Exercise 18-23 (25 minutes)

1. Selling price per composite unit

5 Easy returns @ $50 each………………..…………….….….….….….….. $ 250

2. Variable costs per composite unit

5 Easy returns @ $30 each………………..…………….….….….….….….. $ 150

3 Moderate returns @ $75 each………………………………..………….… 225

3. Break-even point in composite units

Fixed costs .

= Contribution margin per composite unit

4. Unit sales of Easy, Moderate, and Business returns at break-even point

Easy: 5 x 30 units (from 3)…..….….…..…..150 units

Exercise 18-24 (30 minutes)

Instructor note: This exercise is solved in 3 steps

1. Prepare a contribution margin income statement for Co. A to compute its DOL;

Step 1.

Company A

Contribution Margin Income Statement

Sales (given)………………………………..………………….….…..….…. $6,000,000

Variable costs [$6,000,000 x (100% – 60%)]……….……………... 2,400,000

Contribution margin ($6,000,000 x 60%)…………….….….….…. 3,600,000

Step 2.

Company B

Contribution Margin Income Statement

Sales (given)………………………………..………………….….…..….…. $4,500,000

Variable costs [$4,500,000 x (100% – 25%)]……….……………... 3,375,000

Contribution margin ($4,500,000 x 25%)…………….….….….…. 1,125,000

Step 3.

Interpretation: Company A benefits more from a 20% increase in sales.

This is because we expect a 20% increase in sales to yield a 72%

increase in income (computed as 3.6 x 20%). For Company B we expect

Exercise 18-25 (10 minutes)

1. Degree of operating leverage = Total contribution margin

Pretax income

2. If sales decrease by 5%, then pretax income will decrease by 4.0 x 5%,

3. If sales decrease by 5%, a total of 9,120 (computed as 9,600 x 95%)

units will be sold.

Contribution margin income statement, assuming 5% sales decrease:

HUDSON CO.

Forecasted Contribution Margin Income Statement

For Year Ended December 31, 2016

Sales (9,120 x $225)……………….…………………………….….….….….…...$2,052,000

Variable costs (9,120 x $180)……………….……….….….….….….….….… 1,641,600

PROBLEM SET A

Problem 18-1A (25 minutes)

Parts 1 and 2

Tight Drums Company

Contribution Margin Income Statement

For Year Ended December 31, 2015

(1,000 units) Per unit % of sales

Sales ($500 x 1,000)……..……………….. $500,000 $500 100%

Variable costs

Plastic for casing…………………….…..$17,000 $17

Fixed costs

Taxes on factory……..……………..……...5,000

Factory maintenance……..………….…..10,000

Factory machinery deprec…...…........40,000

Sales equipment lease…..……..………..10,000

Accounting staff salaries…….............35,000

Part 3 Analysis Component

Contribution margin shows how much of total sales are available to cover fixed

costs and contribute to operating income. This is why the title for this statement

Problem 18-2A (45 minutes)

