Problem 22-2A (Continued)

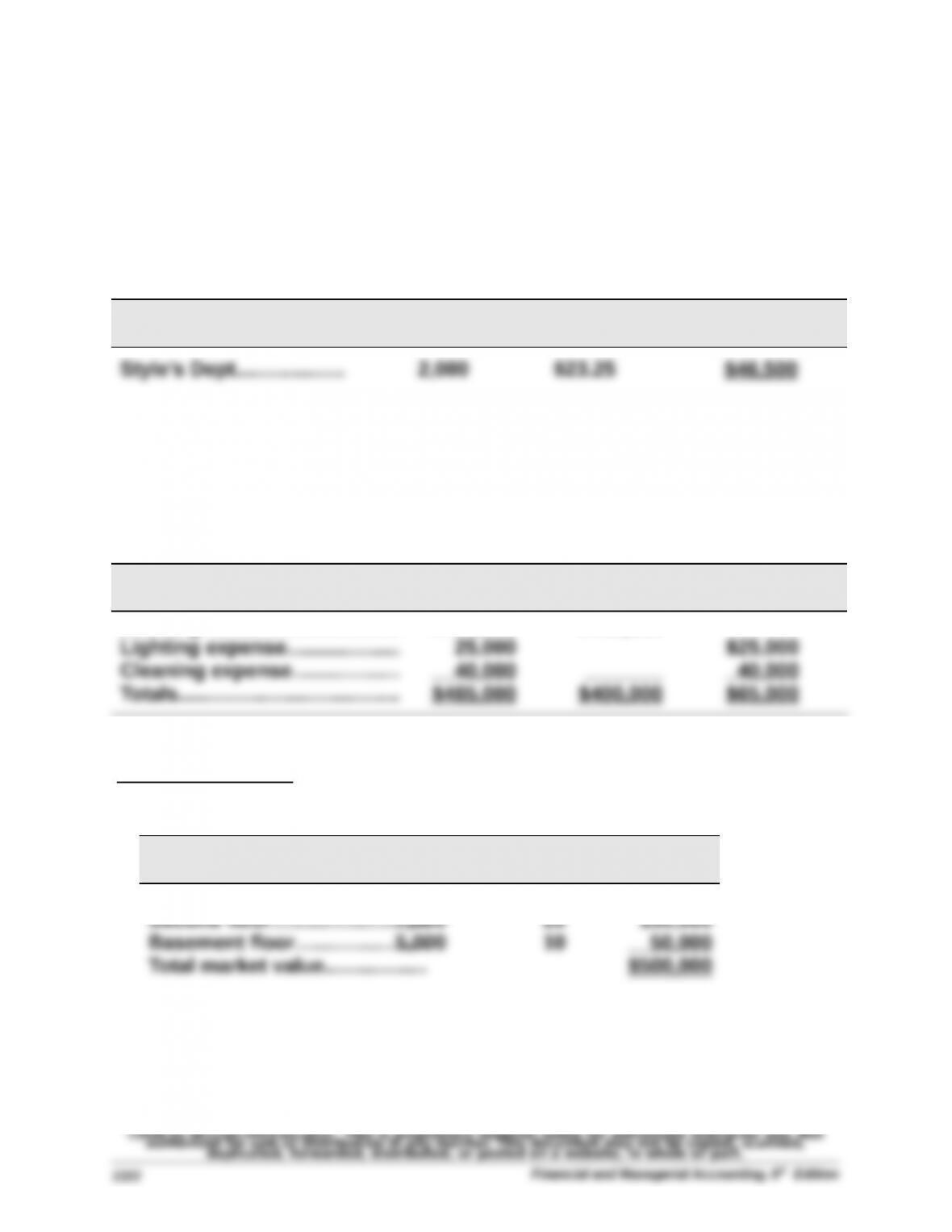

Value-based costs are allocated to departments in two steps

(i) Compute market value of each floor

Floor

Square

Footage

Value per

Sq. Ft. Total

(ii) Allocate $54,000 to each floor based on its percent of market value

Floor

Market

Value

% of

Total

Allocated

Cost

Cost per

Sq. Ft.

First floor……………………….…..$120,000 60% $32,400 $8.10

Second floor….….….……......... 80,000 40 21,600 5.40

Totals………..…..….….…….….….$200,000 100% $54,000

Usage-based costs allocation rate = $12,000 / 8,000 sq. ft.

= $1.50 per sq. ft.

