Exercise 10-11 (20 minutes)

2015

2016

Dec. 31 Interest Expense………………..…………………………………..5,423

Notes Payable……………..………………………………………...24,100

Cash…………………………………..…………..……………….. 29,523

To record second installment payment.

2017

Dec. 31 Interest Expense………………..…………………………………..3,736

Notes Payable……………..………………………………………...25,787

Cash…………………………………..…………..……………….. 29,523

To record third installment payment.

2018

Dec. 31 Interest Expense………………..…………………………………..1,933

Exercise 10-12 (15 minutes)

1a. Current debt-to-equity ratio = $220,000 / $400,000* = 0.55

1b. Potential debt-to-equity ratio = $720,000* / $400,000 = 1.80

2. Montclair’s risk will increase because it will have more debt. That debt

(plus interest) must be repaid even if the project does not work out as

Exercise 10-13B (30 minutes)

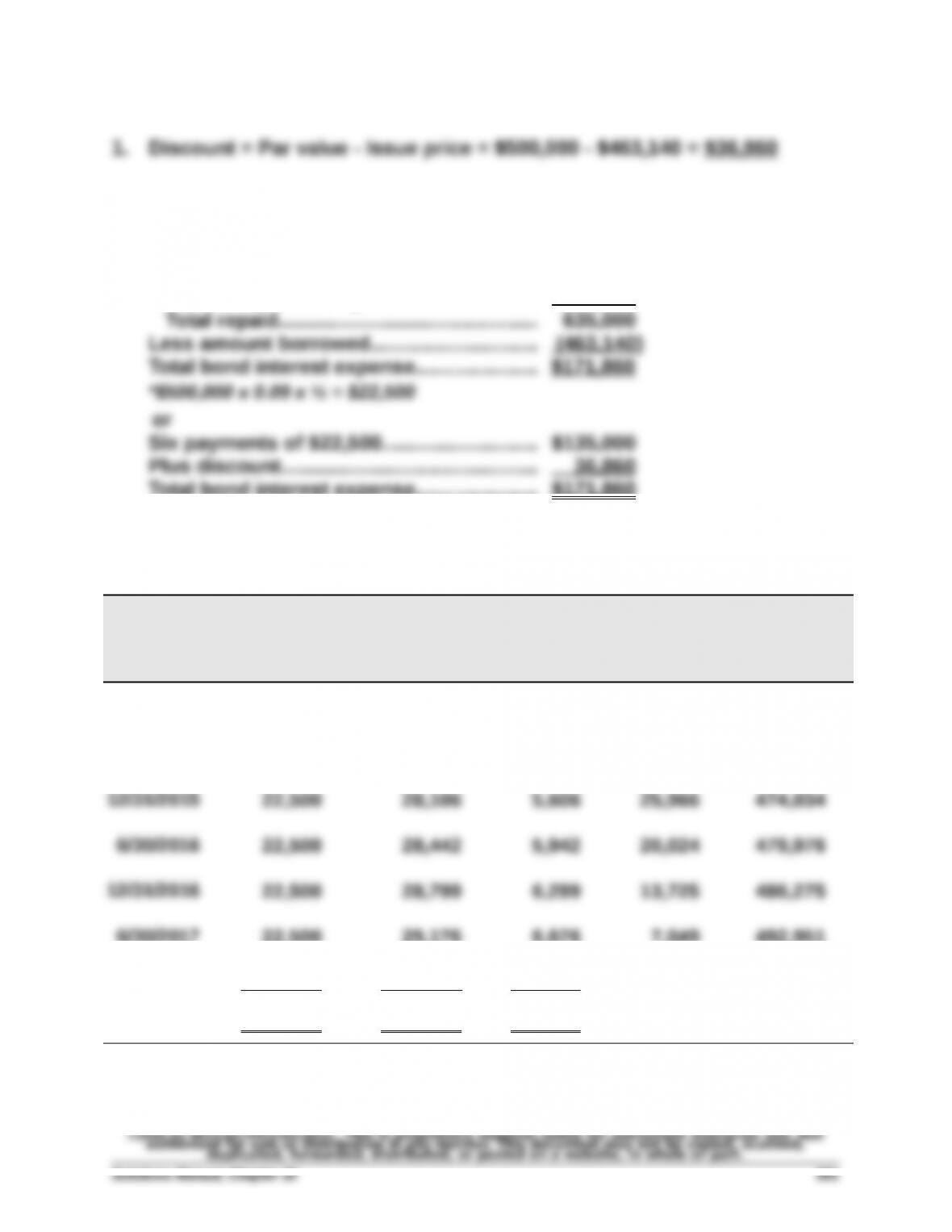

2. Total bond interest expense over the life of the bonds

Amount repaid

Six payments of $22,500*…………….……. $135,000

Par value at maturity………………….……… 500,000

Total bond interest expense……............... $171,860

3. Effective interest amortization table

Semiannual

Interest

Period-End

(A)

