Chapter Outline Notes

3. Ratios in this block:

a. Profit margin—net income divided by net sales;

describes the ability to earn a net income from sales.

b. Return on total assets—net income divided by average

stockholders’ equity; measures the success of a

company in earning net income for its owners.

D. Market Prospects

1. Market measures are useful for analyzing corporations with

publicly traded stock.

2. Market measures use stock price in their computation.

3. Ratios in this block:

a. Price-earnings ratio—market price per share of common

stock divided by earnings per share; used to evaluate the

profitability of alternative common stock investments.

b. Dividend yield—annual cash dividends paid per share of

stock divided by market price per share; used to compare

the dividend paying performance of different investment

alternatives.

E. Summary of Ratios

Exhibit 13.16 on p. 737 of text sets forth the names of each of the

common ratios by category, and includes the formula and a

description of what is measured by each ratio.

V. Global View—Compares U.S. GAAP to IFRS

A. Horizontal and vertical analyses help eliminate many differences

between U.S. GAAP and IFRS when analyzing and interpreting

financial statements. Percentages are consistently applied across

and within periods. However, where reporting rules differ, users

should exercise caution in drawing conclusions.

B. Ratio analysis has many of the advantages and disadvantages of

horizontal and vertical analysis as mentioned above.

13–7

Chapter Outline Notes

VI. Decision Analysis—Analysis Reporting

1. Executive summary

2. Analysis overview

3. Evidential matter

4. Assumptions

5. Key factors

6. Inferences

VI. Sustainable Income—Appendix 13A—When a revenue and expense

transactions are from normal, continuing operations, a simple income

statement is adequate. When activities include events that are not

normal, it must disclose this information by separating the income

statement into different sections as follows (A-D):

A. Continuing Operations

Reports the revenues, expenses, and income generated by the

company’s continuing operations.

B. Discontinued Segments

1. A business segment is a part of a company’s operations that

serves a particular line of business or class of customers.

2. Section reports:

a. Income (loss) from operating the discontinued business

1. An unusual gain or loss is abnormal or otherwise unrelated to

the company’s regular activities and environment.

2. An infrequent gain or loss is not expected to recur given the

company’s operating environment.

3. Items that are unusual or infrequent, but not both, are reported

in the income statement as part of continuing operations but

below the normal revenues and expenses.

D. Earnings per Share

1. Final section of income statement

2. Reports EPS for three subcategories of income (continuing

operations, discontinued segments, and extraordinary items).

13–8

Chapter Outline Notes

E. Changes in Accounting Principles

1. The consistency principle directs a company to apply the same

accounting principle across periods. Changes from one

accounting principles to another (Example: LIFO to FIFO) are

acceptable if justified as improvements in financial reporting.

2. A footnote would describe change and why it is an

improvement.

3. Requires retrospective application (application of new

accounting principle to prior periods as if that principle had

always been used).

13–9

Alternate Demonstration Problem

Chapter 13

Following are data from the statements of two companies selling similar

products:

Current Year-End Balance Sheets

Sled

Company

Zip

Company

Cash………………………………….…………….………….... $ 11,900 $ 20,000

Notes receivable—short-term………..………….…… 7,700 3,200

Accounts receivable, net……………..……..….……… 42,000 64,000

Inventory………….………………………….…………….…. 58,800 87,680

Prepaid expenses……………………………….…………. 1,680 3,520

Plant and equipment, net……………………………….. 232,120 274,400

Total assets…………………….……………..…….……….. $354,200 $452,800

Current liabilities…………………………………………… $ 56,000 $ 80,000

Mortgage payable………………………………………….. 70,000 80,000

Common stock, $10 par value…………………..……. 140,000 160,000

Retained earnings……………………….…….………….. 88,200 132,800

Total liabilities and stockholders’ equity............ $354,200 $452,800

Data from the Current Year’s Income Statement

Sales……………..…………………….…………..…………… $672,000 $880,000

Cost of goods sold………….………………..…….…….. 528,080 699,840

Interest expense…………..……………………..………… 4,200 5,600

Net income……………..……………………….….………… 23,373 28,896

Beginning-of-Year Data

Inventory………….………………………….…………….…. $ 53,200 $ 85,120

Total assets…………………….……………..…….……….. 345,800 443,200

Stockholders’ equity…………………….…….…….…… 217,000 285,120

Required:

1. Calculate current ratios, acid-test ratios, inventory turnovers, and days’ sales

uncollected for the two companies. Then state which company you think is

the better short-term credit risk and why.

2. Calculate return on total assets employed and return on stockholders’

equity. Then, under the assumption that each company’s stock can be

purchased at book value, state which company’s stock you think is the

better investment and why.

