Exercise 15-4 (15 minutes)

1.

Rate = = = 130%

2.

Direct materials……………….……………………………………..….…………... $15,350

Direct labor………………..……………….………………..……..…….…………... 3,200

Exercise 15-5 (20 minutes)

2. Total cost of job in process (given)………….……………………………….…..$ 50,000

Less materials cost of job in process (given)……….…………..……….…. (30,000)

Exercise 15-6 (15 minutes)

1. Raw Materials Inventory……………………….………….…….76,200

2. Work in Process Inventory………………..……………….…..48,000

3. Work in Process Inventory………………..……………….…..15,350

4. Work in Process Inventory………………..……………….…..18,420

Estimated overhead costs

Estimated direct labor

$747,500

$575,000

Exercise 15-7 (30 minutes)

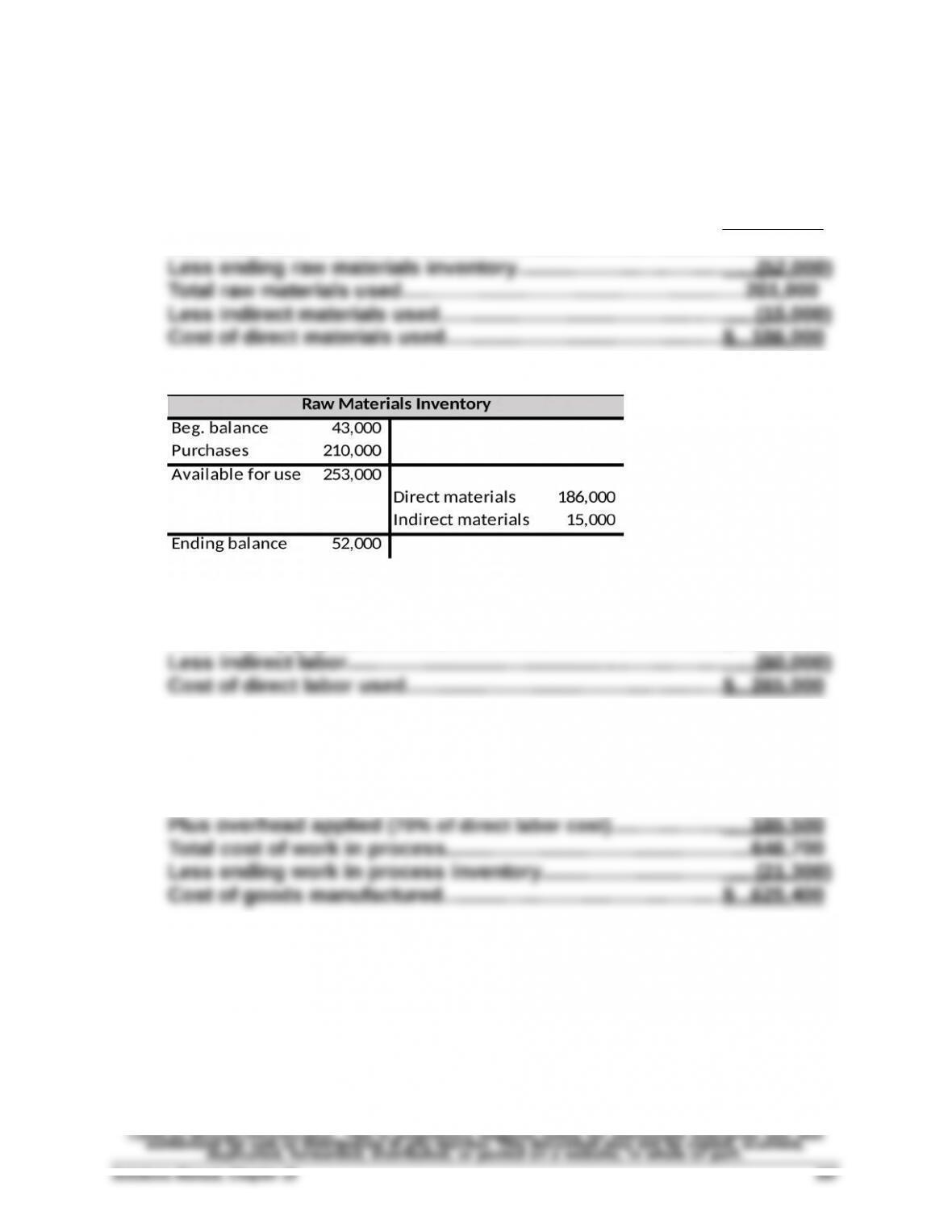

1. Cost of direct materials used

Beginning raw materials inventory…………….……………….…………….$ 43,000

Plus purchases……………………………….………………………………….…… 210,000