Cash Interest

Paid

[4.5% x $500,000]

(B)

Bond Interest

Expense

[6% x Prior (E)]

(C)

Discount

Amortization

[(B) – (A)]

(D)

Unamortized

Discount

[Prior (D) – (C)]

(E)

Carrying

Value

[$500,000 – (D)]

1/01/2015 $36,860 $463,140

6/30/2015 $ 22,500 $ 27,788 $ 5,288 31,572 468,428

6/30/2017 22,500 29,176 6,676 7,049 492,951

12/31/2017 22,500 29,549 * 7,049 0 500,000

$135,000 $171,860 $36,860

*Adjusted for rounding.

Exercise 10-14B (30 minutes)

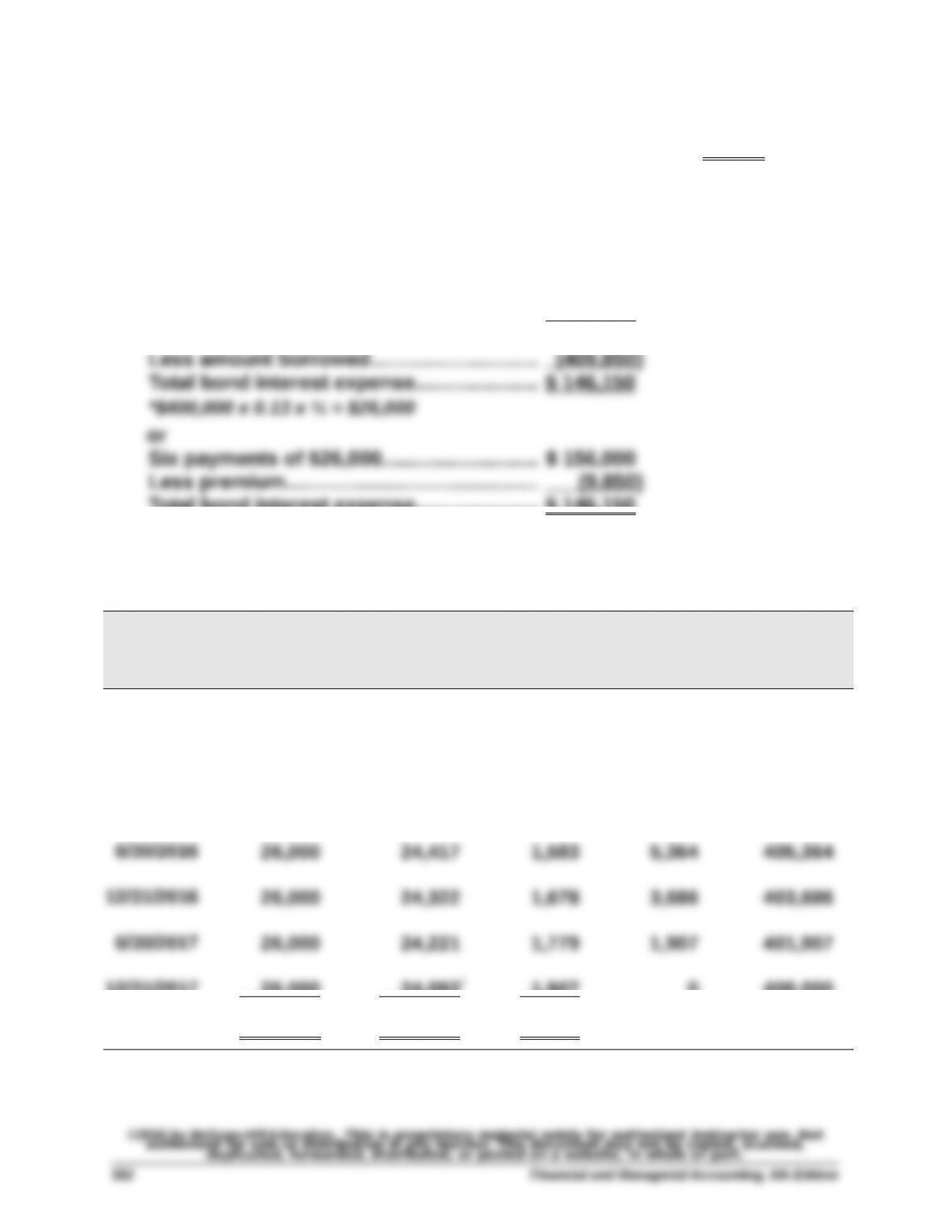

1. Premium = Issue price – Par value = $409,850 – $400,000 = $9,850

2. Total bond interest expense over the life of the bonds

Amount repaid

Six payments of $26,000*…………….……. $ 156,000

Par value at maturity………………….……… 400,000

Total repaid……….…………………….…..…… 556,000

Total bond interest expense……............... $ 146,150

3. Effective interest amortization table

Semiannual

Interest

Period-End

(A)

