CHAPTER 17

ACTIVITY-BASED COSTING AND ANALYSIS

Related Assignment Materials

Student Learning Objectives Discussion

Questions

Quick

Studies*

Exercises* Problems* Beyond the

Numbers

Conceptual objectives:

C1. Distinguish among the plant

wide overhead rate method, the

departmental overhead rate

method, and the activity-based

costing method.

1, 2, 3, 4 17-1, 17-2

C2. Explain cost flows for activity-

based costing.

10, 12, 13,

14, 15, 16

17-7 17-6 17-2, 17-6,

17-8

C3. Describe the four types of

activities that cause overhead

costs.

17-4, 17-13,

17-14

17-17, 17-18 17-6 17-1, 17-3,

17-6, 17-7,

17-8, 17-9

Analytical objectives:

A1. Identify and assess advantages

and disadvantages of the

plantwide overhead and

department overhead rate

methods.

5, 6, 7, 8, 9,

11

17-6 17-16 17-1, 17-2,

17-3, 17-5

A2. Identify and assess advantages

and disadvantages of activity-

based costing.

10 7-11, 17-12,

17-15

17-14, 17-16 17-1, 17-2,

17-3, 17-5

17-1, 17-2,

17-3, 17-4,

17-5

Procedural objectives:

P1. Allocate overhead costs to

products using the plantwide

overhead rate method.

17-3, 17-4 17-1, 17-4,

17-6, 17-7,

17-10, 17-16

17-1, 17-3,

17-5

P2. Allocate overhead costs to

products using the

departmental overhead rate

method.

17-5 17-5, 17-6,

17-8

P3. Allocate overhead costs to

products using activity-based

costing.

17-8, 17-9,

17-10

17-2, 17-3,

17-9, 17-10,

17-11, 17-12,

17-13, 17-14,

17-15, 17-16

17-1, 17-3,

17-4, 17-5

*See additional information on next page that pertains to these quick studies, exercises and

problems.

17-1

Additional Information on Related Assignment Material

Connect (Available on the instructor’s course-specific website) repeats all numerical Quick

Studies, all Exercises and Problems Set A. Connect provides new numbers each time the Quick

Study, Exercise or Problem is worked. It allows instructors to monitor, promote, and assess

student learning. It can be used in practice, homework, or exam mode.

Synopsis of Chapter Revision

Suja Juice Company NEW opener.

Clarified departmental overhead rate method and ABC methods as four-step processes.

Re-graded heading levels to highlight plantwide and departmental overhead rate method topics.

Expanded discussion of examples used in the ABC application, to enhance clarity.

Revised Exhibit 17.16, separating Costs of Good Quality from Costs of Poor Quality, thus

highlighting the Cost of Quality Report.

4 new Quick Studies, and some old Quick Studies repurposed to Exercises.

17-2

Chapter Outline

I. Assigning Overhead Costs

Knowing accurate costs for producing, delivering, and servicing

products helps managers set a price to cover product costs and yield a

profit. Product costs consist of direct labor, direct materials and

manufacturing overhead. Overhead costs cannot be traced to units of

product in the same way that direct labor and direct materials can.

Therefore, we must assign such overhead costs using an allocation

system.

A. Plantwide Overhead Rate Method

1. Cost Flows Under Plantwide Overhead Rate Method. This

method is also referred to as the single plantwide overhead

rate method or the plantwide overhead rate method.

a. Target of the cost object is the unit of product.

b. The rate is determined using volume-related measures

such as direct labor hours, direct labor cost dollars, or

machine hours.

c. For industries where overhead costs are closely related to

these volume-related measures, it is logical to use this

method to allocate indirect manufacturing costs to

products.

2. Applying the PlantWide Overhead Rate Method

a. Total budgeted overhead costs are combined into one

overhead cost pool.

b. This cost pool is then divided by the chosen allocation

base to arrive at a single plantwide overhead rate.

c. This rate is then applied to assign costs to all products

based on the allocation base such as direct labor hours

required to manufacture each product.

B. Departmental Overhead Rate Method – use of a single plantwide

overhead rate can produce cost assignments that fail to accurately

reflect the cost to manufacture a specific product.

