Chapter 15

Job Order Costing and Analysis

QUESTIONS

1. Factory overhead is not identified with specific units (jobs) or batches (job lots).

Therefore, to assign costs, estimates of the relation between factory overhead cost

2. Several other factors (allocation bases) are possible and reasonable. These common

factors often include direct materials or machine hours.

3. The job order cost sheet captures information on cost and quantity of direct material

production and to estimate total cost of production.

4. Each job is assigned a subsidiary ledger account. This account serves as the

“posting account” (accumulates all increases and decreases) during production for

direct material, direct labor, and applied factory overhead. The collection of job cost

5. A debit (increase) to Work in Process Inventory for direct materials, a debit (increase)

6. The materials requisition slip is designed to track the movement of materials from

7. The time ticket is used to record how much time an employee spends on each job.

8. Debits (increases) to factory overhead are the recording of actual overhead costs,

9. Assuming that the overapplied or underapplied overhead is immaterial, it is closed to

the Cost of Goods Sold account. However, if the amount is material—meaning it

10. This production run should be accounted for as a job lot (batch). Although individual

iPhones could be viewed as individual jobs, the costs of tracking this detailed

11. A predetermined factory overhead rate must be calculated for at least two reasons:

(1) Not all costs are known in advance, yet the costs must be applied to products

during the current period. (2) A predetermined rate is used to spread indirect costs

12. Each patient in a hospital can be viewed as a “job.” In this case, a job order cost

13. Each of the 30 luxury motorcycles will likely be accounted for as an individual job.

Although similar in many respects, each would have custom features that would

14. Sprint employees can use job cost sheets to accumulate the costs (e.g. labor and

materials) used on each job. Managers can use this job cost information to monitor

QUICK STUDIES

Quick Study 15-1 (5 minutes)

Manufactured as a job: 3, 4, 6

Quick Study 15-2 (10 minutes)

Quick Study 15-3 (10 minutes)

Finished Goods Inventory……….…………………..…..…....10,500

Work in Process Inventory……….………………..….….. 10,500

To transfer cost of completed job to Fin. Goods.

Quick Study 15-4 (15 minutes)

Raw Materials Inventory……………………..……….…..….…50,000

Cash…………………………………..………………….………… 50,000

To record raw material purchases.

Quick Study 15-5 (10 minutes)

Work in Process Inventory…………..………………..….…...140,000

Factory Wages Payable………………..…..…..….…..…. 140,000

To record direct labor.

Quick Study 15-6 (10 minutes)

1. Factory overhead, $117,000 / Direct labor, $468,000 = 25%

Quick Study 15-7 (10 minutes)

Work in Process Inventory…………..………………..….…...117,900

Factory Overhead………….………………..………….….... 117,900

To apply overhead [($175,000–$44,000) x 90%].

Quick Study 15-8 (5 minutes)

Quick Study 15-9 (5 minutes)

