Exercise 21-13 (30 minutes)

1. Preliminary computations

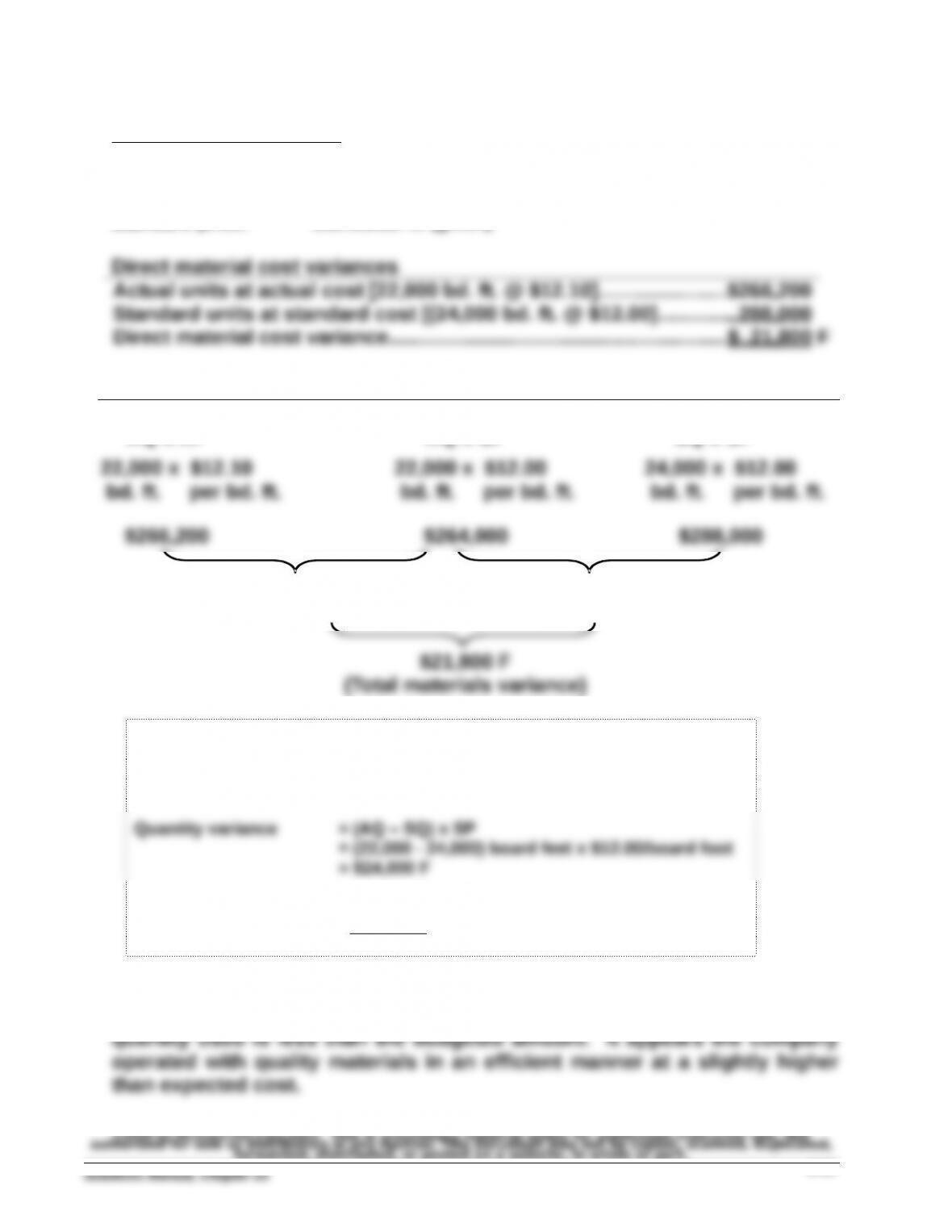

Actual quantity: 22,000 bd. ft. (given)

Standard quantity: 3,000 units x 8 bd. ft./unit = 24,000 bd. ft.

Actual price: $266,200/22,000 bd. ft. = $12.10/bd. ft.