12

Floor Value Usage Total

Department

Square

Footage Rate Total

Part 3

A second-floor manager would prefer allocation based on market value. This is a

reasonable and logical approach to allocation of occupancy costs. The current

method implies all square footage has equal value. This is not logical for this

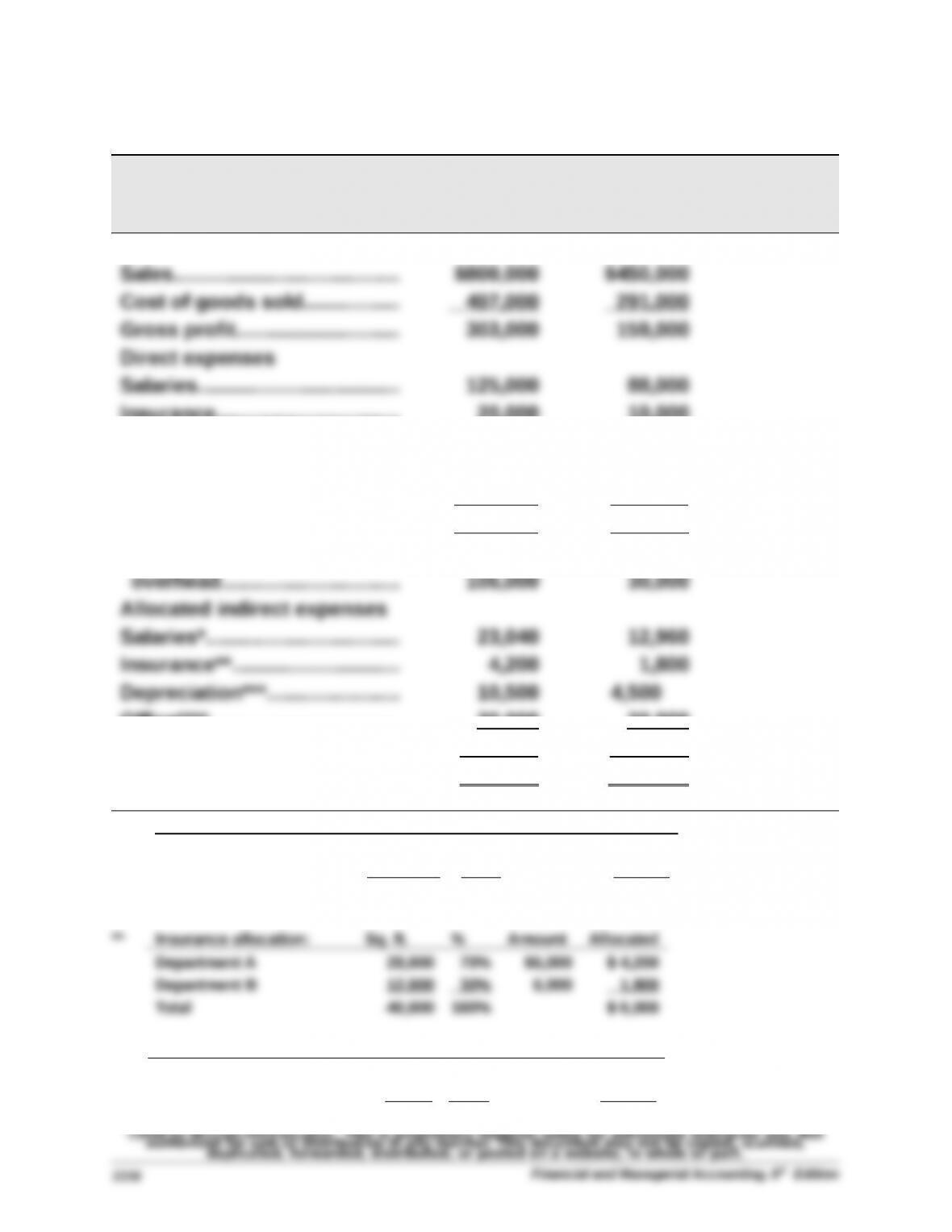

Problem 22-3A (70 minutes)