13–10

Solution: Alternate Demonstration Problem

Chapter 13

Part 1

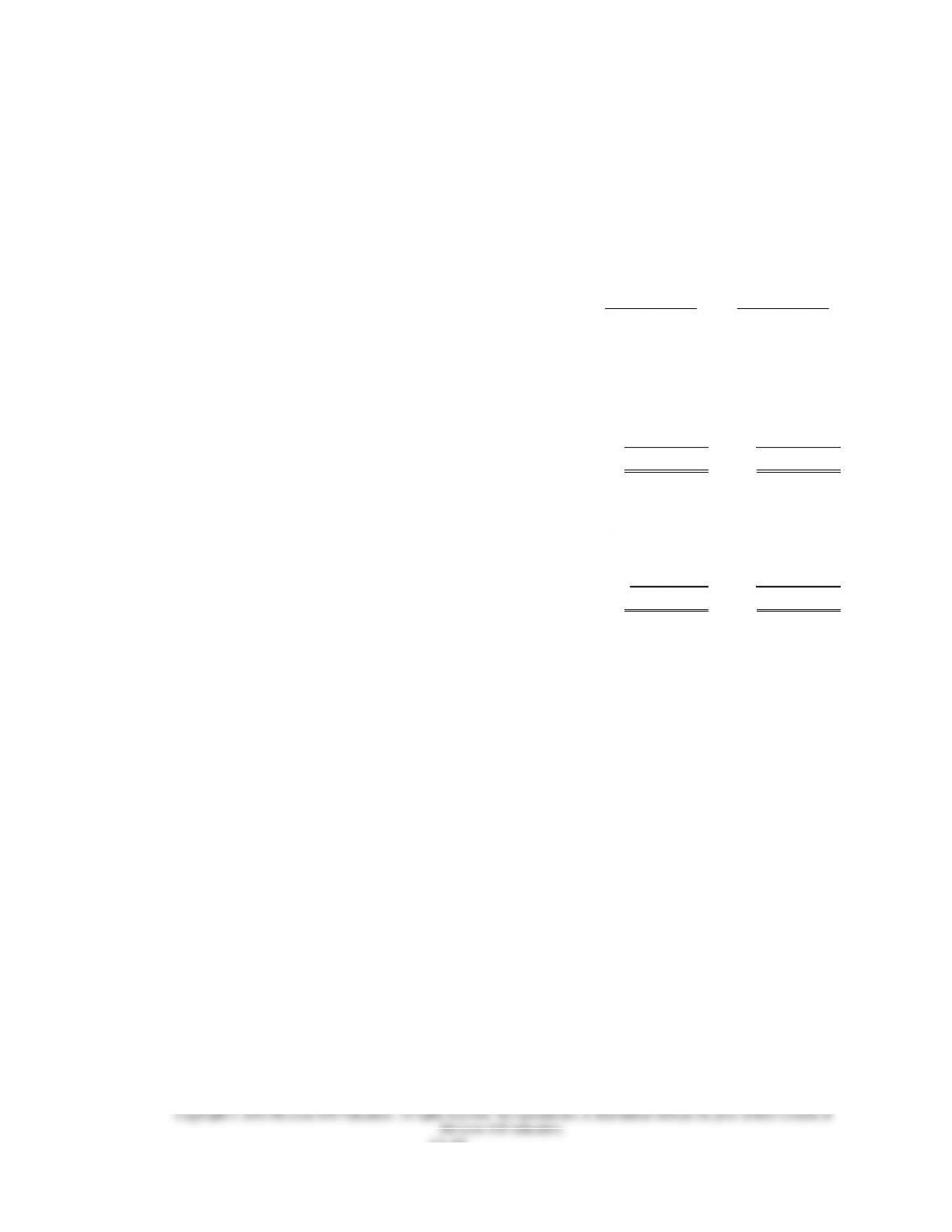

Sled Company Zip Company

Current ratio: $122,080

$ 56,000

= 2.18 to 1 $178,400

$ 80,000

= 2.23 to 1

turnover:

$ 56,000

$ 86,400

Days’ sales

uncollected:

$ 42,000

$672,000

x 365 = 22.8 $ 64,000

$880,000

x 365 = 26.5

Sled Company and Zip Company have almost equal current and acid-test

ratios, so near the same that the differences are not significant. However,

Part 2

Return on total assets: $ 23,373

$350,000 = 6.68% $ 28,896

$448,000 = 6.45%

Assuming that the stock of each company could be purchased at book

value, Sled Company’s stock seems to be the better investment. This

conclusion is based on Sled’s slightly better return on stockholders’ equity

13–11