CHAPTER 5

INVENTORIES AND COST OF SALES

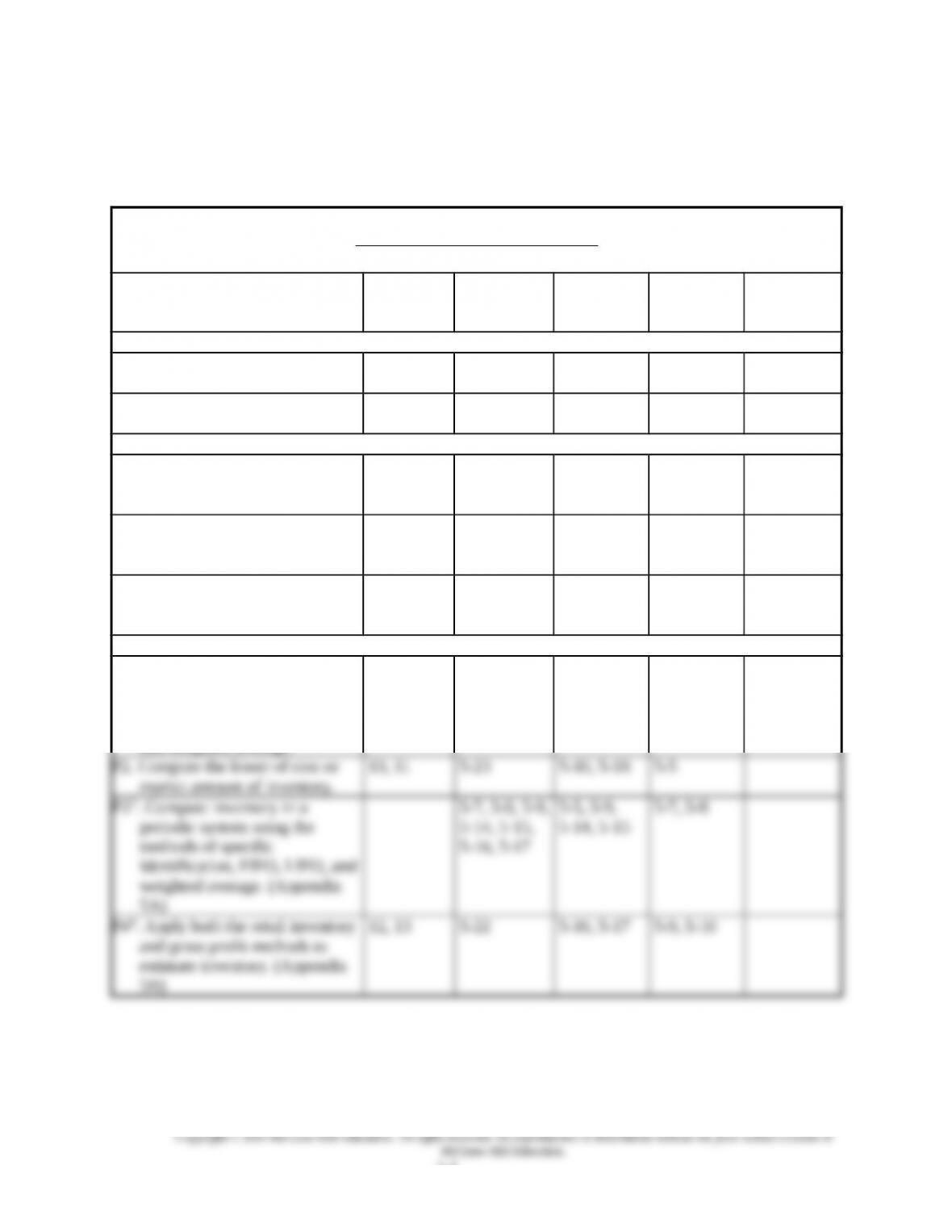

Related Assignment Materials

Student Learning Objectives Questions

Quick

Studies* Exercises* Problems*

Beyond the

Numbers

Conceptual objectives:

C1. Identify the items making up

merchandise inventory.

2, 12, 16 5-1, 5-23 5-1 5-8

C2. Identify the costs of

merchandise inventory.

3, 15, 17 5-2, 5-23 5-2 5-1, 5-8

Analytical objectives:

A1. Analyze the effects of

inventory methods for both

financial and tax reporting.