Raw materials available……………..……………….………………….………..253,000

2. Cost of direct labor used

Total factory payroll…………..……………..………………….………….………$ 345,000

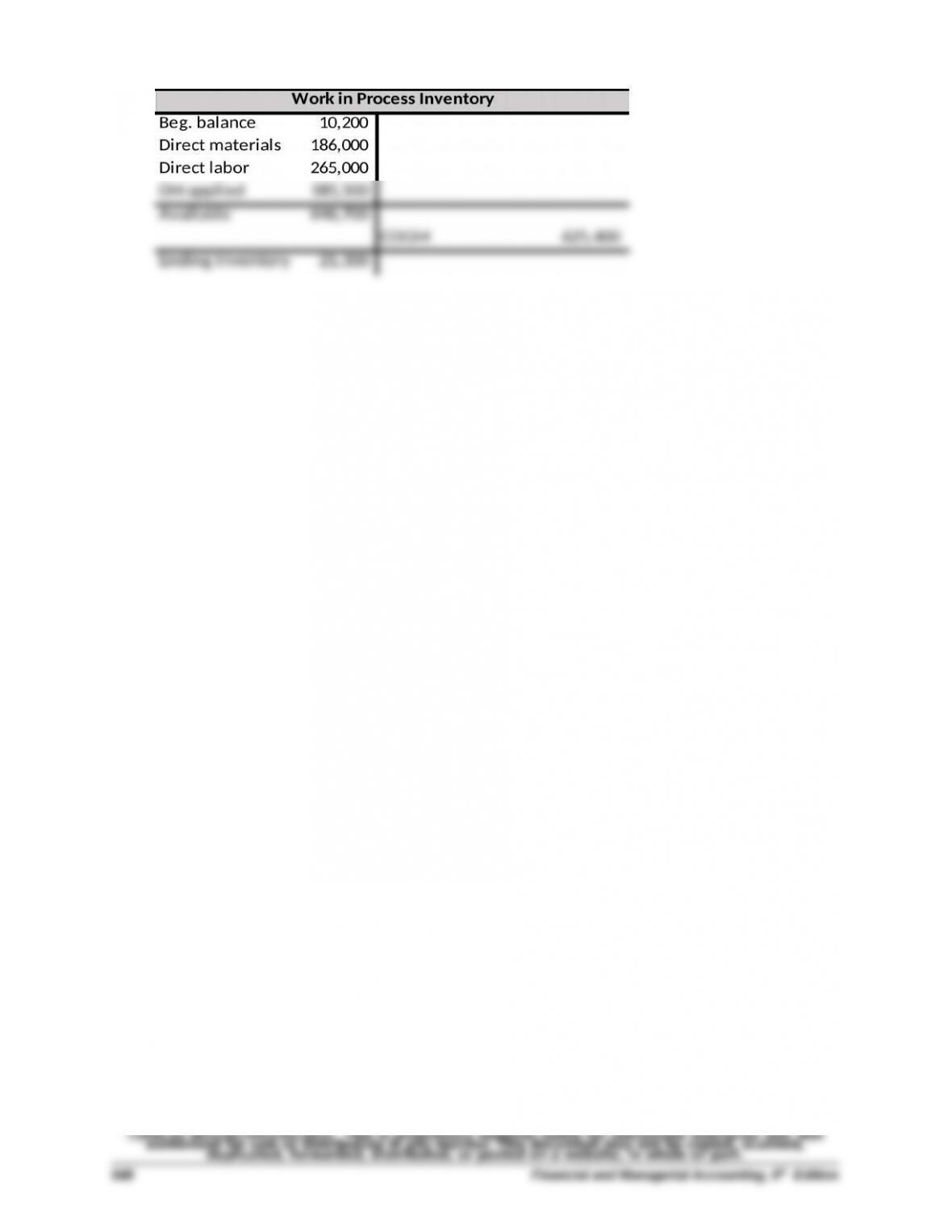

3. Cost of goods manufactured

Beginning work in process inventory…………….………………….……..$ 10,200

Plus direct materials……………..………………………………….………….…. 186,000

Plus direct labor…………………………….……………………..….………….…. 265,000

Exercise 15-7 (continued)

