Problem 13-2B (60 minutes)

Part 1

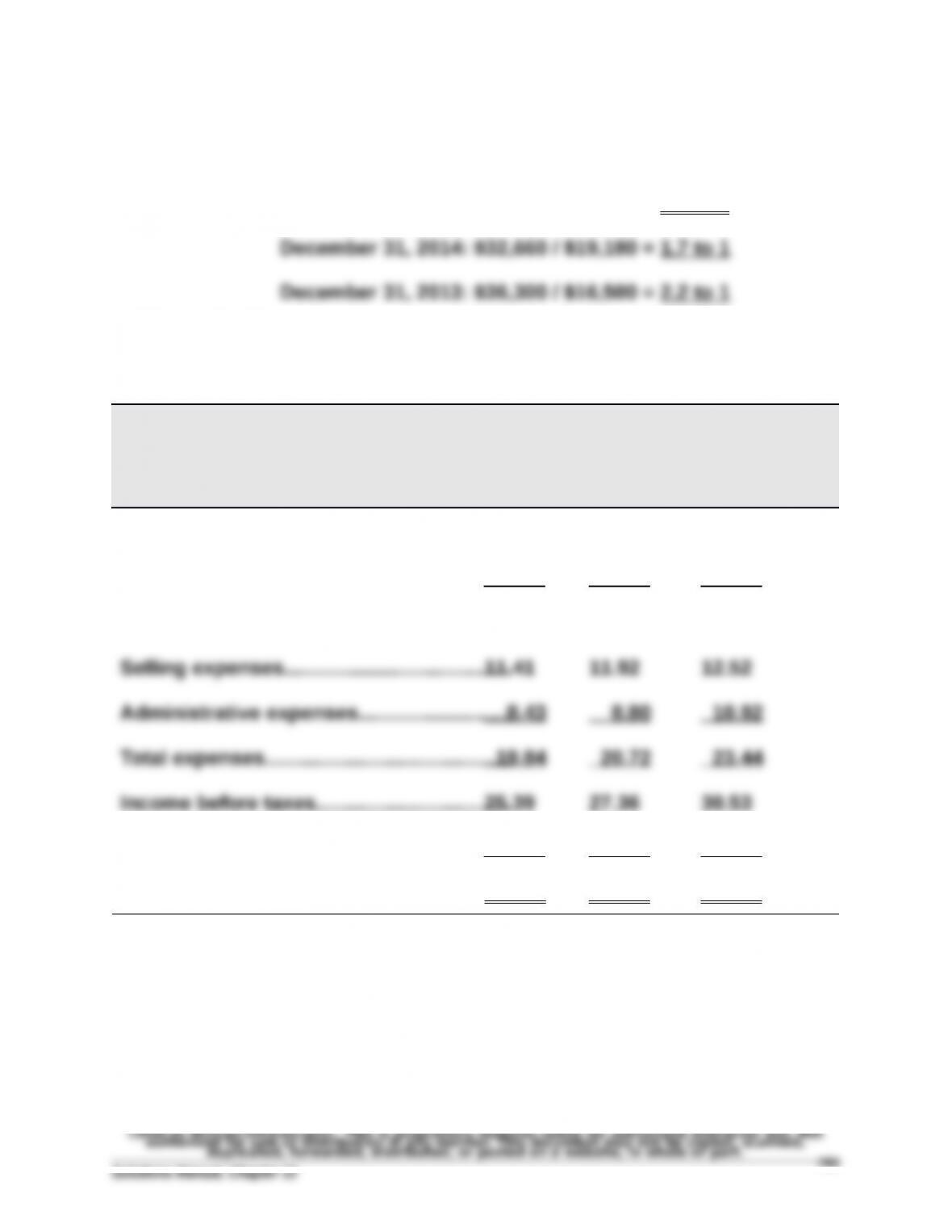

Current ratio: December 31, 2015: $54,860 / $22,370 = 2.5 to 1

Part 2

BLUEGRASS CORPORATION

Common-Size Comparative Income Statements

For Years Ended December 31, 2015, 2014, and 2013

2015 2014 2013

Sales……………..……………………..……….….…100.00% 100.00% 100.00%

Cost of goods sold………….………………..…. 54.77 51.91 46.04

Gross profit…………………………………………. 45.23 48.09 53.96

Income taxes………………..….…….…….….…. 3.04 3.56 3.69

Net income……………..………………………..…. 22.34 % 23.80 % 26.84 %

* Some totals do not reconcile due to rounding.

