Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

Chapter 16

Process Costing and Analysis

QUESTIONS

1. The main deciding factor in choosing between a job order costing system or a

process costing system is the type of product or service. Examples where a

process costing system is likely appropriate include chemicals, cleaning fluids, mail

services, and consulting. (Hybrid systems are also common.)

2. The main focus in process costing is the production department (process).

3. Yes, services can be delivered by processes. For example, Federal Express delivers

4. The journal entries to match cost flows with product flows are primarily the same

for both process costing and job order costing. In process costing, the materials

5. A materials consumption report is an alternative control document.

6. The computation of equivalent units of production focuses on converting partially

completed units to a measure in terms of completed units. We need to use EUP

because some units of the production process are partially completed at the end of

completed.

7. The two main methods of process costing are the weighted-average and the first-in,

first-out (FIFO) methods. The weighted-average method considers “average flow”

8. A process cost accounting system treats labor that is used entirely within one

9. Direct labor costs flow first from the Factory Payroll account to the Work in Process

10. At the end of the accounting period the Factory Overhead account should have a

zero balance.

11. Yes, it is possible to have either underapplied or overapplied overhead in a process

12. Equivalent units for direct materials differ from that for direct labor (and overhead) if

direct materials and direct labor (and overhead) are added at different stages in the

13. The four steps in accounting for production activity (for process operations) are: 1)

14. The process cost summary serves at least three purposes: (a) to help department

managers control their departments; (b) to help factory managers evaluate

department managers’ performances; and (c) to provide cost information for the

15. Yes. Google might use process costing to determine the cost of manufacturing

16. Likely processing steps for digital televisions include making the frame and

preparing the televisions for shipping.

Financial and Managerial Accounting, 6th Edition

QUICK STUDIES

Quick Study 16-1 (5 minutes)

1. Job order operation 4. Job order operation

Quick Study 16-2 (5 minutes)

Quick Study 16-3 (10 minutes)

1. Process operation. 5. Job order operation.

Quick Study 16-4 (10 minutes)

Units

Units in beginning inventory 150,000

+ Units started 310,000

= Total units to account for 460,000

Quick Study 16-5 (10 minutes)

Equivalent units under the weighted-average method

Equivalent

EUP for conversion—Weighted average Units

Units completed and transferred out (340,000 x 100%)..................... 340,000

Quick Study 16-6 (10 minutes)

Equivalent units under the FIFO method

Equivalent

EUP for conversion—FIFO Units

Equivalent units to complete beginning WIP (150,000 x 20%)......... 30,000

Equivalent units started and completed*............................................ 190,000

* Units completed – Units in beginning work in process = Units started and completed

340,000 – 150,000 = 190,000

Quick Study 16-7 (5 minutes)

Cost per equivalent unit of production--weighted-average method

Beginning inventory cost + Current production costs = $394,900 + $907,500

Equivalent units of production 740,000

Quick Study 16-8 (10 minutes)

Equivalent units under the weighted-average method

Equivalent

EUP for conversion—Weighted average Units

Units completed and transferred out (680,000 x 100%)..................... 680,000

Units of ending work in process

Financial and Managerial Accounting, 6th Edition

Quick Study 16-9 (15 minutes)

Equivalent units under the FIFO method

Equivalent

EUP for conversion—FIFO Units

Equivalent units to complete beginning WIP (320,000 x 75%)......... 240,000

Equivalent units started and completed*............................................ 360,000

Quick Study 16-10 (15 minutes)

Equivalent units of production—Weighted average

Direct

Materials Conversion

Units completed & transferred out (9,000 x 100%)...............9,000 9,000

Units of ending work in process

Direct materials, 3,000 x 80%...............................................2,400

Quick Study 16-11 (25 minutes)

Cost per equivalent unit—Weighted average

Direct

Materials Conversion

Costs of beginning work in process.............................. $ 996 $ 585

Costs incurred this period.............................................. 10,404 12,285

Total costs........................................................................ $11,400 $12,870

Financial and Managerial Accounting, 6th Edition

Quick Study 16-12 (10 minutes)

Cost assignment—Weighted average

Direct

Materials Conversion

Costs of units transferred out

Direct materials (9,000 EUP* x $1.00 per EUP)......... $9,000

Conversion (9,000 EUP* x $1.30 per EUP)................ 11,700

Total costs transferred out............................................ $20,700

Costs of ending work in process

Direct materials (2,400 EUP* x $1.00 per EUP)......... 2,400

*EUP from QS 16-10

**Equals costs to account for of $24,270, computed as $1,581 + $10,404 + $12,285

Quick Study 16-13 (5 minutes)

Work in Process Inventory—Painting..........................20,700

Work in Process Inventory—Assembly................. 20,700

To transfer costs of goods across departments.