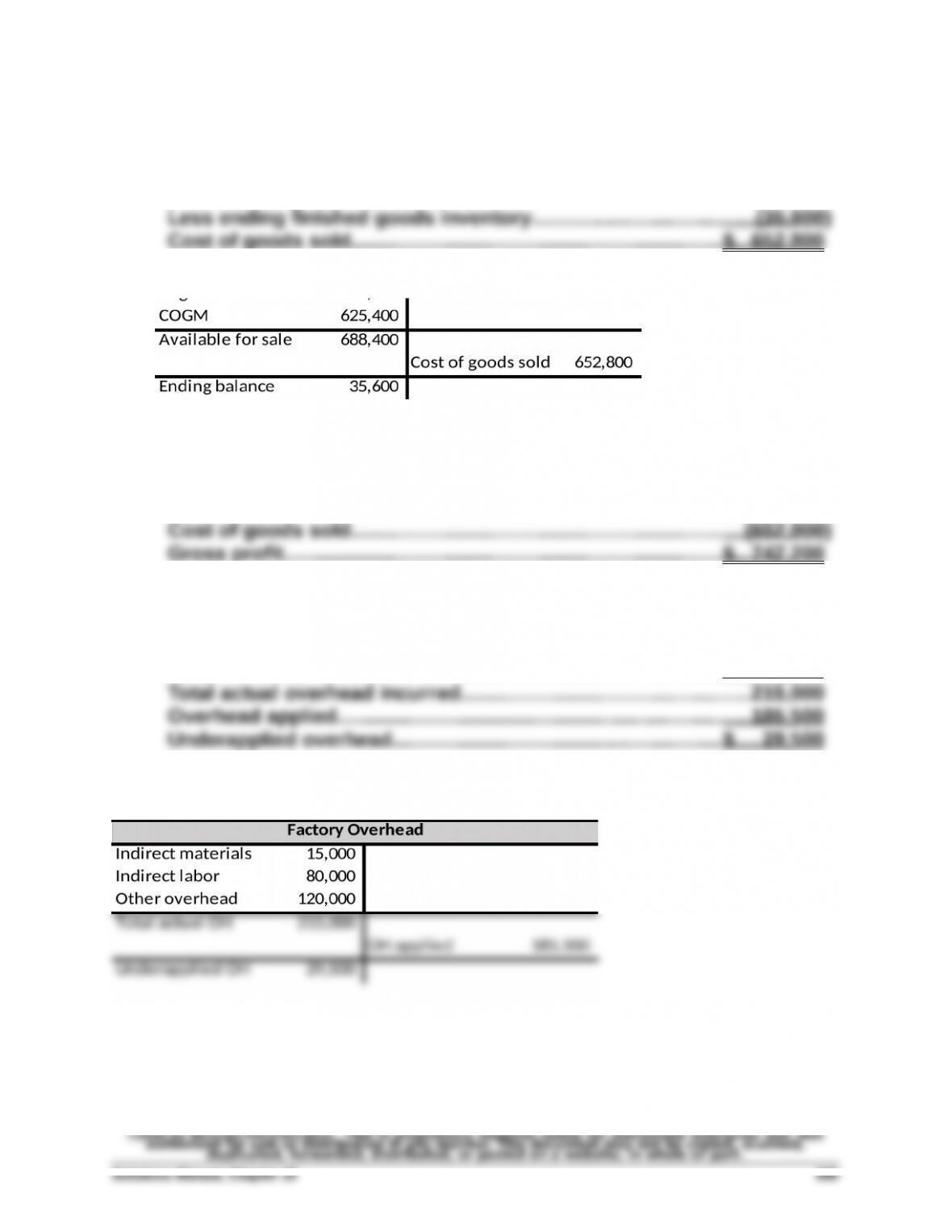

4. Cost of goods sold

Beginning finished goods inventory……………..………………………….$ 63,000

Plus cost of goods manufactured……………….…….………….………….625,400

5. Gross profit

Sales……………..………………………………..……………………….………….….$1,400,000

6. Actual overhead incurred

Indirect materials…………………………………………………..…………………$ 15,000

Indirect labor……………….…………………………………………………………..80,000

Other overhead costs…………………………………….…….………….……… 120,000

Exercise 15-8 (10 minutes)

1. Raw Materials Inventory………………………..……….………210,000

2. Work in Process Inventory……….………………..…….…….186,000

To assign direct materials to jobs.

3. Factory Overhead……….………………….……………………...15,000

Exercise 15-9 (10 minutes)

1. Work in Process Inventory……….………………..…….…….265,000

2. Factory Overhead……….………………….……………………...80,000

3. Factory Payroll Payable…………………….………………..….345,000

Exercise 15-10 (10 minutes)

1. Factory Overhead………………..……………..………………….120,000

2. Work in Process Inventory……….………………..…….…….185,500

Exercise 15-11 (10 minutes)