Problem 13-2B (Concluded)

Part 3

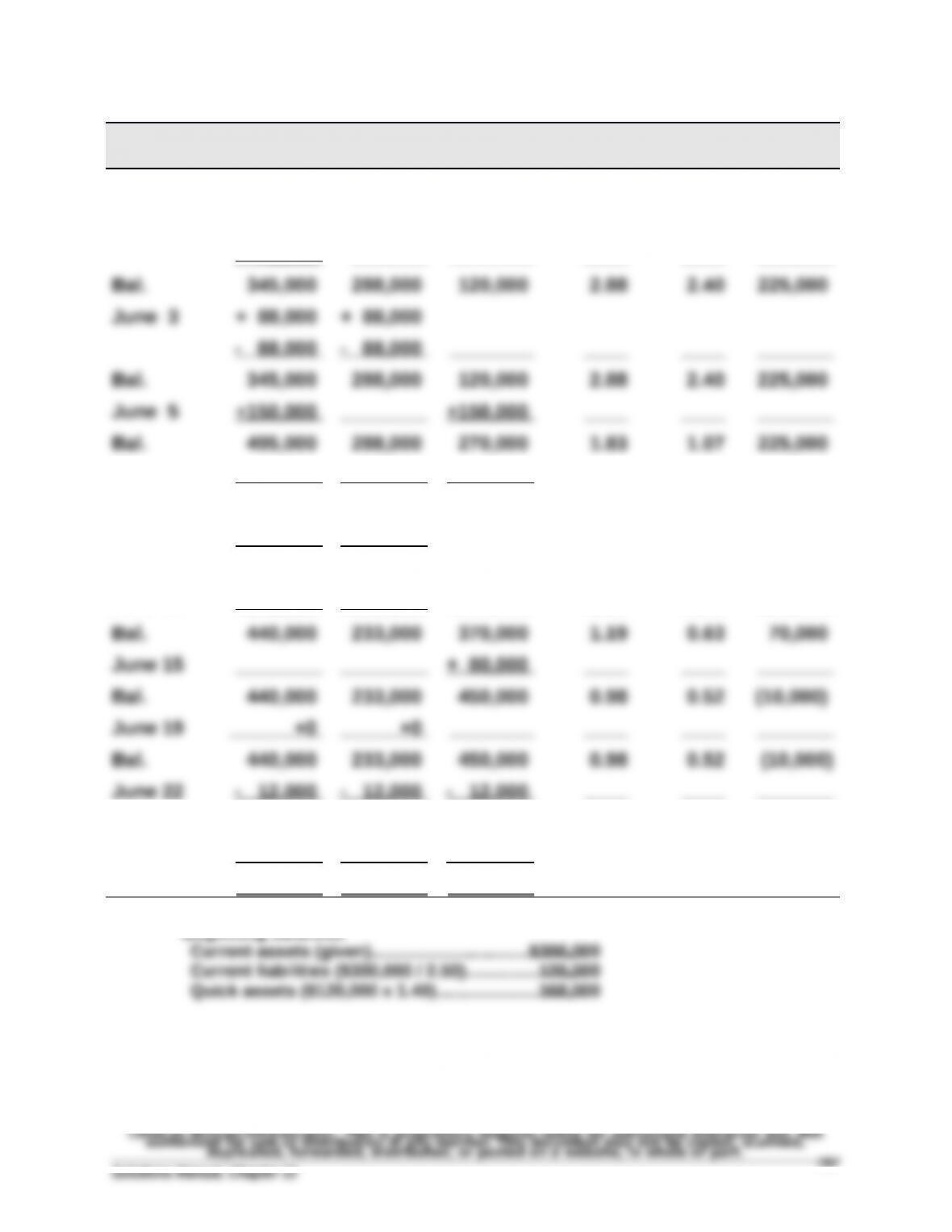

BLUEGRASS CORPORATION

Balance Sheet Data in Trend Percents

December 31, 2015, 2014, and 2013

2015 2014 2013

Assets

Current assets………..………………..….….…..151.13% 89.97% 100.00%

Long-term investments…..….…….…….…...0.00 16.04 100.00

Plant assets……………..……….….………..……142.80 143.87 100.00

Total assets………………………….………………133.18 117.57 100.00

Liabilities and Equity

Part 4

Significant relations revealed

Bluegrass’s cost of goods sold took a larger percent of sales each year.