Cash Interest

Paid

[6.5% x $400,000]

(B)

Bond Interest

Expense

[6% x Prior (E)]

(C)

Premium

Amortization

[(A) – (B)]

(D)

Unamortized

Premium

[Prior (D) – (C)]

(E)

Carrying

Value

[400,000 + (D)]

1/01/2015 $9,850 $409,850

6/30/2015 $ 26,000 $ 24,591 $1,409 8,441 408,441

12/31/2015 26,000 24,506 1,494 6,947 406,947

12/31/2017 26,000 24,093 * 1,907 0 400,000

$156,000 $146,150 $9,850

*Adjusted for rounding.

Exercise 10-15 (40 minutes)

1. Straight-line amortization table (($100,000-$95,948)/8 = $506.5)

Semiannual

Period-End

Unamortized

Discount †

Carrying

Value

6/01/2015….….……....... $4,052 $95,948

11/30/2015….….……….... 3,546 96,454

5/31/2016….….……....... 3,040 96,960

11/30/2016….….……….... 2,534 97,466

5/31/2019….….……....... 0 100,000

* Adjusted for rounding difference.

† Supporting computations

Eight payments of $3,500**…...…………... $ 28,000

Par value at maturity………………………….. 100,000

Total repaid………………………………..…...… 128,000

Less amount borrowed….………..……...... (95,948 )

Semiannual straight-line interest expense = $32,052 / 8 = $4,006 (rounded)

2.

2015

Nov. 30 Bond Interest Expense………………………………….……….4,006

Dec. 31 Bond Interest Expense……………..…..….………….……….. 668

Discount on Bonds Payable…………….……………..… 84

2016

May 31 Interest Payable………………….……………….…………..……. 584

Bond Interest Expense……………..…..……….….…………..3,338

the accrued interest liability.

Exercise 10-16C (20 minutes)

1. Semiannual cash interest payment = $3,400,000 x 9% x ½ year = $153,000

2. Journal entries

2015

May 1 Cash………………………..…………….…………………..……….…3,502,000

Interest Payable…………….…………….…………………... 102,000

Sold bonds with 4 months’ accrued interest.

June 30 Interest Payable……………………….……………….…….……..102,000

Dec. 31 Bond Interest Expense…………………….…….………….…..153,000

Cash…………………………………..…………..……………….. 153,000

Paid semiannual interest on the bonds.

Exercise 10-17D (10 minutes)

Exercise 10-18D (20 minutes)