Standard price: $12.00/bd. ft. (given)

Price and quantity variances

Actual Cost

AQ x AP AQ x SP

Standard Cost

SQ x SP

$2,200 U

(Price variance)

$24,000 F

(Quantity variance)

Alternate solution format

Price variance = AQ x (AP – SP)

= 22,000 board feet x ($12.10 – $12.00)

= $2,200 U

Price variance……….....….....$ 2,200 U

Quantity variance…….......... 24,000 F

Total variance......…....…......$21,800 F

2. The unfavorable price variance means the actual price paid is more than

the budgeted price. The favorable quantity variance means the actual

forwarded, distributed, or posted on a website, in whole or part.

Exercise 21-14A (25 minutes)

1.

Work in Process Inventory………………..………………..….….…...288,000

Direct Materials Price Variance*……………………………………….2,200

2.

Direct Materials Quantity Variance………………….….….…….….24,000

Direct Materials Price Variance………………………..……... 2,200

3. The $24,000 materials quantity variance should be investigated because of

Financial and Managerial Accounting, 6th Edition

Exercise 21-15 (25 minutes)

Part 1

Direct materials price variance:

Actual cost of direct materials used (16,000 x $4.05)…………………….…...$ 64,800

Direct materials quantity variance:

Actual quantity used x Standard price (16,000 x $4.00)…..….….….….…...$ 64,000

Part 2

Direct labor rate variance:

Actual hours x Actual rate per hour (5,545 x $19.00***)………………….……$105,355

Direct labor efficiency variance:

Actual hours x Standard rate per hour (5,545 x $20.00)………………….…..$110,900

Standard hours x Standard rate per hour (5,000** x $20.00)……………….. 100,000

Exercise 21-16 (30 minutes)

1.