Selling and administrative expenses and income taxes took a somewhat

smaller portion each year, but not enough to offset the effect of cost of

goods sold. As a result, income became a smaller percent of sales each

year.

Financial and Managerial Accounting, 6th Edition

Problem 13-3B (60 minutes)

Trans-

action

Current

Assets

Quick

Assets

Current

Liabilities

Current

Ratio

Acid-Test

Ratio

Working

Capital

Beginning* $300,000 $168,000 $120,000 2.50 1.40 $180,000

June 1 +120,000 +120,000

– 75,000 _______ ________ ____ ____ _______

June 7 +100,000 +100,000 +100,000 ____ ____ _______

Bal. 595,000 388,000 370,000 1.61 1.05 225,000

June 10 +120,000 +120,000 _______ ____ ____ _______

Bal. 715,000 508,000 370,000 1.93 1.37 345,000

June 12 – 275,000 – 275,000 ________ ____ ____ _______

Bal. 428,000 221,000 438,000 0.98 0.50 (10,000)

June 30 – 80,000 – 80,000 – 80,000 ____ ____ _______

Bal. $348,000 $141,000 $358,000 0.97 0.39 (10,000)

*Beginning balances

Problem 13-4B (50 minutes)

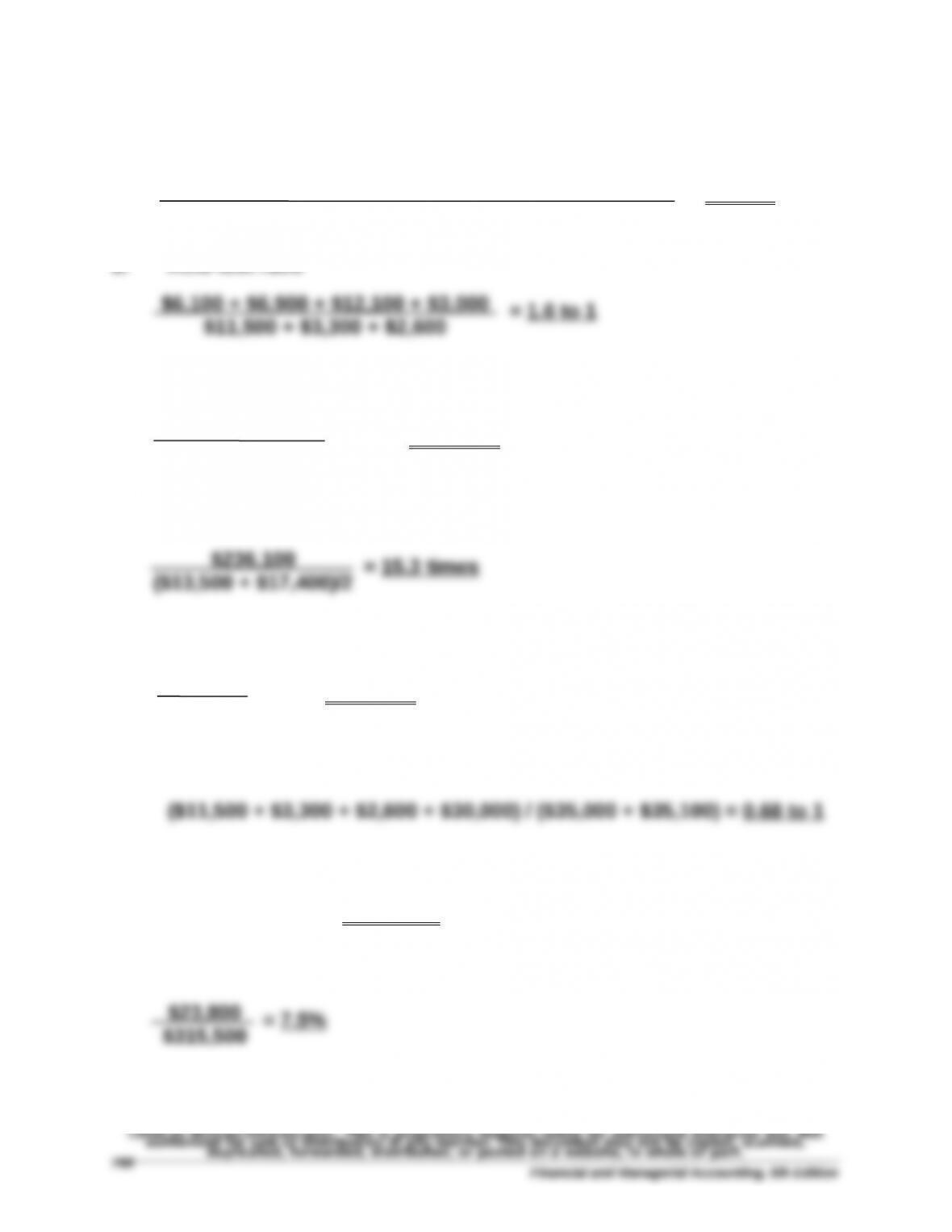

1. Current ratio

= 2.5 to 1

2. Acid-test ratio

3. Days’ sales uncollected

x 365 = 17.5 days

4. Inventory turnover

5. Days’ sales in inventory

x 365 = 20.9 days

6. Debt-to-equity ratio

7. Times interest earned

$30,200 / $2,200 = 13.7 times

8. Profit margin ratio

$6,100 + $6,900 + $12,100 + $3,000 + $13,500 + $2,000

$11,500 + $3,300 + $2,600

$12,100 + $3,000

$315,500

$13,500

$236,100

Problem 13-4B (Concluded)

9. Total asset turnover

10. Return on total assets

= 22.4%

11. Return on common stockholders’ equity

©2016 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not

authorized for sale or distribution in any manner. This document may not be copied, scanned,

duplicated, forwarded, distributed, or posted on a website, in whole or part.

Solutions Manual, Chapter 13

$315,500

($117,500 + $94,900)/2

$23,800

($117,500 + $94,900)/2

769

Problem 13-5B (60 minutes)

