Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

Problem 10-8BB (Concluded)

Part 4

2015

June 30 Bond Interest Expense..................................................7,940

discount amortization.

2015

Dec. 31 Bond Interest Expense..................................................7,969

Problem 10-9BB (45 minutes)

Part 1

Ten payments of $14,400...........................$144,000

Par value at maturity.................................. 320,000

or:

Ten payments of $14,400...........................$144,000

Part 2

Semiannual

Interest

Period-End

(A)

Cash Interest

Paid

[4.5% x $320,000]

(B)

Bond Interest

Expense

[4% x Prior (E)]

(C)

Premium

Amortization

[(A) - (B)]

(D)

Unamortized

Premium

[Prior (D) - (C)]

(E)

Carrying

Value

[$320,000 + (D)]

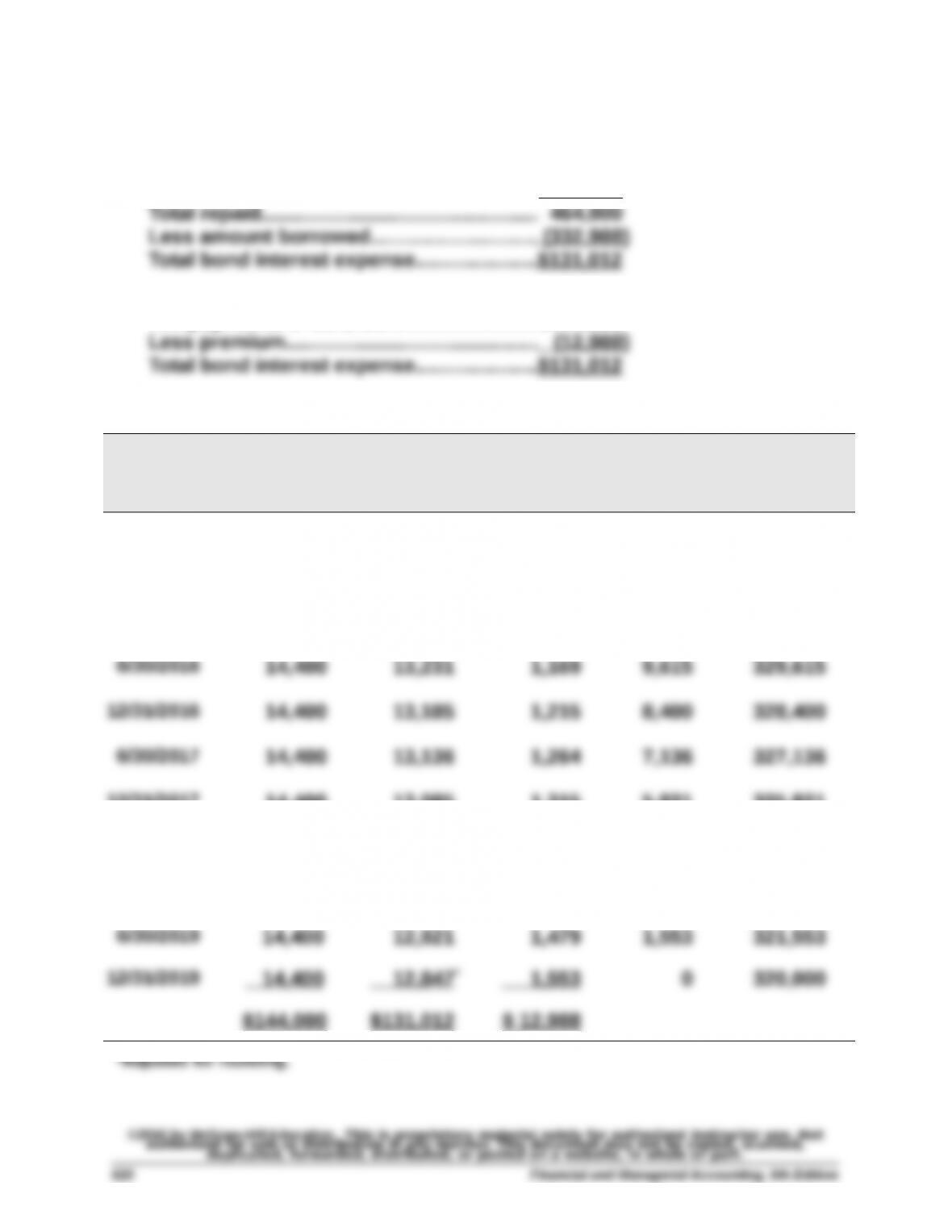

1/01/2015 $12,988 $332,988

6/30/2015 $ 14,400 $ 13,320 $ 1,080 11,908 331,908

12/31/2015 14,400 13,276 1,124 10,784 330,784

12/31/2017 14,400 13,085 1,315 5,821 325,821

6/30/2018 14,400 13,033 1,367 4,454 324,454

12/31/2018 14,400 12,978 1,422 3,032 323,032

Problem 10-9BB (Concluded)