1. Cost Flows Under Departmental Overhead Rate Method

a. Use of multiple overhead rates can result in better overhead

cost allocations and improve management decisions.

b. The departmental overhead rate method uses a different

overhead rate for each production department. This is

usually done through a two-stage assignment process where

departments are the cost objects in the first stage and

products are the cost objects in the second stage.

c. Overhead costs are first determined separately for each

production department. Then an overhead rate is computed

for each production department to allocate the overhead.

Notes

17-3

Chapter Outline Notes

d. This method allows each department to have its own

overhead rate and its own allocation base.

2. Applying the Departmental Overhead Rate Method – 4 step

process.

a. Step 1: Assign overhead costs to departmental cost pools.

b. Step 2: Select an allocation base for each department. If

overhead costs are common to several departments,

companies must allocate overhead to departments applying

reasonable allocation bases. Each department determines an

allocation base for its operations.

c. Step 3: Compute overhead allocation rates for each

department.

d. Step 4: Apply overhead costs to each product based on

departmental overhead rates.

e. This method usually results in more accurate overhead

allocations as compared to the plantwide rate method.

When analysts are able to logically trace costs to cost

objects, costing accuracy is improved.

C. Assessing the Plantwide and Departmental Overhead Rate

Methods

1. Advantages:

a. Based on readily available information.

b. Easy to implement.

c. Consistent with GAAP and can be used for external

reporting needs.

2. Disadvantage – overhead costs are too complex to be

explained by one factor like direct labor or machine hours.

3. Usefulness based on the single plantwide overhead rate

depends on two critical assumptions:

a. Overhead costs change with the allocation base.

b. All products use overhead costs in the same proportions.

4. Reasonableness of these assumptions varies.

a. For companies that manufacture few products or are labor–

intensive, the single plantwide method can yield

reasonably useful information.

b. For companies with many different products or ones that

use overhead costs in very different ways, the assumptions

of the single plantwide rate are not reasonable.

5. The departmental overhead rate method is more refined but

also has limitations.

17-4

Chapter Outline Notes

b. When products differ in batch size and complexity, they

usually consume different amounts of overhead costs.

D. Activity-Based Costing Rates and Method

1. Cost Flows Under Activity-Based Costing Method. Activity-

based costing (ABC) attempts to more accurately assign

overhead costs to the users of overhead by focusing on

activities.

a. Basic principle is that activities, which are tasks,

operations, or procedures, cause costs to be incurred.

b. All activities of an organization can be linked to use of

resources.

c. Activity cost pool is a collection of costs that are related to

the same or similar activity.

d. Pooling costs to determine an activity overhead (pool) rate

for all costs incurred by the same activity reduces the

number of cost assignments required.

e. The first stage of ABC is to identify activities (cost objects)

involved in manufacturing products and match those

activities with the costs they cause (drive).

f. To reduce the number of activities, the homogenous

activities (those caused by the same factor) are grouped

into activity cost pools.

g. The second stage is to compute an activity rate for each cost

pool and then use this rate to allocate overhead costs to

products.

h. ABC is similar to the departmental method in that it uses

more than one overhead rate. It differs from the

departmental method in that it focuses on activities rather

than departments.

II. Applying Activity-Based Costing – Activity-based costing

accumulates overhead costs into activity cost pools and then allocates

those costs to products using activity rates. This involves four steps:

(1) identify activities and the costs they cause, (2) group similar

activities into activity cost pools, (3) determine an activity rate for

each activity cost pool, and (4) allocate overhead costs to products

using those activity rates.

A. Step 1: Identify Activities and the Costs They Cause

1. Commonly done through discussions with employees in

production departments and through review of production

17-5

Chapter Outline Notes

B. Step 2: Trace Overhead Costs to Cost Pools

1. Step 2 involves assigning activities and their overhead costs to

cost pools. These costs are commonly accumulated by each

department in a traditional accounting system. Some costs are

traced directly to a specific activity cost pool.

2. Activity-based costing provides more detail about the activities

and the costs they cause than is provided from traditional

costing methods.

3. To form cost pools, companies look for costs that are caused by

the same or similar activities within each activity level.

Pooled costs include only those costs related to the same

driver.