Part 1

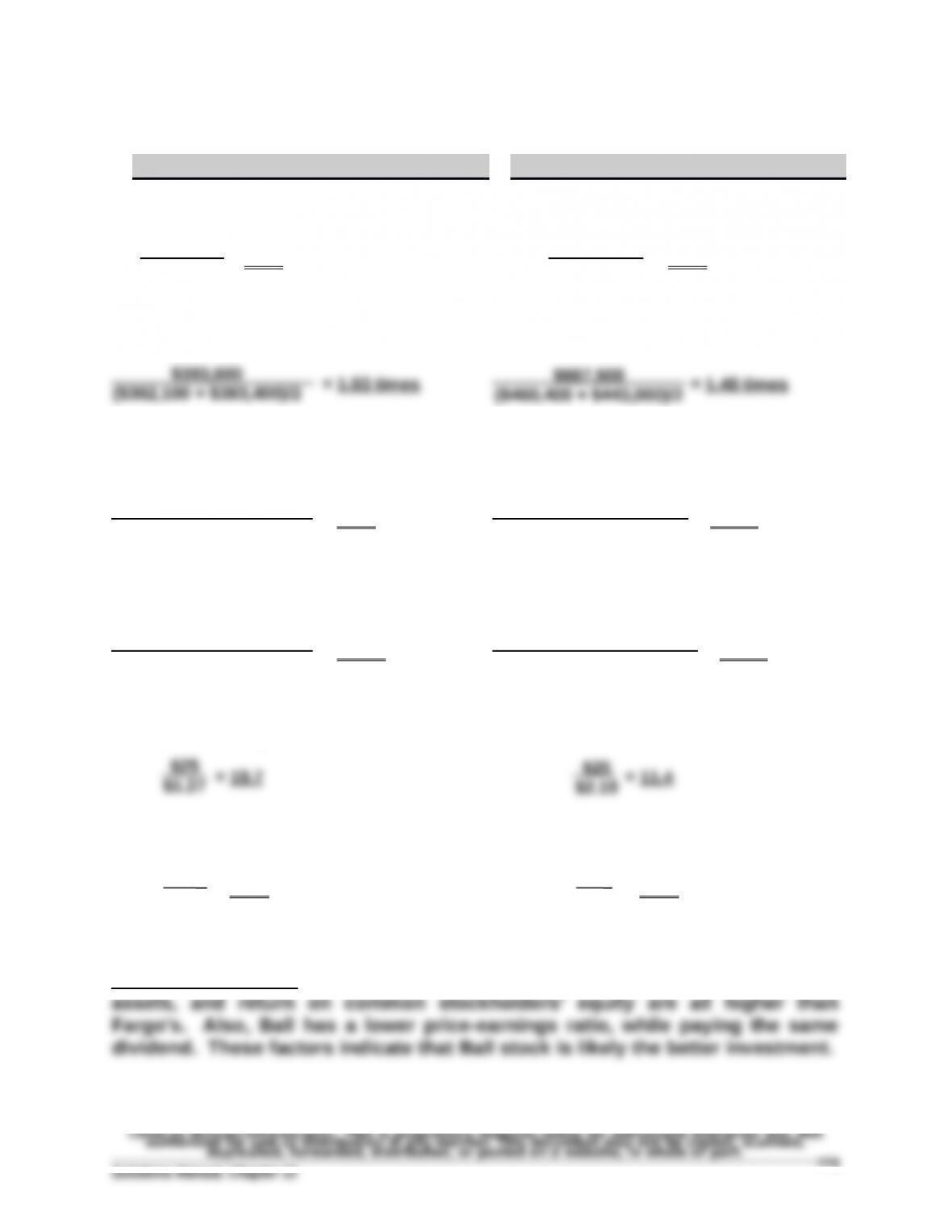

Fargo Company Ball Company

a. Current ratio

b. Acid-test ratio

= 1.2 to 1 = 1.2 to 1

c. Accounts (and notes) receivable turnover

d. Inventory turnover

= 3.0 times = 5.9 times

e. Days’ sales in inventory

f. Days’ sales uncollected

x 365 = 82.3 days x 365 = 43.5 days

Short-term credit risk analysis: Fargo and Ball have nearly equal current

ratios and equal acid-test ratios. However, Ball both turns its merchandise

and collects its accounts receivable much more rapidly than Fargo. On this

basis, Ball probably is the better short-term credit risk.

©2016 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not

authorized for sale or distribution in any manner. This document may not be copied, scanned,

duplicated, forwarded, distributed, or posted on a website, in whole or part.

Financial and Managerial Accounting, 6th Edition

$208,100

$97,000

$205,200

$90,500

$116,000

$97,000

$108,700

$90,500

$480,000

($82,000 + $80,500)/2

$290,600

($86,800 + $105,100)/2

$70,500 + $9,000

$667,500

$77,100 + $11,600

$393,600

Problem 13-5B (Concluded)

Part 2

Fargo Company Ball Company

a. Profit margin ratio

= 8.6% = 9.2%

b. Total asset turnover

c. Return on total assets

= 8.8% = 13.7%

d. Return on common stockholders’ equity

= 17.8% = 23.7%

e. Price-earnings ratio

f. Dividend yield

= 6.0% = 6.0%

Investment analysis: Ball’s profit margin, total asset turnover, return on total

$61,700

$667,500

$33,850

$393,600

$61,700

($460,400 + $443,000)/2

$33,850

($382,100 + $383,400)/2

$61,700

($270,100 + $250,700)/2

$33,850

($198,600 + $182,100)/2

$1.50

$25

$1.50

$25

Problem 13-6BA (60 minutes)