4, 5, 6, 7 5-18 5-4, 5-6,

5-11

5-8 5-3, 5-4, 5-6

A2. Analyze the effects of

inventory errors on current and

future financial statements.

8, 9 5-19, 5-20 5-12 5-6

A3. Assess inventory management

using both inventory turnover

and days’ sales in inventory.

5-21 5-11, 5-13 5-1, 5-2,

5-5, 5-7, 5-9

Procedural objectives:

P1. Compute inventory in a

perpetual system using the

methods of specific

identification, FIFO, LIFO,

and weighted average.

1, 4 5-3, 5-4, 5-5,

5-6, 5-10,

5-11, 5-12,

5-13

5-3, 5-7, 5-8 5-1, 5-2,

5-3, 5-4

5-6

and gross profit methods to

estimate inventory. (Appendix

5B)

*See additional information on next page that pertains to these quick studies, exercises and problems.

5-1

Additional Information on Related Assignment Material

The Serial Problem for Success Systems continues in this chapter. Problems 5-6A and 5-7A can be

completed using Excel.

Connect (Available on the instructor’s course-specific website) repeats all numerical Quick Studies, all

Exercises and Problems Set A. Connect provides new numbers each time the Quick Study, Exercise or

Problem is worked. It allows instructors to monitor, promote, and assess student learning. It can be used

in practice, homework, or exam mode

Synopsis of Chapter Revisions

Proof Eyewear: NEW opener with new entrepreneurial assignment

Streamlined inventory presentation by not repeating seller/buyer entries

Added several new T-accounts to help learning of inventory flow

New simplified presentation and exhibits for periodic inventory methods

New explanatory notes added to exhibits as learning aids

Updated inventory ratios section using Toys `R’ Us

5-2

Chapter Outline Notes

I. Inventory Basics

A. Determining Inventory Items

Includes all goods that a company owns and holds for sale.

1. Goods in transit—included if ownership has passed.

2. Goods on consignment—owned by consignor.

3. Goods damaged or obsolete—not included if they cannot be

sold. If salable, included at a conservative estimate of their net

realizable value (sales price minus cost of making the sale).

B. Determining Inventory Costs

Includes cost of expenditures necessary, directly or indirectly, in

bringing an item to a salable condition and location.

1. Cost example: invoice price minus any discount, plus any

incidental costs such as import tariffs, transportation-in,

storage, insurance, etc.

2. Matching principle states that inventory costs should be

recorded against revenue in the period when inventory is sold.

3. Exception: Under the materiality principle or the cost-to-

benefit constraint (effort outweighs benefit), incidental costs

of acquiring inventory maybe deemed immaterial and

allocated to cost of goods sold in the period when they are

incurred.

C. Internal Controls and Taking a Physical Count

1. Events can cause the Inventory account balance to differ from

the actual inventory available.

2. Physical count is generally taken at the end of its fiscal year or

when inventory amounts are low (at least once per year).

3. Physical inventory is used to adjust the Inventory account

balance to the actual inventory on hand and thus account for

theft, loss, damage, and errors.

4. Internal controls (such as pre-numbered inventory tickets,

assigned primary and secondary counters, and manager

confirmations) are applied when a physical count is taken.

II. Inventory Costing Under a Perpetual System—Accounting for

inventory affects both the balance sheet and the income statement.

There are 4 commonly used inventory costing methods. Each assumes

a particular pattern of how cost flow through inventory. Physical flow

and cost flow need not be the same.

5-3

Chapter Outline Notes

(Note: The following assumes a perpetual inventory system.

The periodic system is addressed in the appendix 5A outline.)

A. Inventory Cost Flow Assumptions

Four methods of assigning costs to inventory and cost of goods

sold are:

1. Specific identification—when each item in inventory can be

identified with a specific purchase and invoice, we can use this

method to assign actual cost of units sold to cost of goods sold

and leave actual cost of units on hand in the inventory

account.

2. First-in, first-out (FIFO)—when sales occur, the costs of the

earliest units acquired are charged to cost of goods sold,

leaving costs of most recent purchases in inventory.

3. Last-in, first-out (LIFO)—when sales occur, costs of the most

recent purchases are charged to cost of goods sold, leaving

costs of earliest purchases in inventory. (Note: LIFO comes

closest to matching current costs against revenues.)

4. Weighted average (also called average cost)—requires we

compute the weighted average cost per unit of inventory at the

time of each sale (cost of goods available divided by units

available). We charge this weighted average cost per unit

times units sold to cost of goods sold.