October variances

Preliminary computations

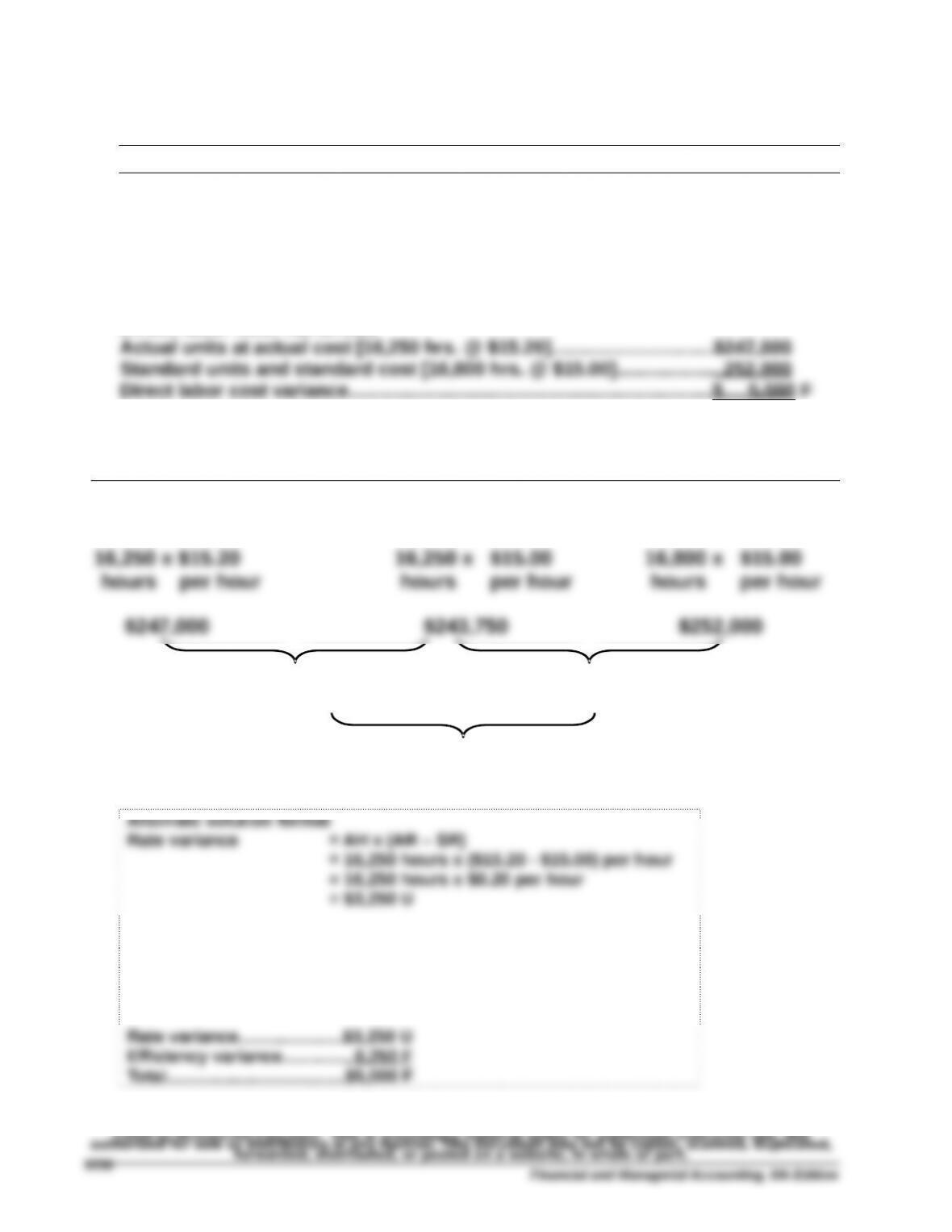

Actual hours: 16,250 hours (given)

Standard hours: 5,600 units x 3 hrs./unit = 16,800 hrs.

Actual rate: $247,000/16,250 hours = $15.20/hr.

Standard rate: $15.00/hr. (given)

Direct labor cost variances

Rate and efficiency variances

Actual Cost

AH x AR AH x SR

Standard Cost

SH x SR

$3,250 U

(Rate variance)

$8,250 F

(Efficiency variance)

$5,000 F

(Total labor variance)

Efficiency variance = (AH – SH) x SR

= (16,250 – 16,800) hours x $15.00 per hour

= (-550 hours) x $15.00 per hour

= $8,250 F

Financial and Managerial Accounting, 6th Edition

Exercise 21-16 (Concluded)