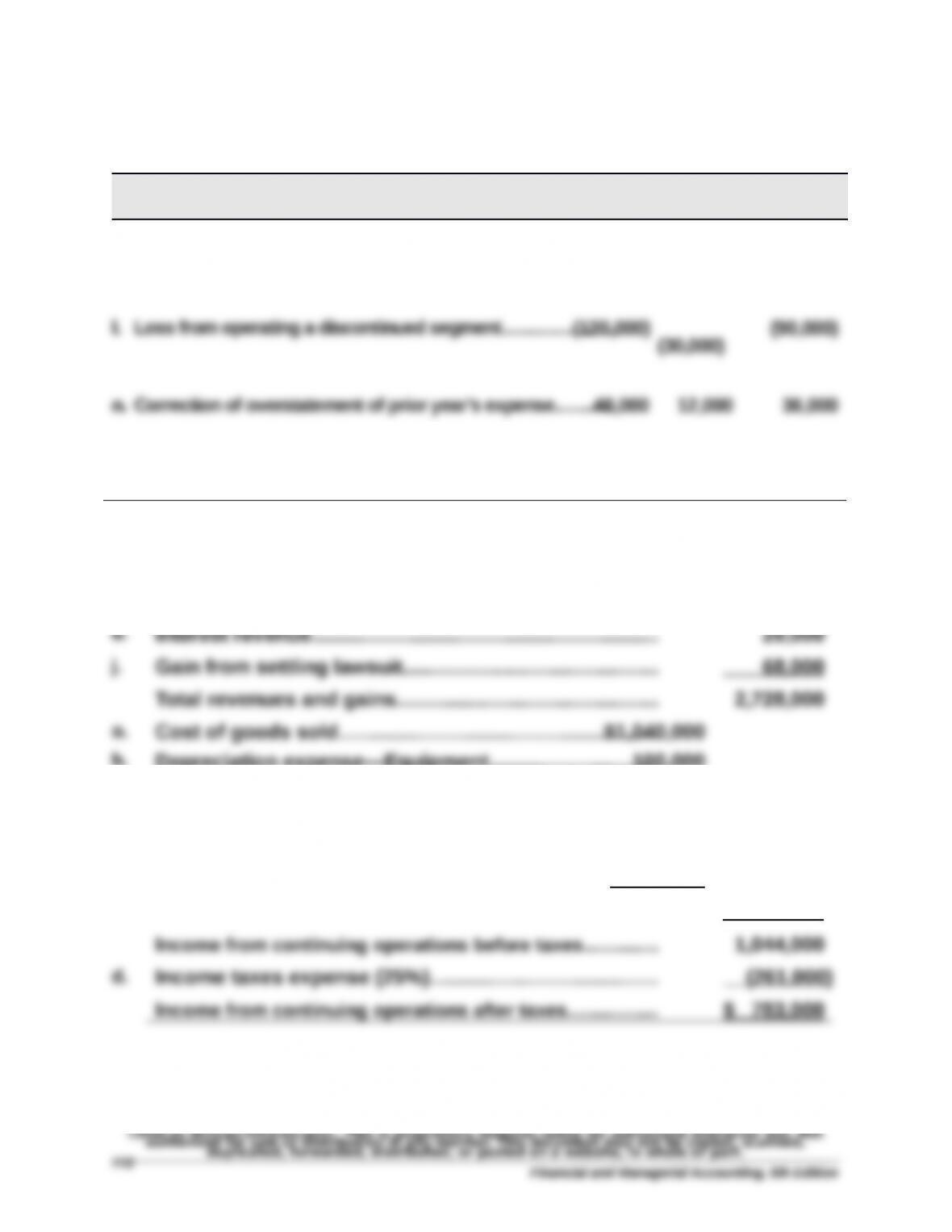

Part 1 Effect of income taxes (debits or losses in parentheses)

Pretax

25% Tax

Effect After-Tax

e. Loss on hurricane damage……………………………....…..….(64,000)

(16,000) (48,000)