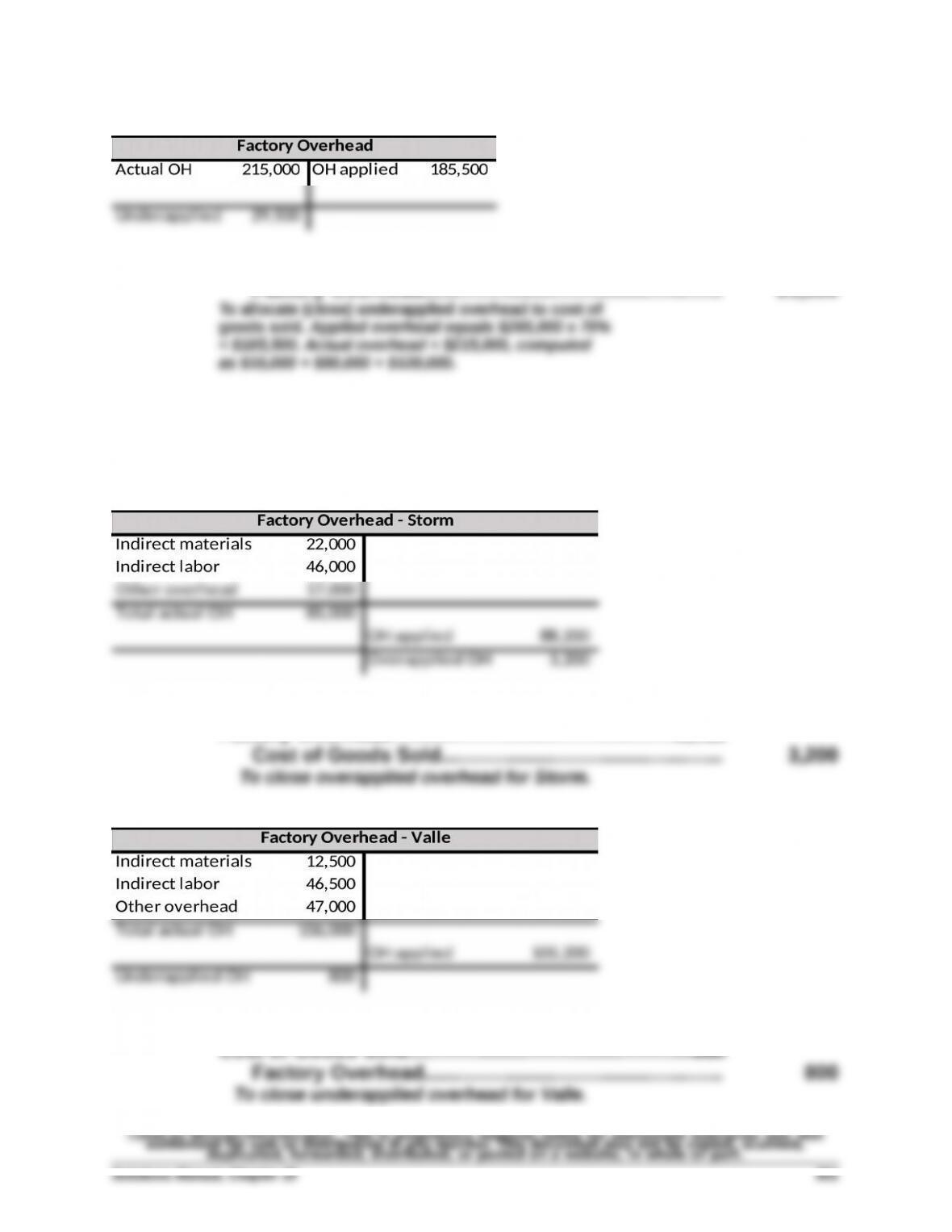

Cost of Goods Sold…………………………………………..……29,500

Factory Overhead………….……………..……………..…… 29,500

Exercise 15-12 (15 minutes)

Factory Overhead………………..……………..………………….3,200

Exercise 15-13 (25 minutes)

a. Raw Materials Inventory……………………….………….…….90,000

Accounts Payable…………………..…….…….…………... 90,000

To record materials purchases.

d. Factory Overhead………………..……………..………………….11,475

Cash…………………………………..………………………….... 11,475

To record other factory overhead paid.

e. Work in Process Inventory………………..……………….…..47,500

Factory Overhead………….……………..……………..…… 47,500

To apply overhead to jobs at the rate of 125% of

direct labor cost.

f. Finished Goods Inventory……………….…………..…………56,800

Work in Process Inventory…………..……….…….……. 56,800

To record jobs completed.

Exercise 15-14 (35 minutes)

