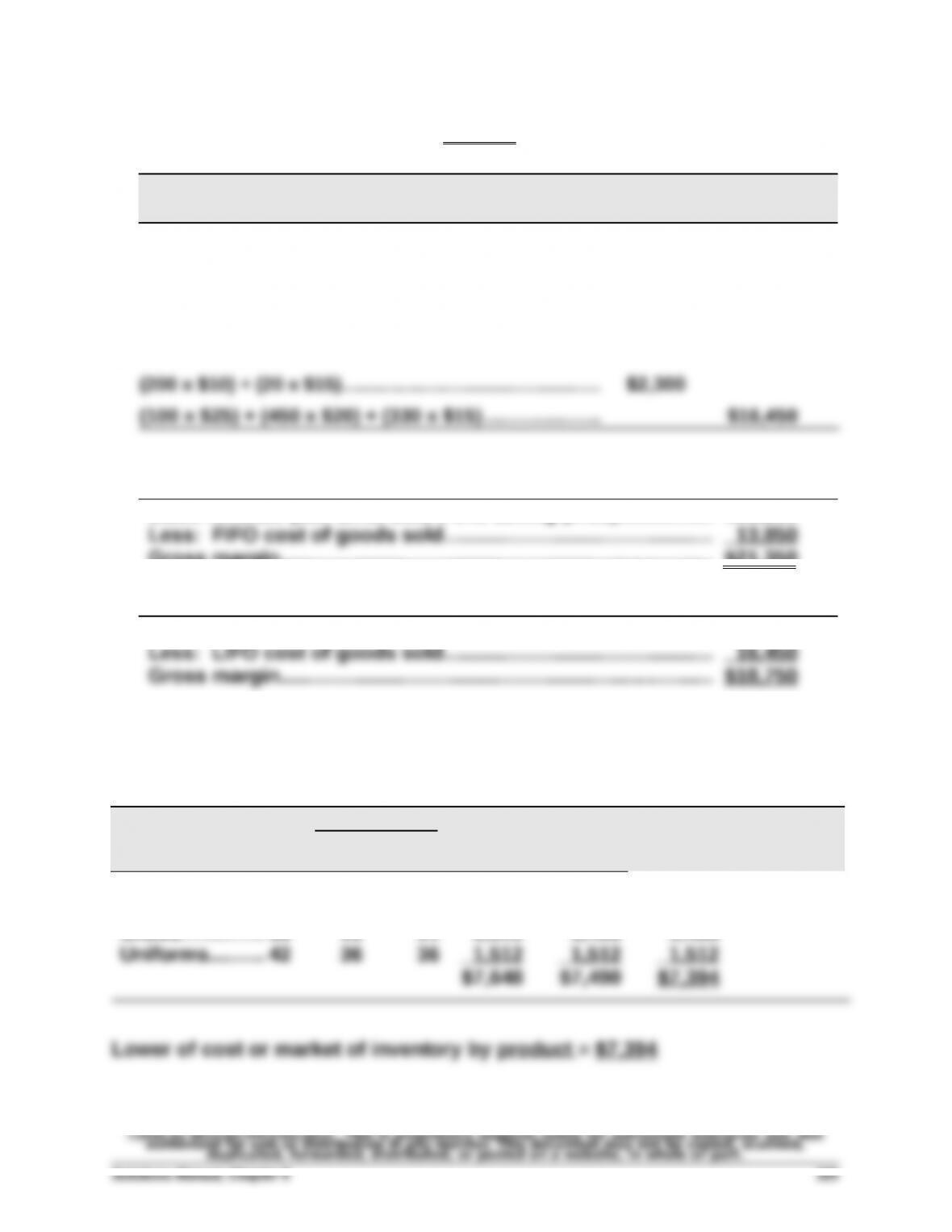

(100 x $25) + (120 x $20)……………………………………….….…... $4,900

(100 x $15)+ (330 x $20)………………….………..………………… $13,850

b. LIFO

FIFO Gross Margin

Sales revenue (880 units sold x $40 selling price)….….…….…….... $35,200

LIFO Gross Margin

Sales revenue (880 units sold x $40 selling price)….….…….…….... $35,200

Exercise 5-8 (15 minutes)

a. Specific Identification method—Cost of goods sold

Cost of goods available for sale……………..…………….….…….. $18,750

Ending inventory under specific identification

3/14 purchase ( 45 @ $15) …………………………….………....$ 675

b. Specific Identification method—Gross margin

Sales revenue (880 units sold x $40 selling price)……………. $35,200

Exercise 5-9A (20 minutes)

Cost of goods available for sale = $18,750 (given in Exercise 5-7)

Ending Cost of

Periodic Inventory System Inventory Goods Sold

a. FIFO—Periodic

(100 x $25) + (120 x $20)…………………….………..…..… $4,900

(200 x $10) + (350 x $15) + (330 x $20).…..…............ $13,850

b. LIFO—Periodic

c.

FIFO—Periodic Gross Margin

Sales revenue (880 units sold x $40 selling price)…………….. $35,200

Gross margin………………………………………………………..…….….. $21,350

LIFO—Periodic Gross Margin

Sales revenue (880 units sold x $40 selling price)…………….. $35,200

Exercise 5-10 (15 minutes)

Per Unit Total Total LCM Applied

to Items

Inventory Items Unit

s

Cost Market Cost Market

Helmets........... 24 $50 $54 $1,200 $1,296 $1,200

Bats……………... 17 78 72 1,326 1,224 1,224

Shoes…………... 38 95 91 3,610 3,458 3,458

Exercise 5-11 (20 minutes)

1. a. LIFO ratio computations

LIFO current ratio (2015) = $220/$200 = 1.1

b. FIFO ratio computations

FIFO current ratio (2015) = $300*/$200 = 1.5

2. The use of LIFO versus FIFO for Cruz markedly impacts the ratios computed.

Specifically, LIFO makes Cruz appear worse in comparison to FIFO numbers

Exercise 5-12 (25 minutes)

2. Reported income figures

Year 2014 Year 2015 Year 2016

Sales.…………….……….... $850,000 $850,000 $850,000

Cost of goods sold

Beginning inventory..... $250,000 $230,000 $250,000