Part 3

2015

June 30 Bond Interest Expense..................................................13,320

premium amortization.

2015

Dec. 31 Bond Interest Expense..................................................13,276

Part 4

As of December 31, 2017

Cash Flow Table Table Value* Amount Present Value

Par value................. B.1 0.8548 $320,000 $273,536

Comparison to Part 2 Table

Except for a small rounding difference, this present value ($325,807) equals

the carrying value of the bonds in column (E) of the amortization table

Problem 10-10BB (70 minutes)

Part 1

2015

Jan. 1 Cash.................................................................................493,608

Sold bonds on stated issue date.

Part 2

Eight payments of $29,250*......................$ 234,000

Par value at maturity.................................. 450,000

Total bond interest expense.....................$ 190,392

*$450,000 x 0.13 x ½ = $29,250

or:

Eight payments of $29,250........................$ 234,000

Part 3

Semiannual

Interest

Period-End

(A)

Cash Interest

Paid

[6.5% x $450,000]

(B)

Bond Interest

Expense

[5% x Prior (E)]

(C)

Premium

Amortization

[(A) - (B)]

(D)

Unamortized

Premium

[Prior (D) - (C)]

(E)

Carrying

Value

[$450,000 + (D)]

1/01/2015 $43,608 $493,608

6/30/2015 $29,250 $24,680 $4,570 39,038 489,038

Problem 10-10BB (Concluded)

Part 4

2015

June 30 Bond Interest Expense..................................................24,680

Premium on Bonds Payable..........................................4,570

2015

Dec. 31 Bond Interest Expense..................................................24,452

Part 5

2017

Jan. 1 Bonds Payable ...............................................................450,000

Premium on Bonds Payable..........................................23,912

Part 6

If the market rate on the issue date had been 14% instead of 10%, the bonds

would have sold at a discount because the contract rate of 13% would have been

lower than the market rate.

been issued at a premium.

The statement of cash flows would show a smaller amount of cash received from

borrowing. However, the cash flow statements presented over the life of the

Problem 10-11BD (35 minutes)

Part 1

Present Value of the Lease Payments

Part 2

Leased Asset—Office Equipment.................................75,816

To record capital lease of office equipment.

Part 3

Capital Lease Liability Payment (Amortization) Schedule

Period

Ending

Date

Beginning

Balance of

Lease

Liability

Interest on

Lease

Liability

(10%)

Reduction

of Lease

Liability

Cash

Lease

Payment

Ending

Balance of

Lease

Liability

Year 1 $75,816 $ 7,582* $12,418 $ 20,000 $63,398

Year 5 18,183 1,817 ** 18,183 20,000 0

$24,184 $75,816 $100,000

* Rounded to nearest dollar.

** Adjusted for prior period rounding errors.

Part 4

Depreciation Expense—Leased Asset, Off. Equip...................15,163

SERIAL PROBLEM — SP 10

Serial Problem — SP 10, Business Solutions (75 minutes)

Part 1

Total equity = $119,393

Thus, total liabilities can be no more than its total equity x 0.8, or

$119,393 x 0.8 = $95,514

Part 2

Assume the secured loan is taken, then the percent of assets financed by:

a. Debt

b. Equity

Part 3

Santana Rey should understand the risks she is taking by borrowing funds

from the bank. She currently has no interest-bearing debt (per prior chapter

serial problems), but the loan will require her to pay interest. The interest

due.

Reporting in Action — BTN 10-1

1. Apple reported long-term debt of $16,960 million as of September 28,

2013.

2. The interest that Apple must pay on $100 million of 4.25% convertible

3. Assuming that Apple had $100 million carrying value of convertible

bonds that convert into 20,000 shares of stock, the following entry

would be recorded upon conversion:

Instructor note: Apple’s stock is no par stock and therefore there is no

4. Answer depends on the financial statement information obtained.