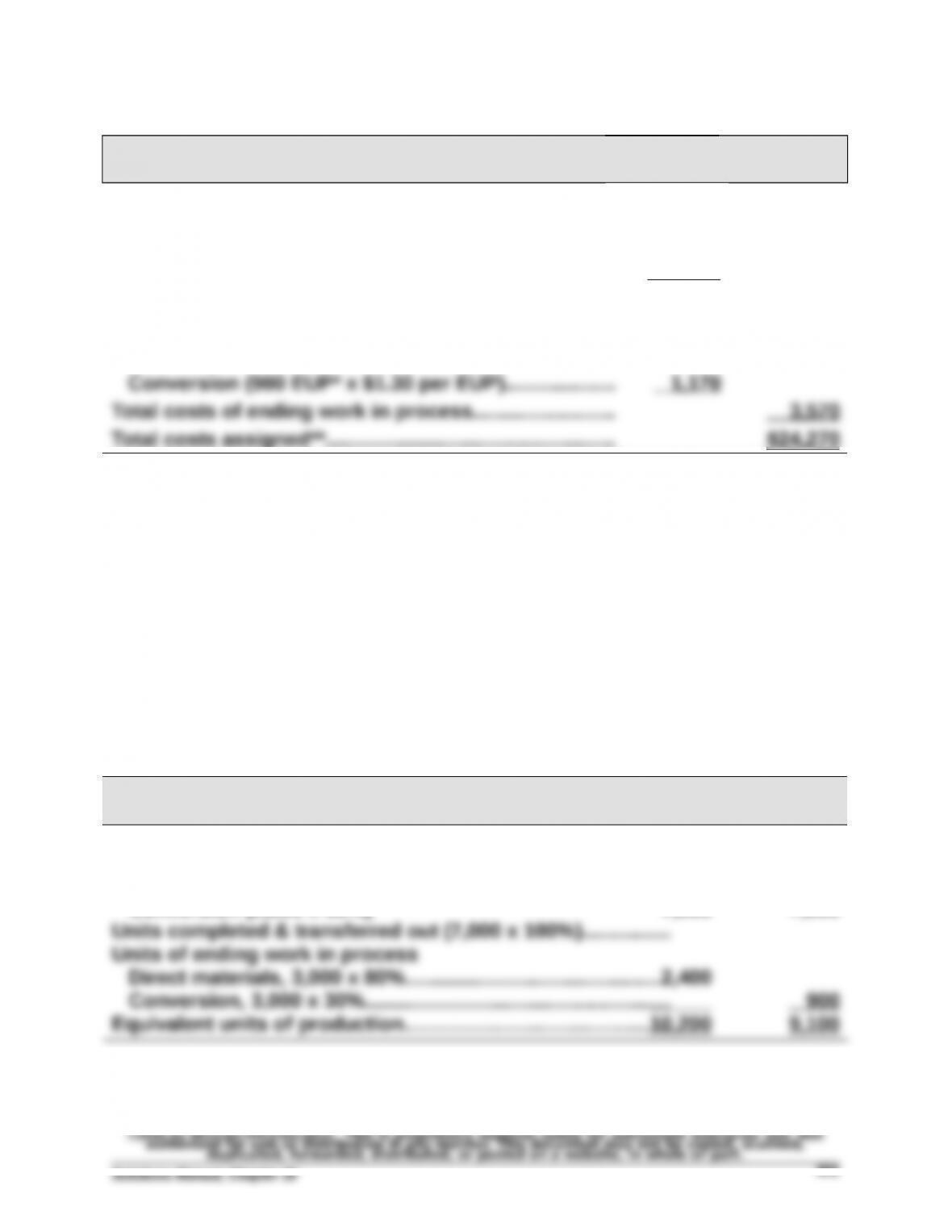

Quick Study 16-14 (15 minutes)

Equivalent units of production—FIFO

Direct

Materials Conversion

Units to complete beginning work in process

Direct materials (2,000 x 40%)..............................................

Conversion (2,000 x 60%)

800

7,000

1,200

7,000

Quick Study 16-15 (5 minutes)

Cost per equivalent unit – FIFO

Direct

Materials Conversion

Costs incurred this period.............................................. $10,404 $12,285