C. Step 3: Determine Activity Rates

1. Step 3 is to compute activity rates used to assign overhead

costs to final cost objects such as products.

2. Proper determination depends on (1) proper identification of

the factor that drives the cost in each activity cost pool, and (2)

proper measures of activities.

3. The cost driver is that activity causing costs in the pool to be

incurred.

4. Next, an activity driver, a measure of activity level, is

determined for use as the allocation base.

5. Examples of activity drivers include: number of products

devised or modified, number of square feet occupied, and the

number of batches.

6. To compute the activity rate, total cost in an activity cost pool

is divided by the measure of the activity.

D. Step 4: Assign Overhead Costs to Cost Objects

1. Step 4 is to assign overhead costs in each activity cost pool to

final cost objects using activity rates.

2. Overhead costs in each activity cost pool are allocated to

product lines based on the actual level of activity used,

multiplied by a predetermined activity rate for each cost pool.

3. The unit overhead cost is computed by dividing total overhead

cost allocated to the product lines by the number of product

units.

4. When ABC is used, overhead costs commonly shift from

standardized, high-volume products to low-volume,

customized specialty products that consume more resources.

17-6

Chapter Outline Notes

E. Differences between ABC and Multiple Departmental Rates.

1. ABC recognizes that overhead costs are complex and

emphasizes activities and costs of these activities.

2. ABC better reflects the complex nature of overhead costs and

how these costs are used in making products.

III. Assessing Activity-Based Costing

A. Advantages of Activity-Based Costing

1. More Accurate Overhead Cost Allocation – because (1) there

are more cost pools, (2) costs in each pool are more similar,

and (3) allocation is based on activities that cause overhead

costs.

2. More Effective Overhead Cost Control – can be used to

identify activities that can benefit from process improvement.

Also helps managers effectively control overhead cost by

focusing on processes or activities instead of only direct labor.

3. Focus on Relevant Factors – provides better customer

profitability information by including all resources consumed

to serve a customer. Allows managers to make better pricing

decisions on custom orders and to better manage customers by

focusing on those that are most profitable.

4. Better Management of Activities – helps managers identify the

causes, or activities that drive costs. Activity-based

management is an out-growth of ABC that draws on the link

between activities and cost incurrence for better management.

Activity-based management can be useful in distinguishing

value-added activities which add value to a product from non-

value-added activities, which do not.

5. Costs of quality–costs resulting from manufacturing

defective products or providing services that do not meet

customer expectations. Costs of quality include prevention,

appraisal, internal failure and external failure costs. Can be

summarized in a cost of quality report.

B. Disadvantages of Activity-Based Costing

1. Costs to Implement and Maintain ABC. Collecting and

analyzing cost data are expensive and so is maintaining an

ABC system.

2. Uncertainty with Decisions Remains. Managers must

interpret ABC data with caution in making managerial

decisions. Managers must examine carefully the

controllability of costs before making decisions.

C. ABC for Service Providers – ABC also applies to service

providers. The only requirements are the existence of costs and

demand for reliable cost information.

17-7

Chapter Outline

D. Types of Activities:

1. Unit level activities – performed on each product unit. Costs

tend to change with the number of units produced

2. Batch level activities – performed only on each batch or group

of units. Costs do not vary with the number of units, but with

the number of batches.

Notes

3. Product level activities – performed on each product line and

are not affected by either the number of units or batches. Costs

do not vary with the number of units or batches.

4. Facility level activities– performed to sustain facility capacity as

a whole and are not caused by any specific product. Costs do

not vary with what is manufactured, number of batches, or the

output quantity.

IV. Global View: Many lean manufacturers embrace lean accounting, which

has two key components:

A. First, the company applies lean thinking to eliminate waste in its

accounting process.

B. Instead of focusing on cost allocation methods, such as activity-based

costing, the company develops alternative performance measures that

better reflect the benefits of manufacturing process changes.

V. Decision Analysis: Customer Profitability. Companies cause the ABC

method to analyze their customer profitability. ABC encourages

management to consider all resources consumed to serve a customer, not

just manufacturing costs that are the focus of traditional costing methods.

