Exercise 17-8 (25 minutes)

1. Components $1,004,000/6,000 MH $167.33/machine hour*

*rounded

Model 145 Model 212

Component Overhead

1,800 MH x $167.33/MH $ 301,194*

4,200 MH x $167.33/MH $ 702,786*

Finishing

800 WH x $155.10/WH 124,080

2,200 WH x $155.10/WH 341,220

Support

2. Model 145 Model 212

Materials & labor per unit $250.00 $180.00

3. Model 145 Model 212

Price per unit $820.00 $480.00

Model 145 appears profitable and Model 212 appears unprofitable.

Management may be inclined to stop producing Model 212, or may

Exercise 17-9 (35 minutes)

1.

Components

Changeover $500,000 / 800 batches $625/batch

Finishing

Welding $180,300 / 3,000 welding hours $60.10/WH

Support

Purchasing $135,000 / 450 purchase orders $300/PO

Model 145 Model 212

Changeover

400 batches x $625/batch $ 250,000 $ 250,000

Machining

1,800 MH x $46.50/MH 83,700

4,200 MH x $46.50/MH 195,300

Setups

Rework

160 rework orders x $250/rework order 40,000

140 rework orders x $250/rework order 35,000

Purchasing

300 purchase orders x $300/PO 90,000

150 purchase orders x $300/PO 45,000

Space & Utilities

1,500 units x $19.40/unit 29,100

Exercise 17-9 (concluded)

2. Model 145 Model 212

Materials & labor cost per unit $250.00 $180.00

3. Model 145 Model 212

Price per unit $820.00 $480.00

Both product lines appear profitable. Using ABC we see that Model

145 is not generating nearly as much profit as it appeared to generate

using the volume-based systems in Exercise 17-7 and Exercise 17-8.

Exercise 17-10 (35 minutes)

1. Total direct labor hours:

Product A: 10,000 units x 0.20 DLH/unit = 2,000 DLH

Plant-wide overhead rate:

$249,000/2,500 DLH = $99.60/DLH

Product A Product B

Direct materials

A: 10,000 units x $2/unit $ 20,000

B: 2,000 units x $3/unit $ 6,000

Direct labor

A: 2,000 DLH x $24/DLH 48,000

B: 500 DLH x $24/DLH 12,000

2. Product A Product B

Price per unit $20.00 $60.00

Cost per unit 26.72 33.90

Exercise 17-10 (concluded)

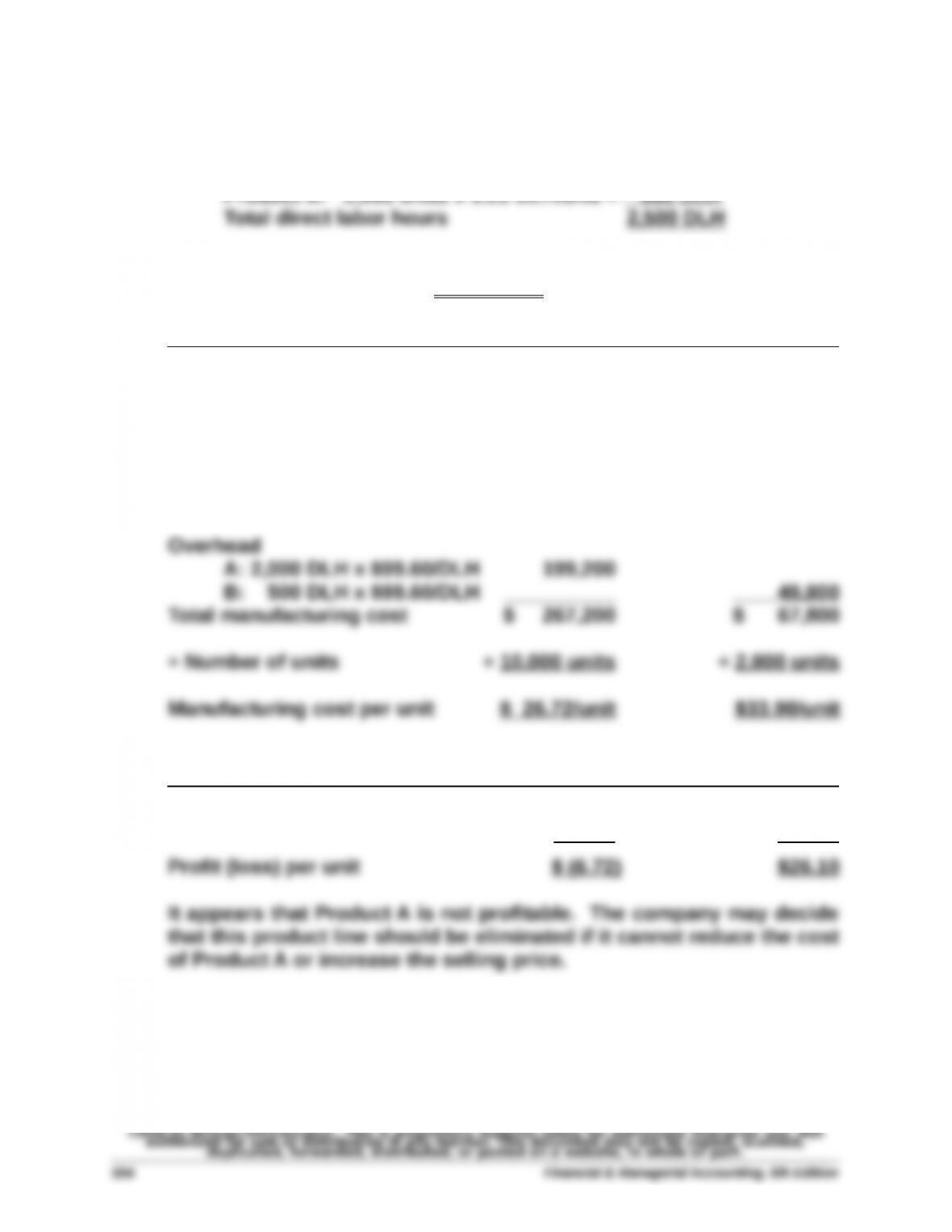

3. Overhead rates

Machine setup $121,000/(10 + 12) setups $5,500/setup

Material handling $48,000/16,000 parts* $3/part

Product A Product B

Direct Materials (from part 1) $ 20,000 $ 6,000

Direct labor (from part 1) 48,000 12,000

Overhead

Machine setup

A: 10 setups x $5,500/setup 55,000

B: 12 setups x $5,500/setup 66,000

Material handling

A: 10,000 parts x $3/part 30,000

B: 6,000 parts x $3/part 18,000

Quality control

4. Product A Product B

Price per unit $20.00 $ 60.00

Using this approach (activity based costing) the company sees that

Product B is not profitable, and Product A is profitable. The company

should evaluate the activities used to produce Product B and

Exercise 17-11 (15 minutes)

Overhead cost allocation of indirect labor and supplies to Department 1

Rate: ($5,400 + $2,600) / $32,000 = $0.25 / $ of labor cost

Overhead cost allocation of rent and utilities, general office, and

depreciation to Department 1

Total overhead allocated to Department 1

Exercise 17-12 (15 minutes)

1.

Expected Activity Activity

Activity Cost Driver Rate

1 $ 93,000 7,750 $ 12.00

2 92,000 10,000 9.20

2. and 3. Standard Deluxe

Activity 1

2,500 x $12 30,000

5,250 x $12 63,000

Activity 2

4,500 x $9.20 41,400

5,500 x $9.20 50,600

Exercise 17-13 (20 minutes)

1.

Client consultation $270,000/1,500 contact hours $180/con.hr.

Drawings $115,000/2,000 design hours $57.50/design hr.

Modeling $30,000/40,000 sq. ft. $0.75/sq. ft.

2.

Client consultation 450 contact hours x $180/con. hr. $ 81,000

Drawings 340 design hrs. x $57.50/design hr. 19,550

Modeling 9,200 sq. ft. x $0.75/sq. ft. 6,900

Exercise 17-14 (30 minutes)

Calculation of predetermined overhead rates to apply ABC

Overhead Cost

Category (Activity

Cost Pool)

Total

Cost

Total

Amount of

Cost Driver Predetermined Overhead Rate

Supervision…….………......$ 5,400 $36,000 15% of direct labor cost

1. Assignment of overhead costs to the two products using ABC

Rounded edge

Cost

Driver

Cost per

Driver Unit Assigned Cost

Supervision…………..…………... $12,200 15% $ 1,830

Machinery depreciation......... 500 hours $ 28.30 14,150

Squared edge

Cost

Driver

Cost per

Driver Unit Assigned Cost

Supervision…………..…………... $23,800 15% $ 3,570

2. Average cost per foot of the two products

Rounded edge Squared edge

Direct materials ….….…….……...... $19,000 $ 43,200

Direct labor ……………………………. 12,200 23,800

Overhead (using ABC) …….......... 23,340 84,660

*rounded

3. Using ABC, the average cost of rounded edge shelves declines and the

average cost of squared edge shelves increases. Under the current