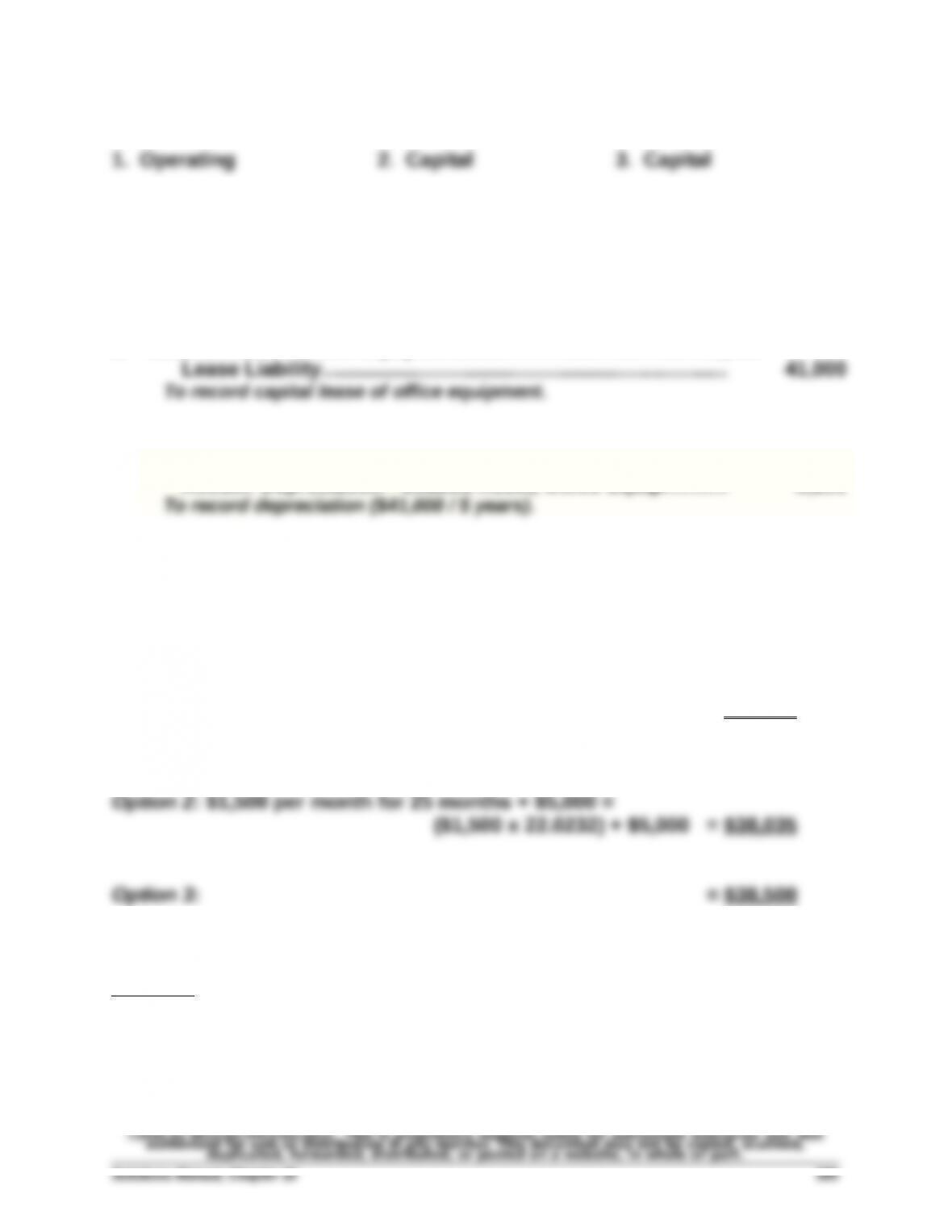

1. Leased Asset—Office Equipment………………..….…………….……41,000

2. Depreciation Expense—Leased Asset, Office Equip…............8,200

Accum. Depreciation—Leased Asset, Office Equip........... 8,200

Exercise 10-19D (15 minutes)

[Note: 12% / 12 months = 1% per month as the relevant interest rate.]

Option 1: $1,750 per month for 25 months = $1,750 x 22.0232 = $38,541

Analysis: Option 2 has the lowest present value at $38,035 and, thus, is the

best lease deal for the customer.

Exercise 10-20 (20 minutes)

(amounts in euros millions)

1. Cash……………………………………………..………………………. 1,663

2. Loans and Borrowings…………………..….….……….……… 2,400

Premium on Loans and Borrowings…………….…………. 24

Retirement of loans and borrowings pre-maturity.

3. Heineken’s Loans and Borrowings carried a premium of €112 as of

4. The contract rate was higher than the market rate at issuance. This is

(Recall: Contract rate > Market rate Premium)

PROBLEM SET A

Problem 10-1A (50 minutes)

Part 1

a.

Cash Flow Table Table Value* Amount Present Value

Par value….……….…..... B.1 0.4564 $40,000 $18,256

Interest (annuity)......... B.3 13.5903 2,000** 27,181

Price of bonds...........

$45,437

Bond premium…………. $ 5,437

* Table values are based on a discount rate of 4% (half the annual market rate) and 20

periods (semiannual payments).

** $40,000 x 0.10 x ½ = $2,000

b.

2015

Jan. 1 Cash……………………………………………………………………...45,437

Part 2

a.

Cash Flow Table Table Value* Amount Present Value

Par value….……….…..... B.1 0.3769 $40,000 $15,076

same, the bonds sell at par and there is no discount or premium.)

b.

2015

Jan. 1 Cash……………………………………………………………………...40,000

Bonds Payable……………..…………….……………………. 40,000

Sold bonds on stated issue date.

Problem 10-1A (Concluded)

Part 3

a.

Cash Flow Table Table Value* Amount Present Value

Par value……..….……… B.1 0.3118 $40,000 $12,472

periods (semiannual payments).

b.

2015

Jan. 1 Cash……………………………………………………………………...35,412