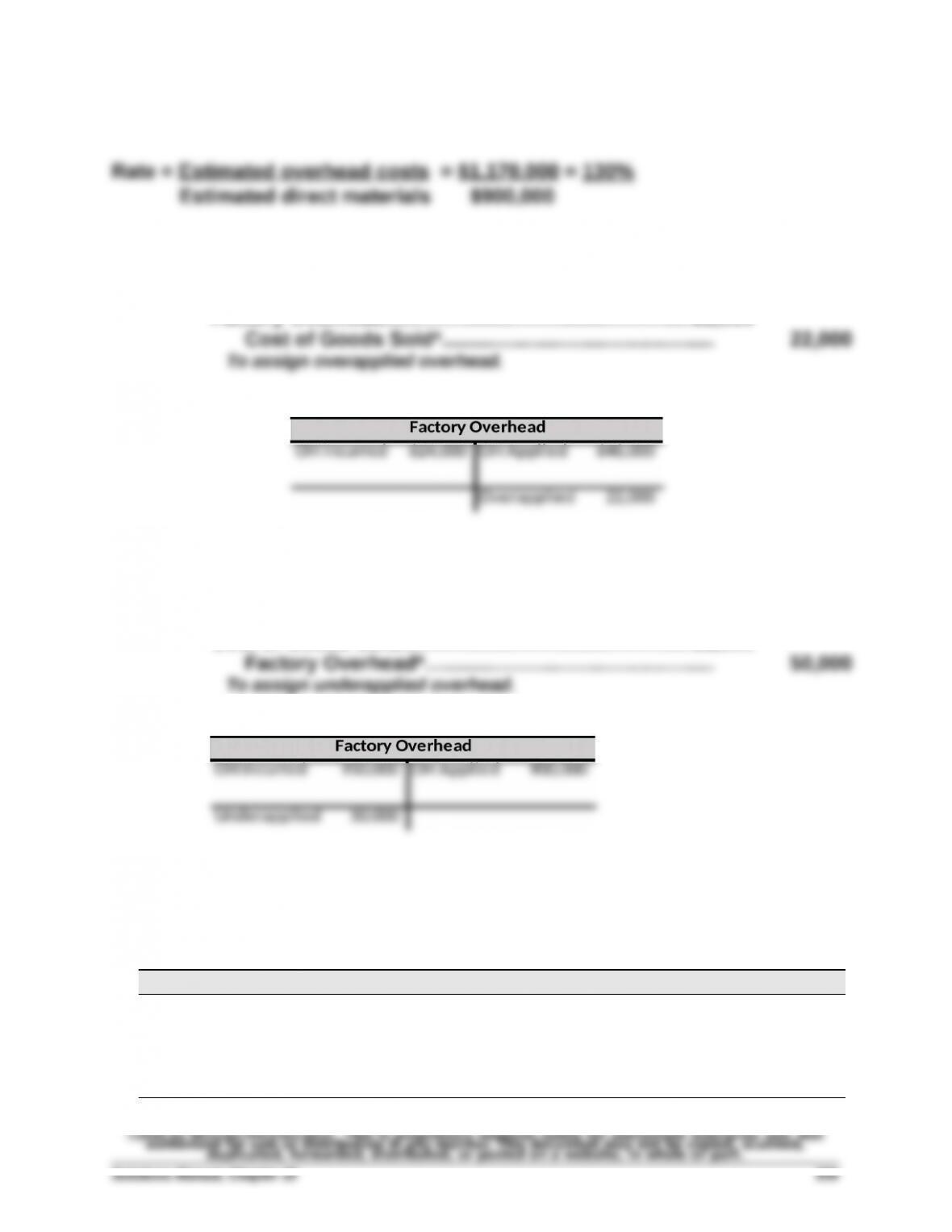

Factory Overhead……….…………………….……………..…....22,000

Quick Study 15-10 (15 minutes)

Cost of Goods Sold………………………………………….…....50,000

Quick Study 15-11 (10 minutes)

Overhead Applied

Job 1 ($5,000 x 40%)…..….…......... $2,000

Job 2 ($7,000 x 40%)…..….….........

Job 3 ($1,500 x 40%)…..….….........

2,800

600

Quick Study 15-12 (10 minutes)