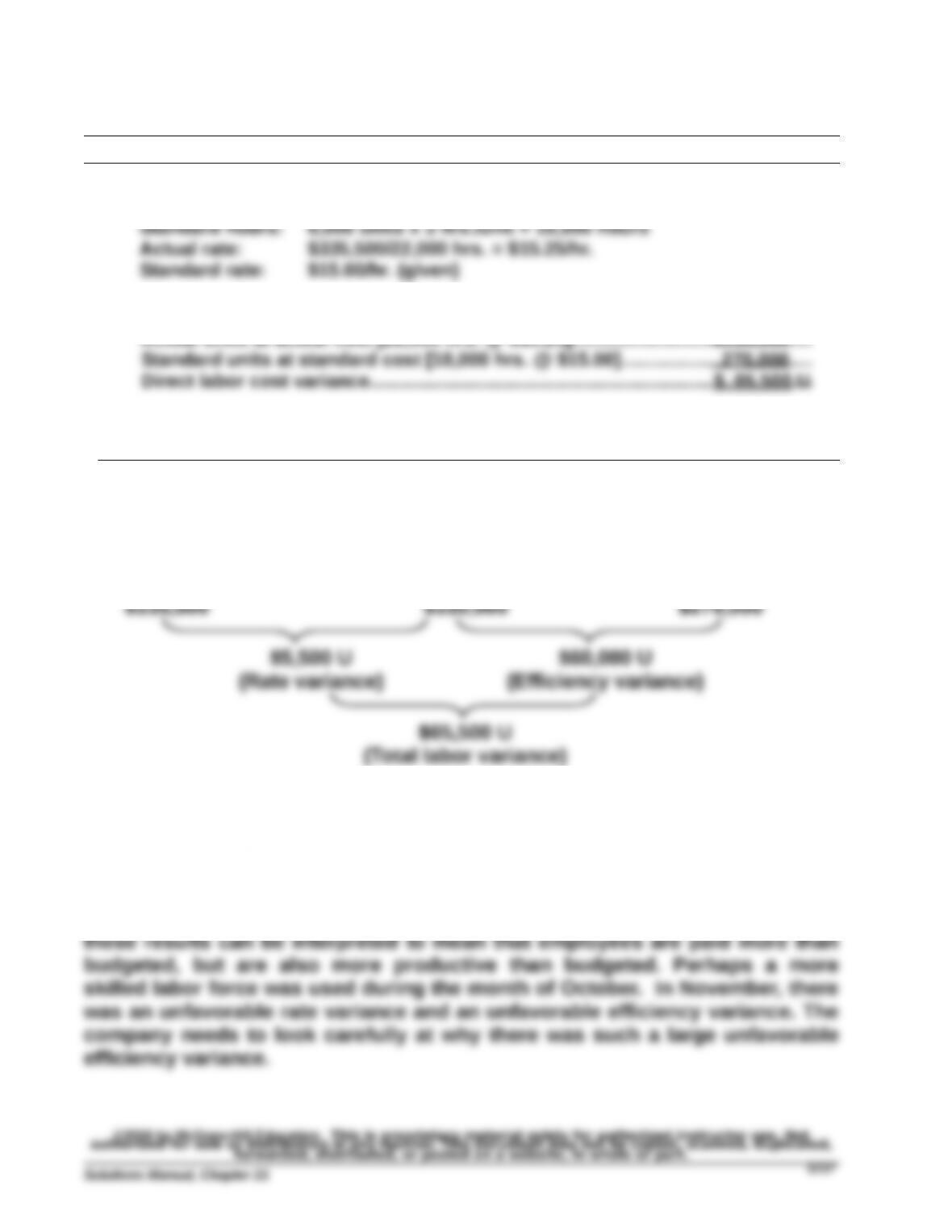

November variances

Preliminary computations

Actual hours: 22,000 hours (given)

Direct labor cost variances

Actual units at actual cost [22,000 hrs. @ $15.25]…………..……..……………………$335,500

Rate and efficiency variances

Actual Cost

AH x AR AH x SR

Standard Cost

SH x SR

22,000 x $15.25 22,000 x $15.00 18,000 x $15.00

hours per hour hours per hour hours per hour

2.

The unfavorable labor rate variance in October means the actual rate for an

hour of labor is greater than budgeted. The favorable labor efficiency

variance means the actual hours used are less than budgeted. Together,

Exercise 21-17 (20 minutes)

1. Predetermined overhead rate computations

Expected volume……………………………….…………………………... 75%

Expected total overhead……………..………………………………….. $2,100,000

Expected hours……………………………….…..….…….….….….….… 375,000 hrs.