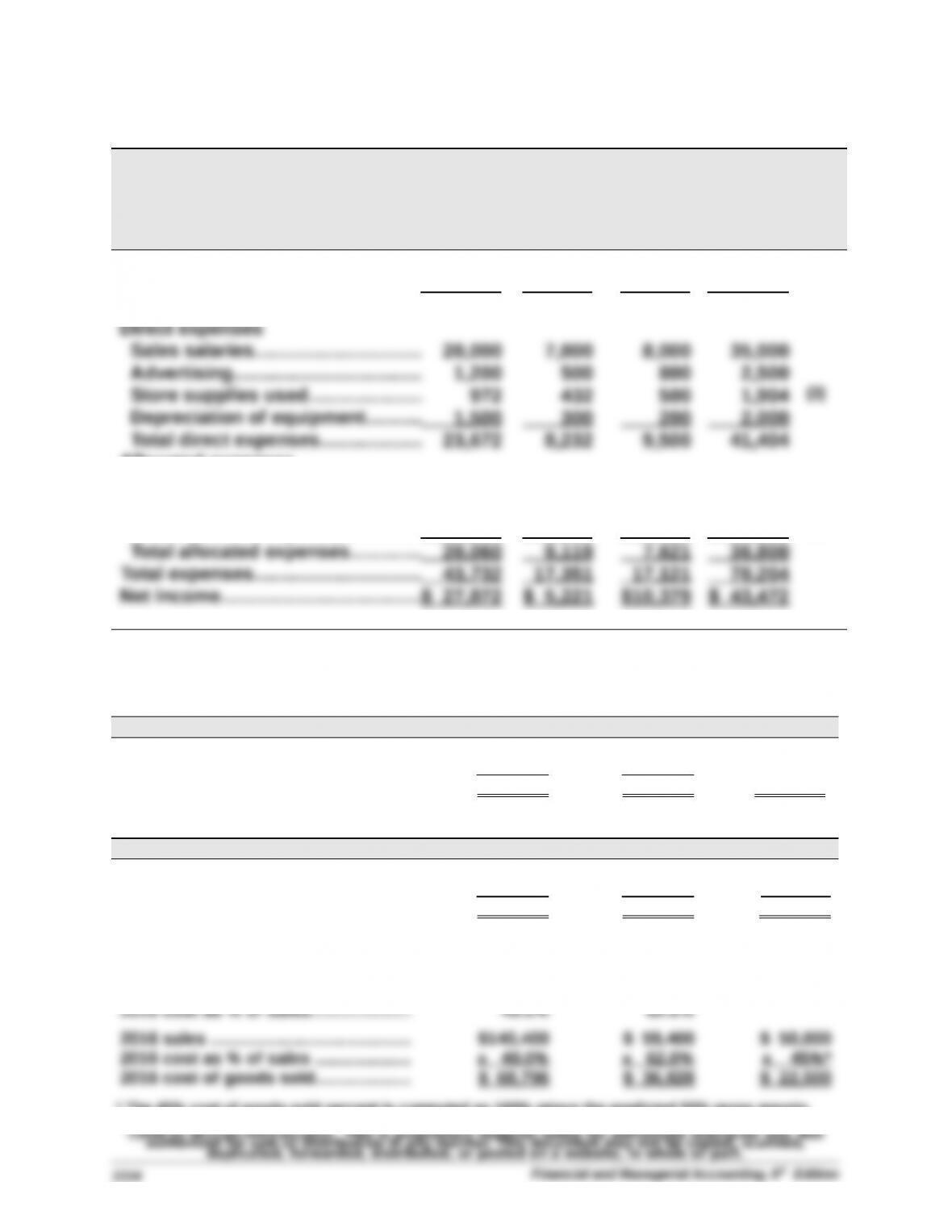

Williams Company

Forecasted Departmental Income Statements

For Year Ended December 31, 2016

Clock Mirror Paintings Combined

Sales………………..…………...…………..$140,400 $59,400 $50,000 $249,800 (1)

Cost of goods sold…….………......... 68,796 36,828 22,500 128,124 (2)

Gross profit………………..…………...... 71,604 22,572 27,500 121,676

Allocated expenses

Rent expense…..…………..……….…. 5,616 2,835 2,349 10,800 (4)

Utilities expense………………..…….. 2,080 1,048 872 4,000 (4)

Share of office dept. expenses.... 12,364 5,236 4,400 22,000 (5)

Supporting Computations—coded (1) through (5) in statement above

Note 1 (Sales)

Clock Mirror Paintings

2015 sales…………………........….......... $130,000 $ 55,000

Growth rate (8% increase)..…........... x 108% x 108%

2016 sales…………………........….......... $140,400 $ 59,400 $ 50,000

Note 2 (Cost of Goods Sold)

Clock Mirror Paintings

2015 cost of goods sold…................ $ 63,700 $ 34,100 $ 50,000

Growth rate (8% increase)..…........... x 108% x 108% x 45%*

2016 cost of goods sold…................ $ 68,796 $ 36,828 $ 22,500

ALTERNATIVELY

2015 cost of goods sold…................ $ 63,700 $ 34,100

2015 sales…………………........….......... $130,000 $ 55,000

* The 45% cost of goods sold percent is computed as 100% minus the predicted 55% gross margin.