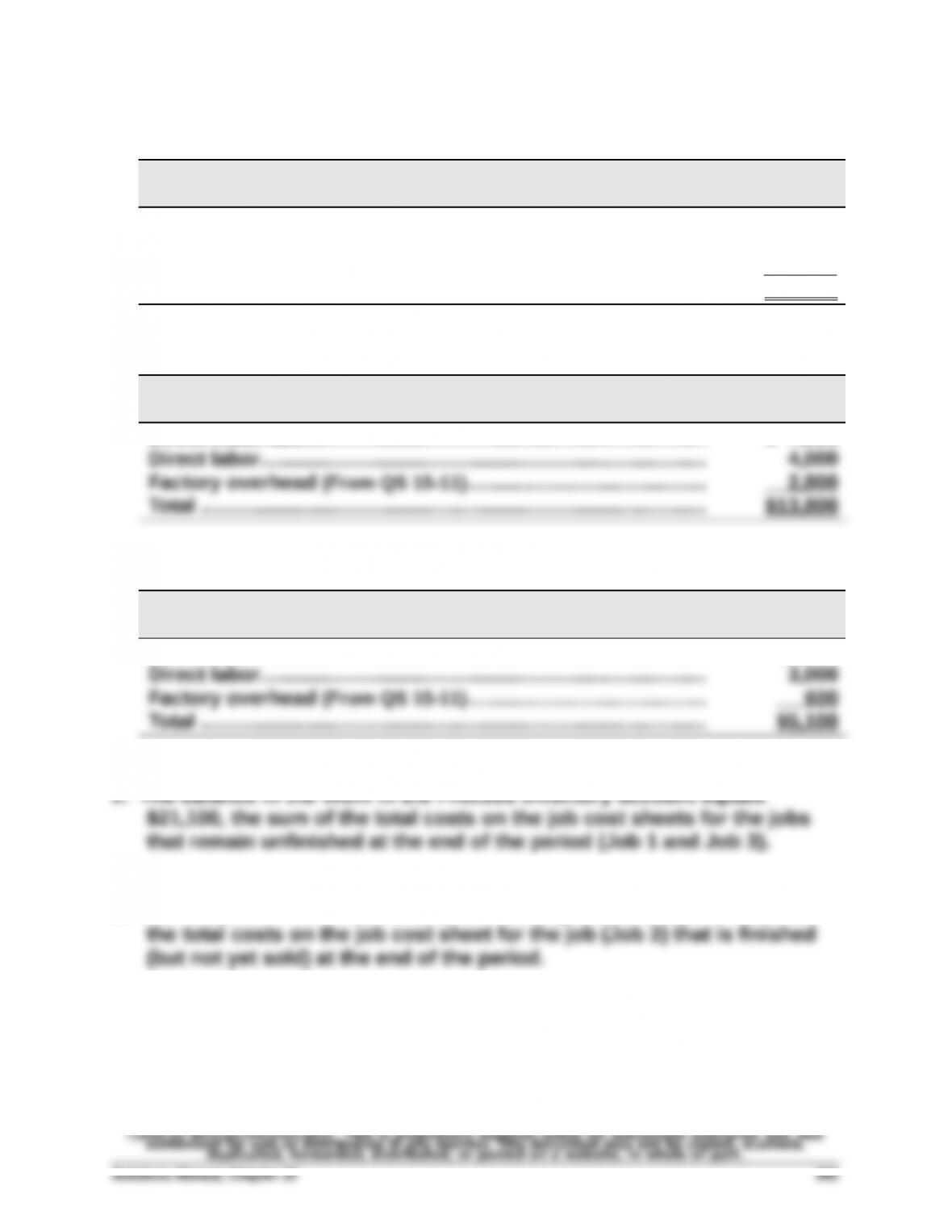

1.

JOB COST SHEET

Job 1

Direct materials……………….…………………………..…..….…..….…

Direct labor………………..……………….……………….…..….…..….…

$ 5,000

9,000

Factory overhead (From QS 15-11)..….……………………………… 2,000

Total ……………………………..……………..………………………..…..…. $16,000

JOB COST SHEET

Job 2

Direct materials……………….…………………………..…..….…..….…

$ 7,000

JOB COST SHEET

Job 3

Direct materials……………….…………………………..…..….…..….…

$1,500

3. The balance in the Finished Goods Inventory account equals $13,800,

Quick Study 15-13 (10 minutes)

JOB COST SHEET

Direct labor ($50 x 200)…………………………………..………….….. $10,000

Quick Study 15-14 (5 minutes)

Since each car is custom-ordered, Porsche produces in jobs rather in job

EXERCISES

Exercise 15-1 (10 minutes)

Exercise 15-2 (15 minutes)

JOB COST SHEET: Job 9-1005

Direct materials

Q-4698.…………………………………....$1,250

Q-4725………………..….…..….…..…… 1,000 $2,250

Direct labor

Exercise 15-3 (25 minutes)

1.The cost of direct materials requisitioned in the month equals the total

direct materials costs accumulated on the three jobs less the amount of

direct materials cost assigned to Job 102 in May:

Job 102 …………………………………….…………..… $15,000

Less prior costs………………..….…..…..…..….... ( 6,000 ) $ 9,000

2.Direct labor cost incurred in the month equals the total direct labor

costs accumulated on the three jobs less the amount of direct labor cost

assigned to Job 102 in May:

Job 102 …………………………………….………………....$8,000

Less prior costs…………………….…..……….…..…... (1,800 ) $ 6,200

Job 103 …………………………………….……………….... 14,200

3.The predetermined overhead rate equals the ratio of the amount of

overhead assigned to jobs divided by the amount of direct labor cost

assigned to them. Since the same rate is used for all jobs started and

completed within a month, the ratio for any one job equals the rate that

was applied. This table shows the ratio for jobs 102 and 104:

Job 102 Job 104

Overhead……………..……………………..………………..$ 4,000 $10,500

4.The cost transferred to finished goods in June equals the total costs of

the two completed jobs for the month, which are Jobs 102 and 103:

Job 102 Job 103 Total

Direct materials……………..….…..…... $15,000 $33,000 $48,000