2. Variable overhead cost variance

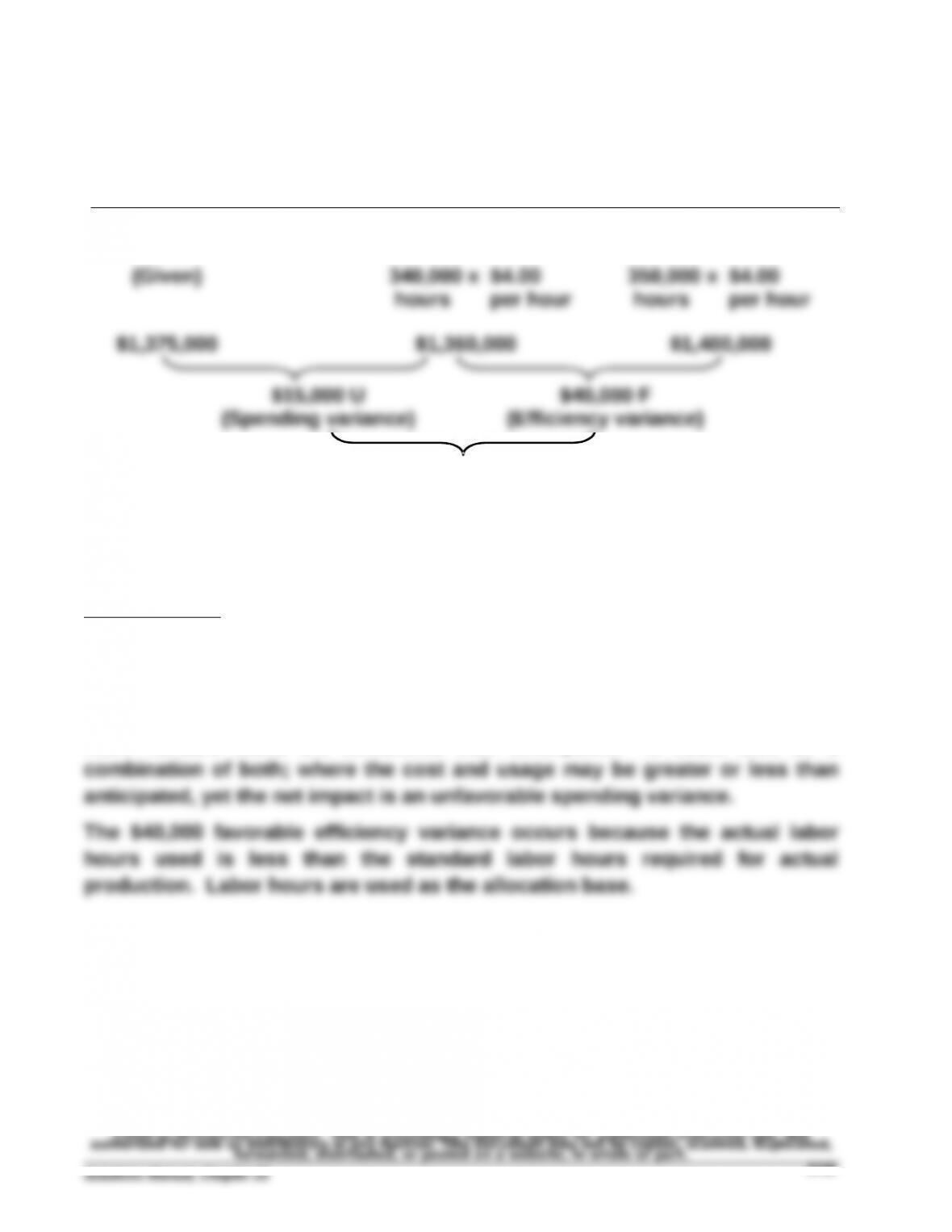

Variable overhead cost incurred [given]…………..…………………..…..….……$1,375,000

Fixed overhead cost variance

Fixed overhead cost incurred [given]…………………………….….….….$ 628,600

Financial and Managerial Accounting, 6th Edition

Exercise 21-18A (20 minutes)

1.

Variable overhead spending and efficiency variances

Actual Overhead

AH x AVR AH x SVR

Applied Overhead

SH x SVR

$25,000 F

(Total variable overhead variance)

Interpretation:

The $15,000 unfavorable spending variance means the actual cost of variable

overhead is more than budgeted. This unfavorable variance can occur

because the cost of variable overhead is greater than budgeted or because

more variable items are consumed than anticipated. It could also be a

Exercise 21-18A (continued)

2.

Fixed overhead spending and volume variances

Actual Overhead Budgeted Overhead Applied Overhead

(Given) (Given) 350,000 x $1.60

hours per hour

Interpretation

The $28,600 unfavorable spending variance means actual cost of fixed

overhead is more than budgeted.

3. The controllable variance is computed as:

Variable overhead spending variance…………….………….….… $15,000 U

Fixed overhead spending variance………………..….…….….….. 28,600 U

Controllable variance…………..……………..………………………….. $ 3,600 U

The controllable variance refers to activities that are considered within

Financial and Managerial Accounting, 6th Edition

Exercise 21-19 (20 minutes)

Information given

Planned units to be produced = 80% x 50,000 capacity = 40,000 units

Planned hours of direct labor = 25,000 hours

Total standard hrs. for actual production: 35,000 units x 0.625/unit = 21,875 hours

1. Total overhead planned at 80% level (25,000 direct labor hours)

Predetermined

Cost

Cost per

Hour

Fixed overhead………………..….….….. $ 50,000 $ 2.00

2. Total overhead variance

Total actual overhead (given)…………..……………….……………….….….……...$305,000

Exercise 21-20 (30 minutes)