17-8

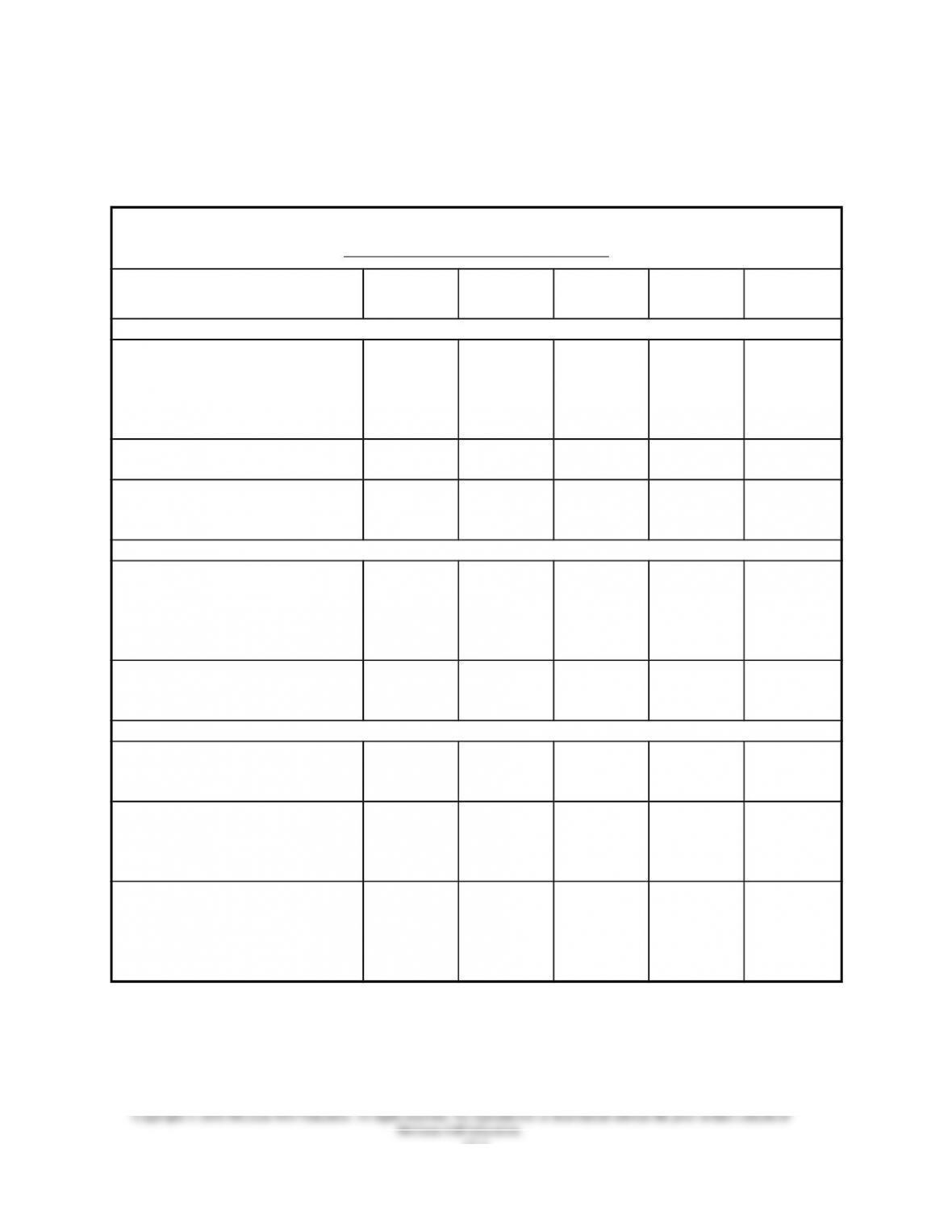

Chapter 17 Alternate Demonstration Problem #1

Windy River Float Trips uses activity-based costing to compute the cost of

the river raft trips. Each raft holds six customers and a guide. The costs

for these float trips are as follows:

Activities (cost driver) Costs

Trailer rent fee (trip) $127 per trip

Advertising (trips) 215 per trip

Insurance (trips) 50 per trip

Depreciation (trips, people) 40 per trip plus $8 per person

Wages (trips, guides) 400 per trip per guide

Shore lunch (people) 60 per person

Compute the cost of a raft trip with 4 rafts, 24 customers and 4 guides.