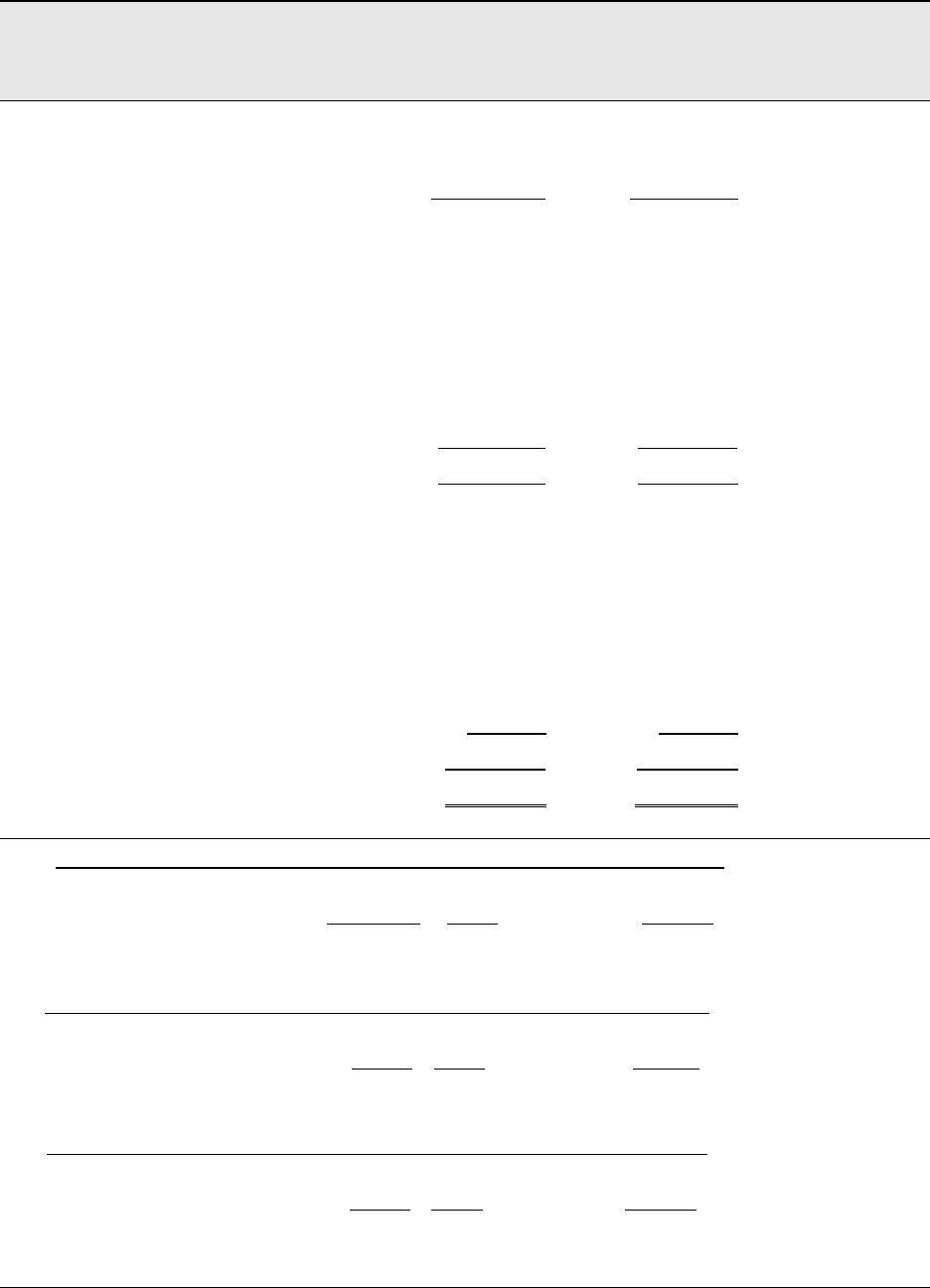

Problem 22-3A (Continued)