Note: Advanced computing technology has made perpetual

inventory systems more affordable and more widely used.

B. Financial Statement Effects of Costing Methods

When purchase prices are different, the 4 costing methods nearly

always assign different cost amounts. When costs regularly rise,

note the following results:

1. FIFO assigns the lowest amount to cost of goods sold yielding

the highest gross profit and the highest net income.

2. LIFO assigns the highest amount to cost of goods sold

yielding the lowest gross profit and the lowest net income.

3. Weighted average method yields results between FIFO and

LIFO.

4. Specific identification always yields results that depend on

which units are sold.

Note: When costs regularly decline the reverse of above occurs

for FIFO and LIFO.

All 4 methods are acceptable. Companies must disclose the

method used in its financial statements or notes. Each method

offers certain advantages:

1. FIFO assigns an amount to inventory on the balance sheet that

approximates current replacement costs.

5-4

Chapter Outline Notes

2. LIFO better matches current costs with revenues on the

income statement.

3. Weighted average tends to smooth out erratic changes in costs.

4. Specific Identification exactly matches costs with revenues

they generate.

C. Tax Effects of Costing Methods

Since inventory costs affect net income, they have potential tax

effects. Companies can use different methods for financial

reporting and tax reporting. Exception: When LIFO is used for tax

purposes, IRS requires it also be used for financial statements.

D. Consistency in Using Costing Methods

The consistency principle requires that a company use the same

accounting methods period after period (for comparability) unless

a change will improve financial reporting. Full-disclosure

principle requires any change, its justification and effect of net

income be reported.

III. Valuing Inventory at LCM and the Effects of Inventory Errors

A. Lower of Cost or Market (LCM)

Accounting principles require that inventory be reported on the

balance sheet at market value when market is lower than cost.

1. Market in the term LCM is defined as replacement cost.

2. LCM is applied in one of three ways:

a. to each individual item separately

b. to major categories of products

c. to the entire inventory.

3. The most widely used approach to apply LCM is to each

individual item in the inventory and only this approach is

illustrated in this chapter.

4. When replacement cost (market) drops below cost, inventory

is adjusted downward to market value with the following

entry: Debit to cost of goods sold and credit Inventory for the

amount of the decrease.

5. LCM is often justified with reference to conservatism

principle.

B. Financial Statement Effects of Inventory Errors

1. Inventory errors cause misstatements in cost of goods sold,

gross profit, net income, current assets, and equity.

2. Erroneous ending inventory of one period becomes erroneous

beginning inventory of the next and results in misstatements in

that next period’s statements.

3. An inventory error, although serious, is said to be self-

correcting because it always yields an offsetting error in the

next period.

5-5

Chapter Outline Notes

4. Understated ending inventories result in understated assets and

equity (on balance sheet), and an understated net income (on

income statement) that period. Note: overstated ending

inventories have the reverse effects.

5. Beginning inventory errors do not affect the balance sheet but

do affect the current period’s net income.

IV. Global View—Compares U.S. GAAP to IFRS

A. Items and costs making up inventory—both systems include broad

and similar guidance.

B. Assigning costs to inventory—both systems allow specific

identification. GAAP also allows FIFO, Weighted Average, and

LIFO. IFRS does not currently allow LIFO but does allow FIFO

and Weighted Average.

C. Estimating inventory costs—Both systems apply LCM to write

down decline in inventory value. Only IFRS allows reversals to

original cost if market increases in future periods

V. Decision Analysis—Inventory Turnover and Days’ Sales in

Inventory

A. Inventory Turnover

1. Calculated by dividing cost of goods sold by average

merchandise inventory.

2. Reveals how many times a company turns over (sells) it

inventory during a period.

3. Users apply it to analyze short-term liquidity and to assess

management’s ability to control inventory availability.

4. A low ratio (in comparison to competitors) suggests inefficient

use of assets and a high ratio suggests inventory may be too

low.

B. Days’ Sales in Inventory

1. Reveals how much inventory is available in terms of the

number of days’ sales (how many days one can sell from

inventory if no new items are purchased).

2. Calculated by dividing ending inventory by cost of goods sold,

and then multiplying the result by 365.

C. Analysis of inventory management

A major emphasis for most merchandisers to both plan and control

inventory purchases and sales.