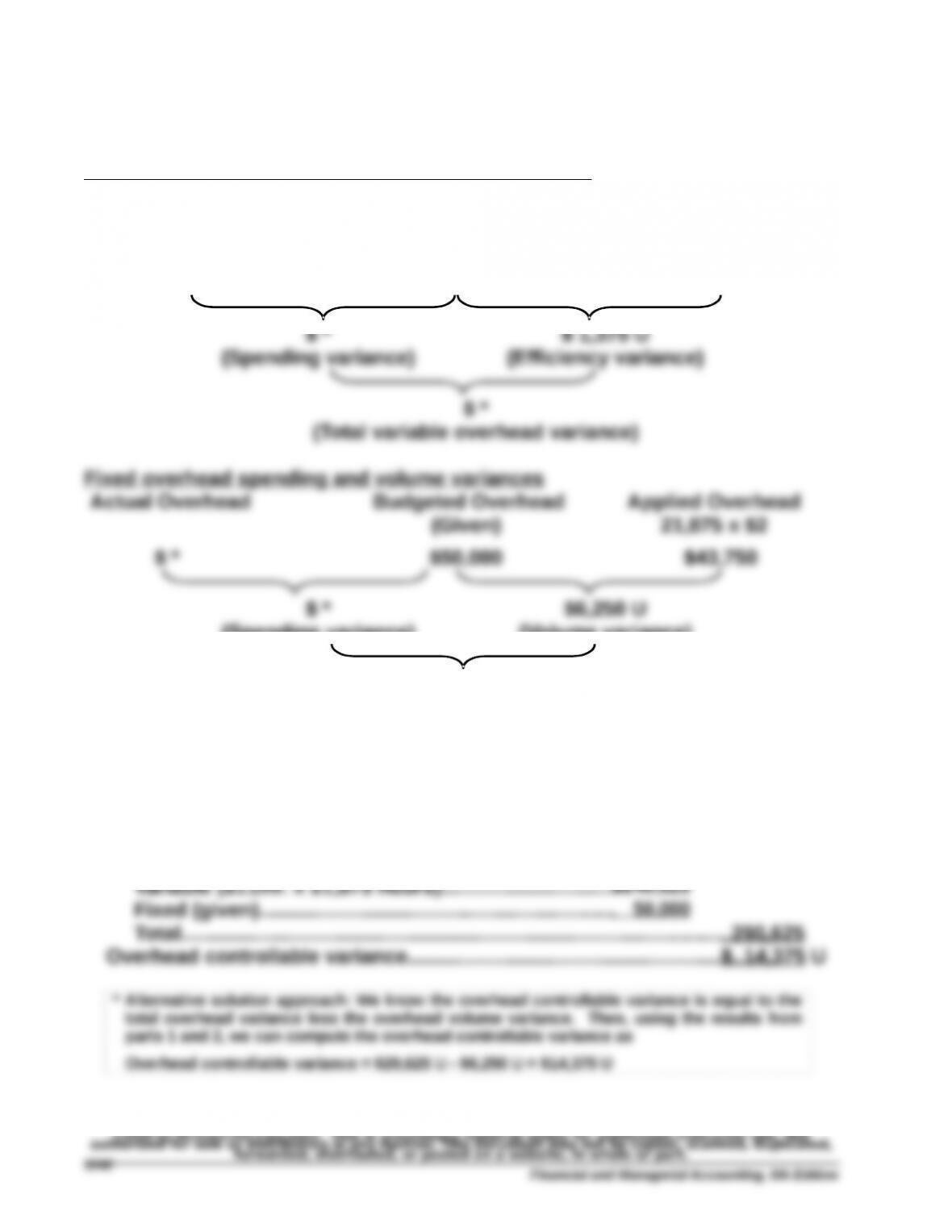

1. Preliminary variance computations

Variable overhead spending and efficiency variances

Actual Overhead

AH x AVR AH x SVR

Applied Overhead

SH x SVR

22,000 x $11 21,875 x $11

$ * $242,000 $240,625

$ *

$ 1,375 U

(Spending variance)

(Volume variance)

$ *

(Total fixed overhead variance)

* Not computable from information given

2. Overhead controllable variance*

Total actual overhead (given) $305,000

Flexible budget overhead

Financial and Managerial Accounting, 6th Edition