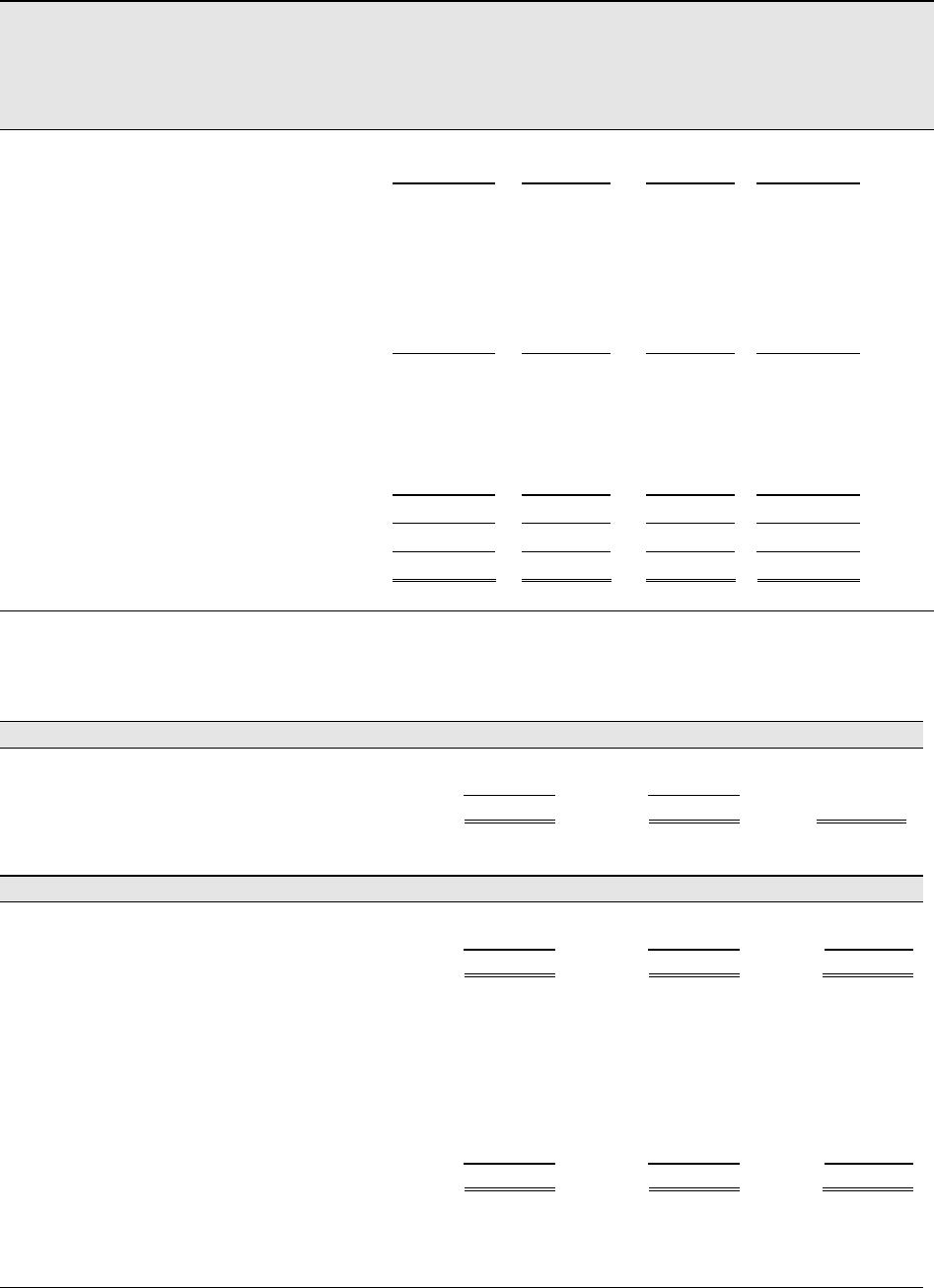

Note 3 (Store Supplies Used)

Clock Mirror Paintings

2015 store supplies used ………........... $ 900 $ 400

Growth rate (8% increase)……….………. x 108% x 108%

2016 store supplies ………….…..………… $ 972 $ 432 $ 500

2015 rent …….…………..…………..…………. $ 7,020 $ 3,780

One-fifth from clock to paintings……… (1,404) $ 1,404

One-fourth from mirror to

2016 allocation of $4,000

total utilities …………………..………..…… $ 2,080 $ 1,048 $ 872

†Adjusted to eliminate rounding difference.

Note 5 (Office Department Expenses)

Clock Mirror Paintings

2015 sales …..………….……………………... $140,400 $ 59,400 $ 50,000

Percent of total sales *…….………………. 56.2% 23.8% 20.0%

2016 allocation of $22,000

* Instructor note: If students round to something other than one-tenth of a percent, their

numbers will slightly vary.