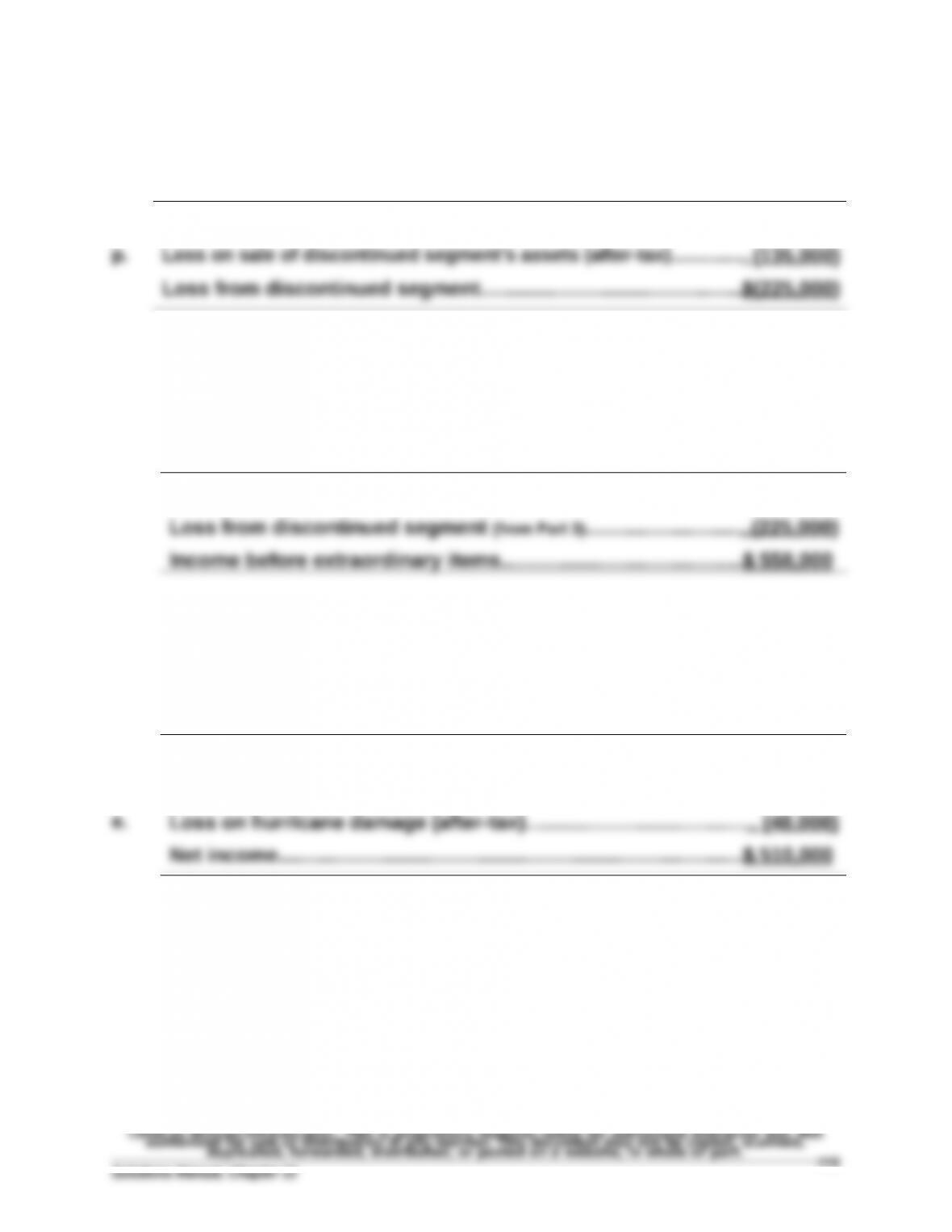

p. Loss on sale of discontinued segment’s assets……………….

(180,000)

(45,000)

(135,000)

Part 2 Income from continuing operations (and its components)

c. Net sales…………….……………………..……………….……….... $2,640,000

h. Depreciation expense—Equipment………………….….….100,000

m. Depreciation expense—Buildings………………….….……156,000

g. Other operating expenses………….……………………….….328,000

k. Loss on sale of equipment…………………………..….……..24,000

i. Loss from settling lawsuit……………………..….….…….…. 36,000

Total expenses and losses…………………………..………... 1,684,000

Financial and Managerial Accounting, 6th Edition

Problem 13-6BA (Concluded)

Part 3 Income from discontinued segment

l. Loss from operating a discontinued segment (after-tax)…...............

$ (90,000)

Part 4 Income before extraordinary items

Income from cont. operations after taxes (from Part 2)………........$ 783,000

Part 5 Net income

Income before extraordinary items……………….….……….…….…..$ 558,000

Extraordinary item: