VISUAL #5-2

Schedule of Cost of Goods Available

Units Cost* Total

Jan. 1 Beginning Inventory 60 @ $10 = $ 600

Mar. 27 Purchase 90 @ 11 = 990

Aug. 15 Purchase 100 @ 13 = 1,300

Nov. 6 Purchase 50 @ 16 = 800

Goods available for sale 300 $3,690

Units in physical count at year end 70

*CPU= Cost per unit

Cost Flow Assumptions or

Methods of Assigning Cost to Units in Ending Inventory

(Using a Periodic Inventory System)

(1) Specific Identification – requires that each item in an inventory be assigned

its actual invoice cost.

(2) Weighted Average – a weighted average cost per unit is determined based

on total cost and units of goods available for sale. This cost is assigned to

units in the ending inventory.

(3) First-in, First-out (FIFO) – assumes the first units acquired (beginning

inventory) are the first to be sold and that additional sales flow is in the order

purchased. Therefore, the costs of the last items received are assigned to the

ending inventory.

(4) Last-in, First-out (LIFO) – assumes the last units acquired (most recent

purchase) are the first units sold. Therefore, the cost of the first items

acquired (starting with beginning inventory) is assigned to the ending

inventory.

Note: In all methods, Cost of Good Sold equals Cost of Good Available minus

Ending Inventory (as computed by chosen method).

5-11

5-12

VISUAL #5-3

5-13

EI CGS

Which costs

to assign to

each?

Varies by

method

FIFO

out = sold

(first or earliest

costs)

LIFO

out = sold

(last or most

recent)

In an inflationary

period

(rising prices)

EI

most recent

costs

EI

earliest

costs

CGS

earliest

costs

CGS

most recent

costs

highest

lowest

lowest

highest

OBSERVATIONS

CGA Net Sales

– EI (varies by method) – CGS (affected by method)

CGS (affected by method) Gross Profit (affected by method)

Verbally identify the impact of LIFO & FIFO on net income in a period of rising

prices and a period of declining prices.

Which method(s) will result in the same EI and CGS under both a Perpetual and

Periodic Inventory System?

CGA

always

has 2 parts

5-14

Alternate Demonstration Problem #1

Chapter 5

The ABC Company had the following inventory record for the month of

January:

# of Unit

Date Description Items Price Item

1/1 Beginning

inventory 5 $20 Z1–Z5

1/5 Sale 2 Z2, Z5

1/11 Purchase 9 12 Z6—Z14

1/28 Sale 7 Z1, Z3, Z6, Z7, Z8, Z9, Z14

Required:

Assuming a perpetual inventory system is used, determine the cost of

goods sold and the ending inventory

1. FIFO

2. LIFO

3. Weighted average

4. Specific identification

5-15

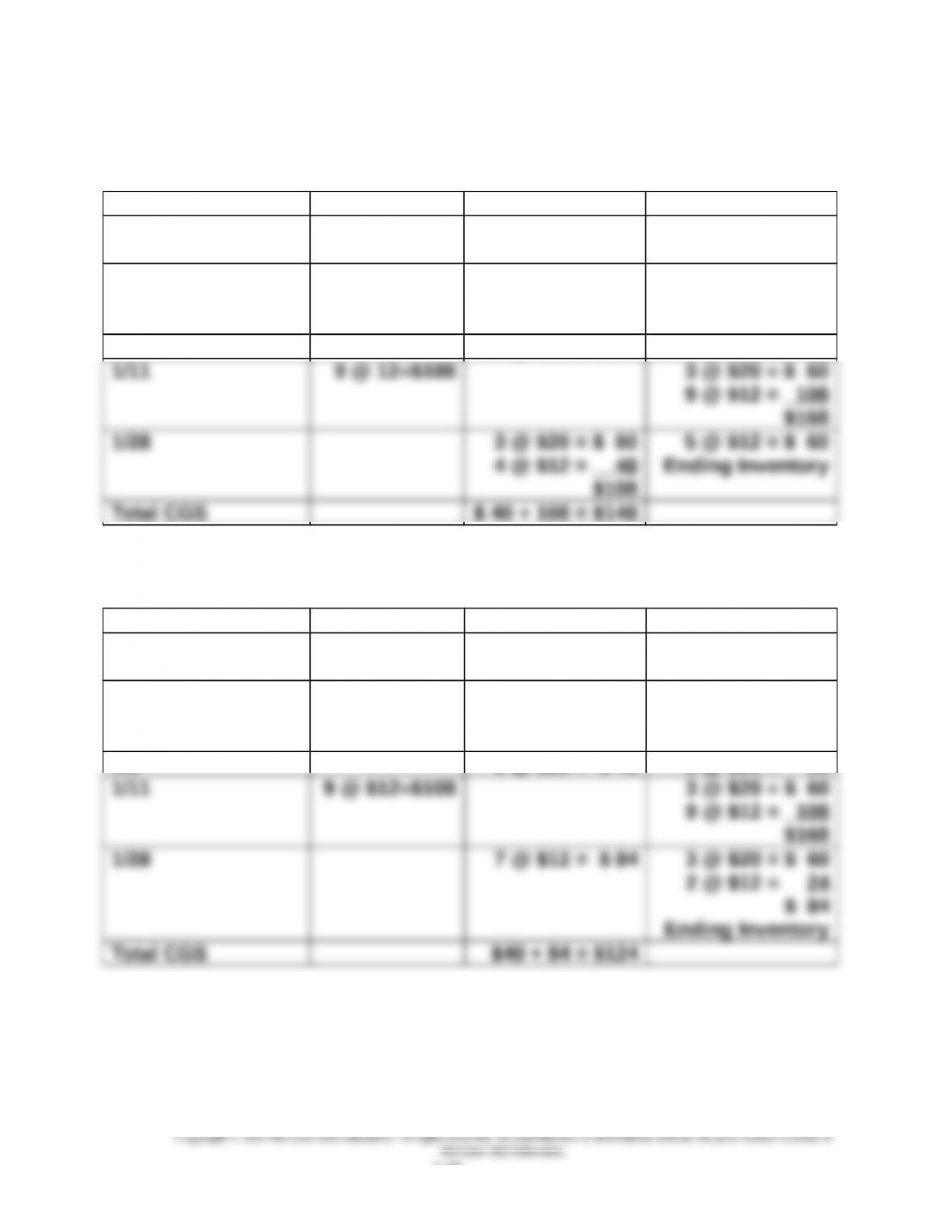

Solution: Alternate Demonstration Problem

Chapter 5

1.

FIFO Perpetual

Date Purchases Sales at Cost

Inventory Balance

1/1

Beginning

Inventory

5 @ $20 = $100

1/5 2 @ $20 = $ 40 3 @ $20 = $ 60

2.

LIFO Perpetual

Date Purchases Sales at Cost

Inventory Balance

1/1

Beginning

Inventory

5 @ $ 20 = $100

1/5 2 @ $20 = $ 40 3 @ $20 = 60

5-16

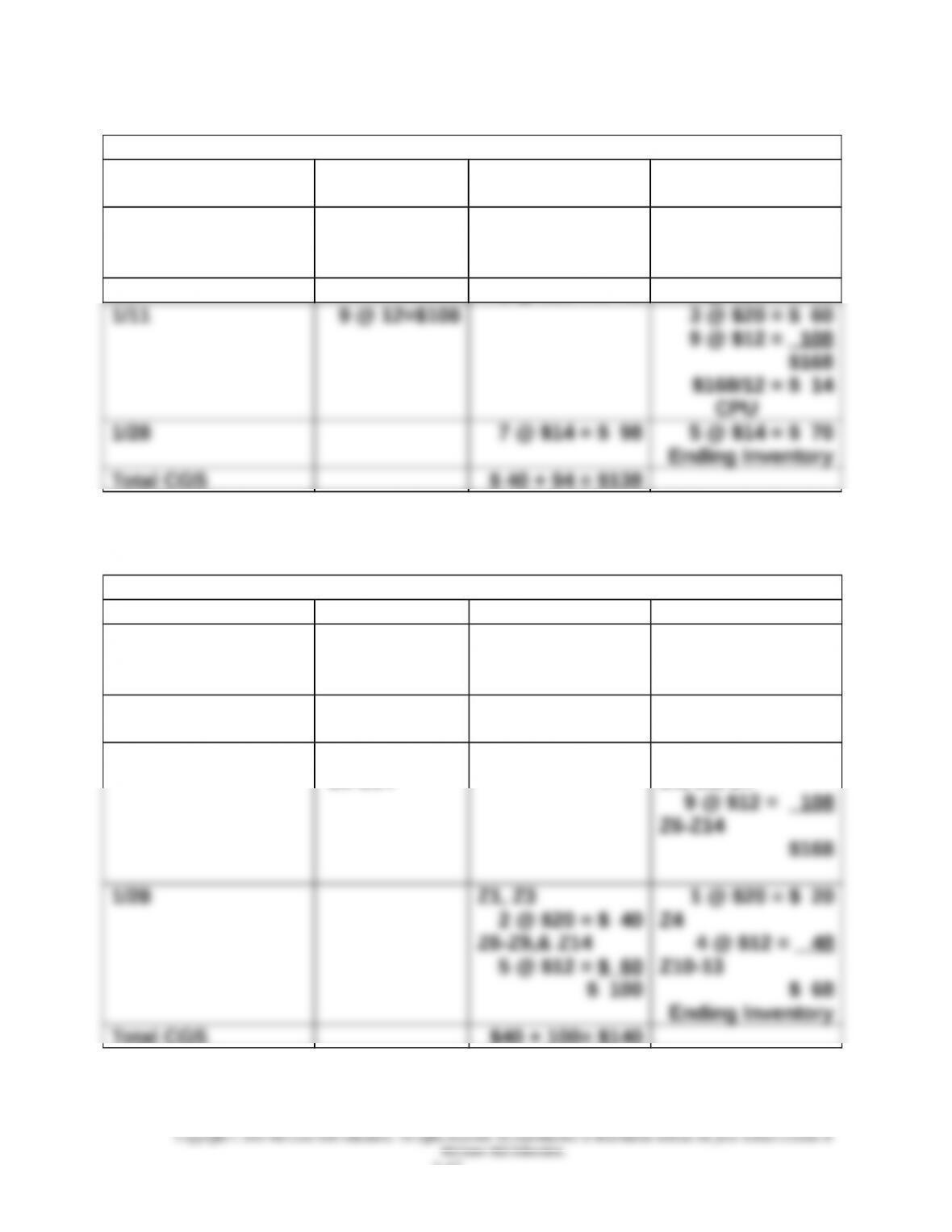

3.

Weighted Average Perpetual

Date Purchases Sales at Cost

Inventory Balance

1/1

Beginning

Inventory

5 @ $20 = $100

1/5 2 @ $20 = $ 40 3 @ $20 = $ 60

4.