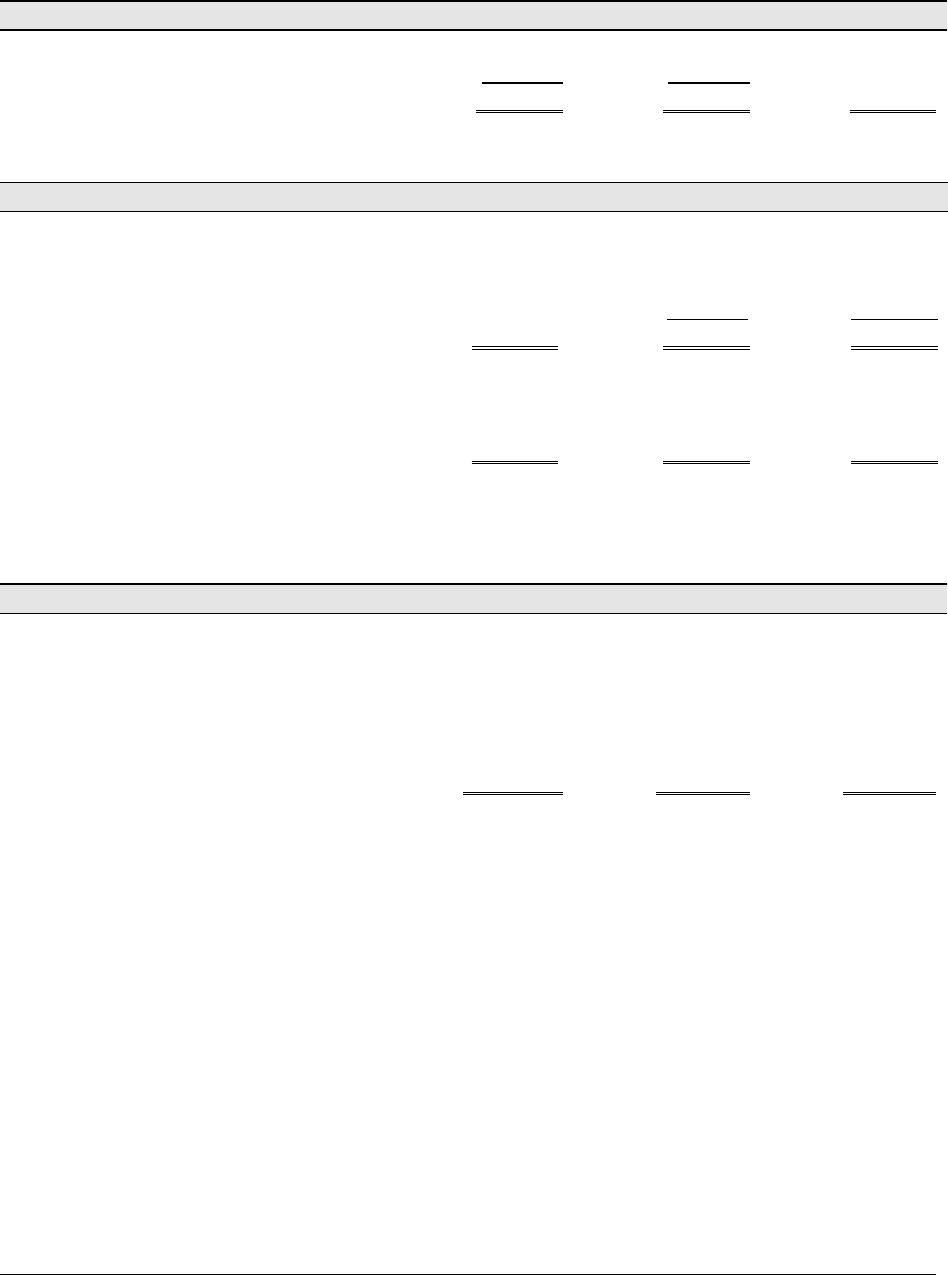

Problem 22-4A (45 minutes)

Part 1

VORTEX COMPANY

Departmental Contribution Statements

Dept. A Dept. B

Insurance………………………..…

Utilities………………………………

Depreciation………………..……..

20,000

24,000

21,000

10,000

14,000

12,000

Maintenance………………..…….. 7,000 5,000

Total direct expenses…..…….. 197,000 129,000

Departmental contributions to

Office****…………….………….…..

Total indirect expenses……….

30,000

67,740

20,000

39,260

Operating income………….…... $ 38,260 $ (9,260)

*Salaries allocation: Sales % Amount Allocated

Department A $ 800,000 64% $36,000 $23,040

Department B 450,000 36% 36,000 12,960

Total $1,250,000 100% $36,000

*** Depreciation allocation: Sq. ft. % Amount Allocated

Department A 28,000 70% $15,000 $10,500

Department B 12,000 30% 15,000 4,500

Total 40,000 100% $15,000

Problem 22-4A (Concluded)