VI. Inventory Costing Under a Periodic System (Appendix 5A)

A. The basic aim of the periodic and perpetual system is the same.

The aim is to assign costs to inventory and cost of goods sold.

5-6

Chapter Outline

Notes

B. When you use Periodic Inventory System, you don’t keep track of

the units you sell during the period. To compute cost of goods

sold you first compute the cost of the units on hand and then

subtract the cost of ending inventory from cost of goods available

for sale to determine cost of goods sold.

Cost of goods available for Sale

less: Cost of ending inventory

Cost of Goods Sold

C. The same four methods of assigning costs are used in each system

but the results may differ by inventory system due to timing of

cost assignment (Note: perpetual—cost assigned at point of sale

vs. periodic—costs assigned at year end when physical count is

taken).

1. Specific identification—periodic results will be same as

perpetual since specific cost will always be the same

regardless of system used.

2. First-in, first-out (FIFO)—periodic results will be same results

as perpetual since first costs will always be the same

regardless of system used.

3. Last-in, first-out (LIFO)—periodic results differ from

perpetual results because timing of cost assignment changes

what is identified as the last cost. Perpetual LIFO identifies

last cost at point of sale, whereas periodic LIFO identifies last

cost at year end.

4. Weighted average—periodic results differ from perpetual

because timing of cost assignment changes what costs are

averaged. Periodic weighted average is computed once at year

end and is based on total cost of goods available for sale and

total units available for sale.

D.Financial Statement Effects

A periodic system has the same general affects on financial

statements as perpetual system.

5-7

VII. Inventory Estimation Methods (Appendix 5B) Notes

A. Retail Inventory Method

Estimates the cost of ending inventory for interim statements in a

periodic inventory system when a physical count is taken only

annually or to estimate if casualty loss makes physical count

impossible.

Steps:

1. Subtract sales (general ledger amount) from goods available

measured at retail price (retail data in supplementary records)

to get ending inventory at retail.

2. Find cost ratio by dividing total of goods available at cost by

total of goods available at retail.

3. Apply cost ratio to ending inventory at retail to convert to

ending inventory at cost.

B. Gross Profit Method

Estimates the cost of ending inventory for insurance claims when

inventory is destroyed, lost or stolen.

Preliminary steps:

1. Determine the normal gross profit percentage from recent years.

2. Find the cost of goods percentage (100% less gross profit

percentage).

Steps to estimate inventory using gross profit method:

Beginning Inventory (from general ledger account)

+ Cost of Goods Purchased (from general ledger account)

Goods Available for Sale at Cost

– Estimated Cost of Goods Sold (Net Sales x COGS%)

Estimated Ending Inventory

5-8

VISUAL #5-1

Schedule of Cost of Goods Available

Units Cost Total

Jan. 1 Beginning Inventory 60 @ $10 = $ 600

Jan. 7 Purchase 90 @ 11 = 990

Jan. 15 Purchase 100 @ 13 = 1,300

Jan 25 Purchase 50 @ 16 = 800

Goods available for sale 300 $3,690

Sold a total of 230 units for $20 per unit. Timing of sales is as follows:

Jan. 1- Sold 30 units (actual CPU* $10)

Jan. 9- Sold 70 units (actual CPU: 20 @ $10 and 50 @ $11)

Jan 17-Sold 100 units (actual CPU: 50 @ $13, 30 @ $11 and 20 @ $10)

Jan 28-Sold 30 units (actual CPU: 20 @ 16, 10 @ $13)

*CPU= Cost per unit

Cost Flow Assumptions or

Methods of Assigning Cost to Units as Sold (CGS)

(Using a Perpetual Inventory System)

(1) Specific Identification – Each time a sale occurs, the actual invoice cost of

the units sold is identified and charged to cost of goods sold. This leaves the

actual cost of units left in inventory.

(2) Weighted Average – Each time a sale occurs, the weighted average cost per

unit is determined (based on total cost of goods available at point of sale

divided by total number of units of goods available at point of sale). This

cost is charged to cost of goods sold, leaving a weighted average cost in

inventory.

(3) First-in, First-out (FIFO) – Each time a sale occurs, the costs of the earliest

units acquired are charged to cost of goods sold, leaving costs of most recent

purchases in inventory.

(4) Last-in, First-out (LIFO) – Each time a sale occurs, costs of the most

recent purchases are charged to cost of goods sold, leaving costs of earliest

purchases in inventory.

5-9

5-10