17-9

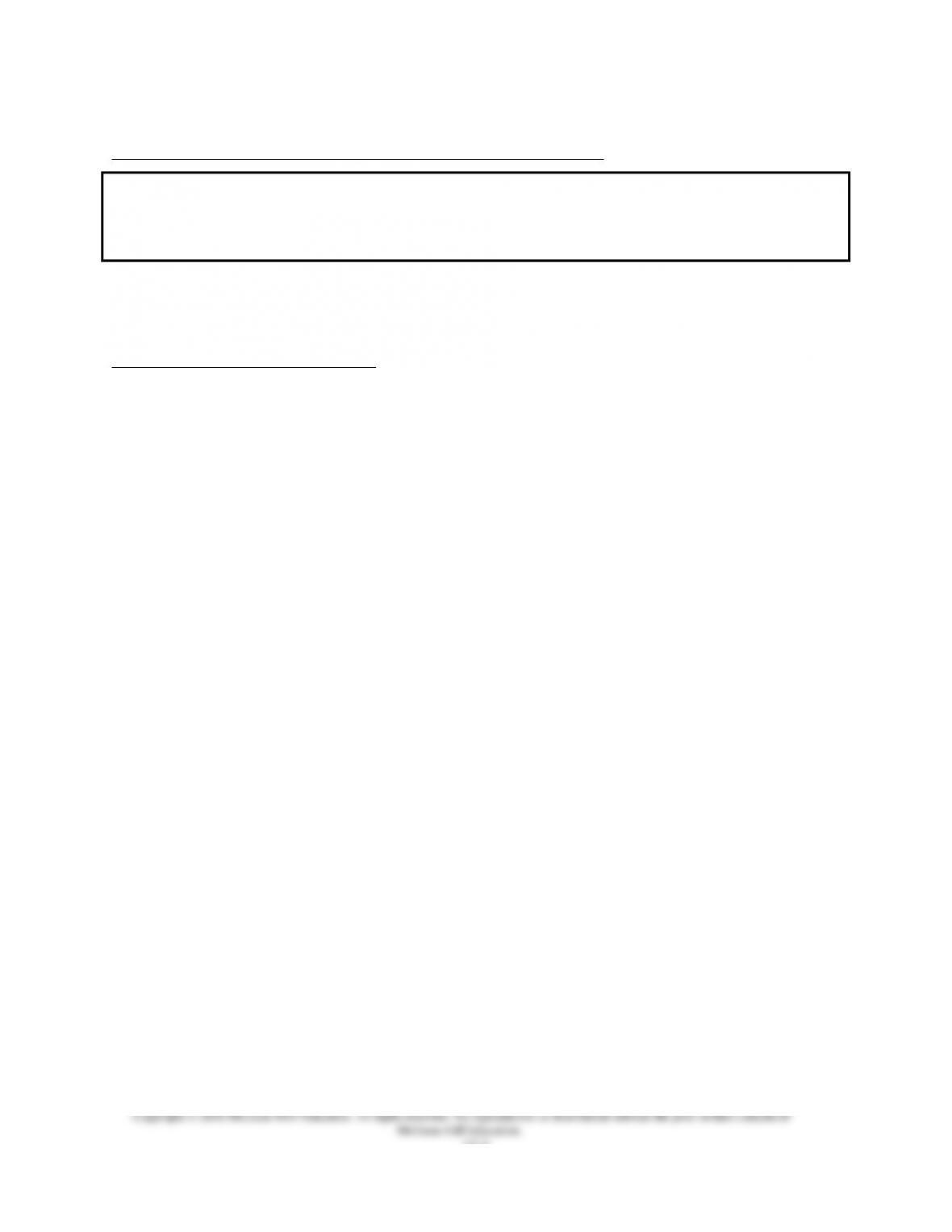

Solution: Chapter 17 Alternate Demonstration Problem #1

Activities River Float Trips

Trailer Rent Fee $ 127

Advertising 215

Insurance 50

17-10