**** Office expense allocation: Employees % Amount Allocated

Department A 75 60% $50,000 $30,000

Department B 50 40% 50,000 20,000

Total 125 100% $50,000

Part 2

Although Department B has a negative departmental income, it is

contributing $30,000 to overhead. If none of the indirect expenses can be

P

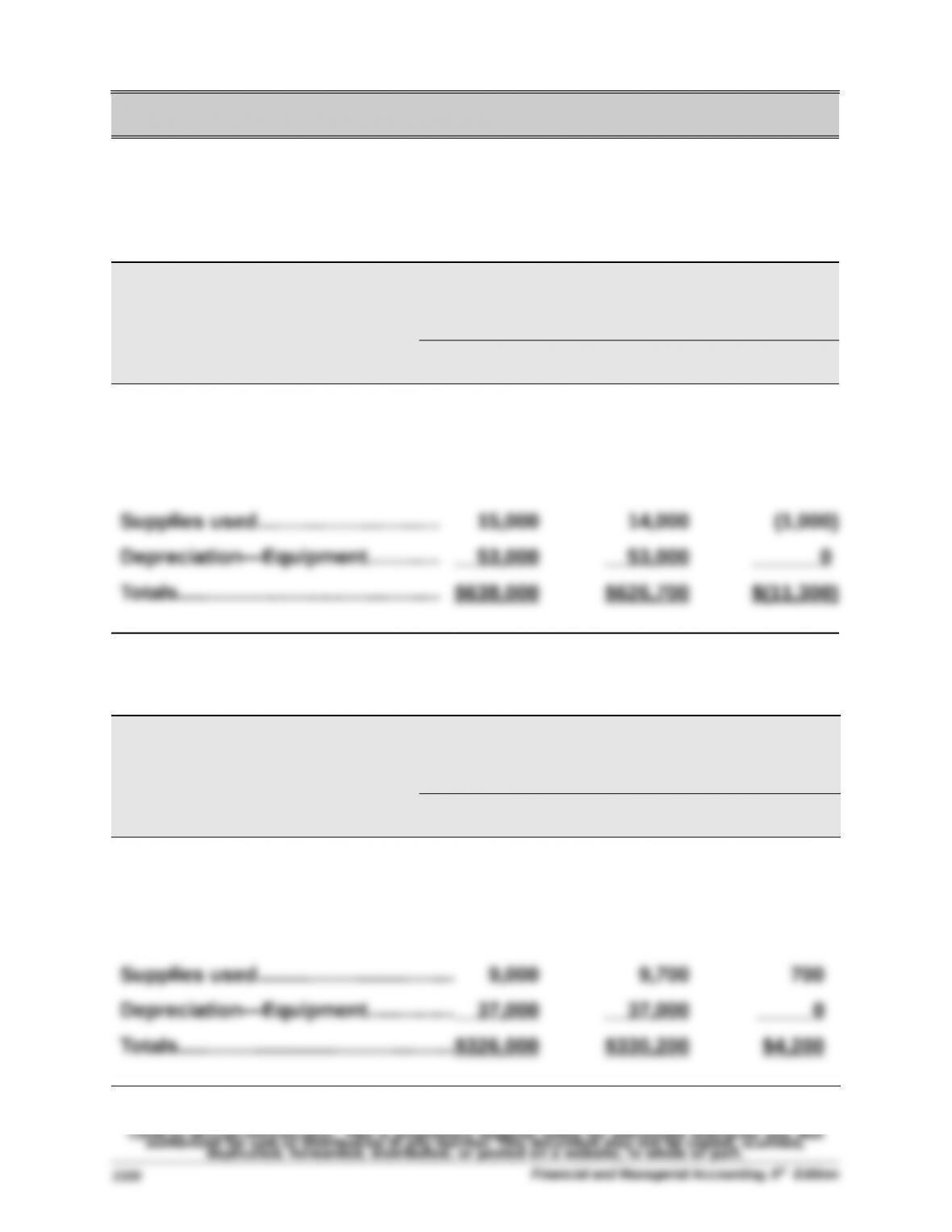

Problem 22-5AB (60 minutes)

Part 1

Allocations of joint costs on the basis of sales values

Tree pruning and care: $405,000

Grade

Sales

Value

Percent

of Total

Allocated

Cost

No. 1…………….……….…..$450,000 48.0% $194,400

No. 2…………….……….…..300,000 32.0 129,600

Picking, sorting, and grading: $202,500

Grade

Sales

Value

Percent

of Total

Allocated

Cost

No. 1…………….……….…..$450,000 48.0% $ 97,200

No. 2…………….……….…..300,000 32.0 64,800

Delivery: $30,000 to Grade Nos. 1 & 2

Grade

Sales

Value

Percent

of Total

Allocated

Cost

No. 1…………….……….…..$450,000 60.0% $18,000

* If students did not round percents to one-tenth, their answers will vary

slightly from those reported here.

**The No. 3 Grade delivery costs are given in the problem description.

Problem 22-5AB (Continued)

Part 2

GEORGIA ORCHARDS

Income Statement

For Year Ended December 31, 2015

No. 1 No. 2 No. 3 Combined

Sales (by grade)

Costs

Tree pruning and care…….…………..

194,400 129,600 81,000 405,000

Picking, sorting & grading….......... 97,200 64,800 40,500 202,500

Delivery..……………………………………

18,000 12,000 37,500 67,500

Part 3

Delivery costs include both crating and hauling costs. Georgia is able to

identify the portion of the cost directly related to the No. 3 peaches,

at least for the No. 1 and No. 2 peaches.

However, since the No. 1 and No. 2 peaches are different grades and are

sold for different prices per pound, it seems safe to assume they are crated

PROBLEM SET B

Problem 22-1B (50 minutes)

Part 1

a.

Responsibility Accounting Performance Report

Dept. Manager, Refrigerator Department

For the Month of April

Budgeted Actual Over (Under)

Amount Amount Budget

Controllable Costs

Raw materials….….…….….…….…... $400,000 $385,000 $(15,000)

Employee wages……………..…….…. 170,000 174,700 4,700

b.

Responsibility Accounting Performance Report

Dept. Manager, Dishwasher Department

For the Month of April

Budgeted Actual Over (Under)

Amount Amount Budget

Controllable Costs

Raw materials…………………..….….….$200,000 $202,000 $ 2,000

Employee wages………..….….…….…. 80,000 81,500 1,500

Problem 22-1B (Continued)

c.