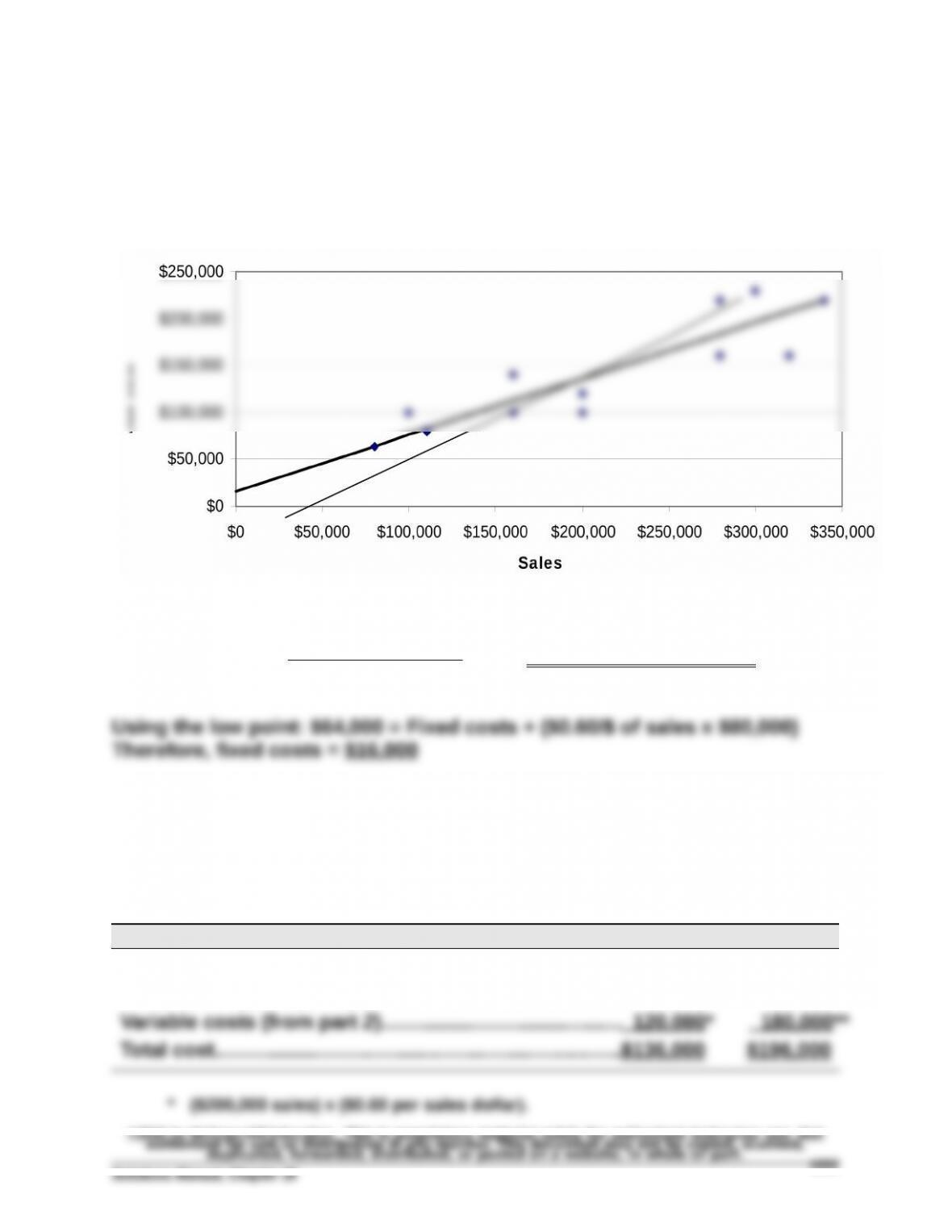

Parts 1 and 2

The scatter diagram and its estimated line of cost behavior appear below.

Part 2 – Calculation of variable and fixed costs

Variable costs = = $0.60 per dollar of sales

Part 3

The estimates in Part 2 can be used to predict the total costs that will be

incurred at sales levels of $200,000 and $300,000.

Predictions

Sales (given)………………………………..……………..….….….$200,000 $300,000

Fixed costs (from part 2)……………………….….….….….… 16,000 16,000

$220,000 – $64,000

$340,000 – $80,000

Alden Co.

Problem 18-3A (40 minutes)

Part 1

(a)Instructor note: Use the equation in Exhibit 18.11

Break-even in sales units = Fixed costs / Contribution margin per unit

(b)Instructor note: Use the equation in Exhibit 18.12

Break-even in sales dollars = Fixed costs / Contribution margin ratio

*Contribution margin ratio = $60 / $200 = 30%

Problem 18-3A (Continued)

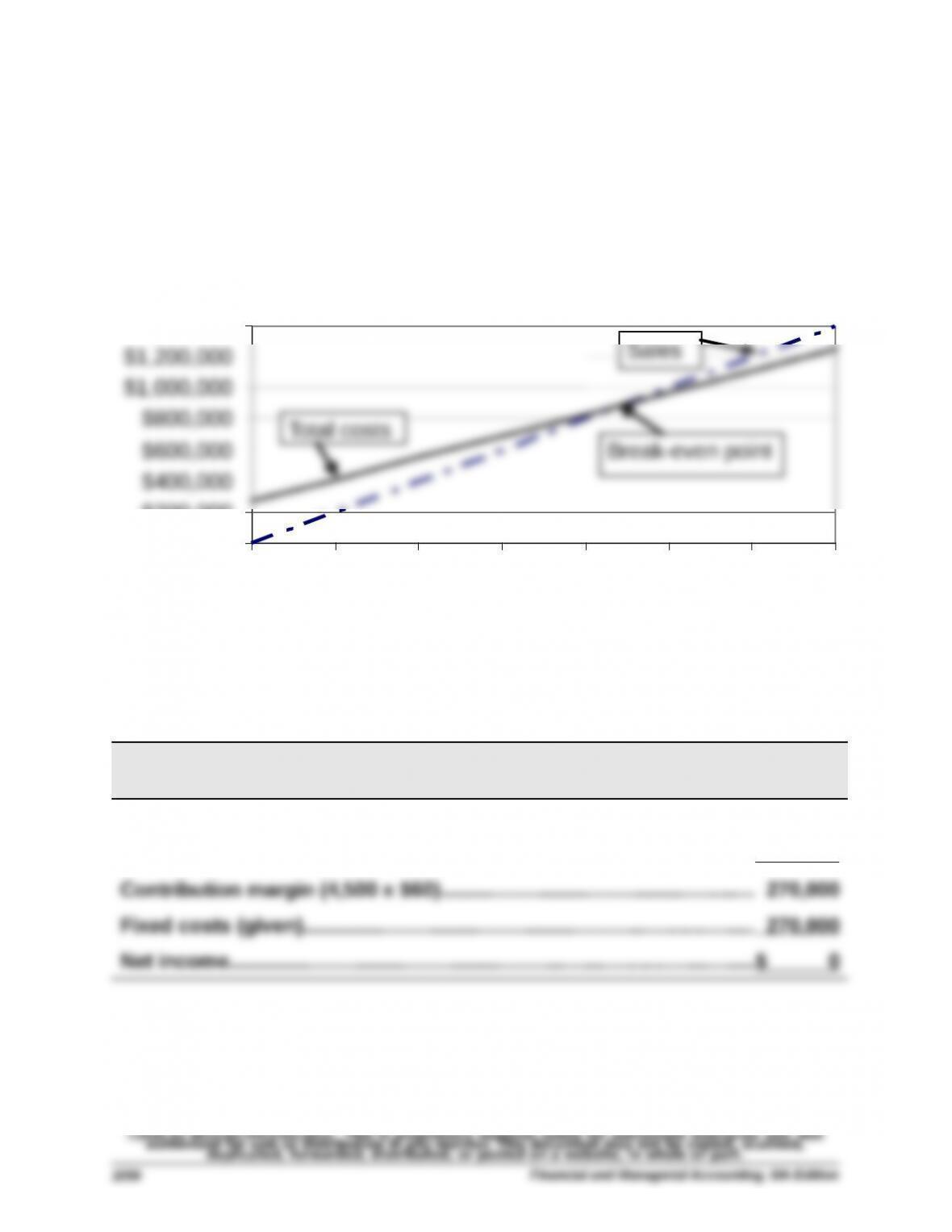

Part 2

CVP Chart for Praveen Company

$800,000

$1,000,000

$1,200,000

$1,400,000

Sales

Problem 18-4A (75 minutes)

Part 1 Instructor note: Use the equation in Exhibit 18.12

2015 break-even in sales dollars = Fixed costs / Contribution margin ratio

Part 2 Instructor note: Use the equation in Exhibit 18.12 with predicted

numbers

2016 break-even in sales dollars = Fixed costs / Contribution margin ratio

Part 3

ASTRO COMPANY

Forecasted Contribution Margin Income Statement

For Year Ended December 31, 2016

Sales (20,000 x $50)……………….…………………………….….….….….…...$1,000,000

Variable costs (20,000 x $20)……………….……….….….….….….….….… 400,000

Problem 18-4A (Continued)

Part 4 Instructor note: Use equations in Exhibits 18.22 and 18.23 with

predicted numbers

(Fixed costs + Target pretax income)

Required sales in dollars = Contribution margin ratio

Alternately:

Required sales in units = $1,083,333† / $50 Sales price per unit

= 21,667 units (rounded to whole units)

* 2015 fixed costs plus 2016 increase ($250,000 + $200,000)……………….….…..…$450,000

** Predicted contribution margin ratio ($50- $30) / $50)—from part 2……............. 60%

† Taken from “required sales in dollars” above

Part 5

ASTRO COMPANY

Forecasted Contribution Margin Income Statement

For Year Ended December 31, 2016

Sales (21,667 units x $50)………………….……………….………….….…..…..$1,083,350

Variable costs (21,667 units x $20)………….………………….….….….…... 433,340