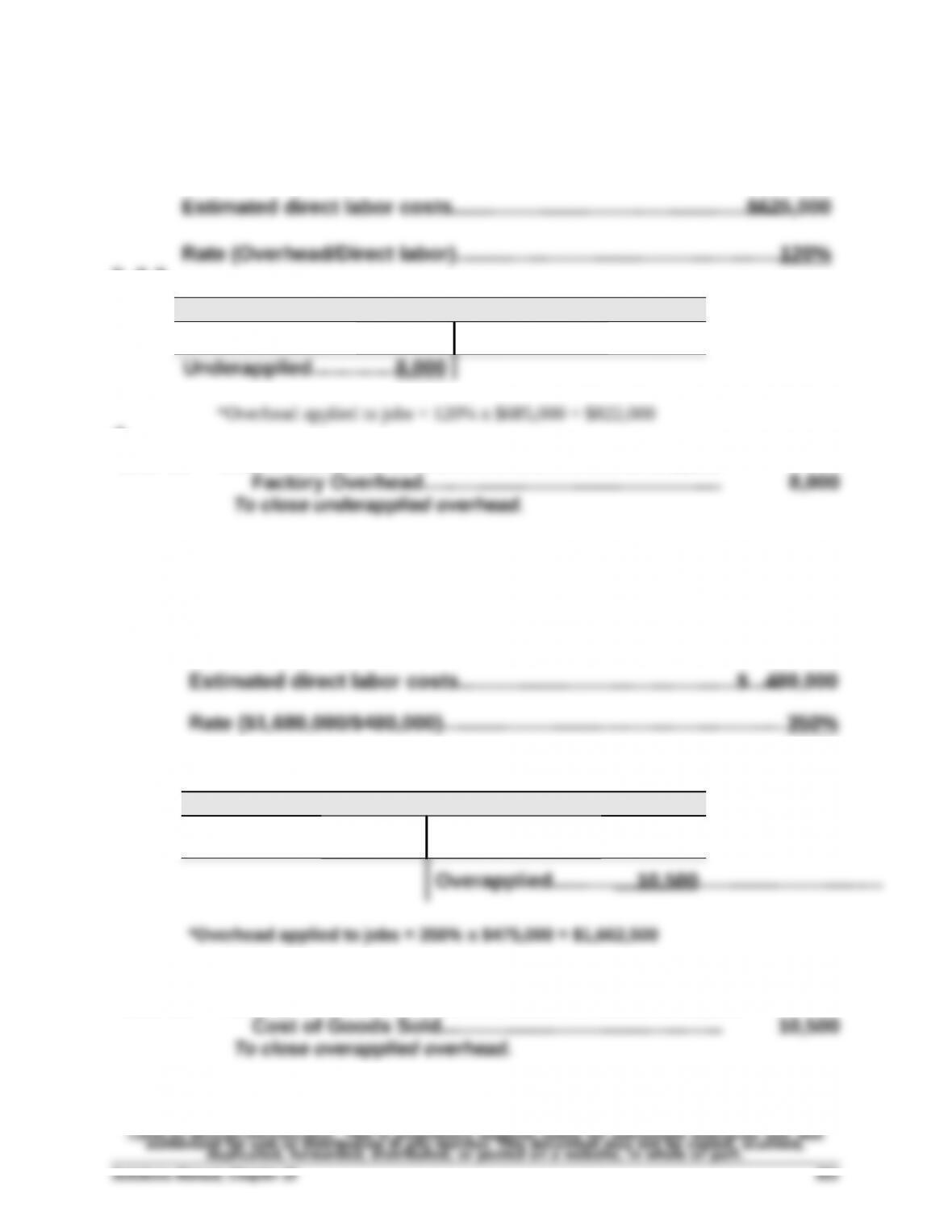

1. Predetermined overhead rate

Estimated overhead costs………………….……………………….…………$750,000

2. & 3.

Factory Overhead

Incurred……….…………...830,000 Applied*………………………….……………..…….…….…822,000

4.

Dec. 31 Cost of Goods Sold………………………..………………………8,000

Exercise 15-15 (25 minutes)

1. Predetermined overhead rate

Estimated overhead costs………….……………….………………….…….$1,680,000

2. & 3.

Overhead

Incurred……….…………...1,652,000 Applied*…………………………….…………………..….….1,662,500

4.

Dec. 31 Factory Overhead………………..……………….………….…….10,500

Exercise 15-16 (30 minutes)

1. Overhead rate = Total overhead costs / Total direct labor costs

2.

Total cost of work in process inventory……….………………..… $ 71,000

Deduct: Direct labor………………..……………..…………..……….…. (20,000)

3.

Total cost of finished goods inventory…….…….….………….… $490,000

We also know that the total of direct labor costs (X) and factory

overhead costs (0.6X) equals $240,000. Thus, to get the individual