Responsibility Accounting Performance Report

Plant Manager, Chicago Plant

For the Month of April

Budgeted Actual Over (Under)

Amount Amount Budget

Controllable Costs

Dept. manager salaries…....... $ 104,000 $ 101,500 $ (2,500)

Utilities….….….…….….…….…... 48,000 55,200 7,200

Building rent….….….…….….…. 80,000 82,300 2,300

Dishwasher department……… 326,000 330,200 4,200

Totals………..…..….….…….….…. $1,257,000 $1,260,900 $ 3,900

Part 2

The refrigerator department manager did a good job of controlling costs

and meeting the budget, spending $11,300 below budget. However, the

Problem 22-2B (60 minutes)

Part 1

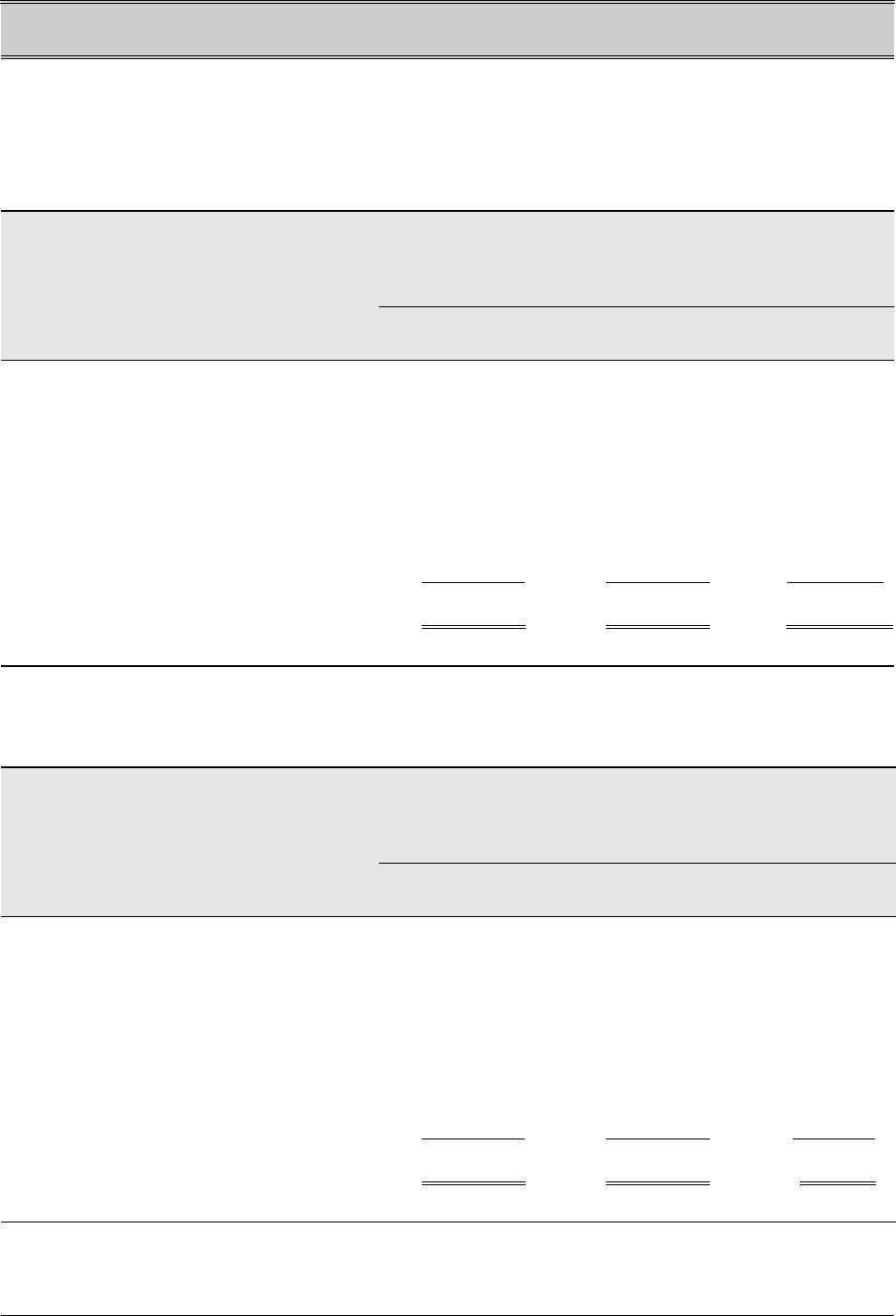

Average occupancy cost = $465,000 / 20,000 sq. ft. = $23.25 per sq. ft.

These costs are assigned to Style’s department as follows

Department Square

Footage

Rate Total

Part 2

Market rates are used to allocate occupancy costs for the building rent.

Lighting and cleaning costs are allocated to the departments on all three

floors at the average rate per square foot. Costs assigned to each class are:

Occupancy Costs

Total

Costs

Value-Based

Costs

Usage-Based

Costs

Building rent….….….…….….…. $400,000 $400,000

Value-based costs are allocated in two steps

(i) Compute market value of each floor

Floor

Square

Footage

Value per

Sq. Ft. Total

First floor……………………….…..7,500 $40 $300,000