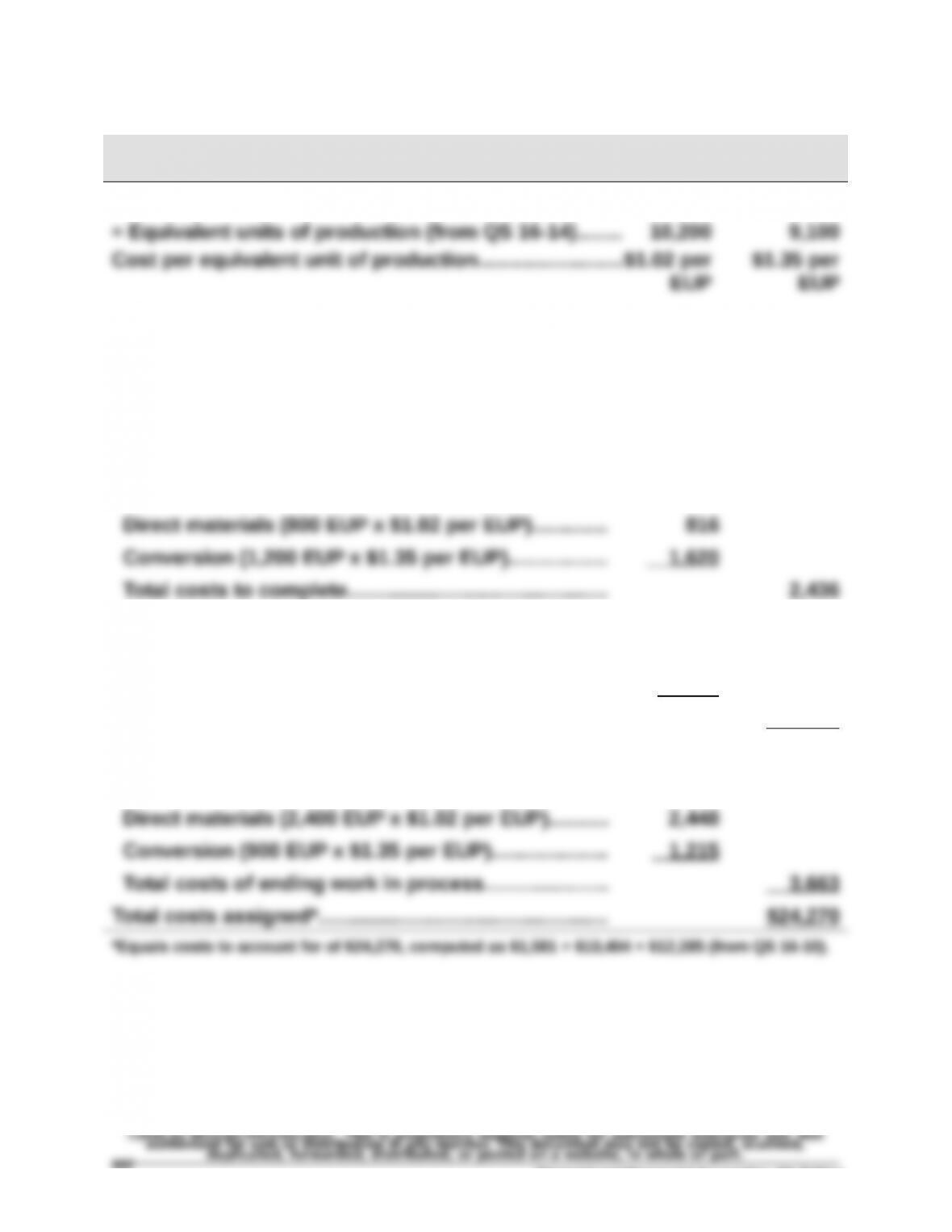

Quick Study 16-16 (20 minutes)

Assignment of costs to output of department—FIFO

Costs of units transferred out

Cost of beginning work in process inventory............ $ 1,581

Costs to complete beginning work in process

Cost of units started and completed this period

Direct materials (7,000 EUP x $1.02 per EUP).......... 7,140

Conversion (7,000 EUP x $1.35 per EUP)................. 9,450

Total cost of units started and completed................ 16,590

Total costs of units transferred out............................. $20,607

Cost of ending work in process inventory

Financial and Managerial Accounting, 6th Edition

902

Quick Study 16-17 (5 minutes)

Work in Process Inventory—Painting..........................20,607

Quick Study 16-18 (10 minutes)

a)

Equivalent units of production—Weighted average

Direct

Materials

Units completed & transferred out (17,000 x 100%).............17,000

Units of ending work in process

b)

Cost per equivalent unit—Weighted average

Direct

Materials

Costs of beginning work in process.............................. $ 1,200

Costs incurred this period.............................................. 27,900

Total costs........................................................................ $29,100

Quick Study 16-19 (10 minutes)

Cost assignment—Weighted average

Direct

Materials

Costs of units transferred out

Direct materials (17,000 EUP x $1.50 per EUP)........ $25,500

Costs of ending work in process

Quick Study 16-20 (10 minutes)

The ending balance in Work in Process Inventory—Cutting is $7,100 and

the ending balance in Work in Process Inventory—Binding is $17,042, as

computed below.

Work in Process—Cutting

Beg. Inventory 3,445

Dir. materials 8,240

Conversion 11,100

Work in Process—Binding

Beg. Inventory 6,426

Transferred-in 15,685

Dir. materials 6,356

Conversion 18,575

Financial and Managerial Accounting, 6th Edition