Specific Identification Perpetual

Date Purchases Sales at Cost Inventory Balance

1/1

Beginning

Inventory

5 @ $ 20 = $100

Z1-Z5

1/5 2 @ $20 = $ 40

Z2, Z5

3 @ $20 = $ 60

Z1, Z3, Z4

1/11 9 @ $12=$108

Z6-Z14

3 @ $20 = $ 60

Z1, Z3, Z4

Total CGS $40 + 100= $140

5-17

Alternate Demonstration Problem #2

Chapter 5

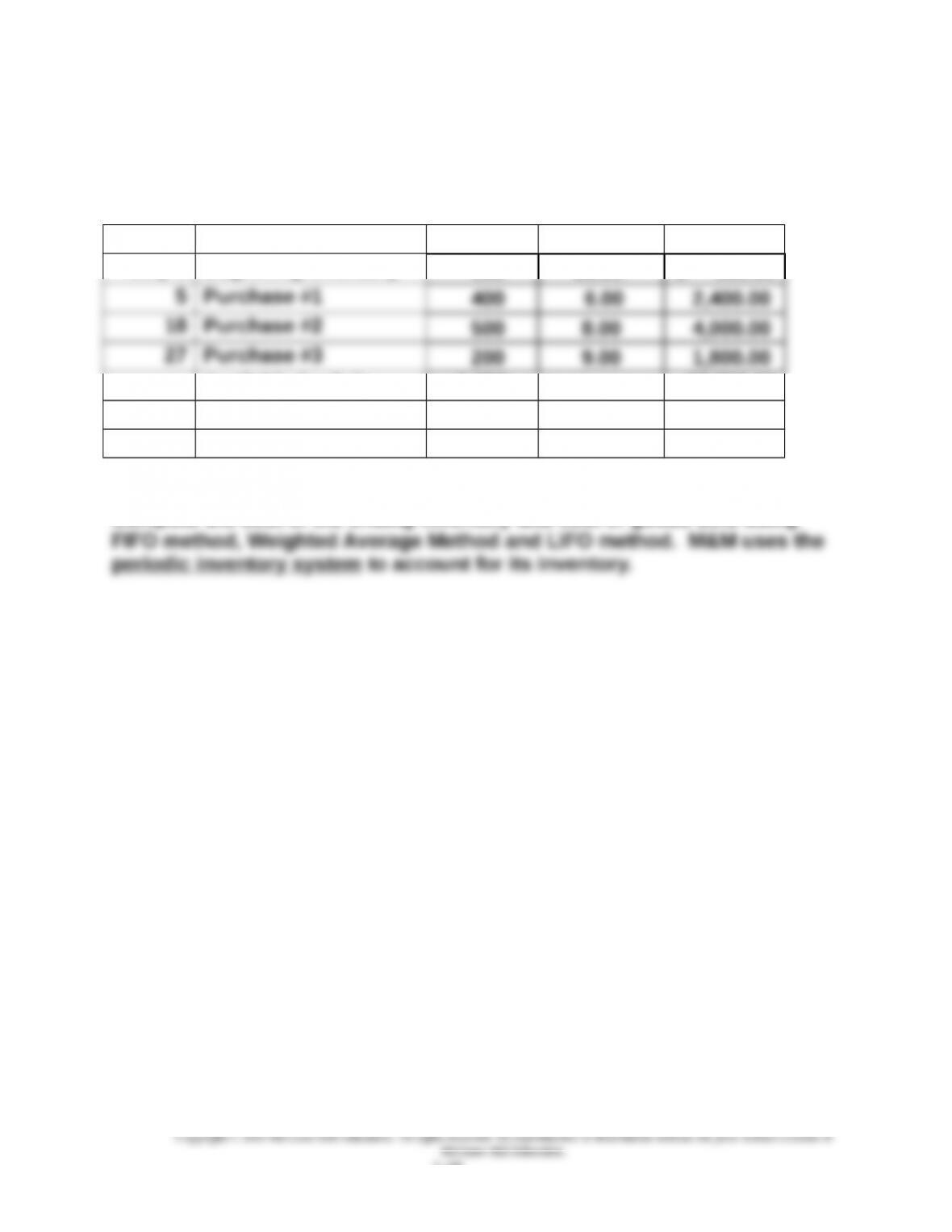

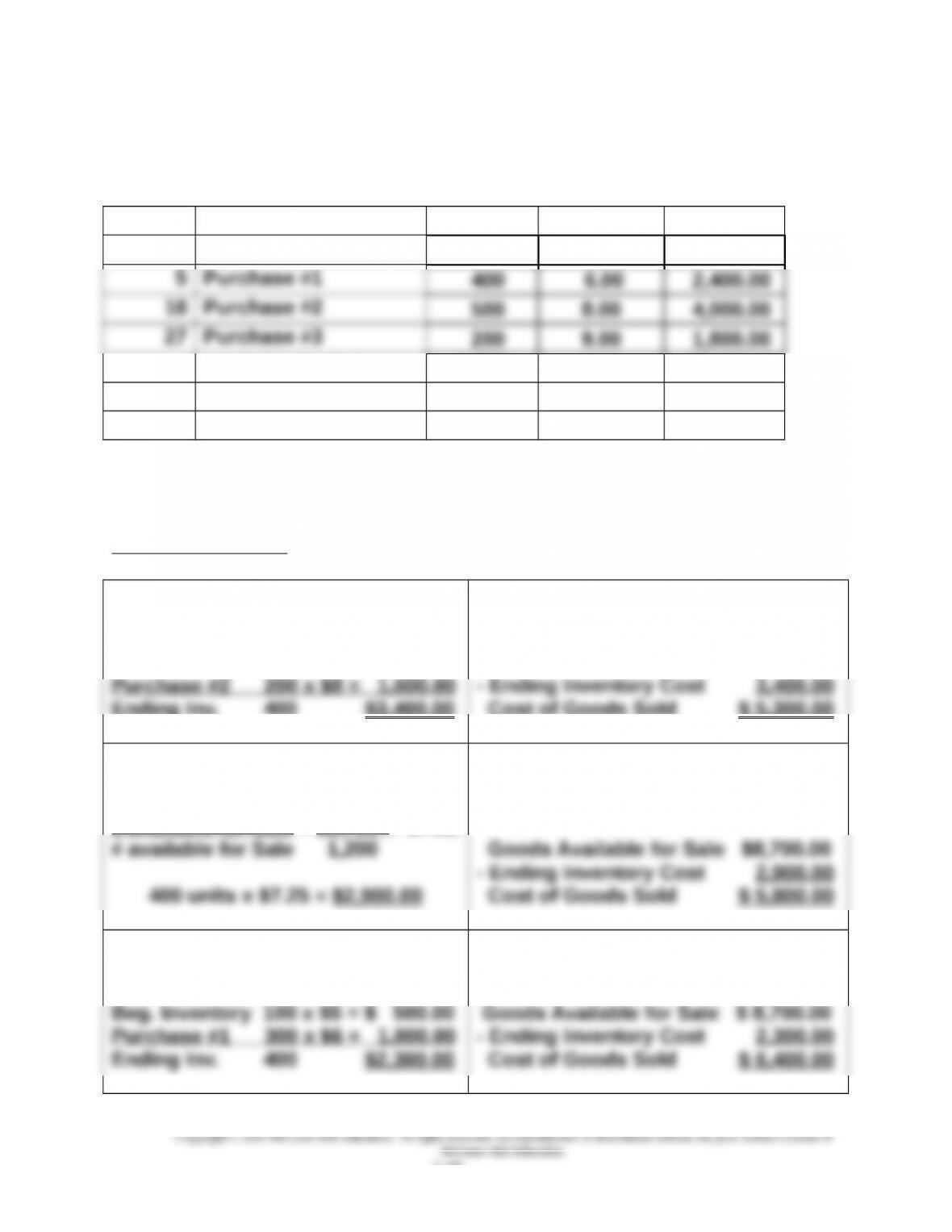

M&M Company had the following inventory record for the month of July:

Date Description Quantity Unit Price Total

July 1 Beginning Inventory 100 $5.00 $ 500.00

Available for Sale 1,200 $8,700.00

July 31 Ending Inventory 400

Required:

Compute the cost of the ending inventory and cost of goods sold using

5-18

Alternate Demonstration Problem #2 Solution

Chapter 5

M&M Company had the following inventory record for the month of July:

Date Description Quantity Unit Price Total

July 1 Beginning Inventory 100 $5.00 $ 500.00

Available for Sale 1,200 $8,700.00

July 31 Ending Inventory 400

Required:

Compute the cost of the ending inventory and cost of goods sold using

FIFO method, Weighted Average Method and LIFO method. M&M uses the

periodic inventory system to account for its inventory.

FIFO Method

Ending Inventory

From

Purchase #3 200 x $9 = $1,800.00

Ending Inv. 400 $3,400.00

FIFO Method

Cost of Goods Sold

Goods Available for Sale $ 8,700.00

Cost of Goods Sold $ 5,300.00

Weighted Average Method

Ending Inventory

$ available for Sale = $8,700 = $7.25

Weighted Average Method

Cost of Goods Sold

LIFO Method

Ending Inventory

From

LIFO Method

Cost of Goods Sold

5-19